United States Pet Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

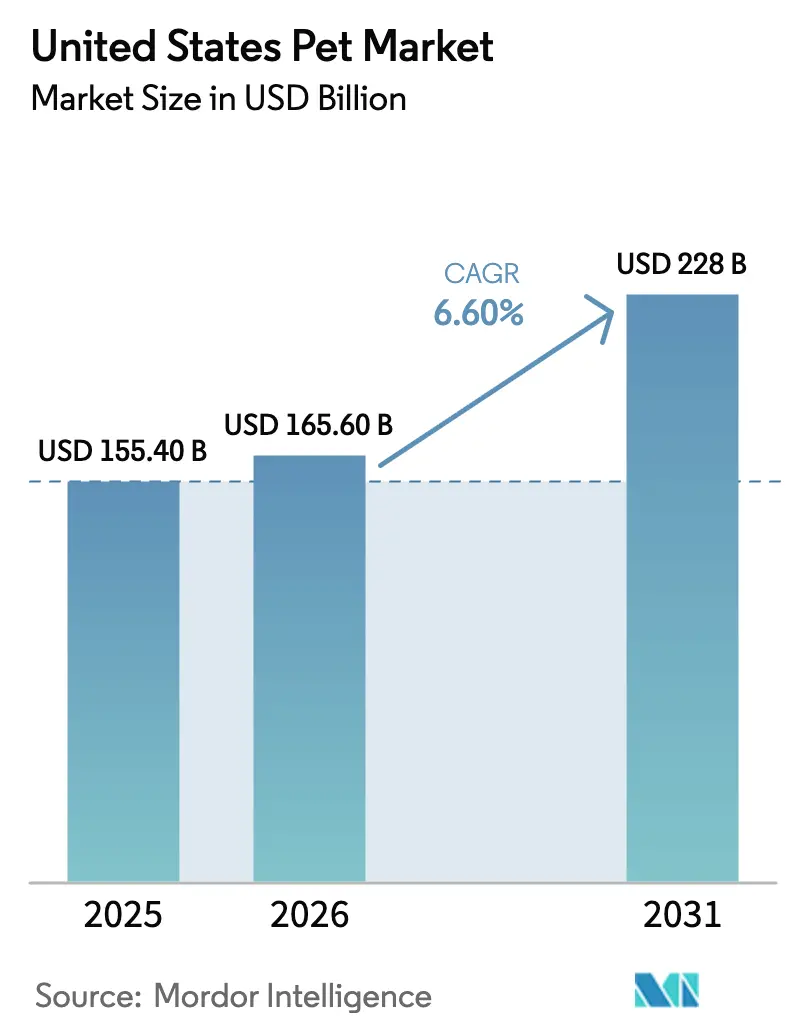

| Base Year Market Size (2025) | USD 155.40 Billion |

| Market Size (2026) | USD 165.60 Billion |

| Market Size (2031) | USD 228 Billion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

