Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

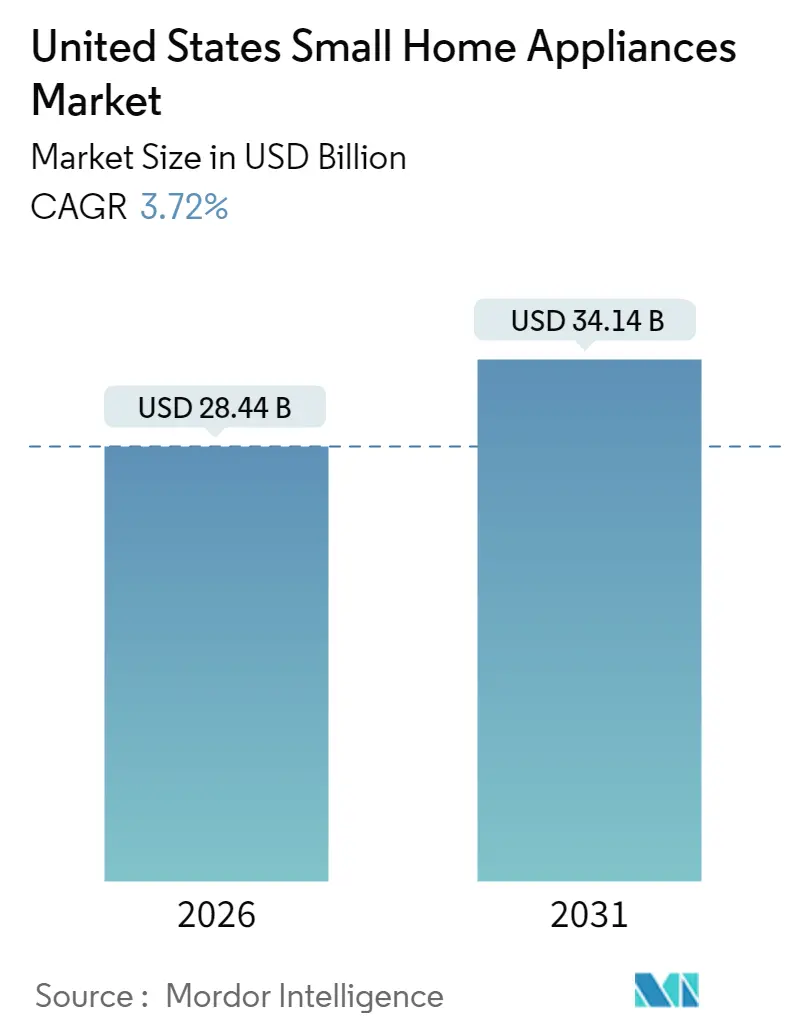

| Market Size (2026) | USD 28.44 Billion |

| Market Size (2031) | USD 34.14 Billion |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Small Home Appliances Market Analysis by Mordor Intelligence

The United States small home appliances market is expected to grow from USD 27.42 billion in 2025 to USD 28.44 billion in 2026 and is forecast to reach USD 34.14 billion by 2031 at 3.72% CAGR over 2026-2031. Steady growth reflects a marketplace where energy-efficiency rules, digital connectivity, and tariff-driven cost dynamics now shape product roadmaps more than sheer volume gains. Federal energy-conservation standards, particularly the Department of Energy’s newly finalized cooking-product rules effective January 2028, are spurring R&D investment aimed at reducing kilowatt-hour consumption while preserving performance[1]U.S. Department of Energy, “Energy Conservation Standards for Cooking Products,” energy.gov . Rapid smart-appliance adoption, aided by common protocols such as Matter 1.4, is moving connectivity from novelty to baseline expectation and enabling premium pricing tiers[2]Qual¬comm, “Matter 1.4 and the Future of Smart Home Interoperability,” qualcomm.com. E-commerce acceleration is widening manufacturer margins through direct-to-consumer (DTC) channels while lowering average transaction prices for shoppers.

Key Report Takeaways

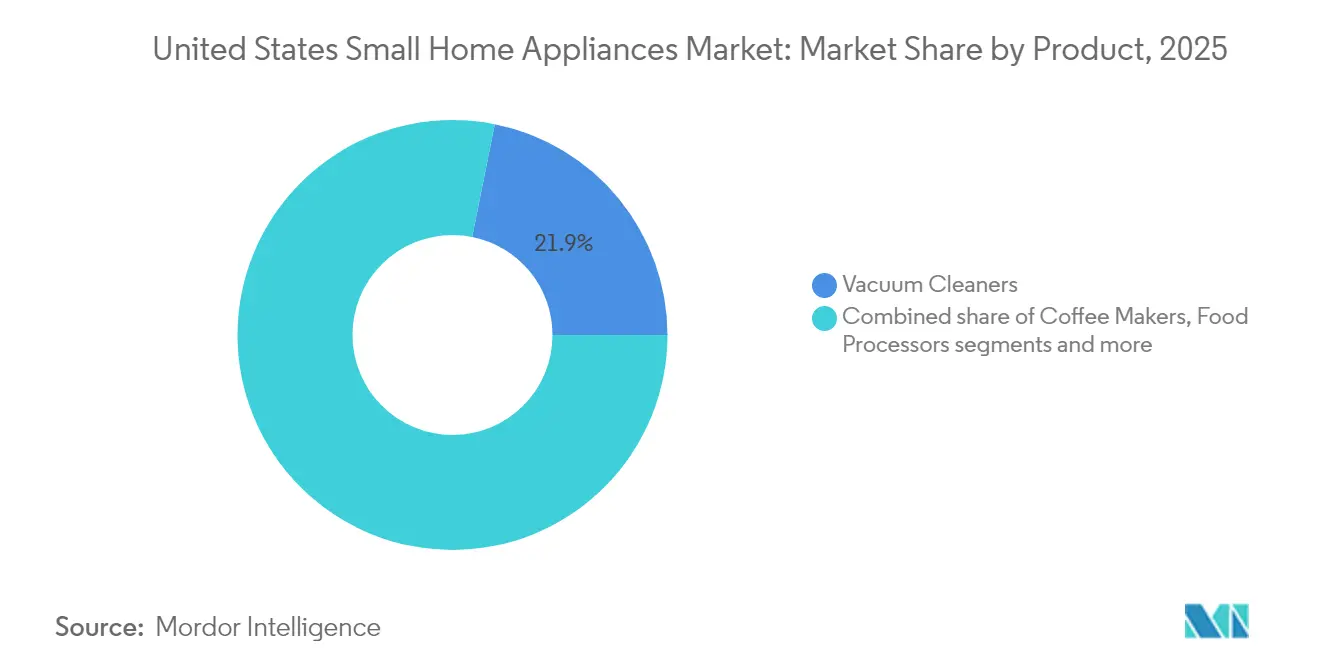

- By product, vacuum cleaners held 21.85% of the US small home appliances market size in 2025; air fryers headline growth with a 7.35% CAGR to 2031.

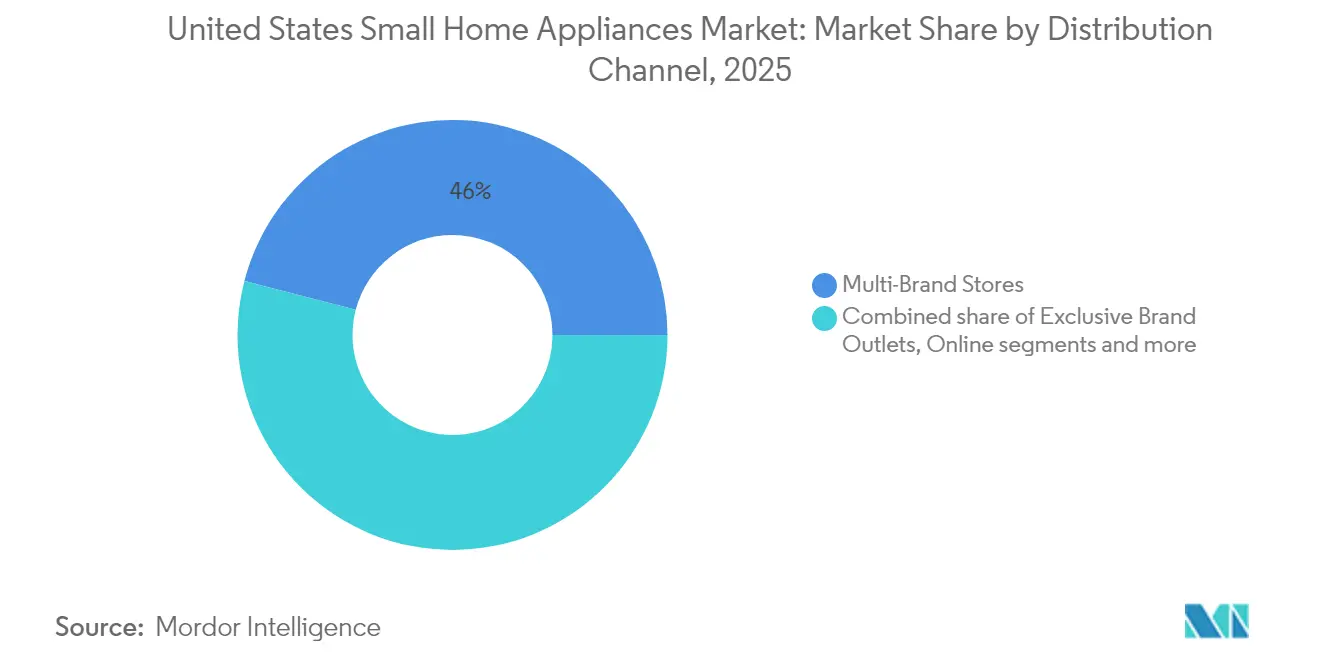

- By distribution channel, multi-brand stores led with a 45.95% of the US small home appliances market share in 2025, while online sales expanded at a 6.05% CAGR through 2031.

- By geography, the Southeast captured 33.45% of 2025 revenue; the West registers the fastest 4.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Small Home Appliances Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency regulations and utility-cost awareness | +0.8% | California, Northeast | Medium term (2–4 years) |

| Rapid adoption of smart and connected appliances | +1.2% | West Coast, urban centers nationwide | Long term (≥ 4 years) |

| Expansion of e-commerce and DTC models | +0.6% | Suburban markets nationwide | Short term (≤ 2 years) |

| Housing starts, renovation boom, and replacement cycles | +0.9% | Southeast, West | Medium term (2–4 years) |

| Growing disposable income, changing lifestyles, and urbanization | +0.5% | Metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Energy-Efficiency Regulations and Utility-Cost Awareness

Federal appliance standards are shortening innovation cycles as vendors redesign platforms to meet lower kilowatt-hour ceilings while maintaining price points that satisfy value-oriented shoppers. The Department of Energy projects its latest water-heater rules will trim US energy use by 17.6 quadrillion Btu over 30 years, underscoring the payoff for high-efficiency compressors and heat-pump integrations[3]Federal Register, “Energy Conservation Program: Energy Conservation Standards for Dishwashers,” federalregister.gov. Dishwasher caps of 223 kWh per year from April 2027 further accelerate the adoption of brushless motors and proprietary heat-recovery modules, prompting system-level design around kitchen ecosystems rather than single units. California’s above-average electricity tariffs heighten consumer payback scrutiny, letting brands with credible Energy Star labels lift average selling prices without eroding demand. Parallel rules for commercial walk-in coolers spill upstream to residential suppliers that share evaporator and insulation sourcing, reinforcing scale advantages for vertically integrated producers.

Rapid Adoption of Smart and Connected Appliances

According to Houzz's "2024 U.S. Kitchen Trends Study," connected appliances penetration reached 30% of US kitchen renovations in 2024, and Wi-Fi is now table stakes, not an upsell. Samsung’s 2025 Bespoke AI range, equipped with 9-inch screens and food-recognition vision, illustrates how embedded intelligence commands premium shelf placement and lifts attachment rates for companion apps. GE Appliances’ SmartHQ platform provisions predictive-maintenance alerts that reduce warranty claims and stimulate aftermarket part sales[4]GE Appliances, “AI-Powered Kitchen Innovations Announced February 2025,” geappliances.com. Interoperability progress under Matter 1.4 reduces consumer risk of ecosystem lock-in, while on-device AI sidesteps privacy pushback linked to cloud-based data retention. Yet advanced mapping in robotic vacuums has drawn scrutiny from privacy advocates, signaling that feature depth must remain balanced against data-security assurances to preserve adoption momentum.

Expansion of E-Commerce and Direct-to-Consumer Models

Digital channels cemented structural gains that emerged during pandemic shutdowns, with 45% of small-appliance buyers now initiating purchase journeys online. DTC strategies yield higher gross margins by bypassing retail slotting fees; SharkNinja’s 2024 net-sales jump of 30%—propelled by optimized search ads and social-commerce tie-ins—illustrates earnings leverage when traffic shifts to proprietary storefronts. Price transparency and dynamic discounting pull average e-commerce selling prices below in-store benchmarks, increasing category penetration among price-sensitive households. Virtual showrooms, augmented-reality placement tools, and live-stream demos now replicate tactile assessment barriers once unique to brick-and-mortar.

Growing Disposable Income, Changing Lifestyles, and Urbanization

Sustained wage gains and moderating inflation keep discretionary budgets intact, supporting substitution from manual to automated solutions even in a maturing US small home appliances market. The share of one-person households continues to climb, favoring compact multifunction devices such as air-fryer-toaster hybrids that optimize counter real estate. Viral social-media recipes, notably on TikTok and Instagram Reels, have catapulted air fryers to mainstream status, creating knock-on demand for pre-packaged meal components optimized for the format. Millennials typically accept higher price tags for connectivity, while Gen Z values low-friction convenience; both demographics enter peak household-formation years, sustaining demand for feature-rich models that promise time savings and healthier cooking.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw materials and semiconductor pricing | −0.7% | Global, import-dependent manufacturers | Short term (≤ 2 years) |

| Supply-chain disruptions and freight-cost pressures | −0.5% | West Coast ports, national logistics | Medium term (2–4 years) |

| Intensifying price competition and private-label expansion | −0.4% | Value-oriented retail channels | Long term (≥ 4 years) |

| Right-to-repair legislation extending product lifecycles | −0.3% | California, Minnesota | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile raw materials and semiconductor pricing

Copper trading above USD 10,000 per metric ton inflates refrigeration-circuit costs by up to 4.2%, forcing OEMs to pursue hedging or redesign evaporator geometries to reduce metal load factors. Global chip shortfalls continue to delay launch calendars for feature-laden models, prolonging SKUs based on legacy microcontrollers and throttling innovation cadence. Steel-based appliance tariffs of 50% effective June 2025, close former import-arbitrage windows and amplify cost inflation that outpaces household wage growth, risking price-driven demand pullbacks.

Supply-chain disruptions and freight-cost pressures

Consecutive 25% levies on Canadian and Mexican imports compel brands such as Bosch and Samsung to reroute component flows, incurring transitional inventory spikes and capital expenditures for North American capacity. Port congestion intermittently snarls inbound shipments, undermining just-in-time models and prompting inventory buffers that tie up working capital. Labor constraints in logistics and assembly—exacerbated by tighter immigration policies—extend lead times, with ripple effects most acute in vacuum-cleaner motors and food-processor gearboxes that rely on high-touch machining. OEM responses include near-shoring of plastics molding and regionalized distribution hubs, but interim duplication of production footprints raises per-unit conversion costs until volume scale catches up.

Segment Analysis

By Product: Air fryers Transform Kitchen Dynamics

Vacuum cleaners preserve the largest 21.85% share, yet robotic entrants backed by aggressive Chinese pricing pressure are squeezing margins, prompting incumbents to layer navigation AI and subscription consumables to stabilize revenues. Air fryers generated the fastest 7.35% CAGR through 2031 as consumers pursued healthier cooking that mimics deep-fried textures without submerging food in oil. The US small home appliances market size for air fryers is projected to grow significantly by 2030, illustrating how a formerly niche tool became central to weeknight meal prep. Food companies now co-develop SKUs engineered for air-fryer performance, while appliance makers incorporate dual-basket designs and app-based recipe platforms to extend usage occasions.

Coffee makers and electric kettles benefit from premiumization as consumers chase café-quality extraction at home. Specialty espresso units with PID-controlled boilers and smartphone telemetry lift attachment sales of branded beans and descaling kits. Food processors and blenders see brand consolidation. Countertop ovens now bundle air-fry and dehydration modes, dissolving historical product silos and encouraging modular component sourcing. The residual “other” segment—waffle irons, mini-rice cookers, niche sous-vide sticks—leverages social-media micro-trends, yielding burst demand cycles that savvy suppliers satisfy via limited-run drops through DTC storefronts.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Online Acceleration Reshapes Retail

Multi-brand stores remained primary, holding 45.95% of 2025 revenue, as wide assortments and instant-take-home appeal to shoppers equipped new properties. Even so, the online pathway’s 6.05% CAGR through 2031 outpaces all offline formats, powered by persistent convenience and broadened acceptance of virtual try-before-you-buy tools. Average digital basket sizes benefit from algorithmic cross-selling (filters for compatible accessories) that brick-and-mortar staff cannot replicate at scale. Exclusive brand outlets face cannibalization as manufacturers escalate DTC pushes that furnish first-party data streams, fueling agile product development. Warehouse clubs and specialty retailers defend their share by layering installation, haul-away, and extended-service packages that digital‐only rivals seldom match. Omnichannel fulfillment options—order online, pick up in store—now function as table stakes, requiring unified inventory visibility and consistent pricing to avoid consumer backlash.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Southeast anchored 33.45% of 2025 sales, lifted by inbound population migration and robust single-family housing starts across Florida, Georgia, and North Carolina. Strong retail footprints for Home Depot and Lowe’s streamline product availability, while comparatively lower utility rates ease the payoff hurdle for mid-tier efficiency models. Appliance bundles tied to builder packages gain traction as regional construction firms embed turnkey kitchen and laundry sets into closing contracts, supporting volume incentives for large OEMs.

The West commands the fastest 4.92% CAGR through 2031, propelled by tech-savvy households in California, Washington, and Colorado that over-index on smart-home adoption. Mountain-state infrastructure investment fuels above-average electrical supply growth, with Nevada reporting 10% and Montana 8% uptick, both translating into retail appliance demand. Metropolitan real-estate constraints drive the popularity of convertible countertop products, while suburban clusters maintain an appetite for full-capacity dishwashers and high-output ranges.

The Northeast and Midwest offer mature but dependable revenue streams. The Northeast’s aging housing stock forces cyclical replacements, and high kilowatt-hour prices boost demand for Energy Star dishwashers despite colder winters that elevate household heating bills. Major universities catalyze early adoption of Wi-Fi-enabled equipment through research partnerships, seeding broader consumer familiarity. The Midwest, meanwhile, combines stable employment with value orientation; mass retailers flourish, yet premium-brand showrooms in cities like Chicago attract upwardly mobile buyers. The Southwest straddles both dynamics: growth hubs such as Phoenix and Austin replicate West Coast tech preferences, whereas rural counties gravitate toward price-focused multipurpose appliances.

Competitive Landscape

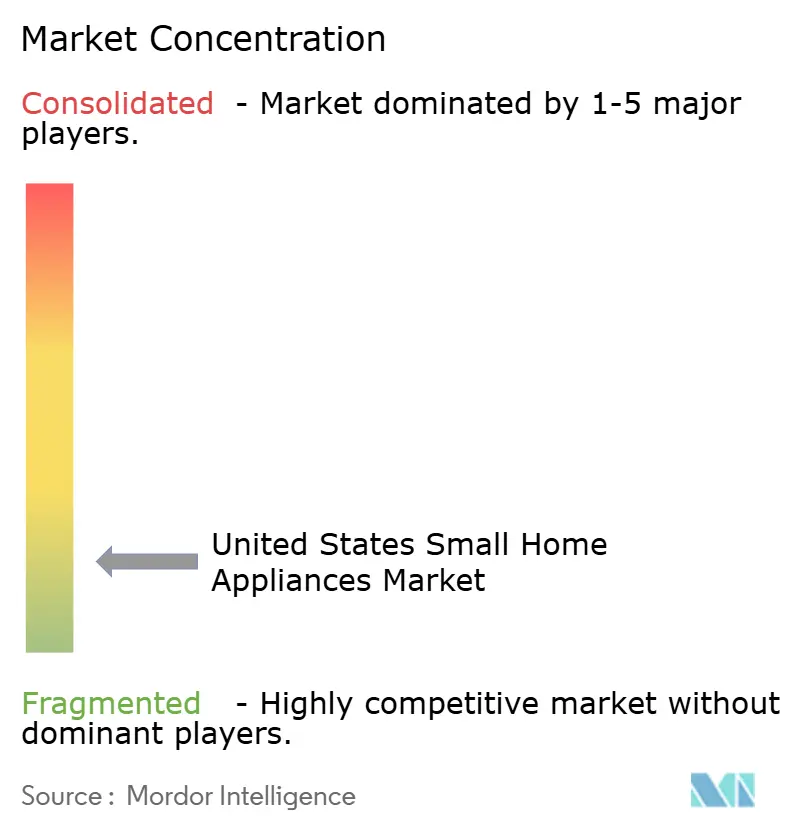

The US small home appliances market remains fragmented, though category-specific concentration differs sharply. SharkNinja’s 2024 revenue reached USD 5.53 billion, a 30% leap credited to ice-cream makers and blenders that tap viral at-home beverage trends [5]SharkNinja Holdings, “Q4 2024 Earnings Release,” investor.sharkninja.com. iRobot’s share erosion—from 22.3% to 13.7%—illustrates disruption risk when fast-follower Chinese entrants undercut pricing with acceptable performance.

Technology leadership drives out-performance: Samsung grabbed a significant share of US robot-vacuum unit sales within two launch cycles, leveraging edge-derived room-mapping and cross-device integration via SmartThings. Private-label encroachment by retailers like Target and Costco compresses mid-tier margins.

Strategic responses include near-shoring component plants to blunt tariff shocks, forging semiconductor allocation agreements, and acquiring niche IP (e.g., advanced air-fry heating elements) to accelerate feature backlog delivery. ESG commitments around recycled plastics and repairability guidelines showcase brand differentiation in sustainability-minded cohorts, while alliances with recipe-content platforms broaden value-chain reach beyond hardware into digital services.

United States Small Home Appliances Industry Leaders

SharkNinja Operating LLC

Hamilton Beach Brands Holding Company

Dyson Ltd.

Keurig Dr Pepper Inc.

Breville Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Samsung introduced its 2025 Bespoke AI lineup featuring 9-inch displays, food-recognition vision, and Knox Matrix security.

- February 2025: SharkNinja posted Q4 2024 net sales of USD 1.79 billion, up 29.7%, with 89% growth in food-prep appliances up from USD 1.3 billion in the same period last year.. This uptick in net sales was driven by growth across all its product categories, with food preparation appliances leading the charge, boasting an impressive growth of nearly 90%.

- July 2024: Haden expanded its US coffeemaker line with precision-brew models.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States small home appliances market as the annual value generated from new, plug-in or battery-powered portable devices used for routine cooking, cleaning, air treatment, and personal care tasks (examples include coffee makers, air fryers, vacuum cleaners, humidifiers, and electric shavers). The definition aligns with NAICS 335210 and excludes major "white-goods," consumer electronics, and manual utensils.

Scope exclusion: Large stationary appliances (refrigerators, ranges, washers, HVAC units) and purely mechanical gadgets are outside this assessment.

Segmentation Overview

- By Product

- Coffee Makers

- Food Processors

- Grills and Roasters

- Electric Kettles

- Juicers and Blenders

- Air Fryers

- Vacuum Cleaners

- Toasters

- Countertop Ovens

- Other Small Home Appliances (Waffle Makers, Deep Fryers, Egg Cookers, Tea Makers, Rice Cookers, Etc.)

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- Northeast

- Southeast

- Midwest

- Southwest

- West

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview appliance makers, component suppliers, big-box buyers, and online retailers across the Midwest, Sunbelt, and Pacific regions. These conversations test preliminary demand pools, typical average selling prices (ASP), and emerging smart-feature premiums, while short consumer surveys validate purchase frequency and replacement cycles.

Desk Research

We begin by mapping the market universe through open datasets such as US Census Quarterly Appliance Shipments, AHAM unit-shipment reports, Bureau of Labor Statistics price series, and U.S. International Trade Commission customs records. Trade association briefs, academic journals on consumer ergonomics, and national retail audit snapshots then clarify adoption triggers and channel splits. Premium libraries, D&B Hoovers for manufacturer revenue, Dow Jones Factiva for merger activity, and Questel for appliance patent flows, supply context on competitive intensity. The sources cited above are illustrative; many further websites, filings, and newsfeeds underpin the desk work that feeds our models.

Market-Sizing & Forecasting

A top-down construct starts with retail sales and shipment tonnage, which are then reconciled with stock-to-sales ratios and replacement rates to size 2024 and 2025 demand. Supplier roll-ups of leading vacuum, blender, and air-fryer brands provide a selective bottom-up lens that adjusts category totals. Key variables like household formation, median disposable income, online appliance penetration, ASP progression from BLS indices, and Energy Star rebate uptake drive a multivariate regression that produces the 2025-2030 outlook. Gaps in bottom-up coverage (for niche items like garment steamers) are bridged by triangulating import values with border-adjusted ASPs.

Data Validation & Update Cycle

Outputs pass three layers of anomaly checks and peer review before sign-off. Reports refresh yearly, and analysts trigger interim revisions when tariffs, rebate rules, or sizable product recalls materially impact volumes.

Why Mordor's United States Small Home Appliances Baseline Stands Firm

Published market estimates often diverge because firms choose dissimilar product baskets, price bases, and refresh cadences.

Key gap drivers include (i) some studies restricting scope to kitchen appliances alone, (ii) others applying global ASPs to U.S. volumes, and (iii) inconsistent handling of smart-premium mark-ups. By contrast, Mordor's definition spans the full household spectrum and our mixed top-down/bottom-up test guards against single-source bias.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 27.42 bn (2025) | Mordor Intelligence | - |

| USD 31.37 bn (2025) | Regional Consultancy A | Relies on modeled e-commerce receipts without shipment cross-check |

| USD 5.54 bn (2025) | Trade Journal B | Covers kitchen appliances only, omits floor-care and air-treatment devices |

In sum, the disciplined source mix, transparent variable map, and annual rebuild ensure Mordor's numbers serve as a balanced, repeatable baseline that decision-makers can trust.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the US small home appliances market?

The market is valued at USD 28.44 billion in 2026.

How fast is the US small home appliances market expected to grow?

It is forecast to expand at a 3.72% CAGR, reaching USD 34.14 billion by 2031

Which product segment is growing the fastest?

Air fryers lead growth, registering a 7.35% CAGR through 2031.

Which distribution channel is gaining share most quickly?

Online sales are advancing at a 6.05% CAGR as shoppers adopt e-commerce and DTC ordering.

What region shows the strongest growth outlook?

The West posts the highest regional CAGR at 4.92% through 2031 due to tech-forward and efficiency-focused consumers.

How are tariffs influencing manufacturers?

New steel, Canadian, and Mexican import tariffs raise input costs, prompting supply-chain restructuring and selective price increases that may temper demand growth.