United States Pharmaceutical Warehousing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

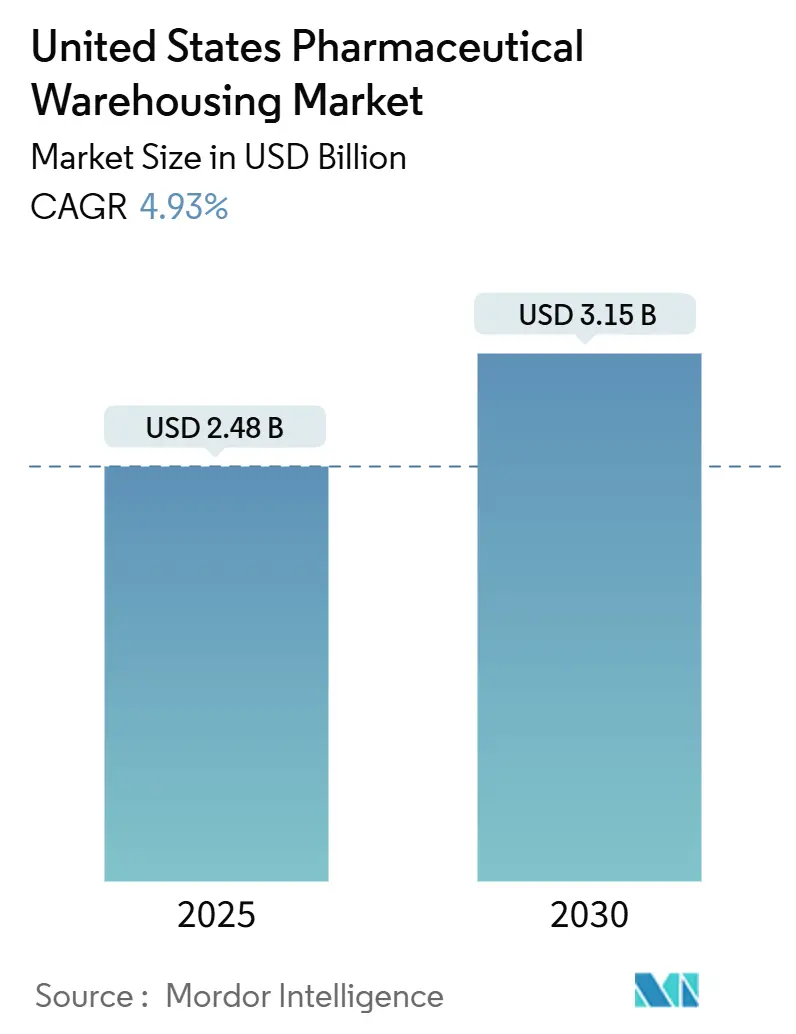

| Market Size (2025) | USD 2.48 Billion |

| Market Size (2030) | USD 3.15 Billion |

| Growth Rate (2025 - 2030) | 4.93% CAGR |

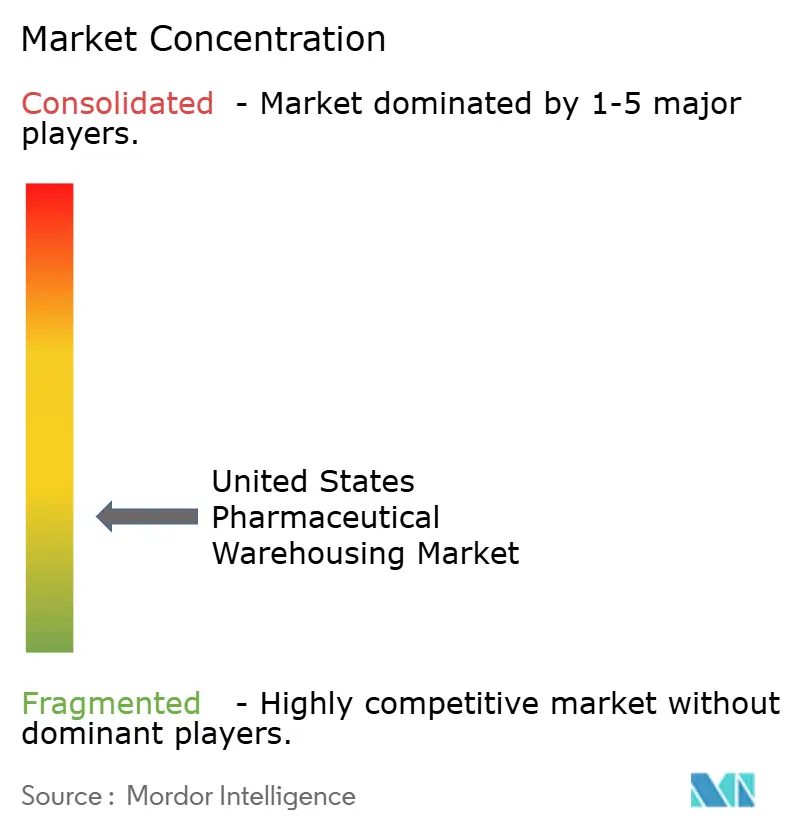

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Pharmaceutical Warehousing Market Analysis by Mordor Intelligence

The United States Pharmaceutical Warehousing Market size is estimated at USD 2.48 billion in 2025, and is expected to reach USD 3.15 billion by 2030, at a CAGR of 4.93% during the forecast period (2025-2030).

Rising biologics output, full enforcement of the DSCSA serialization rule, and surging e-commerce fulfillment volumes are channeling new capital into temperature-controlled infrastructure and automation. Cell and gene therapy pipelines are adding ultra-low temperature requirements that lift revenue per square foot, while secure track-and-trace systems mandated by 21 CFR 211.142 are reshaping warehouse IT budgets. Cost headwinds energy, real estate and specialized labor remain pronounced, yet continuous investment in robotics, IoT sensors and green cold-chain designs is improving operating leverage. Intensifying consolidation among third-party logistics (3PL) leaders aims to capture higher-margin healthcare contracts and defend share against vertically integrating manufacturers and health-system operators.

Key Report Takeaways

- By service type, Distribution and Inventory Management captured 45.87% of the United States pharmaceutical warehousing market share in 2024, whereas value-added services are forecast to advance at a 6.06% CAGR through 2030.

- By warehouse type, non-cold-chain facilities held 58.65% of the United States pharmaceutical warehousing market size in 2024, while cold-chain capacity is expanding at a 6.34% CAGR to 2030.

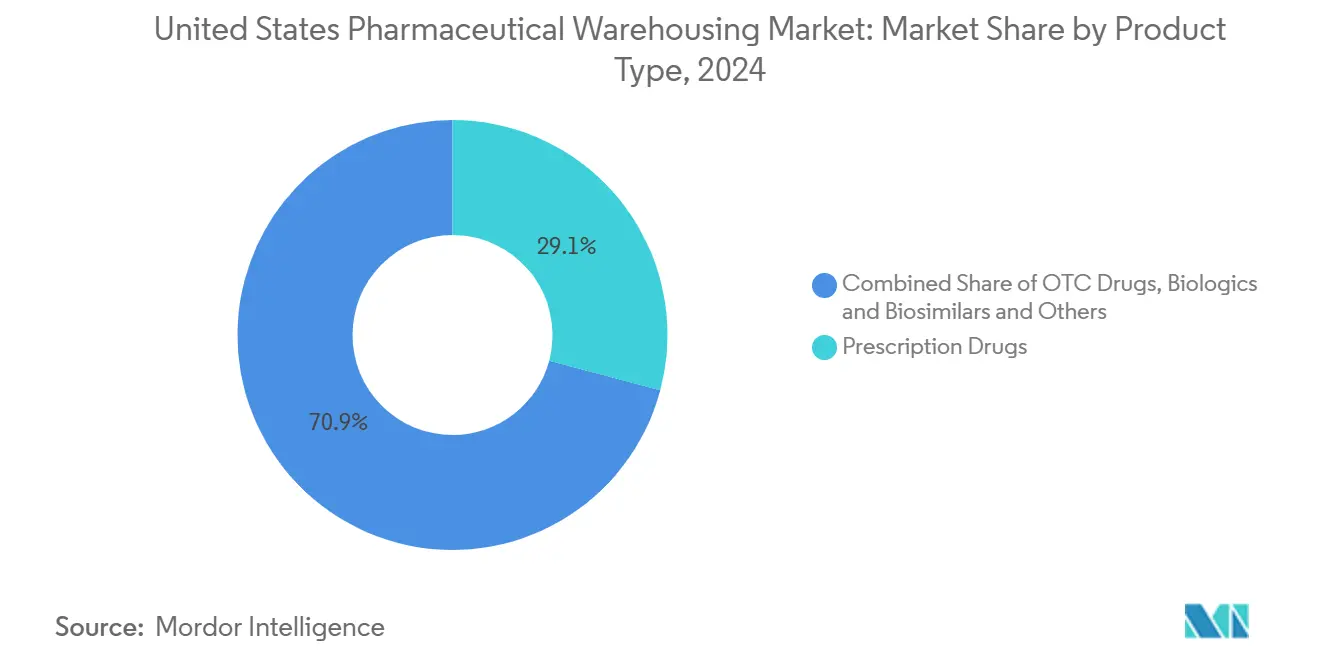

- By product type, prescription drugs led with 29.14% revenue share in 2024; cell and gene therapies are projected to grow at 8.86% CAGR through 2030.

- By end user, pharmaceutical manufacturers accounted for 33.04% of demand in 2024, while healthcare providers record the fastest growth at a 5.95% CAGR on vertical-integration moves.

United States Pharmaceutical Warehousing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust the United States pharmaceutical output | +1.2% | NJ, CA, NC | Medium term (2-4 years) |

| Expansion of 2-8 °C and ultra-low storage | +0.8% | Northeast & West Coast | Long term (≥ 4 years) |

| Growing biologics and specialty-drug volumes | +1.5% | Boston, SF, Research Triangle | Long term (≥ 4 years) |

| Rapid B2B/B2C e-commerce fulfillment | +0.9% | National urban hubs | Short term (≤ 2 years) |

| DSCSA serialization compliance | +0.6% | Nationwide | Medium term (2-4 years) |

| Urban micro-fulfillment proximity | +0.7% | NYC, LA, Chicago, Dallas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust Growth of U.S. Pharmaceutical Output

Annual capital spending of USD 160 billion in 2025 up 15% from 2024 couples every USD 1 billion invested with 2.3 million sq ft of extra warehouse need. Biologics represent 44% of new builds, prompting modular layouts that can flex with continuous-manufacturing schedules. FDA support for Advanced Manufacturing Technologies is accelerating real-time monitoring adoption, pushing facilities to embed redundant power and data systems. Decentralized production of cell therapies is spawning micro-warehouses near treatment centers, eroding the legacy hub-and-spoke network. These shifts collectively lift demand for secure, high-throughput storage nodes across the United States pharmaceutical warehousing market.

Expansion of Temperature-Controlled Storage Needs

Ultra-low requirements from mRNA vaccines (-80 °C) to cryogenic therapies (-196 °C) are now mainstream, raising energy use 20-30% above ambient operations rules under 21 CFR 600.15 mandate precise ranges, prompting IoT-enabled validations and alarm redundancies[1] “21 CFR 211.142—Warehousing Procedures,” FDA, ecfr.gov . Sustainability targets are spurring reusable shippers that cut fossil-fuel reliance 60%. Operators retrofit high-efficiency compressors and LED lighting to curb consumption, yet capital intensity remains a barrier for smaller entrants. Consequently, cold-chain capacity garners pricing power within the United States pharmaceutical warehousing market.

Surge in Biologics & Specialty-Drug Volumes

More than 1,000 ongoing cell and gene therapy trials necessitate sterile, multi-temperature zones and chain-of-custody tracking. Personalized batches elevate handling complexity 35% over traditional drugs, but premium reimbursement offsets added cost. European ATMP guidelines are informing United States builds, leading to stringent biological-variability controls in storage. Failure-mode analyses reveal cold-chain breaches cost USD 35 billion annually, sustaining investment in predictive analytics. As biologics pipelines proliferate, specialty capacity tightens across the United States pharmaceutical warehousing market, rewarding first movers.

Rapid B2B/B2C E-commerce Fulfillment Requirements

Amazon Pharmacy aims to cover 45% of Americans with same-day service by 2025. Micro-fulfillment nodes as small as 10,000 sq ft integrate robotics that pick 250 cases per hour, raising inventory velocity 15%. Warehouse management systems must reconcile DSCSA mandates with parcel-level accuracy, spawning API-rich platforms. Health-system chains replicate retail playbooks to control specialty spend, widening customer expectations for near-instant availability. This omni-channel pressure amplifies throughput demand inside the United States pharmaceutical warehousing market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent FDA cGMP & GDP costs | -0.4% | High-cost coasts | Long term (≥ 4 years) |

| Rising energy & real-estate costs | -0.6% | CA, Northeast metros | Medium term (2-4 years) |

| Labor shortages & automation skill gaps | -0.3% | Nationwide | Short term (≤ 2 years) |

| Cybersecurity vulnerabilities | -0.2% | Integrated networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent FDA cGMP & GDP Compliance Costs

Continuous temperature logging, electronic tracing and quarantine zones add 25% to 2025 compliance budgets. DSCSA serialization systems cost USD 0.5-2 million per facility, stretching small operators; 26% remain non-compliant post-stabilization[2]ISPE, “Cell and Gene Therapies & Their GMP Requirements,” ispe.org. Penalties range from fines to criminal liability, accelerating consolidation. Documentation load drives demand for third-party specialists, yet shrinks margins for commodity storage. This regulatory burden dampens the growth curve of the United States pharmaceutical warehousing market.

Rising Energy and Real-Estate Costs for Cold Storage

Cold facilities spend over USD 13,000 yearly on utilities, with refrigeration drawing 79% of electricity. Los Angeles warehouse rents hit USD 18-22 per sq ft against a national average of USD 9.00. Ultra-low freezers add USD 750-1,000 each in annual power outlay. Energy-efficient retrofits promise 15-20% savings but entail heavy capex. These dual cost curves erode operator profitability inside the United States pharmaceutical warehousing market.

Segment Analysis

By Service Type: Storage Dominance Drives Infrastructure Investment

Distribution and Inventory Management generated 45.87% of 2024 revenue, a testament to long-term contracts that stabilize cash flows within the United States pharmaceutical warehousing market. Value-added offerings—serialization, kitting and regulatory documentation—are scaling at a 6.06% CAGR as DSCSA enforcement tightens. Cloud-based WMS solutions now cover 90% of facilities, enhancing visibility and audit readiness[3]“GDP in the US: DSCSA Updates,” GMP-Compliance, gmp-compliance.org.

Value-added services typically bill 25-40% above baseline rates, offsetting compliance overhead. Robotics-as-a-Service models lower entry barriers for mid-tier operators, supporting market fragmentation while bolstering efficiency. FDA 21 CFR 205.50 stipulates secure storage and handling, favoring providers that can turnkey compliance at scale. These dynamics reinforce storage as the anchor while upgrading service complexity across the United States pharmaceutical warehousing market.

Note: Segment shares of all individual segments available upon report purchase

By Warehouse Type: Cold-Chain Expansion Accelerates Despite Cost Pressures

Non-cold-chain sites still constitute 58.65% of the United States pharmaceutical warehousing market size, but cold-chain capacity is outpacing at a 6.34% CAGR through 2030. Chilled, frozen and ultra-low zones command rates 150-200% higher than ambient alternatives, compensating for energy drain.

Operators retrofit ambient structures with modular cool chambers to balance flexibility and capex. IoT sensors cut temperature excursion risk 60%, curbing USD 35 billion annual losses industry-wide temperature mandates create high compliance hurdles, shielding incumbents. As biologics pipelines swell, cold-chain share will progressively rise within the United States pharmaceutical warehousing market.

By Product Type: Prescription Drugs Lead While Cell Therapies Surge

Prescription drugs maintained 29.14% share in 2024, underpinned by volume stability and efficient parcel networks[4]“How AI Is Transforming Warehouse Efficiency,” Automate.org, automate.org. In contrast, cell and gene therapies clock a 8.86% CAGR, leveraging premium storage fees tied to cryogenic handling.

Medical devices and diagnostics piggyback on pharmaceutical logistics, broadening revenue diversity. Vaccine distribution depends on ultra-cold lanes costing USD 750-1,000 annually per freezer. Personalized medicine elevates tracking complexity 40%, driving investment in advanced WMS and blockchain. These shifts diversify throughput across the United States pharmaceutical warehousing market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Manufacturers Dominate While Healthcare Providers Integrate Vertically

Pharmaceutical Manufacturers contributed 33.04% of 2024 revenue, preferring 3PLs for non-core logistics to preserve R&D focus. Health-system warehouses are growing 5.20% CAGR as providers insource specialty drug management to control costs.

Distributor consolidation centers inventory at mega-nodes in Texas and Pennsylvania, leveraging economies of scale. Specialty pharmacies inside hospital networks demand secure, multi-temperature micro-sites, intensifying capex. AI-driven demand forecasting curbs waste of short-shelf-life biologics, reinforcing vertical integration gains. These patterns reshape customer demand across the United States pharmaceutical warehousing market.

Geography Analysis

The Northeast remains the nation’s densest cluster thanks to proximity to pharma R&D hubs; Northern New Jersey rents average USD 16-20 per sq ft, the highest in the United States pharmaceutical warehousing market. Dallas–Fort Worth leads sheer capacity at 613 million sq ft, leveraging central geography and low taxes. Phoenix’s 44% footprint hike reflects California overflow, with rents at USD 6-8 per sq ft. Savannah’s 64% surge underscores port-led import flow, especially APIs.

California retains specialized biologics storage despite USD 18-22 rates, while ambient overflow migrates inland. The Midwest offers near-optimal single-warehouse reach; Vincennes, Indiana, yields 2.29-day national transit averages. Energy and labor variability across states yields 15-20% operating cost swings, influencing site selection.

Uniform FDA oversight keeps compliance baselines constant, but utility incentives in the Southeast enhance cold-chain ROI. Real-estate constraints near Boston and San Francisco spur multistory builds, despite higher capex. Collectively, geography decisions pivot on balancing cost, proximity and regulatory risk across the United States pharmaceutical warehousing market.

Competitive Landscape

UPS heads the field with USD 91 billion revenue and 32 million sq ft, expanding cold network via Frigo-Trans and BPL acquisitions. FedEx operates 40 million sq ft and secured USD 400 million new healthcare contracts while upgrading sensor-based tracking. DHL earmarked USD 2.2 billion to double healthcare revenue to USD 10.8 billion by 2030, emphasizing green warehouses.

Technology is the key battleground: AI inventory, robotics picking and blockchain serialization yield 15-25% efficiency bumps. Amazon’s push to same-day coverage for 45% of citizens forces incumbents to deploy urban micro-fulfillment. Specialized cold-chain firms such as Lineage Logistics and Americold monetize deep-frozen know-how with premium SKUs.

Barriers include cGMP audits, DSCSA tech stack and skill shortages; yet entrants offering turnkey compliance and data analytics attract venture backing. Margin pressure in ambient storage triggers portfolio pruning, whereas biologics lanes support price resilience. Consolidation is likely to escalate, shaping capacity allocation within the United States pharmaceutical warehousing market.

United States Pharmaceutical Warehousing Industry Leaders

-

United Parcel Service Inc.

-

DHL Supply Chain

-

FedEx Corp.

-

GEODIS SA

-

CEVA Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: UPS Healthcare acquired Frigo-Trans and BPL to scale temperature-controlled capacity.

- February 2025: Trilantic Europe and Alto Partners merged Doppel Farmaceutici and Mipharm into Domixtar Pharmaceuticals.

- April 2024: Eli Lilly purchased Nexus Pharmaceuticals’ Wisconsin plant to boost injectable output.

- January 2024: Alcami bought Pacific Pharmaceutical Services, expanding CDMO warehousing.

United States Pharmaceutical Warehousing Market Report Scope

Warehouses are used by manufacturers, importers, exporters, wholesalers, transport businesses, customs, etc. Pharmaceutical Warehousing, therefore, is much more than the simple storage of products. It is an operation that preserves the integrity of drugs that affect health and well-being. Stored goods can include any pharmaceutical drugs raw materials, packing materials, and finished goods associated pharmaceutical sector.

The report sheds light on the market trends like growth factors, restraints, and opportunities in this sector. The competitive landscape of the United States Pharmaceutical Warehousing Market is depicted through the profiles of active key players. The report also covers the Impact of Geopolitics and Pandemic on the market and future projections.

The United States pharmaceutical warehousing market is segmented by service type (storage, distribution, inventory management, packaging and others) and by mode (cold chain warehouse, non-cold chain warehouse), and by end user (pharmaceutical companies, hospital and clinics, research institutes and government agencies and others). The report offers market size and forecasts for the United States pharmaceutical warehousing market in value (USD) for all the above segments.

| Storage |

| Distribution and Inventory Management |

| Value-added Services and Others |

| Cold-Chain Warehouse | Chilled (0-5°C) |

| Frozen (-18-0°C) | |

| Ambient | |

| Deep-Frozen / Ultra-Low (less than-20 °C) | |

| Non-Cold-Chain Warehouse |

| Prescription Drugs |

| OTC Drugs |

| Biologics and Biosimilars |

| Vaccines and Blood Products |

| Clinical Trail Materials |

| Cell and Gene Therapies |

| Specialty Medicine (non-biologic) |

| Veterinary Medicine |

| Others |

| Pharmaceutical Manufacturers |

| Healthcare Providers |

| Retail and Pharmacies |

| Distributors and Wholesalers |

| Others |

| By Service Type | Storage | |

| Distribution and Inventory Management | ||

| Value-added Services and Others | ||

| By Warehouse Type | Cold-Chain Warehouse | Chilled (0-5°C) |

| Frozen (-18-0°C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| Non-Cold-Chain Warehouse | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| Biologics and Biosimilars | ||

| Vaccines and Blood Products | ||

| Clinical Trail Materials | ||

| Cell and Gene Therapies | ||

| Specialty Medicine (non-biologic) | ||

| Veterinary Medicine | ||

| Others | ||

| By End User | Pharmaceutical Manufacturers | |

| Healthcare Providers | ||

| Retail and Pharmacies | ||

| Distributors and Wholesalers | ||

| Others | ||

Key Questions Answered in the Report

What is the 2025 value of the United States pharmaceutical warehousing market?

The sector is valued at USD 2.48 billion in 2025.

How fast is pharmaceutical cold-chain capacity growing in the United States?

Cold-chain warehousing is expanding at a 6.34% CAGR through 2030.

Which United States metro has the largest concentration of pharmaceutical warehouse space?

Dallas–Fort Worth leads with 613 million sq ft of distribution capacity.

Why are healthcare providers building their own warehouses?

Vertical integration helps hospitals control specialty-drug inventory and reduce procurement costs.

What technology investments are top 3PLs prioritizing?

Leaders are rolling out AI-driven inventory platforms, IoT temperature sensors and robotics to boost efficiency and maintain FDA compliance.

Page last updated on: