| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 2.60 Billion |

| Market Size (2030) | USD 3.36 Billion |

| CAGR (2025 - 2030) | 5.25 % |

Major Players*Disclaimer: Major Players sorted in no particular order |

US Small Bone and Joint Devices Market Analysis

The US Small Bone And Joint Devices Market size is estimated at USD 2.60 billion in 2025, and is expected to reach USD 3.36 billion by 2030, at a CAGR of 5.25% during the forecast period (2025-2030).

The US small bone and joint devices industry is experiencing significant transformation driven by demographic shifts and evolving healthcare needs. According to the 2022 United Nations Population Fund statistics, 65% of the US population falls within the working age group of 15-64 years, while 17% are aged 65 years and above, indicating a substantial patient pool requiring orthopedic interventions. The increasing participation in sports and recreational activities has led to a rise in related injuries, with the National Safety Council reporting in 2022 that sports and recreational injury rates rose 20% compared to the previous year. This demographic and lifestyle pattern has created a robust demand for innovative orthopedic extremities solutions and specialized treatment approaches.

The market landscape is being reshaped by technological innovations and advanced surgical techniques, particularly in minimally invasive procedures. In February 2023, a groundbreaking study by researchers at the Hospital for Special Surgery (HSS) demonstrated that bunion procedures do not worsen flatfoot conditions and may even improve them, showcasing the advancement in surgical techniques. The industry has witnessed a surge in the development of specialized instruments and implants designed to improve surgical outcomes while reducing recovery time, leading to increased adoption of these advanced solutions across healthcare facilities, particularly in foot and ankle devices.

The competitive environment has been marked by strategic consolidations and product innovations throughout 2023. Notable developments include Arthrex's launch of the Bunionectomy System in December 2022, offering patients an improved alternative to traditional bunion surgery with faster recovery times. The industry has also seen significant partnerships, such as Premier Orthopedic Associates' alliance with American Orthopedic Partners in February 2023, aimed at transforming orthopedic care delivery models and expanding access to advanced treatment options.

The market is witnessing a shift toward ambulatory surgical centers and specialized orthopedic facilities. This trend is exemplified by strategic developments such as NCH Healthcare System's partnership with Hospital for Special Surgery in November 2022 to establish a USD 70 million ambulatory surgery center in Southwest Florida. Healthcare providers are increasingly focusing on creating dedicated centers of excellence for orthopedic care, improving operational efficiency while providing specialized treatment options. This structural transformation is accompanied by the adoption of value-based care models and an enhanced focus on patient outcomes, driving the development of more efficient and cost-effective treatment solutions, especially in the realm of orthopedic extremities.

US Small Bone and Joint Devices Market Trends

Increasing Prevalence of Degenerative Joint Diseases and the Growing Geriatric Population

The rising prevalence of degenerative joint diseases such as osteoarthritis, rheumatoid arthritis, osteoporosis, and carpal tunnel syndrome is creating substantial demand for orthopedic extremities surgery and associated devices in the United States. Osteoarthritis, the most common type of arthritis affecting hands, wrists, feet, and ankles, is particularly significant as it often requires surgical intervention when conservative treatments prove ineffective. According to the Centers for Disease Control and Prevention data from October 2021, by 2040, an estimated 78 million (26%) United States adults aged 18 years and older will have doctor-diagnosed arthritis, indicating a growing patient population requiring treatment. The elderly population, which is more susceptible to various bone and joint disorders, continues to expand, further driving the need for effective treatment options.

The burden of joint diseases is particularly evident in specific anatomical areas, with hand and wrist conditions showing notable prevalence. For instance, according to data published by Hand Surgeries Specialists of Texas in March 2021, over 124,000 hand injuries occur in the United States annually, with a significant proportion of the population developing degenerative hand conditions. The impact extends beyond acute injuries to chronic conditions, as one in seven persons in the United States has wrist arthritis, representing nearly 13.6% of the population. Additionally, the prevalence of rheumatoid arthritis affecting the wrist impacts approximately 2.5 million people in the United States, creating a substantial patient population requiring specialized small joint replacement devices for treatment.

Understand The Key Trends Shaping This Market

Download PDF

Technological Advancements and Growing Demand for Joint Surgeries

The small bone and joint devices market is experiencing significant growth driven by technological innovations in fixation implants, plating systems, and surgical techniques. Manufacturers are developing new and advanced solutions that offer improved patient outcomes and enhanced surgical efficiency. For example, in February 2023, CurvaFix, Inc. introduced its 7.5mm CurvaFix IM Implant, specifically designed to simplify surgery and provide strong, stable fixation in small-boned patients. Similarly, in April 2022, Medline Unite Foot and Ankle launched its Calcaneal Fracture plating system with IM fibula implant, featuring various implant options and new, large, fully threaded headed cannulated screws, demonstrating the industry's commitment to advancing surgical technologies.

The demand for joint surgeries is further amplified by the high incidence of sports-related injuries and workplace accidents. According to the National Safety Council Statistics 2022, sports and recreational injury rates rose 20% in 2021 compared to the previous year, with 3.2 million people requiring emergency department treatment for sports and recreational equipment injuries. The most common sports-related injuries were observed in basketball (259,779 cases), followed by skateboards, scooters, and hoverboards (245,177 cases), and ATVs, mopeds, and minibikes (238,404 cases). These injuries often require surgical intervention using orthopedic trauma devices, particularly for treating ligament tears, cartilage damage, and fractures. The advancement in surgical techniques and technologies has also led to improved outcomes, making these procedures more attractive to patients and healthcare providers. Furthermore, the development of small joint arthroscopy techniques has enhanced the precision and recovery time for such surgeries, contributing to their growing popularity.

Segment Analysis: By Device Type

Hand and Wrist Devices Segment in US Small Bone and Joint Devices Market

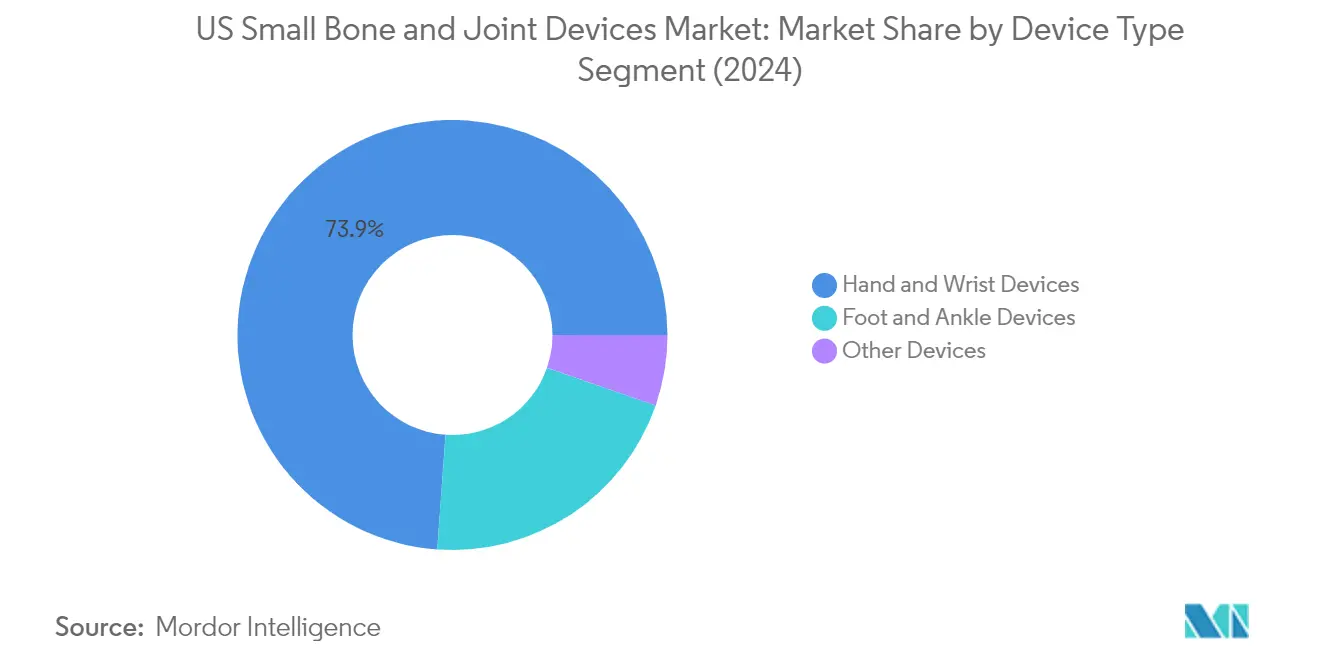

The hand and wrist devices segment continues to dominate the US small bone and joint devices market, commanding approximately 74% of the total market share in 2024. This substantial market presence is driven by the high prevalence of hand and wrist injuries in the United States, with over 124,000 hand injuries occurring annually. The segment's dominance is further strengthened by continuous technological advancements in fixation implants, plating systems, and fixation devices. The introduction of innovative products like enhanced ergonomic designs and advanced plating systems that offer improved patient outcomes and reduced procedure time has significantly contributed to maintaining this segment's leading position in the market. Additionally, the increasing adoption of minimally invasive surgical techniques and the rising demand for effective treatment options for degenerative hand and wrist conditions have further solidified this segment's market leadership.

