Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

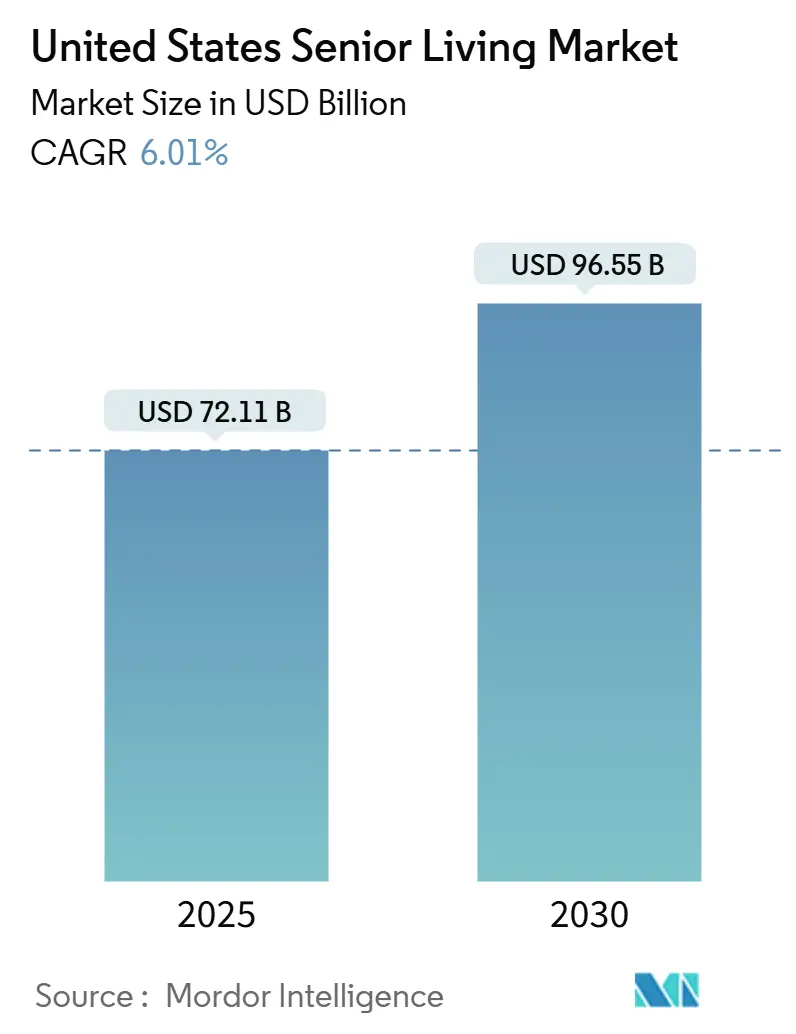

| Market Size (2025) | USD 72.11 Billion |

| Market Size (2030) | USD 96.55 Billion |

| Growth Rate (2025 - 2030) | 6.01% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Senior Living Market Analysis by Mordor Intelligence

The United States senior living market size stands at USD 72.11 billion in 2025 and is forecast to reach USD 96.55 billion by 2030, advancing at a 6.01% CAGR over the period. Continued demand from an aging population, constrained new‐build supply, and sophisticated capital inflows combine to create pricing power for operators while supporting steady occupancy gains. Healthcare integration deepens competitive moats because communities that embed primary care and rehabilitation services capture higher margins, lift length of stay, and reduce hospital transfers. Rental pricing flexibility lets operators respond quickly to wage inflation and regulatory costs, helping to maintain operating margins despite labor pressures. Institutional investors, especially healthcare REITs, sustain development pipelines through joint ventures and sale-leasebacks, fueling consolidation even as interest rates remain elevated. Technology adoption, from electronic health records to predictive analytics, further enhances resident outcomes and cost efficiency.

Key Report Takeaways

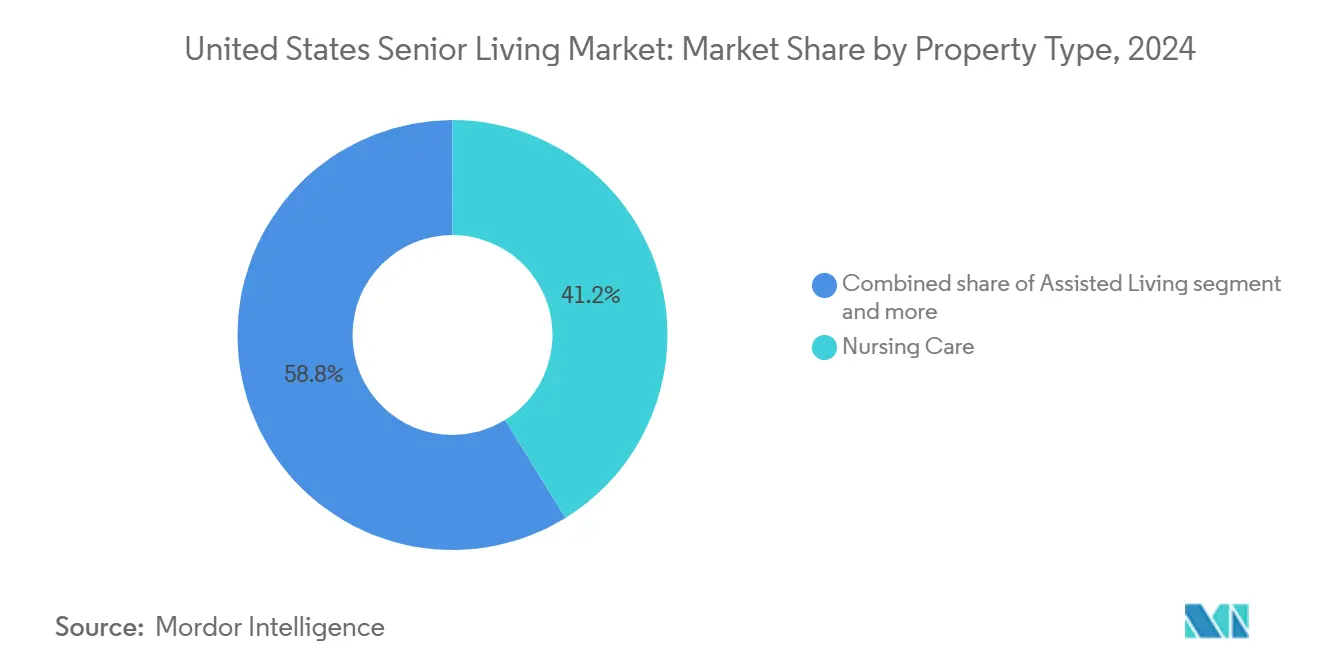

- By property type, nursing care captured 41.2% of the United States senior living market share in 2024 and leads growth with a 6.55% CAGR through 2030.

- By business model, the Long-Lease / Rental format held 82.3% of the United States senior living market share in 2024, while the Hybrid (Sale + Lease) model records the highest projected CAGR at 6.71% to 2030.

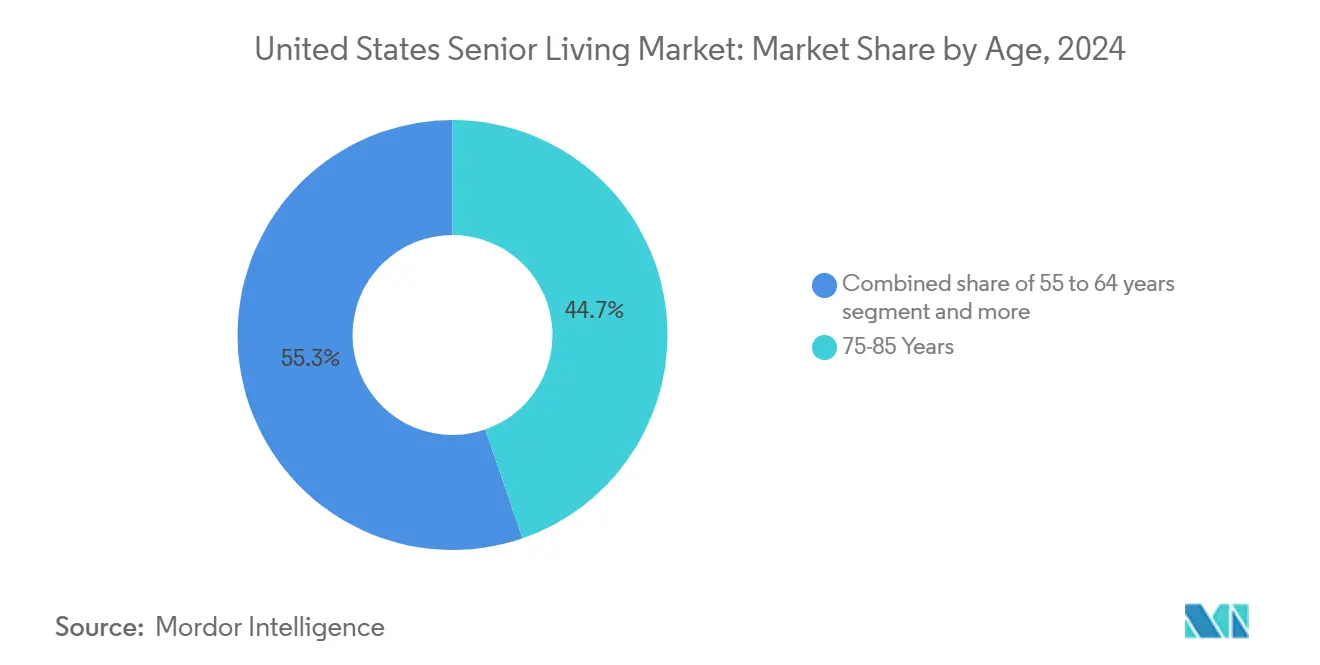

- By age, residents aged 75-85 accounted for 44.7% of demand in 2024; residents above 85 are projected to expand at a 7.01% CAGR through 2030.

- By geography, California led with a 12.2% revenue share in 2024, whereas Texas is advancing at a 7.22% CAGR to 2030.

United States Senior Living Market Trends and Insights

Drivers Impact Analysis

| Drivers | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging baby-boomer cohort driving sustained demand across independent, assisted, and memory care | +2.1% | National; high density in California, Florida, Texas | Long term (≥ 4 years) |

| Deep capital markets and active healthcare REITs supporting development and consolidation | +1.4% | National, primary metropolitan areas | Medium term (2-4 years) |

| Shift to healthcare-integrated models, enhancing the value proposition | +1.2% | National; early adoption in California, the Northeast | Medium term (2-4 years) |

| Home-sale equity and retirement savings enabling private-pay affordability | +0.9% | High-income metros: California, Northeast | Short term (≤ 2 years) |

| Technology adoption elevates care quality and efficiency | +0.4% | National; faster in urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Aging Baby-Boomer Cohort Driving Sustained Demand Across Care Levels

Nearly all 69 million baby boomers will be 70 or older by 2033, dramatically enlarging the resident pool for the United States senior living market. Higher home ownership and net worth among this cohort underpin private-pay affordability, while broader acceptance of technology raises comfort with digitally enabled care. The 85-plus population, most likely to require skilled nursing and memory care, is set to double by 2040, guaranteeing demand for high-acuity services. States attracting retirees through favorable taxes and climate, such as Texas and Florida, will see especially strong growth. Operators that tailor amenities, payment plans, and marketing to this wealthier, tech-savvy generation are positioned to capture lifetime value. Green Street estimates show more than 40% of seniors can pay for senior housing without liquidating assets, indicating significant latent demand.

Deep Capital Markets and Active Healthcare REITs Supporting Development and Consolidation

Healthcare REITs are pouring record funds into United States senior living market assets. Ventas lifted its 2025 investment target to USD 1.5 billion after deploying USD 2 billion in 2024, signaling long-term conviction in sector fundamentals. Welltower’s USD 3.2 billion acquisition of Amica Senior Lifestyles illustrates the scale REITs will transact to secure premier portfolios. Debt capital remains abundant, with Walker & Dunlop arranging USD 600 million in seniors-housing loans during 2024. Private equity heavyweights such as Fortress add further competition for assets, driving valuations and spurring operational upgrades. Strong liquidity supports new builds in undersupplied metros and offers exit paths for regional owner-operators, accelerating consolidation and professionalization across the ecosystem[1]Roberta Katz, “2025 Investor Presentation,” Ventas Inc., ventasreit.com.

Shift to Healthcare-Integrated Models Enhancing Value Proposition and Resident Outcomes

Operators now embed primary care, chronic disease programs, and rehabilitation services directly inside communities, recasting senior living as a healthcare platform. Brookdale’s HealthPlus residents experienced 78% fewer urgent-care visits and 36% fewer hospitalizations compared with peers in traditional communities. Integration widens revenue streams via Medicare Advantage partnerships and ancillary billing while boosting resident loyalty. Specialized memory-care wings, on-site labs, and therapy gyms create one-stop solutions that alleviate family burden and justify premium pricing. Electronic health records and telehealth link on-site clinicians with external providers, ensuring seamless care coordination. Regulatory support is growing as payers reward demonstrable outcome improvements.

Home-Sale Equity and Retirement Savings Enabling Private-Pay Affordability

Home price appreciation over the past decade has given many seniors sizable equity cushions that can be tapped through sales or reverse mortgages to fund entry fees or monthly rents. High savings rates among white-collar retirees further buttress affordability, especially in coastal and high-income metros. Financial advisors increasingly recommend senior living communities as cost-effective alternatives to prolonged in-home care, encouraging earlier move-ins. Operators respond with bridge-financing programs and refundable entrance fees to lower perceived barriers. While macroeconomic volatility can delay home sales, longer trend lines point to a steady supply of qualified residents for the United States senior living market.

Restraints Impact Analysis

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages and wage inflation are pressuring margins and service levels | −1.8% | National; acute in rural and secondary markets | Short term (≤ 2 years) |

| State-by-state regulatory complexity is increasing compliance costs and timelines | −0.7% | National; highest in California, New York, Illinois | Medium term (2-4 years) |

| Affordability gaps and uneven occupancy recovery in certain secondary markets | −0.5% | Secondary and rural markets; Midwest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages and Wage Inflation Pressuring Margins and Service Levels

Severe staffing shortages plague virtually every care level, forcing communities to raise hourly wages, expand benefits, and rely heavily on agency labor. New CMS nursing-home staffing rules requiring 3.48 nursing hours per resident per day ripple into assisted and independent living through competition for licensed nurses. Only 6% of nursing homes currently meet the 24/7 RN mandate, driving cross-sector bidding wars that compress margins. Caregiver wage campaigns, such as Nevada’s push from USD 16 to USD 20 per hour, spotlight inflationary pressures. The FTC’s pending ban on non-compete clauses may further elevate turnover, undermining continuity of care. Operators in rural areas confront the steepest hurdles, sometimes restricting admissions to maintain mandated staff-resident ratios[2]Chiquita Brooks-LaSure, “Minimum Staffing Standards for Long-Term Care Facilities and Medicaid Institutional Payment Transparency Reporting,” Centers for Medicare & Medicaid Services, cms.gov.

State-by-State Regulatory Complexity Increasing Compliance Costs and Development Timelines

The absence of uniform federal oversight means each state sets its own licensing, inspection, and reporting rules. Fifteen states updated assisted-living statutes between July 2023 and July 2024, with 88% now imposing infection-control mandates. California’s multi-agency approval process for Residential Care Facilities for the Elderly demands financial, architectural, and care-model reviews, stretching timelines and consultancy fees. New CMS surveyor guidance, effective March 2025, layers additional federal documentation on admission assessments and chemical-restraint policies. Multi-state operators must maintain disparate policy handbooks, duplicative training, and localized audit teams, diluting scale efficiencies[3]Karen Hoffman, “State Infection Control Requirements in Assisted Living, 2024 Update,” National Center for Assisted Living, ncal.org..

Segment Analysis

By Property Type: Nursing Care Demand Mirrors Rising Acuity Needs

Nursing care facilities controlled 41.2% of the United States senior living market size in 2024 and will post the quickest 6.55% CAGR through 2030. Demand stems from residents with multiple chronic conditions who prefer aging in place within a continuum-of-care setting instead of hospital transfers. Assisted-living remains the mainstream entry point, yet operators retrofit wings for memory-care or sub-acute services to retain residents and capture value. Independent-living communities focus on lifestyle amenities, fitness centers, chef-led dining, and cultural programs, geared toward younger seniors who prize autonomy. The maturation of memory-care units, complete with secured layouts and dementia-trained staff, illustrates the sector’s pivot to higher acuity while preserving residential ambience. Continuing-care retirement communities, though niche, gain traction among affluent seniors desiring contractual access to multiple care levels.

Nursing-care dominance compels capital investment in clinical staff training, negative-pressure rooms, and on-site therapy suites. Operators deploy electronic medication-administration records and smart lifts to boost safety and efficiency. Rising acuity also attracts insurer partnerships seeking reduced readmissions, adding payer-driven revenue to the United States senior living market. However, regulatory scrutiny on staffing ratios, infection control, and reimbursement adequacy remains intense, requiring sophisticated compliance infrastructures.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Business Model: Rental Flexibility Outweighs Upfront Cost of Ownership Alternatives

Long-lease and rental communities accounted for 82.3% of the U.S. senior living market, driven by consumer preference for flexible month-to-month agreements and low upfront costs. Operators benefit from predictable cash flow and the ability to swiftly adjust pricing to offset labor or utility cost inflation. Marketing efforts emphasize liquidity, appealing to seniors seeking to avoid capital lock-in through entry fees. In contrast, hybrid models, primarily Continuing Care Retirement Communities (CCRCs), are forecasted to grow at a 6.71% CAGR. These models attract high-net-worth households by offering real estate appreciation and contractual care guarantees. Entrance fees, typically ranging from USD 200,000 to 1 million, provide funding for expansions and refurbishments without leveraging debt, thereby enhancing community standards and resale values.

Emerging hybrid contracts offer partial refunds on entrance fees or equity interests, combining the benefits of ownership with rental flexibility. Securitization of entrance-fee receivables enables operators to access cost-effective financing, accelerating the development of resort-style communities in key metropolitan markets. Rental communities are adopting à-la-carte care packages and subscription-based wellness programs to emulate the lifetime-care assurances of CCRCs, but without significant upfront costs. This approach facilitates broader market penetration within the U.S. senior living sector.

By Age: Above-85 Residents Propel High-Margin Services

Residents aged 75-85 supplied 44.7% of 2024 occupancy, yet the above-85 cohort will climb at a 7.01% CAGR and account for a growing share of premium-priced units. Communities design universal-access apartments with wider doorways, zero-threshold showers, and voice-activated controls to accommodate frailty without sacrificing aesthetics. Higher-age residents generate elevated per-capita revenue due to greater care intensity, spurring investment in 24/7 nursing stations, memory-care curricula, and hospice partnerships. Early retirees aged 55-64, meanwhile, gravitate toward active-adult rental enclaves with pickleball courts and co-working lounges, viewing the move as a lifestyle upgrade rather than a health need.

Programming across age bands becomes increasingly personalized. Cognitive-fitness classes, tele-rehab sessions, and chef-guided nutrition coaching address preventive health for younger cohorts, whereas fall-prevention technologies and chronic-disease clinics target the oldest residents. The United States senior living market thus segments not just by age but by wellness goals, enabling operators to diversify revenue streams and lengthen resident tenure.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

California commanded 12.2% of United States senior living market revenue in 2024, underpinned by high household wealth, robust home equity, and stringent licensure that limits new entrants. Operators capitalize on dense healthcare networks and thriving technology ecosystems to pilot telehealth platforms, electronic health records, and green-building retrofits that resonate with environmentally conscious residents. Elevated land and labor costs lift monthly fees, yet affluent clientele sustain occupancy and fund premium amenities. California’s wildfire and seismic risk necessitate resilient construction and emergency preparedness investments, which further raise barriers for smaller competitors.

Texas delivers the fastest 7.22% CAGR through 2030, buoyed by pro-business regulations, modest land prices, and significant retiree in-migration. Streamlined licensing allows quicker groundbreakings, and diversified metro economies in Dallas, Austin, and Houston support both middle-income and luxury projects. Labor supply is deeper, and wage levels are comparatively moderate, improving operating margins. The Ensign Group’s multi-property acquisitions highlight confidence in Texas as a springboard for the United States senior living market expansion.

Florida, New York, and Illinois represent mature yet opportunity-rich states. Florida communities confront hurricane risk and insurance cost spikes, prompting investments in hardened infrastructure and microgrid energy systems. New York grapples with high labor costs and unionization pressures but benefits from dense wealth pockets and sophisticated healthcare partnerships. Illinois sees regulatory scrutiny over staffing and refund-timing for CCRCs, but maintains steady demand in Chicago’s affluent suburbs. Emerging growth states such as North Carolina, Arizona, and Colorado draw developers thanks to favorable tax climates and healthcare system growth, evening out geographic risk for national platforms. Consolidation in secondary markets accelerates as regional chains merge to access capital and technology scale.

Competitive Landscape

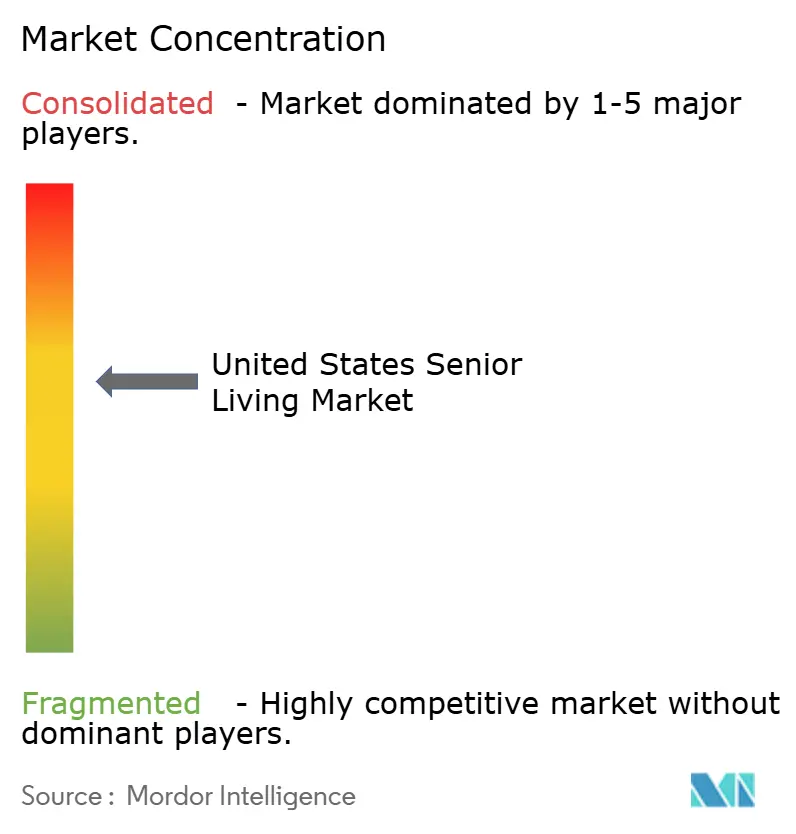

The United States senior living market remains moderately fragmented, with the top five operators controlling just under one-third of total units, while hundreds of local firms serve niche geographies. Brookdale, Atria, and Sunrise leverage national brands, purchasing clout, and data analytics to optimize pricing and staffing across portfolios. Healthcare REIT partners such as Ventas and Welltower furnish acquisition capital and performance-based lease structures that incentivize operational excellence. Private equity sponsors buy underperforming communities, inject technology upgrades, and deploy centralized revenue-management systems to fast-track value creation.

Competitive advantage coalesces around healthcare integration. Operators offering on-site primary care, therapy services, and advanced memory-care programs win referrals from hospital systems eager to reduce readmissions. Technology is another battleground. Electronic health records, predictive staffing algorithms, and resident engagement apps differentiate larger platforms and appeal to adult-child decision makers. Smaller operators respond by joining purchasing alliances and outsourcing IT functions to achieve cost parity.

Regulatory compliance capacity influences market share as CMS staffing mandates tighten and states heighten infection-control audits. Companies with robust clinical governance teams and real-time reporting dashboards mitigate citation risk and sustain five-star quality ratings, which directly correlate with occupancy. Capital access rounds out the landscape story: organizations with REIT or private-equity partners can execute multi-property portfolios, whereas stand-alone operators may become acquisition targets to secure succession planning or relieve debt burdens.

United States Senior Living Industry Leaders

-

Brookdale Senior Living Inc.

-

Atria Senior Living Inc.

-

LCS (Life Care Services)

-

Erickson Senior Living

-

Sunrise Senior Living

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: The Ensign Group announced the acquisition of five healthcare properties, further strengthening its presence with 343 operations across 17 states, showcasing its continued expansion strategy.

- Apr 2025: Fortress Investment Group completed the acquisition of The Village at Gainesville, a 639-residence community offering independent living, assisted living, and memory care services, reinforcing its portfolio in senior housing.

- March 2025: Welltower disclosed its agreement to acquire Amica Senior Lifestyles for CAD 4.6 billion (USD 3.2 billion), adding 47 properties and development sites to its portfolio, marking a significant investment in the senior living market.

- March 2025: Brookdale Senior Living finalized the acquisition of 30 communities for USD 310 million, increasing its real-estate ownership to over 75% of its consolidated portfolio, aligning with its strategic growth objectives.

United States Senior Living Market Report Scope

The US senior living market provides a wide range of housing and lifestyle options suitable for the needs of an aging population.

The report on the US senior living market includes market dynamics, technological trends, insights, and government initiatives related to the market.

The US senior living market is segmented by property type (assisted living, independent living, memory care, nursing care, and other property types) and key states (New York, Illinois, California, North Carolina, Washington, and the Rest of the United States). The report offers the United States senior living market size in value terms in (USD) for all the segments mentioned above.

By Property Type

| Assisted Living |

| Independent Living |

| Memory Care |

| Nursing Care |

By Business Model

| Outright Sale (Freehold) |

| Long-Lease / Rental |

| Hybrid (Sale + Lease) |

By Age

| 55 to 64 years |

| 65 to 74 years |

| 75 to 85 years |

| Above 85 years |

By States

| Texas |

| California |

| Florida |

| New York |

| Illinois |

| Rest of US |

| By Property Type | Assisted Living |

| Independent Living | |

| Memory Care | |

| Nursing Care | |

| By Business Model | Outright Sale (Freehold) |

| Long-Lease / Rental | |

| Hybrid (Sale + Lease) | |

| By Age | 55 to 64 years |

| 65 to 74 years | |

| 75 to 85 years | |

| Above 85 years | |

| By States | Texas |

| California | |

| Florida | |

| New York | |

| Illinois | |

| Rest of US |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the United States senior living market?

The market is valued at USD 72.11 billion in 2025 and is projected to reach USD 96.55 billion by 2030.

Which property type leads revenue in senior living communities?

Nursing care facilities account for 41.2% of 2024 revenue and will post the fastest 6.55% CAGR through 2030.

Why are healthcare REITs investing heavily in senior housing?

REITs view integrated care models and growing demand as durable income streams, prompting multibillion-dollar acquisitions and development pipelines.

How does Texas compare to California in market growth?

California holds the largest share at 12.2%, whereas Texas is the fastest-growing state with a 7.22% CAGR to 2030.

Page last updated on: