| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| CAGR | 2.75 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

United States Printing Ink Market Analysis

The United States Printing Inks Market is expected to register a CAGR of greater than 2.75% during the forecast period.

The printing inks industry is experiencing significant transformation as traditional print media adapts to changing consumer preferences and technological advancements. The newspaper industry continues to face challenges, with the combined average circulation of the 25 largest US titles declining by 14% in the period leading to September 2023. Despite this shift, the industry maintains resilience through diversification into specialized printing segments and the adoption of innovative technologies. The Wall Street Journal and New York Times, while remaining the largest dailies in the country, have experienced year-on-year declines of 14% and 13%, respectively, reflecting the broader industry's need to adapt to changing market dynamics.

The textile printing ink sector has emerged as a significant growth driver for the printing inks industry, demonstrating remarkable resilience and expansion. According to the National Council of Textile Organizations, US textile and apparel shipments reached an impressive USD 64.8 billion in 2023, establishing the United States as the world's third-largest textile exporter. This growth is particularly noteworthy as the industry supplies over 8,000 textile products to the US military, highlighting the diverse applications and strategic importance of textile printing ink in this sector.

The packaging segment is witnessing substantial investments and technological advancements, reflecting the industry's commitment to innovation and sustainability. In August 2023, American Packaging demonstrated this trend by opening a new flexible packaging ink manufacturing facility in Cedar City, Utah, with a USD 100 million investment. Similarly, Klarpet of Turkey and Triton International Enterprises announced a joint venture to develop a state-of-the-art food packaging ink facility in Berkeley County, with a planned investment of USD 50 million, indicating strong market confidence and growth potential.

The industry is experiencing significant technological advancement and capacity expansion, particularly in the label production sector. In April 2024, R.R. Donnelley & Sons Company confirmed the installation of four new presses in its US facilities to expand label production capacity, aiming to enhance flexibility and address changing consumer needs. These developments are complemented by innovations in ink formulation, as demonstrated by Hubergroup's launch of three new solvent-based inks in August 2023: Gecko Platinum Plus, Gecko Platinum NT, and Gecko Gold, featuring extended run times and superior print quality while maintaining eco-friendly characteristics. The commercial printing ink sector continues to evolve, adapting to these technological advancements and market demands.

United States Printing Ink Market Trends

Growing Demand from the Digital Printing Industry

The digital printing industry is experiencing unprecedented growth, driven by technological advancements and changing market demands. Before the mid-1990s, analog methods dominated personal and business communications, especially in print and broadcast media. However, the landscape has dramatically shifted with the advent of digital technologies over the last two decades. Digital printing has revolutionized the industry by introducing environmentally friendly methods that, while still requiring paper, consume significantly less than conventional printing. Traditional printers typically experience 15% material waste during regular operations, while digital printers, leveraging electronic charges, have reduced this waste to merely 5%. Some advanced digital printers even embrace recycled paper, further minimizing environmental impact.

The industry's commitment to innovation and sustainability is evident through recent technological developments and investments. In March 2024, Dscoop Edge, collaborating with HP Inc., unveiled an impressive lineup of HP digital printing presses and intelligent solutions designed to address current production challenges in commercial printing, labels, and packaging sectors. The technology's environmental prowess was highlighted in a 2023 study by Konica Minolta, which revealed a substantial 57% reduction in electricity consumption compared to conventional screen printing ink. Beyond this, inkjet ink printers enhance production efficiency, saving energy in ancillary operations like air conditioning and lighting. Digital printing significantly reduces overall printing costs by eliminating the need for new plates for each print job, making it particularly cost-effective for small-volume print runs and enabling color printing at costs comparable to black and white. The use of digital printing ink has further optimized these processes, ensuring high-quality outputs with minimal waste.

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand from the Packaging Sector

The packaging sector is witnessing substantial growth, primarily driven by increasing investments and innovations in sustainable solutions. The industry has been experiencing robust demand from the food and pharmaceutical sectors, with companies making significant investments to expand their capabilities. In August 2023, Klarpet of Turkey and Triton International Enterprises of the United States planned a joint venture to develop a state-of-the-art food packaging facility in Berkeley County with a planned investment of USD 50 million. Similarly, American Packaging opened a new flexible packaging manufacturing facility in Cedar City, Utah, with a total investment of USD 100 million, aimed at manufacturing flexible packaging solutions for industries such as drinks, dairy, liquid packaging, fresh produce, frozen foods, snacks, groceries, personal care, healthcare, and pet food.

The industry's focus on sustainability and innovation is reshaping packaging solutions, with flexible packaging emerging as a dominant trend. Flexible packaging offers significant advantages, requiring 91% less material than rigid packaging and providing approximately 96% space savings. The sector's growth is further bolstered by its applications in food packaging, where properties such as moisture absorption, product freshness maintenance, and temperature control are crucial. Companies are actively investing in sustainable solutions, as evidenced by Nestle's plans to invest USD 2 billion in sustainable packaging and increase production to boost the packaged food industry's sales. Additionally, in March 2022, Graphic Packaging International expanded its range of sustainable multi-pack packaging for the beverage industry, launching EnviroClip, a soft material paperboard alternative to standard plastic rings and shrink film for beverage cans, demonstrating the industry's commitment to supporting a more circular economy. The integration of packaging ink technologies has been pivotal in achieving these sustainable goals, offering innovative solutions that align with environmental standards.

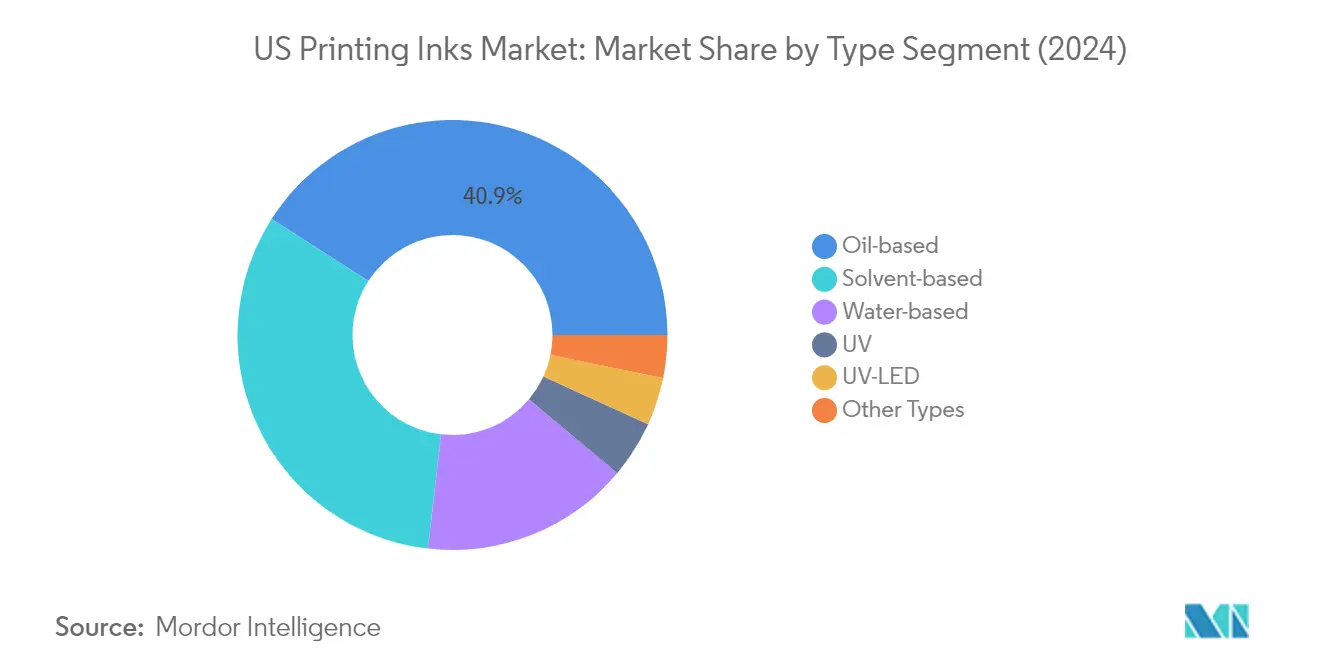

Segment Analysis: Type

Oil-based Segment in US Printing Inks Market

The oil-based printing inks segment dominates the United States printing inks market, commanding approximately 41% market share in 2024. This segment's prominence is attributed to its versatility and established presence in offset printing ink, particularly in producing high-quality books, magazines, newspapers, and commercial materials. Oil-based inks, primarily derived from vegetable oils like soybean and linseed oils, offer superior durability and resistance to fading, making them ideal for long-lasting applications. The segment's strength is further reinforced by its strong adhesion properties, particularly on paper and cardboard substrates, ensuring consistent print quality and longevity. Recent innovations in plant-based formulations have enhanced the segment's appeal, as demonstrated by Ricoh Company Ltd's introduction of its innovative 'Ricoh Plant-Based Ink' in 2024, which primarily sources from vegetable oils like soybean oil, marking a significant advancement in commercial graphics and packaging printing.

UV-LED Segment in US Printing Inks Market

The UV-LED printing inks segment is experiencing the most dynamic growth in the market, projected to expand at approximately 4% CAGR from 2024 to 2029. This growth is driven by the segment's superior environmental credentials, with UV-LED systems consuming up to 80% less electricity than traditional UV lamps and 95% less than conventional heat drying methods. The technology's rapid advancement has enhanced its compatibility with a broader range of substrates, including heat-sensitive materials, enabling printing on plastics, films, and textiles. UV-LED inks' instant curing capabilities significantly reduce production times, with some processes seeing up to 40% faster turnaround times while maintaining exceptional print quality. The segment's growth is further supported by its integration with digital workflows, offering compatibility with variable data printing and on-demand production, making it particularly attractive for personalization and short-run printing applications.

Remaining Segments in US Printing Inks Market

The remaining segments in the market include solvent-based, water-based, UV, and other types of printing inks, each serving distinct applications and market needs. Solvent-based inks continue to maintain a significant presence due to their exceptional adhesion properties and versatility across various substrates. Water-based inks are gaining traction due to their environmentally friendly characteristics and excellent performance in packaging applications. The conventional UV segment serves specialized applications requiring swift curing and enhanced durability. Other types, including specialty inks and hybrid formulations, cater to niche applications and specific industry requirements, contributing to the market's diversity and technological advancement.

Segment Analysis: Process

Lithographic Sheetfed Printing Segment in US Printing Inks Market

Lithographic sheetfed printing dominates the US printing inks market, commanding approximately 27% market share in 2024. This segment's prominence stems from its versatility and ability to handle a wide range of paper types and sizes, as well as other substrates like cardboard and plastics. The technology excels in producing high-quality prints with excellent color control and consistency across print runs, making it particularly valuable for commercial printing applications. Lithographic ink has maintained its market leadership through continuous technological advancements, including improved color management systems and enhanced automation features. The segment's strength is further reinforced by its cost-effectiveness for medium to large print runs, particularly in applications such as commercial prints, packaging, business cards, posters, and other promotional materials.

Digital Printing Segment in US Printing Inks Market

Digital printing emerges as the fastest-growing segment in the US printing inks market, projected to expand at approximately 5% CAGR from 2024 to 2029. This remarkable growth is driven by several factors, including the increasing demand for customized and short-run printing solutions. The segment's expansion is further fueled by technological advancements in digital printing ink equipment, enabling higher print quality and faster production speeds. Digital printing's appeal lies in its ability to offer quick turnaround times, reduced waste, and superior flexibility in handling variable data printing. The technology's eco-friendly profile, with features like reduced VOC emissions and lower energy consumption, aligns perfectly with growing environmental consciousness in the industry. Recent innovations in digital printing inks have also enhanced their compatibility with a broader range of substrates, opening up new applications across various sectors.

Remaining Segments in Process Segmentation

The US printing inks market encompasses several other significant process segments, including flexographic ink printing, gravure ink printing, lithographic web printing, and other specialized processes. Flexographic printing maintains a strong presence in the packaging sector, particularly for flexible packaging and labels. Gravure printing continues to be crucial for high-volume applications requiring superior print quality, especially in packaging and publications. Lithographic web printing serves the high-speed, high-volume printing needs of newspapers and magazines. Other specialized processes cater to niche applications, including screen printing, letterpress printing, and pad printing, each offering unique advantages for specific printing requirements. These segments collectively contribute to the market's diversity and ability to meet varied printing demands across different industries.

Segment Analysis: Application

Packaging Segment in United States Printing Inks Market

The packaging segment has emerged as both the largest and fastest-growing segment in the United States printing inks market, commanding approximately 55% of the market share in 2024. This dominance is driven by the surge in flexible packaging applications, particularly in food and beverage industries, where flexographic ink and gravure ink are extensively used for stand-up pouches, shrink sleeves, and cold-sealed packaging. The segment's growth is further propelled by innovations in sustainable packaging solutions, with manufacturers like DuPont and Hubergroup introducing eco-friendly water-based inks specifically designed for corrugated, folding cartons, and flexible packaging. The increasing focus on recyclability and sustainability in packaging design has led to the development of specialized inks that meet both environmental standards and performance requirements. Additionally, the expansion of e-commerce and the growing demand for branded packaging solutions have significantly contributed to the segment's prominence, with recent investments in packaging facilities by companies like American Packaging and Klarpet further strengthening the market position.

Remaining Segments in United States Printing Inks Market

The commercial and publication segment continues to maintain its significance in the market despite the digital transformation, primarily serving the printing needs of magazines, newspapers, and various commercial materials. The textile segment has carved out its niche in the market, particularly benefiting from the United States' position as the world's third-largest textile exporter and its leadership in textile research and development. The segment's growth is supported by the increasing adoption of digital textile printing and the rising demand for customized textile products. Other applications, including decorative printing for windows, photo printing, and wallpaper designs, contribute to the market's diversity by catering to specialized printing requirements across various industries. The construction industry's expansion has particularly influenced the demand for decorative printing applications, while the growing photographer population has boosted the demand for photo printing solutions.

United States Printing Ink Industry Overview

Top Companies in United States Printing Inks Market

The US printing inks market is led by prominent players including Sun Chemical, Flint Group, Sakata Inx Corporation, Siegwerk Druckfarben AG & Co. KGaA, and Toyo Ink Co. Ltd. These industry leaders have demonstrated a consistent focus on sustainable product development, particularly in eco-friendly and low-migration packaging ink for packaging applications. Companies are actively investing in research and development to introduce advanced digital printing ink solutions and UV-LED curing technologies. Strategic facility expansions across key industrial regions have strengthened manufacturing capabilities and distribution networks. The market has witnessed significant emphasis on developing bio-based and petrochemical-free formulations to meet evolving environmental regulations. Players are also enhancing their technical support services and establishing innovation centers to better serve customer requirements across various printing processes.

Fragmented Market with Strong Regional Players

The US printing inks market exhibits a fragmented structure with a mix of global conglomerates and specialized regional manufacturers. While multinational companies like Sun Chemical and Flint Group command significant market presence through their extensive product portfolios and nationwide distribution networks, regional players have carved out strong niches in specific applications and geographic territories. The market has witnessed strategic consolidation through acquisitions, exemplified by ALTANA's acquisition of Silberline Group and IN Groupe's purchase of Gleitsmann Security Inks from Hubergroup Deutschland GmbH, indicating a trend toward capability enhancement and market expansion.

The competitive dynamics are characterized by the presence of both diversified chemical companies and dedicated ink manufacturers. Global players leverage their research capabilities and economies of scale to maintain market leadership, while regional manufacturers compete through specialized product offerings and close customer relationships. The market structure encourages continuous innovation and customization capabilities, with companies maintaining dedicated facilities for basic ink production and specialized blending operations to serve diverse customer requirements across commercial printing ink, packaging, and digital applications.

Innovation and Sustainability Drive Future Success

Success in the US printing inks market increasingly depends on developing sustainable solutions and embracing digital transformation. Incumbent players must focus on expanding their eco-friendly product portfolios, investing in advanced manufacturing technologies, and strengthening their digital printing capabilities to maintain market leadership. Companies need to establish strong partnerships across the value chain, from raw material suppliers to end-users, while continuously improving their technical service capabilities. The ability to provide comprehensive solutions, including specialized applications for emerging sectors and value-added services, will be crucial for maintaining competitive advantage.

Market contenders can gain ground by focusing on niche applications and developing innovative solutions for specific industry segments. Success factors include building strong distribution networks, offering customized solutions for local market needs, and maintaining agility in responding to changing customer requirements. Companies must also consider potential regulatory changes regarding environmental protection and food safety, particularly in packaging applications. The increasing adoption of digital media and changing consumer preferences necessitate continuous adaptation of product portfolios and business strategies. Players need to maintain robust research and development capabilities while ensuring operational efficiency to remain competitive in this evolving market landscape.

United States Printing Ink Market Leaders

-

Sun Chemical

-

Flint Group

-

Sakata Inx Corporation

-

Siegwerk Druckfarben AG & Co. KGaA

-

Hubergroup Deutschland GmbH

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

United States Printing Ink Market News

- In May 2021, Epple Druckfarben AG and Zeller+Gmelin GmbH & Co. KG were working together in the field of UV ink technology. The first result of this partnership is a jointly developed UV-LED ink for sheetfed offset. The products are developed for different areas of application, which Epple will market worldwide under the LightStar brand.

United States Printing Ink Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Demand from the Digital Printing Industry

- 4.1.2 High Demand from the Packaging Sector

-

4.2 Restraints

- 4.2.1 Rising Demand for Digital Advertisements and E-books

- 4.2.2 Stringent Regulations Regarding Disposal

- 4.3 Industry Value Chain

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION

-

5.1 Type

- 5.1.1 Solvent-based

- 5.1.2 Water-based

- 5.1.3 Oil-based

- 5.1.4 UV

- 5.1.5 UV-LED

- 5.1.6 Other Types

-

5.2 Process

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Gravure Printing

- 5.2.4 Digital Printing

- 5.2.5 Other Processes

-

5.3 Application

- 5.3.1 Packaging

- 5.3.1.1 Rigid Packaging

- 5.3.1.1.1 Paperboard Containers

- 5.3.1.1.2 Corrugated Boxes

- 5.3.1.1.3 Rigid Plastic Containers

- 5.3.1.1.4 Metal Cans

- 5.3.1.1.5 Other Rigid Packaging

- 5.3.1.2 Flexible Packaging

- 5.3.1.3 Labels

- 5.3.1.4 Other Packaging

- 5.3.2 Commercial and Publication

- 5.3.3 Textiles

- 5.3.4 Other Applications

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Altana

- 6.4.2 Dainichiseika Color & Chemicals Mfg Co. Ltd

- 6.4.3 Dow

- 6.4.4 DuPont

- 6.4.5 Electronics For Imaging Inc.

- 6.4.6 Flint Group

- 6.4.7 FUJIFILM Corporation

- 6.4.8 Hubergroup Deutschland GmbH

- 6.4.9 Sakata Inx Corporation

- 6.4.10 Sicpa Holding SA

- 6.4.11 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.12 Sun Chemical

- 6.4.13 T&K TOKA Corporation

- 6.4.14 Tokyo Printing Ink Mfg Co. Ltd

- 6.4.15 Toyo Ink SC Holdings Co. Ltd

- 6.4.16 Wikoff Color Corporation

- 6.4.17 Zeller+Gmelin

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emergence of Bio-based and UV-curable Inks

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

United States Printing Ink Industry Segmentation

Printing inks consist of pigments or pigments of required color mixed with oil or varnish, majorly a black ink made from carbon blacks and thick linseed oil added. The market for printing inks is segmented by type, process, and application. By type, the market is segmented into solvent-based, water-based, oil-based, UV, UV-LED, and other types. By process, the market is segmented into lithographic printing, flexographic printing, gravure printing, digital printing, and other processes. By application, the market is segmented into packaging, commercial and publication, textiles, and other applications. The report offers market size and forecasts for printing ink in the United States in volume in kilo tons for all the above segments.

| Type | Solvent-based | |||

| Water-based | ||||

| Oil-based | ||||

| UV | ||||

| UV-LED | ||||

| Other Types | ||||

| Process | Lithographic Printing | |||

| Flexographic Printing | ||||

| Gravure Printing | ||||

| Digital Printing | ||||

| Other Processes | ||||

| Application | Packaging | Rigid Packaging | Paperboard Containers | |

| Corrugated Boxes | ||||

| Rigid Plastic Containers | ||||

| Metal Cans | ||||

| Other Rigid Packaging | ||||

| Flexible Packaging | ||||

| Labels | ||||

| Other Packaging | ||||

| Commercial and Publication | ||||

| Textiles | ||||

| Other Applications | ||||

Need A Different Region or Segment?

Customize Now

United States Printing Ink Market Research FAQs

What is the current United States Printing Inks Market size?

The United States Printing Inks Market is projected to register a CAGR of greater than 2.75% during the forecast period (2025-2030)

Who are the key players in United States Printing Inks Market?

Sun Chemical, Flint Group, Sakata Inx Corporation, Siegwerk Druckfarben AG & Co. KGaA and Hubergroup Deutschland GmbH are the major companies operating in the United States Printing Inks Market.

What years does this United States Printing Inks Market cover?

The report covers the United States Printing Inks Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United States Printing Inks Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

United States Printing Inks Market Research

Mordor Intelligence provides a comprehensive analysis of the printing inks industry, drawing on decades of expertise in technical market research. Our extensive coverage includes all major segments such as screen printing ink, flexographic ink, and gravure ink technologies. We also explore emerging solutions like conductive ink and inkjet ink systems. The report offers detailed insights into various applications, ranging from offset printing ink and lithographic ink processes to specialized industrial ink uses. This information is available in an easy-to-download report PDF format.

Our analysis benefits stakeholders across the value chain by offering a detailed examination of digital printing ink trends, packaging ink developments, and textile printing ink innovations. The report thoroughly investigates niche segments, including security printing ink, commercial printing ink, and newspaper printing ink sectors. It also covers publication ink, ceramic printing ink, and metal decorating ink applications. This comprehensive research enables businesses to make informed decisions based on current market dynamics and future growth opportunities in the printing inks industry.