Hand and Wrist Devices Segment Growth in US Small Bone and Joint Devices Market

The hand and wrist devices segment is projected to maintain its growth momentum with an expected CAGR of approximately 6% during the forecast period 2024-2029. This growth trajectory is primarily fueled by the increasing adoption of technologically advanced implants and the rising number of product launches featuring innovative designs and improved functionalities. The segment's growth is further supported by the expanding geriatric population, which is more susceptible to degenerative joint diseases affecting hands and wrists. The development of patient-specific solutions and the integration of advanced materials in device manufacturing are expected to drive innovation in this segment. Moreover, the increasing focus on developing devices that facilitate faster recovery and improved patient outcomes, coupled with the rising demand for minimally invasive surgical procedures, is anticipated to sustain this segment's robust growth rate over the forecast period.

Remaining Segments in US Small Bone and Joint Devices Market by Device Type

The foot and ankle devices segment represents a significant portion of the market, offering comprehensive solutions for various foot and ankle conditions, including trauma, arthritis, and degenerative diseases. This segment continues to evolve with the introduction of new plating systems and innovative fixation technologies designed specifically for complex foot and ankle procedures. The other devices segment, while smaller in market share, plays a crucial role in addressing specific needs in small bone and joint procedures, particularly in areas such as elbow joints and other specialized applications. Both segments benefit from ongoing technological advancements and the increasing focus on developing specialized solutions for specific anatomical requirements, contributing to the overall growth and diversification of the small bone and joint devices market.

Segment Analysis: By Procedure Type

Upper Extremities Segment in US Small Bone and Joint Devices Market

The Upper Extremities segment dominates the US Small Bone and Joint Devices market, commanding approximately 77% of the total market share in 2024. This significant market position is attributed to the high prevalence of hand and wrist injuries, coupled with the increasing adoption of advanced surgical techniques in upper extremity procedures. The segment encompasses various procedures including finger joint fusion, wrist arthroplasty, carpometacarpal procedures, and other upper extremity surgeries. The growth is further supported by continuous technological advancements in surgical devices and implants, particularly in areas such as wrist replacement systems and finger joint fusion technologies. Additionally, the rising incidence of degenerative joint diseases affecting the upper extremities, combined with the growing elderly population requiring such procedures, continues to drive the segment's dominance in the market.

Lower Extremities Segment in US Small Bone and Joint Devices Market

The Lower Extremities segment is emerging as the fastest-growing segment in the US Small Bone and Joint Devices market, projected to grow at approximately 6% CAGR from 2024 to 2029. This accelerated growth is driven by increasing cases of foot and ankle disorders, coupled with the rising demand for minimally invasive surgical procedures. The segment's growth is further propelled by continuous innovations in surgical techniques and device technologies, particularly in areas such as bunionectomy and hammertoe procedures. The introduction of advanced implant materials and designs, coupled with improved surgical outcomes, has significantly enhanced the adoption of lower extremity procedures. Additionally, the increasing focus on sports-related injuries and the growing awareness about foot and ankle health among the general population have contributed to the segment's rapid expansion in the market.

Segment Analysis: By End User

Hospitals Segment in US Small Bone and Joint Devices Market

The hospitals segment has emerged as both the dominant and fastest-growing segment in the US small bone and joint devices market, holding approximately 61% market share in 2024. This commanding position is attributed to hospitals being well-equipped with necessary advanced equipment, infrastructure, and qualified medical staff to effectively manage and perform orthopedic interventions such as small bone and joint procedures. The segment's growth is further bolstered by the significant presence of orthopedic surgeons in hospital settings, with over 2,470 orthopedic surgeons employed at general medical and surgical hospitals across the United States. Strategic developments such as expansions and partnerships by hospitals in orthopedic care continue to strengthen this segment's position. The establishment of new specialty orthopedic hospitals and formation of strategic partnerships between healthcare providers has enhanced the accessibility of orthopedic treatments, including small bone and joint procedures, contributing to the segment's robust performance in the market.

Clinic Segment in US Small Bone and Joint Devices Market

The clinic segment represents a significant portion of the US small bone and joint devices market, demonstrating steady growth through strategic developments and expanding orthopedic care services. Clinics are actively enhancing their service offerings through partnerships with established orthopedic institutes and expanding their presence in various regions. These facilities are increasingly focusing on providing specialized orthopedic care, including procedures involving small bone and joint devices, in outpatient settings. The segment's growth is supported by the rising trend of performing less complex orthopedic procedures in clinic settings, offering patients more convenient and cost-effective treatment options. Clinics are also investing in advanced equipment and recruiting specialized orthopedic professionals to improve their service capabilities. The increasing adoption of minimally invasive procedures and the growing preference for outpatient surgeries have further strengthened the position of clinics in the market.

Remaining Segments in End User Market

The other end users segment, which includes physician offices, specialty centers, ambulatory surgical centers, and medical institutions, plays a vital role in the US small bone and joint devices market. These facilities are increasingly adopting advanced orthopedic technologies and expanding their service offerings through strategic partnerships and collaborations. The segment benefits from the growing trend of performing orthopedic procedures in specialized settings, particularly in ambulatory surgical centers that offer cost-effective alternatives to hospital-based procedures. Medical institutions and specialty centers are also strengthening their positions through partnerships with established orthopedic care providers and investing in advanced equipment and skilled professionals. The segment continues to evolve with the changing healthcare landscape, adapting to patient preferences for specialized care settings and contributing to the overall growth of the small bone and joint devices market.

US Small Bone and Joint Devices Industry Overview

Top Companies in US Small Bone and Joint Devices Market

The market is characterized by intense innovation and strategic developments among key players, including Stryker, Smith+Nephew, Zimmer Biomet, Johnson & Johnson (DePuy Synthes), and other specialized manufacturers like Arthrex and Exactech. Companies are heavily investing in research and development to introduce advanced technologies, particularly in minimally invasive surgical solutions and 3D-printed implants. The industry witnesses frequent product launches focusing on improved surgical outcomes and patient recovery times. Strategic partnerships and distribution agreements have become commonplace as companies seek to expand their market presence and enhance their product portfolios. Manufacturing capabilities are being continuously upgraded to incorporate new technologies and meet increasing quality standards, while companies are also focusing on strengthening their direct sales forces and distribution networks to improve market penetration.

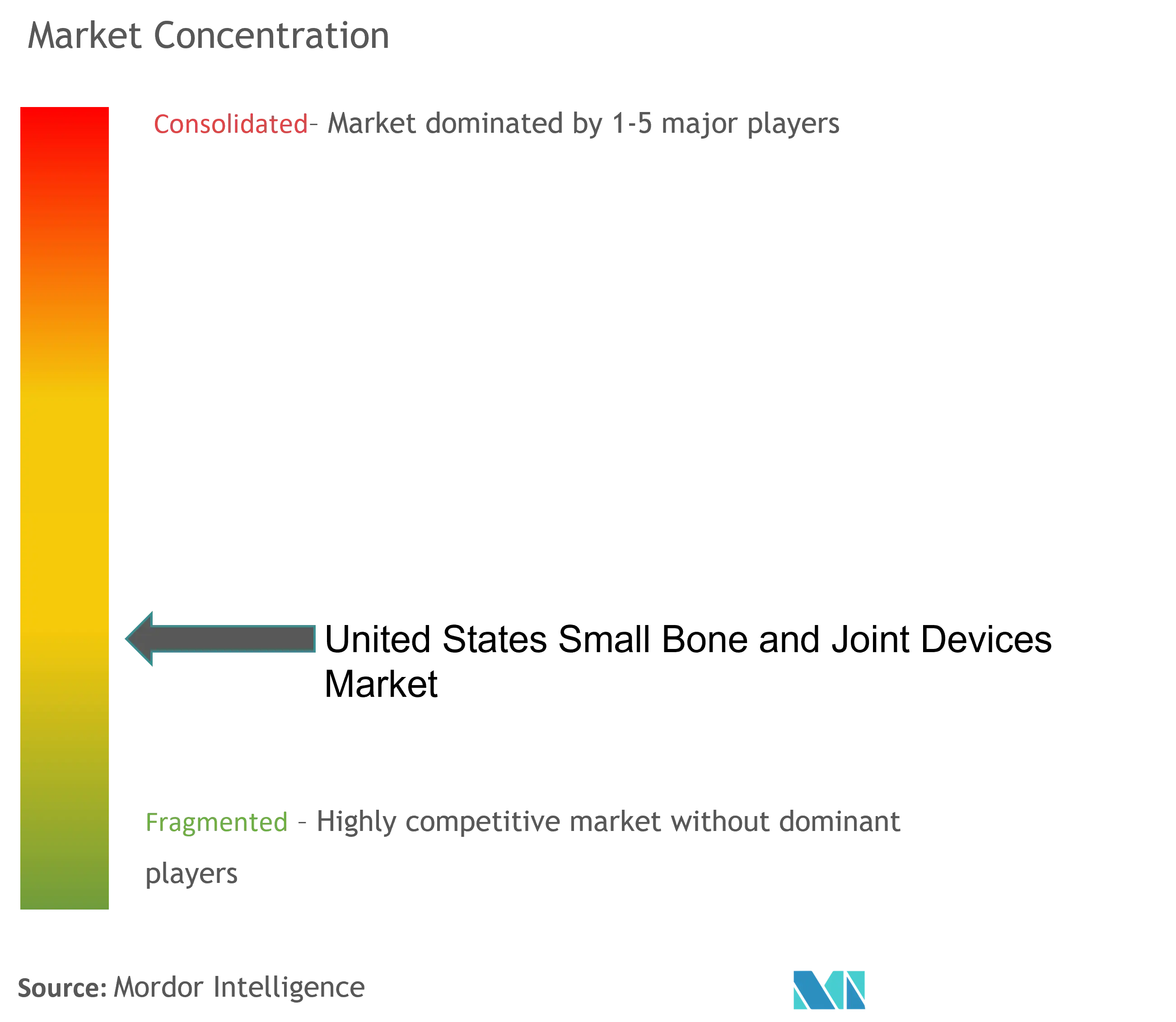

Consolidated Market Led By Global Players

The US small bone and joint devices market demonstrates a high level of consolidation, dominated by large multinational medical device manufacturers with diverse orthopedic portfolios. These established players leverage their extensive research capabilities, robust distribution networks, and strong financial positions to maintain their market leadership. The market structure favors companies with integrated operations spanning research, manufacturing, and distribution, creating significant barriers to entry for newer players. Mergers and acquisitions remain a key strategy for market expansion, with larger companies actively acquiring innovative startups and specialized manufacturers to enhance their technological capabilities and expand their product offerings.

The competitive dynamics are shaped by a mix of global conglomerates and specialized orthopedic device manufacturers, each bringing unique strengths to the market. While global players benefit from economies of scale and extensive resources, specialized manufacturers often lead in niche segments through focused innovation and expertise. The market has seen increased collaboration between established players and technology companies, particularly in developing smart implants and surgical navigation systems. Regional players maintain their relevance through strong local relationships and specialized product offerings tailored to specific market needs.

Innovation and Adaptability Drive Future Success

Success in the market increasingly depends on companies' ability to innovate while maintaining cost efficiency and regulatory compliance. Established players must continue investing in research and development while optimizing their manufacturing processes to maintain competitive pricing. Building strong relationships with healthcare providers and maintaining high product quality standards remain crucial for market success. Companies need to focus on developing comprehensive product portfolios that address various surgical needs while investing in training and education programs for healthcare professionals. The ability to adapt to changing healthcare delivery models and reimbursement policies will be crucial for maintaining market position.

For emerging players and contenders, success lies in identifying and exploiting niche market segments while building strong distribution partnerships. Companies must focus on developing innovative solutions that address unmet clinical needs while ensuring cost-effectiveness. The increasing emphasis on outpatient procedures and ambulatory surgical centers presents opportunities for companies to develop specialized products for these settings. Regulatory compliance and quality management systems will continue to be critical factors, particularly as the FDA maintains strict oversight of orthopedic devices. Companies must also consider the growing influence of healthcare purchasing organizations and the need for strong clinical evidence to support product adoption. The development of orthopedic extremities and small joint replacement solutions, alongside orthopedic trauma devices and extremity reconstruction innovations, will be pivotal in addressing the evolving needs of the healthcare sector.