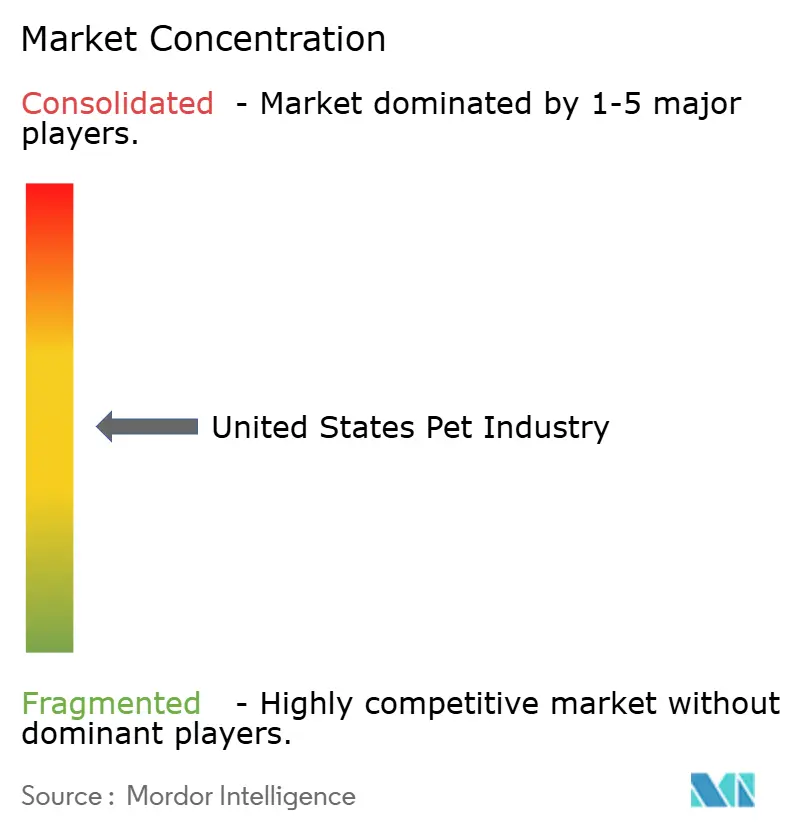

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Pet Market Analysis by Mordor Intelligence

The United States pet market was valued at USD 155.4 billion in 2025 and estimated to grow from USD 165.6 billion in 2026 to reach USD 228.0 billion by 2031, at a CAGR of 6.60% during the forecast period (2026-2031). This expansion demonstrates how pets have shifted from household companions to lifestyle investments, prompting stable demand for premium nutrition, preventive healthcare, and digitally enabled services. Rising employer-sponsored pet benefits, the popularity of fresh and frozen food, and streamlined drug approvals for companion animals are expanding the addressable market while protecting margins against inflation. Online autoship models, direct-to-consumer subscriptions, and omnichannel fulfillment continue to gain traction, reshaping the competitive cost structure and accelerating consolidation. At the same time, veterinary workforce shortages, extended producer responsibility packaging fees, and inflation-driven trade-down behavior temper above-trend growth, underscoring the need for strategic agility to remain critical for brand owners.

Key Report Takeaways

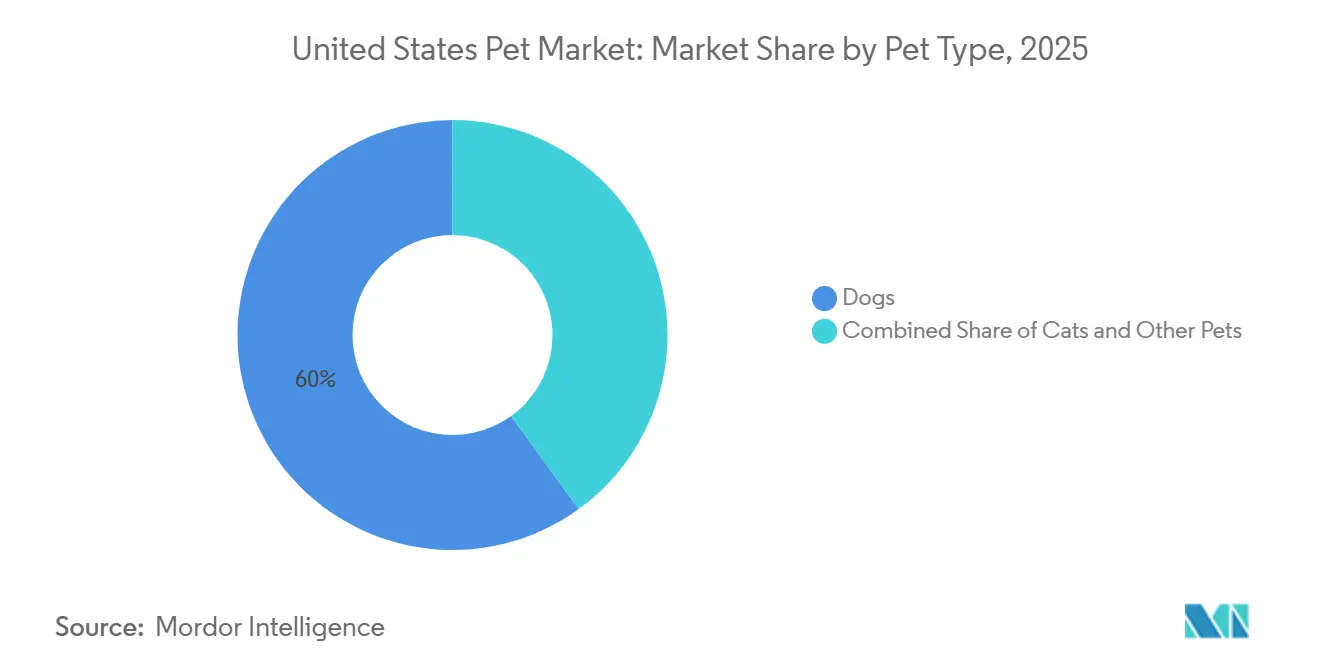

- By pet type, dogs captured 60% of the United States pet market share in 2025, while cats are advancing at a 7.8% CAGR through 2031.

- By product type, food commanded 38.7% of the United States pet market size in 2025, whereas services are forecast to expand at a 16.5% CAGR to 2031.

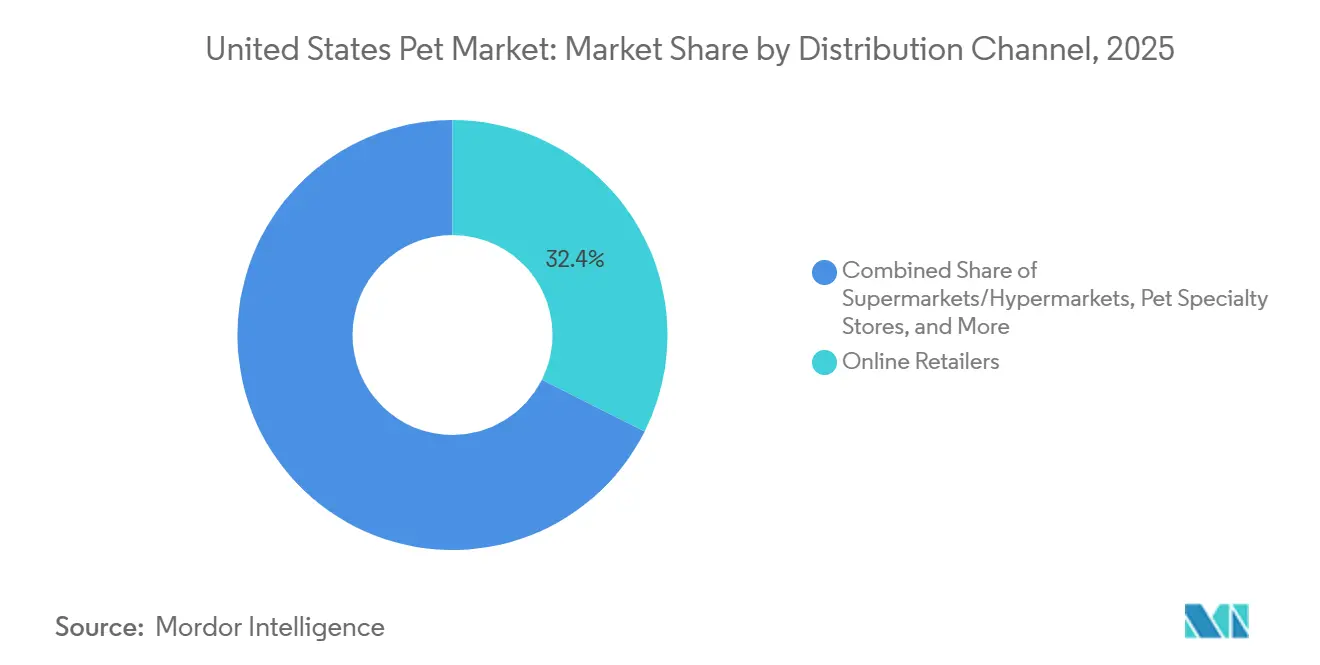

- By distribution channel, online retailers held 32.4% share of the United States pet market size in 2025, while direct-to-consumer brands are scaling at an 18.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Pet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Humanization-Driven Premium Spend | +1.80% | Urban coastal metros and nationwide midsize cities | Long term (≥ 4 years) |

| Accelerating E-commerce and Omnichannel Penetration | +1.50% | Metropolitan areas with same-day delivery infrastructure | Medium term (2-4 years) |

| Rising Pet-Insurance Adoption | +1.20% | States with high employer-benefit adoption and technology hubs | Medium term (2-4 years) |

| Employer-Sponsored Pet-Care Benefits Expansion | +0.70% | Fortune 500 headquarters and technology clusters | Long term (≥ 4 years) |

| FDA Fast-Track Pathway for Novel Therapeutics | +0.60% | Nationwide through FDA Center for Veterinary Medicine | Short term (≤ 2 years) |

| Climate-Resilient Novel Protein Sourcing | +0.50% | Nationwide supply chains and ingredient-sourcing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Humanization-Driven Premium Spend

Fresh and frozen meals have highlighted consumers' willingness to invest in minimally processed, nutritious options. The emphasis on premium offerings has expanded to include services such as grooming, behavioral training, and spa treatments, creating recurring revenue opportunities for specialty retailers. Transparency in product ingredients, including single-protein formulas and non-GMO (genetically modified organism) labels, strengthens brand loyalty among health-conscious pet owners. Additionally, social media platforms contribute to the normalization of high-end purchases by promoting aspirational pet lifestyles, thereby increasing peer-to-peer influence on purchasing decisions. Companies that integrate personalization and functional health claims continue to experience consistent demand for premium products, even during broader economic uncertainties.

Accelerating E-commerce and Omnichannel Penetration

Online channels captured a significant share of the United States pet market revenue in 2025, a share driven by autoship subscriptions that reduce churn and elevate lifetime value. E-retailer Chewy generated USD 11.86 billion in net sales for fiscal 2024, with the majority share derived from autoship customers. Brick-and-mortar chains responded by launching click-and-collect services, deploying mobile apps, and partnering with last-mile couriers to match the immediacy of pure plays. Direct-to-consumer newcomers leverage higher gross margins to fund agile innovation and rapid brand storytelling. This distribution shift compresses prices in commodity categories while widening the gap in premium, data-driven services.

Rising Pet-Insurance Adoption

Pet insurance penetration reached about 3.9% of the United States' pets in 2024, as employer subsidies expanded coverage and reduced out-of-pocket costs. Subscriber growth demonstrates how predictable premiums encourage pet owners to approve diagnostic testing and elective procedures. Aggressive pricing strategies by new entrants are expanding consumer options and increasing market awareness. While state-level regulation remains inconsistent, proposed model legislation under review seeks to standardize policy terms, potentially expanding the addressable market. Additionally, insurance adoption helps stabilize veterinary clinic revenue by mitigating seasonal fluctuations in visit frequency.

FDA Fast-Track Pathway for Novel Therapeutics

An expedited review process compressed approval timelines for monoclonal antibody therapies designed for osteoarthritis, with two treatments cleared in 2024 [1]Source: Association of American Feed Control Officials, “2025 Ingredient Definitions,” aafco.org. Faster market access encourages pharmaceutical firms to reallocate R&D budgets toward companion animals, a segment historically overshadowed by livestock. First movers gain a pricing window before biosimilars arrive, spurring additional research into chronic disease categories such as dermatology and oncology. The regulatory program aligns with broader digital health guidance, facilitating telemedicine integration and prescription fulfillment through online pharmacies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-Driven Trade-Down to Value Brands | −1.1% | Nationwide, most acute in lower-income and rural households | Short term (≤ 2 years) |

| Veterinary Workforce Shortage | −0.9% | Nationwide, severe in rural and underserved urban areas | Medium term (2-4 years) |

| Extended Producer-Responsibility Packaging Fees | −0.5% | California, Oregon, and Maine with additional states considering laws | Long term (≥ 4 years) |

| Social-Media Trend Volatility and Inventory Risk | −0.4% | Nationwide specialty retail and direct-to-consumer channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Trade-Down to Value Brands

Consumer budgets tightened in 2025 as food and energy prices rose, shifting demand toward private-label offerings at mass merchants. A leading warehouse club’s in-house pet food line gained share, compressing volume for mid-tier brands. Bank transaction data indicated that category spending grew just 3.2% in 2025, below long-term averages [2]Source: Bank of America Institute, “Consumer Spending Pulse 2025,” bankofamerica.com. Brands have responded with smaller pack sizes and value-tier extensions to preserve shopper loyalty. While inflation is projected to moderate, price sensitivity could outlast the immediate economic cycle, making portfolio depth essential for manufacturers.

Veterinary Workforce Shortage

Thirty-four percent of veterinarians reported burnout symptoms in 2025, intensifying capacity constraints at clinics [3]Source: American Veterinary Medical Association, “Workforce Report 2025,” avma.org. The average graduate debt deters new entrants from entering companion-animal practice, especially in rural communities. Appointment backlogs prolong elective procedures, curtailing sales of dental, orthopedic, and nutritional products. Telehealth triage and expanded technician scope offer partial relief but cannot fully replace in-person diagnostics. Unless enrollment and retention improve, the shortage will weigh on service revenues through at least 2029.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Cats Narrow the Gap

Dogs accounted for 60% of the United States pet market size in 2025, while cats are projected to outpace with a 7.8% CAGR through 2031. The faster feline trajectory stems from apartment-friendly ownership patterns among young professionals and the recent rollout of premium cat-specific nutrition, therapeutic, and insurance products. Other pets, such as birds, freshwater fish, reptiles, and small mammals, combined, represented comparatively less revenue, benefiting from specialized diets and habitat innovations that boost average basket size. Cats’ expanding penetration into employer-sponsored insurance programs reinforces the frequency of clinical care, narrowing historical disparities with canine coverage. Regulatory approvals, such as the monoclonal antibody for feline osteoarthritis in 2024, further catalyze veterinary spend and anchor the species’ upgrade cycle.

Lower ownership costs and an independent nature make cats attractive for urban dwellers, while social media visibility elevates their cultural status, propelling accessory and furniture purchases. Dogs retain leadership in services such as daycare, training, and outdoor gear, where behavioral complexity supports higher ticket prices. Reptile and exotic avian ownership is limited by interstate transport rules and veterinary accessibility, capping their upside despite niche enthusiasm. Small mammal sales remain stable, buoyed by educational campaigns underscoring responsible care. To succeed across species, manufacturers and retailers must tailor communication and product design to distinct behavioral and health drivers rather than adopting a monolithic strategy.

By Product Type: Services Outpace Goods

Food maintained a 38.7% share of the United States pet market size in 2025, but services are projected to deliver the fastest growth at a 16.5% CAGR. Dry kibble remains the primary choice for pet nutrition. However, fresh and frozen formats are experiencing double-digit growth due to consumer preference for minimally processed diets. Treats and chews account for a substantial share of pet food demand, with functional benefits, including dental health and joint support, increasingly influencing impulse purchases. Pet supplements featuring ingredients like glucosamine, probiotics, and cannabidiol are gaining initial consumer acceptance. Nevertheless, wider retail adoption will require clearer guidance from the United States Food and Drug Administration regarding cannabidiol labeling and claims.

In the services segment, veterinary care remains the largest revenue-generating category. However, growth is limited by shortages of qualified veterinarians and support staff. Boarding and daycare services are recovering as return-to-office trends continue, while pet training is transitioning to virtual formats, reducing geographic barriers and improving accessibility. Supplies maintain stable revenue streams through categories such as grooming products, toys, and non-prescription health treatments. Companies that integrate physical products with service-based ecosystems, such as combining pet insurance with preventive care programs, are well-positioned to capture a larger share of overall pet care spending.

By Distribution Channel: Digital Dominance Accelerates

Online retailers captured 32.4% of the United States pet industry size in 2025, and direct-to-consumer players are scaling at an 18.9% CAGR through 2031. Autoship programs lock in predictable demand, enabling retailers to negotiate favorable supplier terms and reinvest in customer experience. Direct-to-consumer brands achieve profitability by bypassing traditional retail channels, enabling reinvestment in data-driven personalization and customer engagement strategies. Supermarkets and hypermarkets remain significant due to their convenience and ability to drive impulse purchases, though they face growing competition from private-label products. Mass merchants and club stores continue to appeal to value-conscious consumers through bulk packaging and promotional pricing.

Pet specialty retailers have experienced some decline in market share as omnichannel competitors replicate loyalty programs and service-oriented features. Veterinary clinics retain a niche role in distributing prescription diets and therapeutic products. With the convergence of digital and physical channels, retailers are increasingly required to integrate inventory management, pricing, and loyalty data across platforms. Future competitive advantages will depend on investments in last-mile fulfillment, telehealth services, and app-based consumer engagement.

Geography Analysis

Regional demand patterns within the United States pet market vary across the country, reflecting differences in income, population density, and cultural attitudes. Coastal metro areas such as New York, Los Angeles, and Seattle demonstrate the highest per-pet spend, propelled by premium nutrition adoption and employer-sponsored benefits. These markets also post the quickest uptake of telehealth and autoship services, leveraging robust last-mile infrastructure. In contrast, the Midwest and South contribute a larger absolute number of pets but tend to skew toward value-oriented purchases, resulting in higher private-label penetration than the national average.

Rural regions contend with veterinary access gaps exacerbated by workforce shortages, limiting growth in elective procedures and advanced therapeutics. However, direct-to-consumer channels and mobile clinics partially offset clinic scarcity by enabling home delivery of prescription diets and remote consultations. Environmental sustainability resonates more in West Coast states, where extended producer responsibility legislation drives packaging innovation and influences purchasing decisions. States with booming technology sectors Texas, Colorado, and North Carolina, reflect elevated insurance adoption rates, mirroring employer benefit trends.

Weather events also shape regional buying cycles. Hurricane-prone Gulf states witness spikes in emergency preparedness products, including portable kennels and long-life food. Snowbelt areas see higher winter sales of protective apparel and paw balms. Urban apartment restrictions in Northeastern cities fuel cat ownership, whereas suburban Sunbelt communities favor dogs and outdoor accessories. Understanding these micro-geographic nuances allows brands to tailor inventory, promotions, and messaging to maximize regional relevance.

Competitive Landscape

The United States pet market exhibits moderate market concentration, with the top five companies accounting for the majority of the market size in 2025. Mars, Incorporated leads the market with a diverse portfolio covering multiple price tiers and species categories. Nestle S.A. (Purina) leverages its strong research and development capabilities to offer science-backed formulations and veterinarian-aligned products. Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), The J. M. Smucker Company, and General Mills Inc. round out the leading players, each focusing on specific segments such as clinical nutrition, value-oriented offerings, or natural and premium pet food. Meanwhile, direct-to-consumer companies like The Farmer’s Dog, Inc. are gaining popularity among younger, urban pet owners by offering fresh, human-grade meals as a premium yet accessible option.

Established companies are addressing these disruptions through omnichannel strategies, subscription-based models, and acquisitions of niche innovators. A 2025 patent awarded to Mars for a predictive nutrition engine drawing on wearable biometrics exemplifies how data analytics underpin personalized offerings [4]Source: United States Patent and Trademark Office, “US 11,345,678 B2 Personalized Pet Nutrition,” uspto.gov. These efforts are increasingly supported by data analytics and personalization technologies. Retailers are also pursuing vertical integration by incorporating veterinary services into store networks, aiming to capture a larger share of pet healthcare spending and enhance customer loyalty.

Private equity involvement remains robust, driving consolidation among independent veterinary practices and mid-sized nutrition brands. E-commerce platforms are investing in telehealth, pharmacy integration, and artificial intelligence-enabled customer support. As digital-native barriers to entry decrease and regulatory and compliance requirements grow more stringent, competitive advantage is shifting from scale alone to capabilities in data utilization, fulfillment efficiency, and regulatory expertise.

United States Pet Industry Leaders

Mars, Incorporated

Nestle S.A.(Purina)

The J. M. Smucker Company

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

General Mills Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mars, Incorporated opened a USD 450 million Royal Canin plant in Ohio, which produces diets for approximately 4 million pets annually. The added capacity shortens lead times for veterinary-recommended formulas, supporting the scale-up of fresh food and improving mid-Western cold-chain availability.

- February 2025: Colgate-Palmolive acquired Care TopCo Pty Ltd, owner of the Prime100 fresh-pet-food line, to expand Hill’s Pet Nutrition into refrigerated meals. The move pushes mainstream vet-endorsed brands into the fresh segment, accelerating category blurring between therapeutic and everyday diets.

- November 2024: General Mills Inc. finalized its USD 1.45 billion purchase of Whitebridge Pet Brands, adding Tiki Pets and Cloud Star treats to the Blue Buffalo franchise. Portfolio expansion strengthens General Mills’ cat presence and raises innovation stakes in functional treats, spurring faster SKU rotation at specialty retail.

- January 2024: The Association of American Feed Control Officials (AAFCO) has approved Ÿnsect’s dried mealworm meal for use in the United States pet foods, marking the first nationwide green light for insect protein. Regulatory clearance de-risks alternative proteins, opening supply options that can ease pressure on traditional animal and plant sources.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States pet market as the aggregate annual spend on companion-animal food, treats, non-food supplies, veterinary care, and non-medical services purchased for dogs, cats, birds, fish, reptiles, and small mammals. Values are stated in retail and clinic revenues captured inside the United States, expressed in current-year US dollars.

Scope Exclusions: livestock feed, commercial aquaculture inputs, equine racing, and farm animal health services fall outside this boundary.

Segmentation Overview

- By Pet Type

- Dog

- Cat

- Other Pets

- By Product Type

- Food

- Dry Kibble

- Wet / Canned

- Fresh / Frozen

- Treats and Chews

- Supplements

- Supplies

- Grooming and Hygiene

- Toys and Enrichment

- Bedding and Habitat

- Other Supplies

- Services

- Veterinary Care

- Insurance

- Boarding and Day-care

- Training and Behavior

- Food

- By Distribution Channel

- Supermarkets / Hypermarkets

- Mass Merchandisers / Club

- Pet Specialty Stores

- Veterinary Clinics

- Online Retailers

- Direct-to-Consumer Brands

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts next held structured interviews and short surveys with veterinary practitioners, multi-unit specialty retailers, online subscription providers, ingredient suppliers, and pet insurance brokers across the Northeast, Midwest, South, and West. These conversations clarified ownership dynamics, average spend, emerging service formats, and price transmission, which we then triangulated with the desk findings.

Desk Research

We begin by mapping the market universe through freely available, high-credibility sources such as the American Pet Products Association fact sheets, USDA household expenditure tables, Bureau of Labor Statistics CPI microdata for pet food inflation, US Census e-commerce retail series, and AVMA pet ownership surveys. Company 10-Ks, investor decks, and leading trade journals complement these datasets, while D&B Hoovers and Dow Jones Factiva help validate firm-level revenues and channel shifts. The sources quoted here are illustrative; many additional databases and public records were examined to construct the evidence base.

Market-Sizing & Forecasting

A combined top-down, bottom-up model underpins the estimates. Top-down reconstruction starts with reported household pet counts, average category spend, and veterinary visit frequency, adjusted for CPI and channel mix. Bottom-up checks roll up sampled supplier shipments and clinic invoices where accessible, providing a guardrail against over- or under-estimation. Key variables include dog- and cat-owning households, online share of pet food sales, median vet invoice, insured-pet penetration, and pet population growth. Forecasts through 2030 employ multivariate regression with lagged GDP-per-capita, pet population elasticity, and inflation expectations, moderated by expert consensus on price promotions and premiumization. Data gaps, especially in services, are bridged with conservative penetration assumptions validated through follow-up calls.

Data Validation & Update Cycle

Model outputs pass variance checks against independent spend trackers, and anomalies trigger re-runs before sign-off. A senior analyst reviews every calculation line. We refresh the dataset each year and issue interim revisions if material events, such as sudden regulatory shifts or pandemic impacts, alter market dynamics.

Why Mordor's US Pet Market Baseline Commands Reliability

Published figures often diverge because providers differ on which pet categories to include, how to treat clinic mark-ups, and the cadence of currency updates.

Key gap drivers lie in scope; some reports omit services, ASP progression logic, and refresh timing versus rapidly shifting e-commerce shares. Mordor's disciplined definition, variable tracking, and annual refresh narrow these gaps and give decision-makers a dependable starting point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| $157 B (2025) | Mordor Intelligence | - |

| $152 B (2024) | Trade Association A | excludes online-only DTC brands; prior year base |

| $67.5 B (2024) | Global Consultancy B | counts products only, omits vet and service spend |

| $29.9 B (2024) | Industry Report C | focuses on durable hard goods, excludes consumables |

In sum, while other publishers offer valuable snapshots, their narrower scopes or older baselines understate the full economic footprint. Mordor's method stitches together consistent category coverage, multi-source validation, and clearly logged assumptions, giving clients a transparent, repeatable benchmark they can trust when sizing opportunities or stress-testing strategies.

Key Questions Answered in the Report

What is the size of pet spending in the United States in 2026, and what is it anticipated to reach by 2031?

Outlays totaled USD 165.6 billion in 2026 and are projected to climb to USD 228 billion by 2031.

Which pet species is projected to grow the fastest through 2031?

Cats are forecast to advance at a 7.8% CAGR through 2031, outpacing dogs and narrowing the spending gap.

What are the main risks that could slow growth over the next two to four years?

Inflation-linked trade-down to private-label goods, veterinary workforce shortages, and social-media-driven inventory volatility all weigh on near-term performance.

Which regulatory development is accelerating new therapeutics for companion animals?

The FDA (Food and Drug Administration) Center for Veterinary Medicine’s fast-track review pathway has shortened approval timelines for innovative drugs such as monoclonal antibodies targeting osteoarthritis.

Page last updated on: