Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

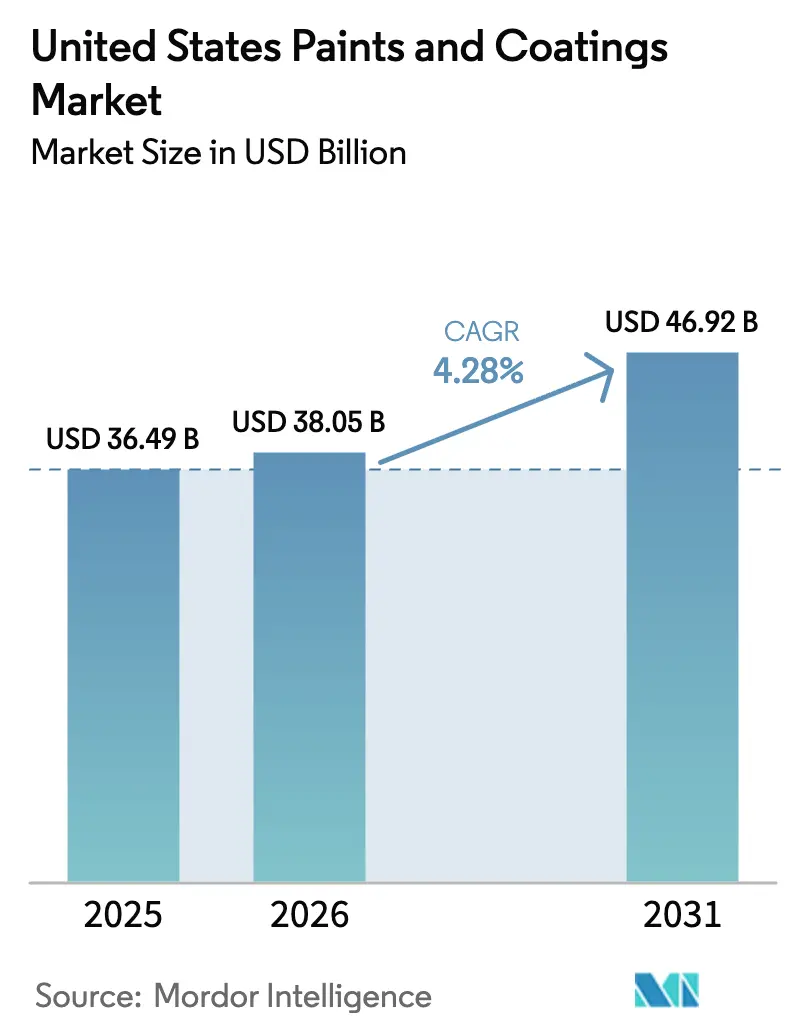

| Base Year Market Size (2025) | USD 36.49 Billion |

| Market Size (2026) | USD 38.05 Billion |

| Market Size (2031) | USD 46.92 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

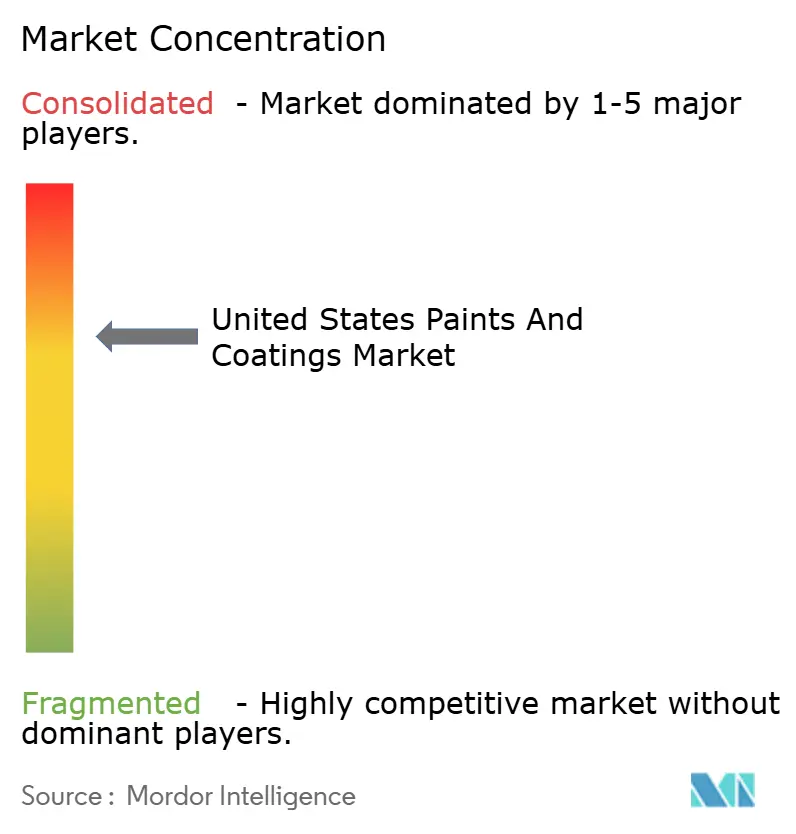

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Paints And Coatings Market Analysis by Mordor Intelligence

The United States Paints and Coatings Market size is projected to expand from USD 36.49 billion in 2025 and USD 38.05 billion in 2026 to USD 46.92 billion by 2031, registering a CAGR of 4.28% between 2026 to 2031. Infrastructure outlays under the Infrastructure Investment and Jobs Act, consistent home-remodeling activity, and rapid diffusion of water-borne as well as UV-curable technologies are the primary engines behind this expansion. Federal bridge and highway budgets lengthen project backlogs for protective-coatings suppliers, while a buoyant residential remodeling pipeline supports architectural volumes. Technology shifts toward low-volatile-organic-compound (VOC) systems let manufacturers safeguard their share amid stricter state rules, especially in California and the Northeast. On the demand side, electric-vehicle (EV) finishes that tolerate aluminum and composite substrates lift average selling prices within automotive original equipment manufacturer (OEM) coatings. Channel dynamics are equally influential: company-owned stores still dominate professional sales, but big-box retailers are enlarging pro desks and click-and-collect options to capture contractor loyalty.

Key Report Takeaways

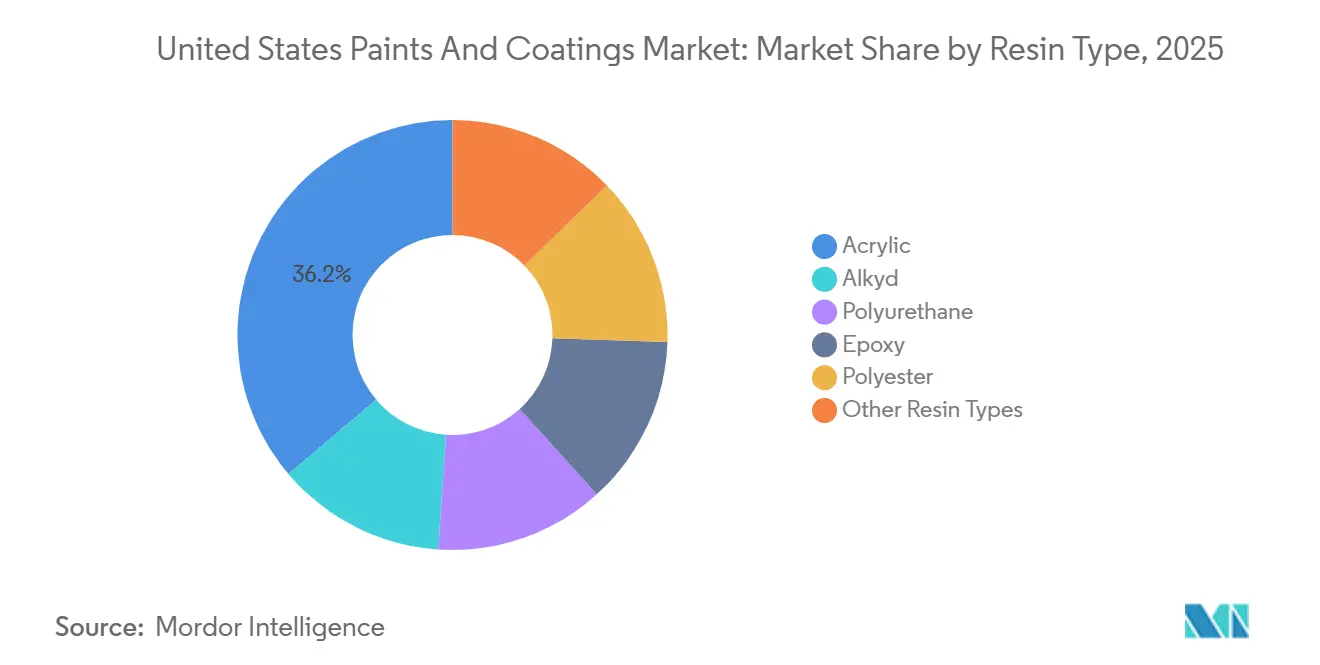

- By resin type, acrylic captured 36.18% of the United States paints and coatings market share in 2025; polyurethane is forecast to expand at a 5.16% CAGR through 2031.

- By technology, water-borne formulations accounted for 68.24% of the United States paints and coatings market size in 2025 and are advancing at a 5.36% CAGR through 2031.

- By distribution channel, company-owned stores held 40.66% revenue in 2025, while big-box retailers and home centers recorded the fastest 7.04% CAGR to 2031.

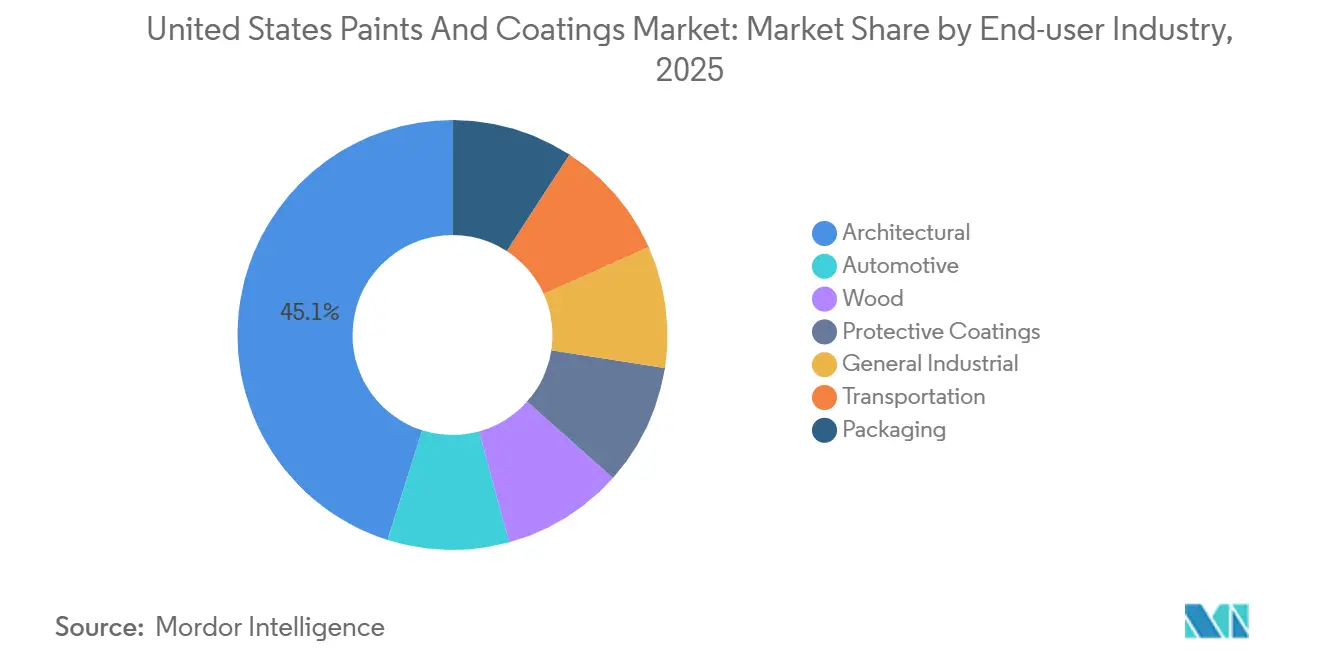

- By end-user industry, architectural coatings represented 45.12% value in 2025 and are growing at a 5.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Paints And Coatings Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal Infrastructure and Jobs Act boosts bridge/highway coatings | +0.8% | National, with concentration in Midwest and Northeast corridors | Medium term (2-4 years) |

| Home-remodeling boom lifts DIY architectural demand | +1.2% | National, strongest in Sun Belt and coastal metros | Short term (≤ 2 years) |

| Shift to water-borne and UV-curable systems to meet VOC rules | +0.9% | National, California and Northeast states leading | Medium term (2-4 years) |

| Automotive production rebound raises OEM and refinish volumes | +0.6% | Midwest manufacturing belt, Southern EV assembly hubs | Short term (≤ 2 years) |

| Antimicrobial coatings adoption in healthcare facilities | +0.3% | National, urban hospital systems and long-term care facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal Infrastructure Spending Propels Protective Coatings

The allocation for roads and bridges is driving demand for zinc-rich primers, epoxies, and polyurethane topcoats, all promising a 25-year service life[1]United States International Trade Commission, “USMCA Rules of Origin Economic Impact Report 2024,” usitc.gov. Contractors are leaning towards single-coat products like Sherwin-Williams' Acrolon 680, which not only reduces lane-closure time but also adheres to strict SSPC specifications. Suppliers boasting NORSOK and ISO performance records are reaping premium margins, and steel fabrication hubs in the Midwest are witnessing a boost in orders, thanks to bridge refurbishments.

Home-Remodeling Boom Bolsters Architectural Paints

By Q3 2025, Harvard’s Joint Center for Housing Studies projects residential remodeling outlays to grow steadily, underscoring the resilience of do-it-yourself (DIY) demand. In fiscal 2024, Home Depot reported strong paint sales. This surge in sales led Home Depot to bolster its pro-contractor platform, following its acquisition of SRS Distribution. In 2024, Sherwin-Williams expanded its footprint by adding more stores, optimizing its network for same-day deliveries. Meanwhile, BEHR capitalized on its exclusive partnership with Home Depot, significantly contributing to Masco's revenue. Although e-commerce accounts for a modest share of paint sales, there's a notable uptick in repeat orders through click-and-collect, particularly benefiting contractors with tight job schedules.

Low-VOC Systems Gain Share Under Stricter Rules

In January 2025, the EPA tightened VOC ceilings for aerosol coatings, pushing formulators to adopt acrylic and polyurethane dispersions with emissions below 50 g/L. Water-borne products continue to dominate the market and show strong growth potential among technologies. PPG's DuraNext line, a UV-curable product, alongside Allnex's UV powder resins, achieved near-zero emissions and rapid line speeds, aiding manufacturers in meeting ISO 14067's carbon footprint standards. California's South Coast district has set a national benchmark, prompting quicker adoption in other states.

Automotive Recovery Lifts OEM Coatings

PPG's automotive OEM division reported a sales increase in Q3 2025, driven by the growing demand for premium EV color packages and specialized conductive primers designed for aluminum bodies. While refinish volumes dipped, attributed to a decline in collisions, this was counterbalanced by robust OEM demand from Southern EV plants. As the megacasting trend gains traction, there's a heightened need for coatings that cure swiftly on larger components. This has catalyzed research and development efforts towards developing new polyurethane clear coats with expedited bake cycles.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ prices compress margins | -0.7% | National, acute for architectural and general industrial segments | Short term (≤ 2 years) |

| Shortage of certified industrial painters delays projects | -0.2% | National, concentrated in Gulf Coast petrochemical corridor | Medium term (2-4 years) |

| Freight-cost inflation disrupts retailer inventory cycles | -0.4% | National, most severe in West Coast and rural distribution | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ Prices Pressure Margins

Chemours and Tronox control a significant portion of the global TiO₂ supply, and their chlorination-based U.S. assets expose formulators to both energy swings and stricter environmental compliance[2]Chemours Company, “Titanium Dioxide Market Update Q2 2025,” chemours.com. Pigment prices remain elevated compared to levels seen before 2020. While Masco has successfully enhanced its margins via hedging and substituting extenders, the diminished hiding power of these substitutes constrains the extent to which calcium carbonate or kaolin can replace TiO₂ in high-end interior paints.

Freight-Cost Inflation Strains Dealer Inventories

Independent dealers, facing elevated less-than-truckload (LTL) rates, are compelled to bolster their working capital to avert stock-outs. Home Depot's acquisition of SRS Distribution empowers it to promise next-day deliveries for contractors. Meanwhile, Sherwin-Williams, with its owned-store model, mitigates inbound volatility but still grapples with elevated diesel surcharges. In 2024, port congestion on the West Coast postponed specialty resin imports, extending lead times for high-performance coatings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane Extends Protective Performance

In 2025, acrylics commanded 36.18% of resin consumption within the United States paints and coatings market, thanks to low odor and quick dry in DIY applications. Polyurethane is slated for a 5.16% CAGR to 2031, outpacing all other resins as bridge, marine, and industrial users prioritize abrasion and chemical resistance. Alkyd demand keeps shrinking under VOC curbs, yet remains relevant for penetrating wood stains. Epoxy dominates heavy-duty primers and floor coatings, benefiting from bridge and offshore wind investments. Polyester, integral to powder coatings, gains from appliance and furniture output, aided by BASF’s new neopentyl glycol supply that lowers product carbon footprints.

Other chemistries, such as vinyl, silicone, and fluoropolymers, fill niche roles. Arkema’s PVDF capacity addition in Kentucky supports high-rise facades that need ultraviolet durability. Silicone resins from Dow and Wacker enable heat-stable finishes on exhaust systems, while fluoropolymer topcoats protect EV battery casings against electrolyte spills. Tailored polymer architectures therefore multiply formulation complexity, discouraging commoditization and raising switching costs.

By Technology: Water-Borne Coatings Dominate Low-Emission Shift

Water-borne systems accounted for 68.24% of the 2025 volume in the United States paints and coatings market and exhibit the swiftest 5.36% CAGR outlook to 2031. Solvent-borne coatings still serve aerospace, marine, and heavy-equipment niches where humidity tolerance and cold-spray properties outweigh emission penalties. Powder coatings, free of solvents and offering 95% transfer efficiency, advance in metal furniture and appliances, while UV-curable coatings penetrate wood flooring and packaging thanks to instant cure and minimal energy use.

End-use variation is stark: architectural interiors are nearly all latex, automotive OEM uses hybrid film stacks, and industrial maintenance leans on high-solids epoxies. Regulatory clamp-downs by the EPA and state air-quality boards continue to push research and development funds toward water-borne and UV chemistries that can match solvent-borne gloss and mar resistance. Manufacturers that master these conversions secure brand equity in sustainability-driven procurement.

By Distribution Channel: Big-Box Retailers Accelerate Contractor Capture

Company-owned outlets represented 40.66% of 2025 sales, anchored by Sherwin-Williams’ 4,800-store network. However, big-box retailers post a 7.04% CAGR through 2031, the quickest among channels, after investing in pro desks, volume pricing, and same-day fulfillment. Home Depot’s SRS buy adds roofing and drywall supply lines that naturally bundle paint, stretching the retailer’s contractor relevance. Independent dealers guard their share with custom tinting, credit, and technical advice, but freight inflation squeezes their thin margins.

Digital commerce remains modest in the United States paints and coatings market, held back by color-match complexity and hazmat shipping restrictions. Nonetheless, contractors appreciate click-and-collect for repeat SKUs, encouraging manufacturers to refine online configurators that sync with store tinting systems.

By End-User Industry: Architectural Coatings Retain Primacy

Architectural applications delivered 45.12% of 2025 revenue and carry a 5.02% CAGR, hinging on remodeling and multifamily construction. Automotive coatings benefit from EV lineups that raise coat counts and introduce conductive primers, even as collision-repair volumes slip. Wood-finish demand rises with furniture and cabinetry orders, where water-borne and UV lacquers reduce plant fire risk. Protective coatings growth accelerates under infrastructure outlays and offshore wind towers needing 25-year corrosion guarantees.

General industrial and transportation coatings adopt powder and high-solids polyurethane for machinery, rail cars, and buses, balancing quick turnarounds with durability demands. Packaging leads the shift to bisphenol-A-free can linings, where PPG’s Innovel enables major beverage brands to meet new food-contact limits. AkzoNobel has launched its Accelshield range, bolstered by a dedicated plant in Spain, focusing on non-epoxy chemistries.

Geography Analysis

The United States paints and coatings market reflects distinct regional rhythms. Sun Belt states such as Texas, Florida, and the Carolinas command architectural volumes through robust single-family starts and remodeling. Midwest manufacturing hubs in Michigan and Ohio fuel OEM and industrial demand, though EV investment volatility clouds long-range forecasts. The Northeast, with aging bridges and tight VOC caps below 50 g/L, prefers low-emission water-borne systems. California’s South Coast Air Quality Management District remains the bellwether for future national standards, nudging nationwide innovation.

Pacific Northwest aerospace clusters around Seattle generate steady orders for high-performance primers and sealants; PPG’s forthcoming Shelby, North Carolina plant targets just-in-time supply for these programs. The Gulf Coast petrochemical belt depends on multi-layer epoxies and polyurethanes that resist saltwater and hydrogen sulfide, making it the largest pocket for protective coatings. Independent dealers here often bundle coatings with abrasive-blasting services, deepening local ecosystems.

Mountain West and Great Plains territories face long freight hauls, raising landed costs and prompting cooperatives to stock multipurpose farm-equipment paints. Offshore wind projects from Massachusetts to Virginia unlock a fresh niche for NORSOK-compliant systems rated for 25-year immersion, positioning suppliers capable of on-site technical audits to capture price premiums. Federal infrastructure grants further tilt coatings shipments toward states with the densest bridge-rehabilitation schedules.

Competitive Landscape

The United States paints and coatings market studied is moderately consolidated. Innovation centers on sustainability and performance. Machine-learning-aided formulation, exemplified by PPG’s Deltron Premium Glamour Speed clear coat, cuts cycle times on luxury vehicles. Self-healing polymers, UV powder resins, and antimicrobial additives occupy current patent pipelines, though commercialization relies on complex regulatory clearances. Raw-material integration, especially in resins and pigments, offers cost buffers against TiO₂ and monomer volatility, giving scale players a durable edge over regional specialists.

United States Paints And Coatings Industry Leaders

The Sherwin-Williams Company

PPG Industries, Inc.

RPM International Inc.

Axalta Coating Systems, LLC

Masco Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PPG Industries, Inc., announced its plan to invest USD 380 million to build a new aerospace coatings and sealants manufacturing facility in Shelby, North Carolina.

- May 2024: PPG Industries, Inc., unveiled plans to channel USD 300 million into advanced manufacturing across North America, aiming to cater to the surging demand for automotive paints and coatings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States paints & coatings market as all solvent-borne, water-borne, powder, and UV-cured liquid film-forming materials sold in the country for architectural, automotive OEM and refinish, wood, general industrial, protective, transportation, and packaging uses. These materials combine binders, pigments, solvents or water, and functional additives to protect or decorate substrates once a uniform film has formed.

Scope exclusion: printing inks, adhesives, and raw resin sales are kept outside the revenue pool.

Segmentation Overview

- By Resin Type

- Acrylic

- Alkyd

- Polyurethane

- Epoxy

- Polyester

- Other Resin Types

- By Technology

- Water-borne

- Solvent-borne

- Powder Coating

- UV Technology

- By Distribution Channel

- Company-Owned Stores

- Independent Paint Dealers

- Big-Box Retailers and Home Centers

- Direct to Industrial OEM

- E-Commerce

- By End-user Industry

- Architectural

- Automotive

- Wood

- Protective Coatings

- General Industrial

- Transportation

- Packaging

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with formulators, bulk distributors, DIY retailers, and facility specifiers across the Midwest, Sunbelt, and coastal states let us stress-test volume assumptions, typical selling prices, and technology adoption timelines. Insights from these stakeholders, combined with feedback from regulatory advisors on upcoming VOC thresholds, closed data gaps that public statistics could not bridge.

Desk Research

We began with federal datasets such as the U.S. Census Bureau's Monthly Construction Spending, the Federal Highway Administration's Highway Statistics, and the Bureau of Economic Analysis' personal consumption tables, which ground baseline demand indicators. Trade association releases from ACA, FEMA customs import records (HS 32 series), and patent analytics from Questel helped capture technology shifts toward powder and low-VOC systems. We also tapped company 10-Ks and quarterly filings to benchmark sales channel splits, while Dow Jones Factiva and D&B Hoovers provided supplementary news and financials to validate strategic capacity moves.

Because coatings demand correlates with macro construction and durable goods cycles, our analysts further screened open-access peer-reviewed journals for resin price elasticity studies and OEM paint shop conversion rates. The sources listed are illustrative; many additional open repositories were reviewed in building and cross-checking the dataset.

Market-Sizing & Forecasting

A top-down build starts with 2024 apparent consumption (domestic production + imports - exports) reconstructed from U.S. Geological Survey pigments output and ITC trade codes, which is then split by end use using housing starts, light-vehicle production, and industrial capacity utilization weights. Bottom-up supplier roll-ups and sampled ASP × volume checks for major resin categories corroborate and refine totals, ensuring the two views converge within a 5% tolerance. Key variables modeled include residential housing permits, commercial floor-space completions, average repair refinish labor hours, titanium-dioxide price indices, and state VOC rule phase-ins. Multivariate regression with scenario overlays projects 2025-2030 demand, while assumption bands are benchmarked with expert consensus before freeze. Data gaps in niche segments (e.g. marine) are interpolated using adjacent-market penetration rates and validated through channel checks.

Data Validation & Update Cycle

Outputs run through variance tests against historical ratios and external signal dashboards; anomalies trigger senior-analyst review and, if needed, rapid re-contacts. Reports refresh each year, with ad-hoc updates after material events so clients always receive the latest calibrated view.

Why Mordor's US Paints And Coatings Baseline Is Trusted

Published figures often diverge because firms choose differing scope boundaries, price bases, and refresh cadences. Our disciplined definition, dual-track modeling, and yearly update rhythm reduce those gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 36.52 B | Mordor Intelligence | - |

| USD 32.94 B | Global Consultancy A | Omits DIY e-commerce revenue and applies lower average selling prices |

| USD 33.65 B | Trade Journal B | Relies mainly on volume extrapolation, limited technology stratification |

| USD 35.70 B | Industry Association C | Counts domestic production only, excludes finished-goods imports |

These comparisons show that once retail channels, imported finished goods, and price progression are fully captured, Mordor's baseline stands higher yet remains well within observed physical demand, giving executives a balanced, transparent reference point for planning.

Key Questions Answered in the Report

How large will the United States paints and coatings market be by 2031?

It is forecast to reach USD 46.92 billion by 2031, growing at a 4.28% CAGR from USD 38.05 billion in 2026.

Which resin type is growing the fastest?

Polyurethane leads with a projected 5.16% CAGR through 2031 due to its superior durability in protective uses.

Why are water-borne coatings gaining share?

Stricter VOC regulations and corporate carbon targets push formulators and buyers toward low-emission water-borne systems, which already hold 68.24% volume in 2025.

What is driving sales through big-box retailers?

Expanded pro-contractor programs, job-site delivery, and click-and-collect services underpin the segment’s 7.04% CAGR outlook.

How does federal infrastructure funding influence demand?

The allocation for roads and bridges extends to order pipelines for high-performance protective coatings with 25-year life requirements.

Page last updated on: