United States Occupational Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

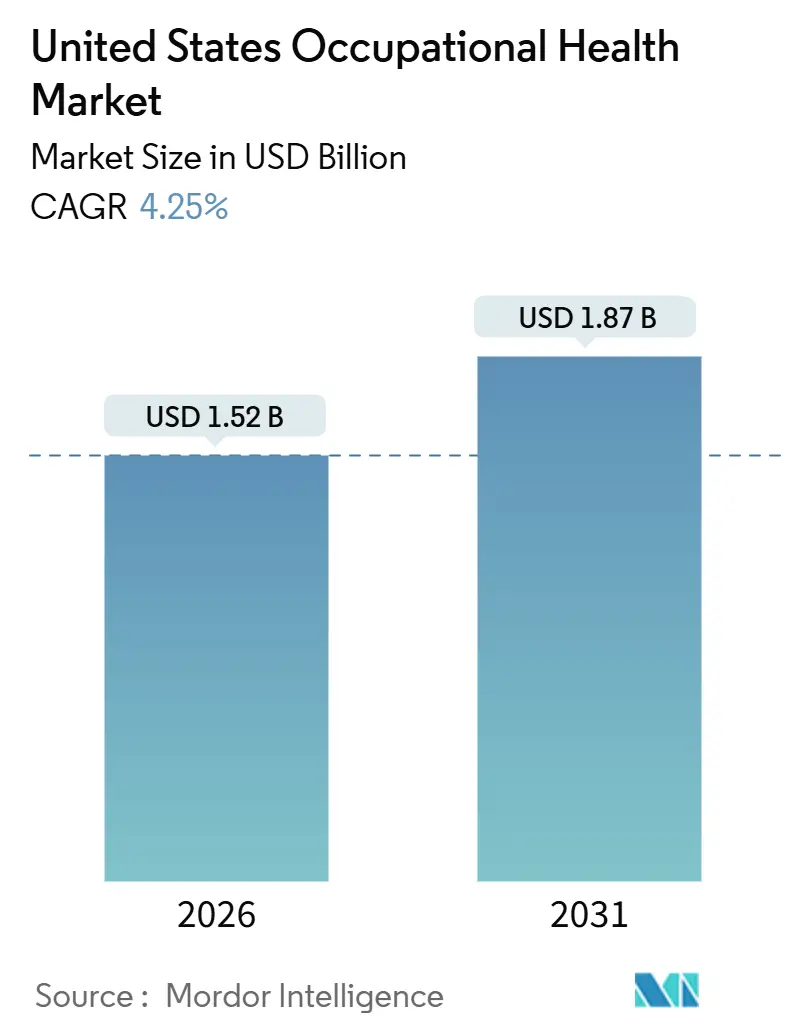

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 1.87 Billion |

| Growth Rate (2026 - 2031) | 4.25% CAGR |

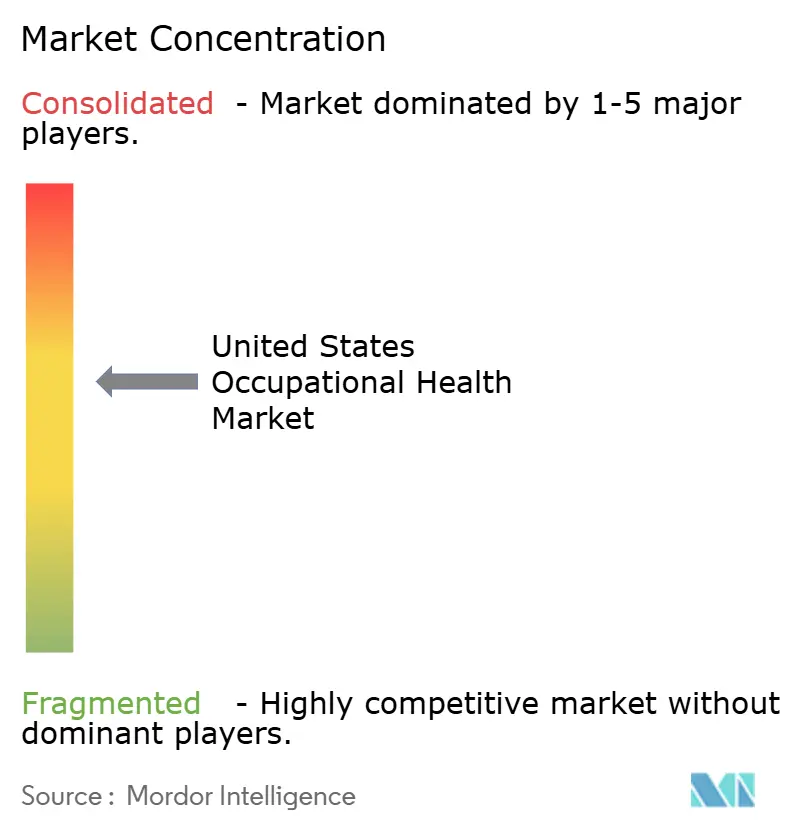

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Occupational Health Market Analysis by Mordor Intelligence

The United States Occupational Health Market size is estimated at USD 1.52 billion in 2026, and is expected to reach USD 1.87 billion by 2031, at a CAGR of 4.25% during the forecast period (2026-2031).

Employer priorities have shifted from reactive injury care toward prevention, mental-health support, and compliance analytics, a transition driven by tight labor conditions, hybrid work, and rising OSHA penalties. Investments now focus on screening and wellness benefits that support talent retention while curbing absenteeism costs. Tele-based screenings have gained momentum as dispersed workforces require asynchronous solutions, and data-driven risk-prediction tools are emerging to help employers anticipate injuries before they trigger claims. Competitive intensity remains moderate because state regulations and the need for local clinical coverage limit large-scale consolidation, yet tele-occupational platforms are creating new efficiencies that threaten brick-and-mortar incumbents.

Key Report Takeaways

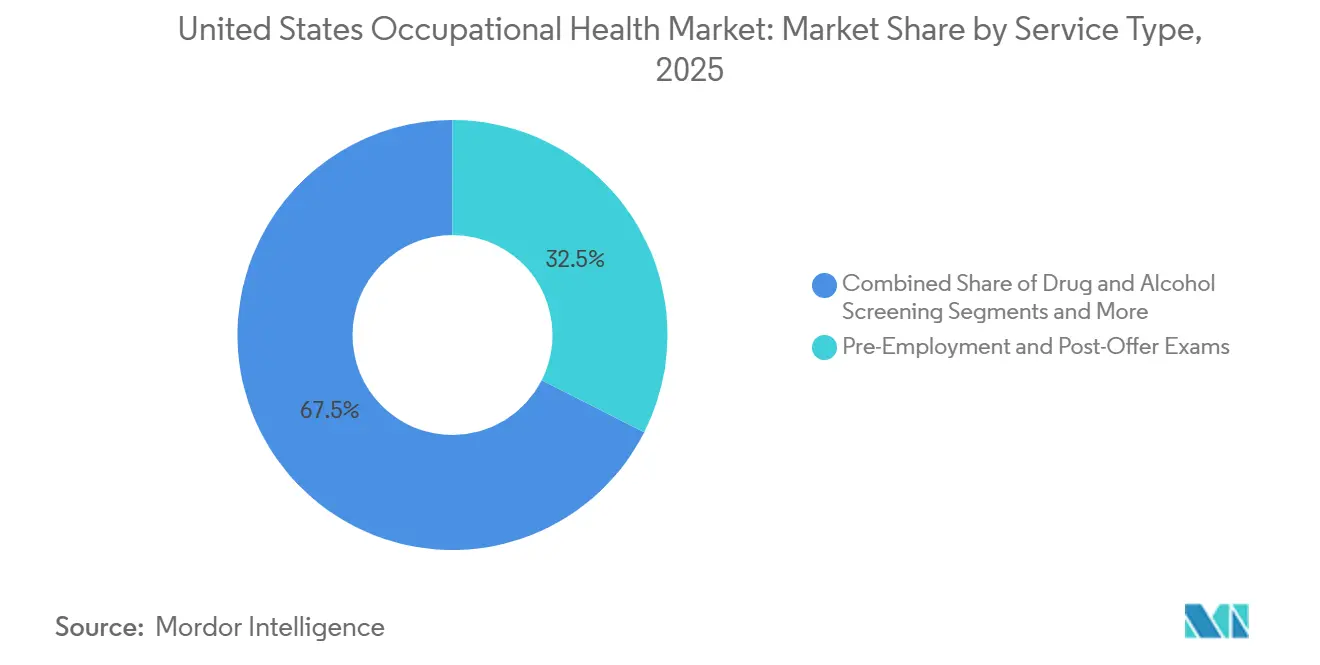

- By service type, Pre-Employment & Post-Offer Exams led with 32.46% of the occupational health market share in 2025.

- By service type, Employee Assistance & Mental-Health Programs are forecast to advance at a 7.25% CAGR through 2031.

- By health condition, Work-Induced Stress commanded 27.57% share of the occupational health market size in 2025 and is growing at an 8.05% CAGR to 2031.

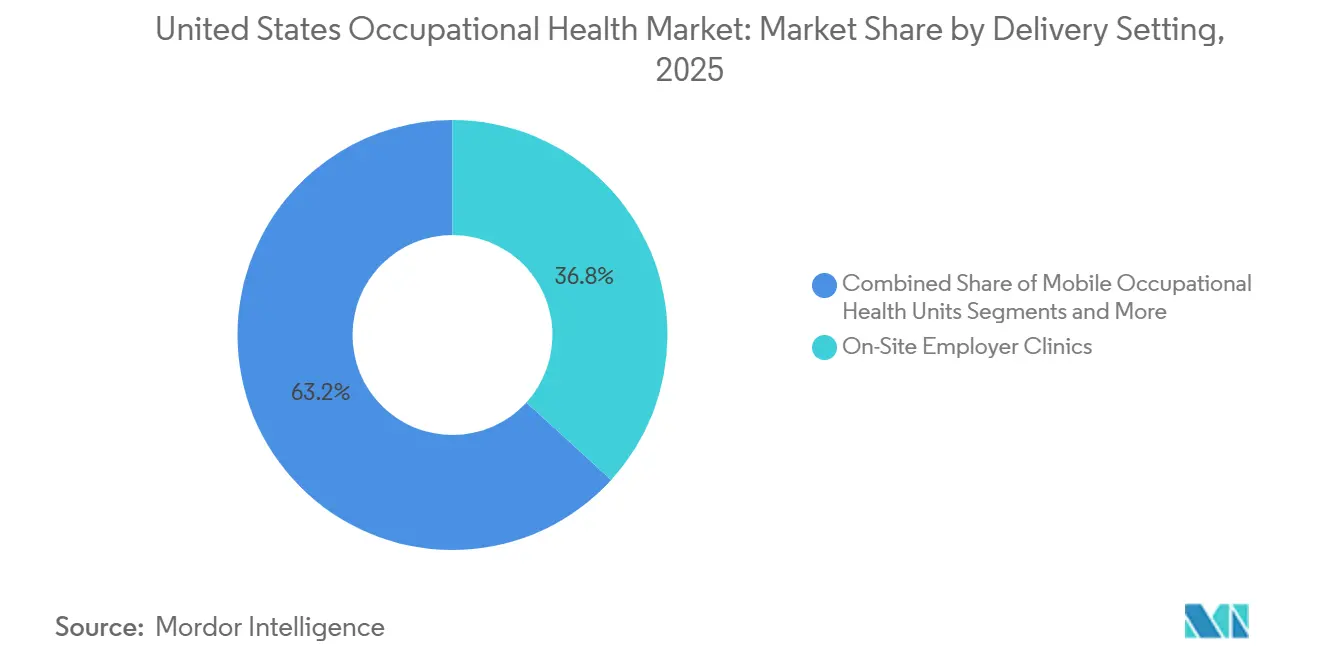

- By delivery setting, On-Site Employer Clinics held 36.77% revenue in 2025, while Tele-Occupational Health Platforms are scaling at a 7.89% CAGR.

- By end-user industry, Manufacturing accounted for 29.84% revenue in 2025, but Transportation & Warehousing posts the fastest 6.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Occupational Health Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding employer-sponsored wellness benefits | +0.8% | National, with higher adoption in metropolitan areas and Fortune 500 employers | Medium term (2-4 years) |

| Growth of remote/hybrid workforce demanding tele-OccMed services | +0.9% | National, concentrated in IT, finance, and professional services hubs | Short term (≤ 2 years) |

| Tight U.S. labor market boosting pre-employment screenings | +0.7% | National, strongest in manufacturing, construction, and transportation sectors | Short term (≤ 2 years) |

| Rise in OSHA citations prompting proactive compliance programs | +0.6% | National, with elevated impact in construction, manufacturing, and warehousing | Medium term (2-4 years) |

| AI-enabled risk-prediction reducing injury costs | +0.5% | National, early adoption in large manufacturing and logistics operations | Long term (≥ 4 years) |

| Climate-related heat-stress prevention services | +0.4% | Sun Belt states, outdoor construction, agriculture, and delivery sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Employer-Sponsored Wellness Benefits

Organizations increasingly view wellness programs as retention tools. A 2024 study reported 12% lower voluntary turnover among companies that bundled biometric screenings, health coaching, and mental-health resources versus peers without such offerings.[1]Emily Johnson, “Telehealth for Occupational Health Services: A Systematic Review,” National Center for Biotechnology Information, ncbi.nlm.nih.govProvider networks now package preventive screenings with nutrition counseling and stress-management workshops, positioning themselves as population-health partners and offsetting flat workers’ compensation premiums in low-risk sectors.

Growth of Remote/Hybrid Workforce Demanding Tele-OccMed Services

Hybrid work dismantles the traditional clinic-centric delivery model. Remote employees can complete fitness-for-duty evaluations by video, submit at-home specimens, and undergo virtual audiometry, accelerating onboarding across multiple states. A 2024 systematic review showed 94% diagnostic concordance between tele-evaluations and in-person visits for non-physical roles. Established clinic operators are therefore acquiring telehealth platforms to protect share within the occupational health market.

Tight U.S. Labor Market Boosting Pre-Employment Screenings

Labor-force participation remained below pre-pandemic levels through 2024, forcing employers to vet larger applicant pools.[2]U.S. Bureau of Labor Statistics, “Labor Force Statistics from the Current Population Survey,” U.S. Bureau of Labor Statistics, bls.gov Drug-testing positivity for safety-sensitive transportation staff rose to 2.9% in 2024, prompting logistics firms to expand screening protocols. These factors sustain demand for pre-hire medical exams within the occupational health market.

Rise in OSHA Citations Prompting Proactive Compliance Programs

OSHA issued more than USD 2.6 million in heat-related penalties in fiscal 2024 and is drafting a national heat-stress rule.[3]Erin Parker, “Heat Injury and Illness Prevention in Outdoor and Indoor Work Settings,” Occupational Safety and Health Administration, osha.gov Employers now invest in heat-stress training, rest-break monitoring, and on-site medical support to avoid fines, which feeds service demand across the occupational health market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automation reducing head-count in heavy industry | -0.5% | National, concentrated in manufacturing and warehousing | Long term (≥ 4 years) |

| Shrinking workers' comp premiums in low-risk sectors | -0.3% | National, most pronounced in IT, finance, and professional services | Medium term (2-4 years) |

| Shortage of board-certified occupational physicians | -0.4% | National, acute in rural and exurban markets | Long term (≥ 4 years) |

| Employer data-privacy concerns over continuous health monitoring | -0.3% | National, heightened in states with biometric data laws (IL, TX, WA) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Board-Certified Occupational Physicians

Fewer than 3,000 certified practitioners are active nationwide, limiting service scope in rural clinics. Operators rely more on nurse practitioners and physician assistants, and expansion slows in underserved regions of the occupational health market.

Employer Data-Privacy Concerns Over Continuous Health Monitoring

Strict biometric‐privacy laws in Illinois, Texas, and Washington carry statutory damages that deter adoption of wearable-driven safety programs. In a 2024 survey, 38% of manufacturing firms halted pilot monitoring projects after employee pushback, delaying penetration of AI safety tools within the occupational health market.

Segment Analysis

By Service Type: Mental Health Drives Fastest Expansion

Pre-Employment & Post-Offer Exams retained a 32.46% occupational health market share in 2025, but growth moderates as automation trims headcount in heavy industry. In contrast, Employee Assistance & Mental-Health Programs grow at a 7.25% CAGR, because burnout-driven absenteeism surpasses injury claims in many white-collar groups. Drug & Alcohol Screening remains a compliance pillar, yet margins tighten with cheaper oral-fluid kits. Rehabilitation services stay stable, aided by insurers that favor early intervention. Ergonomic consulting expands in large warehouses where proactive assessments cut upper-extremity injuries by 23% over two years.

Employers now seek bundled packages instead of individual engagements, forcing providers to diversify offerings or partner with wellness vendors. The occupational health market size for mental-health services is expected to represent an increasing slice of overall revenue by 2031. Tele-based counseling compresses delivery costs and increases session uptake, helping programs reach smaller employers that previously lacked access. Structural growth remains tied to continued recognition of psychosocial hazards as core business costs.

Note: Segment shares of all individual segments available upon report purchase

By Health Condition: Stress Dominates Clinical Volume

Work-Induced Stress captured 27.57% of the occupational health market size in 2025 and leads growth at 8.05% CAGR, reflecting high turnover and disability costs stemming from anxiety and depression. Musculoskeletal Disorders rank second but their share erodes as lift-assist devices spread on factory floors. Respiratory Disease incidence eases due to improved ventilation systems, yet remains a focus in chemical plants. Heat-stress visits rise 18% in Sun Belt emergency rooms, a trend likely to accelerate under OSHA’s new standard.

Providers are expanding behavioral-health capacity and investing in on-staff counselors. Digital tools now triage stress claims before they escalate into leave requests. At the same time, clinics are integrating ergonomic therapy and return-to-work coaching to address cumulative trauma. These service shifts fortify growth prospects inside the broader occupational health market.

By Delivery Setting: Telehealth Scales Amid Hybrid Work

On-Site Employer Clinics generated 36.77% of revenue in 2025 because large manufacturers and hospitals justify fixed staff by volume. However, Tele-Occupational Health Platforms are projected to rise at 7.89% CAGR to 2031, propelled by interstate hiring and scope-of-practice reforms that permit virtual assessments without in-person supervision. Off-Site Centers cater to small and mid-sized employers that rotate staff through local locations, while Mobile Units serve episodic demands at construction or mining sites.

Tele-platforms reduce geographic barriers and align with remote onboarding cycles, creating scalable efficiencies. Traditional clinic operators now partner with telehealth innovators to keep enterprise clients. This convergence is reshaping value pools within the occupational health market and intensifying competition on user experience and analytic insight instead of clinic density alone.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: E-Commerce Logistics Fuels Transportation Growth

Manufacturing retained 29.84% revenue in 2025, stewarded by longstanding compliance programs. Yet Transportation & Warehousing logs the fastest 6.24% CAGR through 2031 as e-commerce expands fulfilment hubs and regulators sharpen focus on driver fatigue and heat exposure. Construction & Mining remains steady amid infrastructure spending and silica-exposure rule tightening, while Healthcare & Social Assistance invests in ergonomic and violence-prevention efforts for frontline workers.

Government agencies integrate wellness stipends to retain an aging workforce, and professional-services firms broaden mental-health plans to address hybrid work stress. As warehouse automation still leaves many high-risk manual tasks, demand for physical-fitness qualifiers and ergonomic coaching persists. These patterns show where occupational health market growth will likely cluster during the forecast window.

Geography Analysis

Sun Belt states lead expansion because reshoring and logistics corridors draw labor-intensive operation to a hot climate that heightens heat-stress risk. OSHA’s proposed heat-illness standard will amplify surveillance demand in these regions. Midwest manufacturing hubs post moderate growth anchored by automotive and food processing, though headcount rises slowly as robotics proliferate. West Coast employers allocate higher per-worker wellness budgets under California and Washington safety regulations that exceed federal rules.

Northeast states present mature, slower-growth dynamics, buffered by established clinic networks. Rural markets nationwide continue to lag due to the physician shortage, translating into tele-occupational health adoption and mobile-unit dispatches that extend reach. As state statutes vary, providers tailor service menus to local workers’ compensation fee schedules and scope-of-practice requirements, leading to pronounced regional differentiation inside the occupational health market.

Competitive Landscape

The occupational health market remains fragmented, with the top providers each holding good national revenue. Concentra, U.S. HealthWorks, and WorkCare compete on clinic density, while Premise Health and Harness Health Partners anchor on-site models that integrate wellness and chronic-care management. Tele-health-first disruptors offer lower-cost pre-hire exams and return-to-work clearances, putting downward pressure on incumbent fees.

In response, incumbents are acquiring digital platforms and analytics vendors. One 2024 patent shows a leading provider embedding machine-learning tools to predict musculoskeletal risk. Barriers such as state licensing, payer contracts, and electronic health-record integrations make client switching costly, moderating volatility in the occupational health market. Yet tele-occupational innovators are unlocking white-space such as at-home drug tests and AI ergonomic coaching that broadens service reach without brick-and-mortar expansion.

Emerging competitors now build subscription models around continuous engagement rather than episodic injury care. Evidence points to rising collaboration between clinic networks and health-tech startups, creating a hybrid competitor class that blends nationwide tele-capabilities with localized triage centers. This dynamic will keep margins under pressure and accelerate service innovation across the occupational health market.

United States Occupational Health Industry Leaders

Premise Health

Concentra, Inc.

Workwell Occupational Medicine, LLC

Occucare International

Examinetics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Wellness Workdays launched BRAVE, a mental-health training program tailored to construction crews, focusing on crisis prevention.

- September 2025: Allianz Partners added mental-health and tele-consult options to its Summit plan for small and mid-sized employers.

- September 2025: Bespoke Concierge MD introduced Corporate Health Plans that bring proactive primary care into workplaces.

- July 2025: Wolters Kluwer began a collaboration with Enterprise Health to embed occupational health algorithms in employer clinics.

United States Occupational Health Market Report Scope

As per the scope of the report, occupational health deals with the prevention and treatment of work-related injuries and illnesses. Physicians specially trained in occupational health can diagnose and treat work-related injuries more effectively than other primary care physicians.

The United States Occupational Health Market is Segmented By Service Type, Health Condition, Delivery Setting and End User Industry. By Service Type, market is segmented into Pre-Employment & Post-Offer Exams, Drug & Alcohol Screening, Immunizations & Travel Medicine, Employee Assistance & Mental-Health Programs, Rehabilitation & Return-to-Work Services, Ergonomic & On-Site Safety Services. By Health Condition, market is segmented into Work-Induced Stress, Respiratory Diseases, Noise-Induced Hearing Loss, Chemical & Vibration-Related Disorders, Musculoskeletal Disorders, Others. By Delivery Setting, the market is segmented into On-Site Employer Clinics, Off-Site Clinics/Stand-Alone Centers, Mobile Occupational Health Units, and Tele-Occupational Health Platforms. By End-User Industry, market is segmented into Manufacturing, Construction & Mining, Healthcare & Social Assistance, Government & Public Sector, Transportation & Warehousing, IT/Finance/Professional Services, Retail & Hospitality. The report offers the market size in value terms in USD for all the abovementioned segments.

| Pre-Employment & Post-Offer Exams |

| Drug & Alcohol Screening |

| Immunizations & Travel Medicine |

| Employee Assistance & Mental-Health Programs |

| Rehabilitation & Return-to-Work Services |

| Ergonomic & On-Site Safety Services |

| Work-Induced Stress |

| Respiratory Diseases |

| Noise-Induced Hearing Loss |

| Chemical & Vibration-Related Disorders |

| Musculoskeletal Disorders |

| Others |

| On-Site Employer Clinics |

| Off-Site Clinics / Stand-Alone Centers |

| Mobile Occupational Health Units |

| Tele-Occupational Health Platforms |

| Manufacturing |

| Construction & Mining |

| Healthcare & Social Assistance |

| Government & Public Sector |

| Transportation & Warehousing |

| IT, Finance & Professional Services |

| Retail & Hospitality |

| By Service Type | Pre-Employment & Post-Offer Exams |

| Drug & Alcohol Screening | |

| Immunizations & Travel Medicine | |

| Employee Assistance & Mental-Health Programs | |

| Rehabilitation & Return-to-Work Services | |

| Ergonomic & On-Site Safety Services | |

| By Health Condition | Work-Induced Stress |

| Respiratory Diseases | |

| Noise-Induced Hearing Loss | |

| Chemical & Vibration-Related Disorders | |

| Musculoskeletal Disorders | |

| Others | |

| By Delivery Setting | On-Site Employer Clinics |

| Off-Site Clinics / Stand-Alone Centers | |

| Mobile Occupational Health Units | |

| Tele-Occupational Health Platforms | |

| By End-User Industry | Manufacturing |

| Construction & Mining | |

| Healthcare & Social Assistance | |

| Government & Public Sector | |

| Transportation & Warehousing | |

| IT, Finance & Professional Services | |

| Retail & Hospitality |

Key Questions Answered in the Report

How large is the U.S. occupational health market in 2026 and where will it be by 2031?

The occupational health market size is USD 1.52 billion in 2026 and is projected to reach USD 1.87 billion by 2031.

Which service line is growing the fastest for employers?

Employee Assistance & Mental-Health Programs are expanding at a 7.25% CAGR, reflecting rising demand for burnout and stress management solutions.

Why are tele-occupational health platforms gaining momentum?

Hybrid and remote workforces need virtual pre-employment exams and return-to-work evaluations; tele-platforms deliver these services at a 7.89% CAGR while lowering travel time and clinic overhead.

What drives the surge in demand from transportation and warehousing employers?

E-commerce fulfillment growth and stricter federal oversight of driver fatigue and heat exposure push the segment forward at a 6.24% CAGR.

How will OSHA’s proposed heat-stress rule affect service demand?

The rule will require rest-break monitoring and medical surveillance in hot environments, boosting requests for heat-stress training and physiological screening, especially in Sun Belt states.