US Small Bone and Joint Devices Market Leaders

-

Stryker Corporation

-

Zimmer Biomet

-

Johnson & Johnson (DePuy Synthes)

-

Smith & Nephew LLC

-

Acumed LLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

US Small Bone and Joint Devices Market News

- February 2023: CurvaFix, Inc. reported the release of its 7.5mm CurvaFixIM Implant, which is designed to simplify surgery and provide strong, stable fixation in small-boned patients. The company will also highlight the 9.5mm CurvaFix implant, which was made available in late 2021, as well as provide updates from recent U.S. cases.

- April 2022: Paragon 28 Inc. launched the R3ACT stabilization system, which is designed to be a simple solution that allows for multi-stage soft tissue healing following an acute or chronic syndesmotic injury to the ankle.

US Small Bone and Joint Devices Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Increasing Prevalence of Degenerative Joint Diseases and Growing Geriatric Population

- 4.1.2 Technological Advancements and Growing Demand for Joint Surgeries

-

4.2 Market Restraints

- 4.2.1 Stringent Regulatory Policies

-

4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - in USD Million)

-

5.1 By Device Type

- 5.1.1 Hand and Wrist Devices

- 5.1.2 Foot and Ankle Devices

- 5.1.3 Other Devices

-

5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Clinic

- 5.2.3 Other End Users

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Johnson & Johnson (DePuy Synthes)

- 6.1.2 Zimmer Biomet

- 6.1.3 Stryker Corporation

- 6.1.4 DJO, LLC

- 6.1.5 Smith & Nephew PLC

- 6.1.6 Arthrex Inc.

- 6.1.7 Orthofix US LLC

- 6.1.8 Acumed LLC

- 6.1.9 Conventus Orthopaedics, Inc. (Flower Orthopedics)

- 6.1.10 Nutek Orthopedics

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

US Small Bone and Joint Devices Industry Segmentation

As per the scope of the report, when the articular cartilage is worn out or damaged, the gliding movements of the bones are disrupted, and small bone and joint devices are employed. These devices allow joints to extend their range of motion, improving their look and allowing them to move without discomfort again. The United States small bone and joint devices market is segmented by device type (hand and wrist devices, foot and ankle devices, and other devices) and end user (hospitals, clinics, and other end users). The report offers the value (in USD) for the above-mentioned segments.

| By Device Type | Hand and Wrist Devices |

| Foot and Ankle Devices | |

| Other Devices | |

| By End User | Hospitals |

| Clinic | |

| Other End Users |

Need A Different Region or Segment?

Customize Now

US Small Bone and Joint Devices Market Research FAQs

How big is the US Small Bone And Joint Devices Market?

The US Small Bone And Joint Devices Market size is expected to reach USD 2.60 billion in 2025 and grow at a CAGR of 5.25% to reach USD 3.36 billion by 2030.

What is the current US Small Bone And Joint Devices Market size?

In 2025, the US Small Bone And Joint Devices Market size is expected to reach USD 2.60 billion.

Who are the key players in US Small Bone And Joint Devices Market?

Stryker Corporation, Zimmer Biomet, Johnson & Johnson (DePuy Synthes), Smith & Nephew LLC and Acumed LLC are the major companies operating in the US Small Bone And Joint Devices Market.

What years does this US Small Bone And Joint Devices Market cover, and what was the market size in 2024?

In 2024, the US Small Bone And Joint Devices Market size was estimated at USD 2.46 billion. The report covers the US Small Bone And Joint Devices Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the US Small Bone And Joint Devices Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

US Small Bone And Joint Devices Market Research

Mordor Intelligence provides a comprehensive analysis of the orthopedic extremities sector, drawing on decades of healthcare research expertise. Our latest report delves into crucial segments such as small joint arthroscopy, small joint arthroplasty, and small joint replacement procedures. The analysis covers various treatment modalities, ranging from orthopedic trauma devices to advanced extremity reconstruction techniques. This offers stakeholders actionable insights into market dynamics and technological innovations.

Industry participants can access detailed evaluations of emerging opportunities in foot and ankle devices and related segments. This information is available in an easy-to-download report PDF format. The research offers strategic insights for manufacturers, healthcare providers, and investors. It features in-depth analysis of regulatory frameworks, reimbursement scenarios, and technological advancements. Our consulting expertise ensures stakeholders receive current data and forecasts to optimize their market positioning and strategic planning initiatives.