Market Trends of United States Nuclear Power Reactor Decommissioning Industry

Commercial Power Reactor Expected to Dominate the Market

- The commercial power reactors are the nuclear reactors that are mainly used for generating electricity. Most of these reactors are being installed in nuclear power plants. Moreover, increasing renewable energy from solar and wind is much cheaper and cleaner.

- Over the past decade, intense competition from electricity generation using low-cost shale gas has hurt the competitiveness of the country's nuclear power industry. Moreover, record low wholesale electricity prices and the high cost of life extension (PLEX) upgrades have driven early nuclear plant retirements.

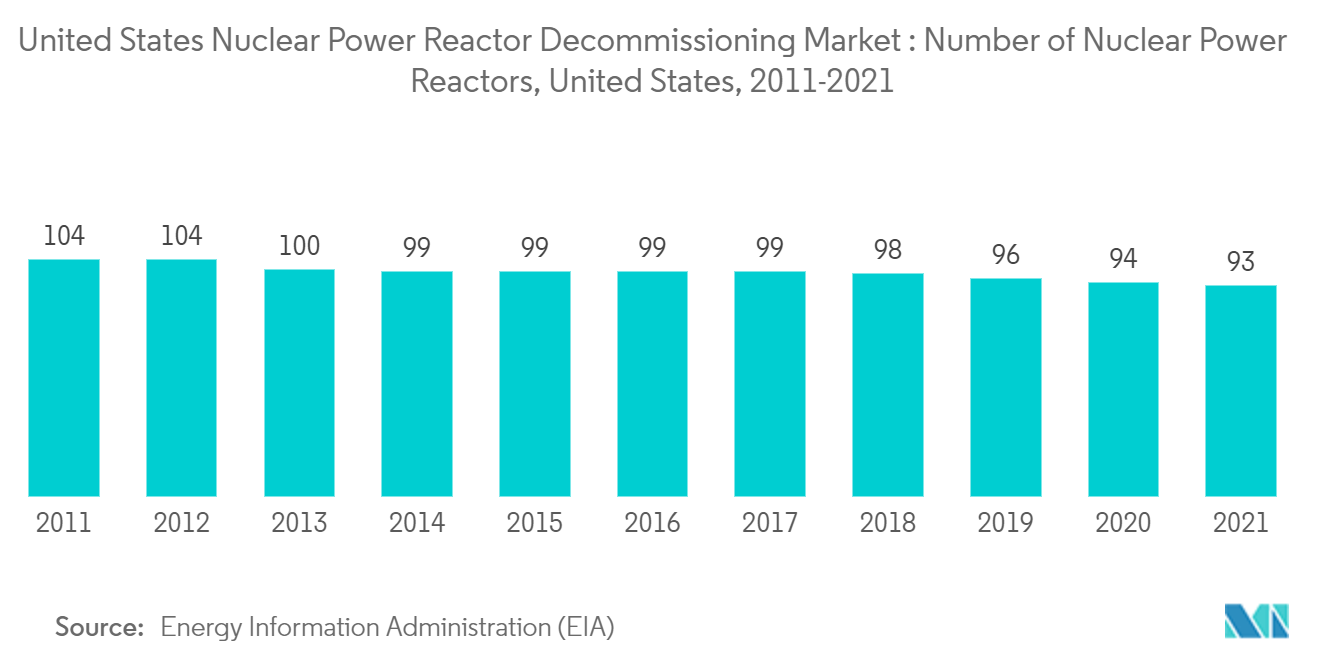

- According to the U.S. Energy Information Administration, by the end of December 2021, the United States had 93 active nuclear reactors. Since 1990, the number of active reactors has declined.

- As of May 2022, the United States had 92 operating nuclear power reactors with a combined capacity of 94.7 GWe in 30 states, operated by 30 different power companies. In addition, two reactors are under construction with a total of 2.23 GWe.

- As the era of nuclear power winds down in the United States, the decommissioning of nuclear power plants is becoming a significant industry. Private companies are acquiring these plants, taking over their licenses, liabilities, decommissioning funds, and waste contracts. Around 38 reactors with a combined capacity of 17.54 GWe were shut down, and there are two reactors under construction. In addition to this, around 198 reactors are expected to shut down by 2030.

Hence, owing to the above points, the commercial power reactor segment is likely to dominate the United States nuclear power reactor decommissioning market during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

Intense Competition from Renewable Energy Sources to Drive the Market

- There is an ongoing surge in the development of renewable energy worldwide. The situation, in turn, decreases FDI and investment in the nuclear power sector in several regions.

- The United States, due to the constant increase in energy demand and an increasing issue related to greenhouse gas emissions, is witnessing a large installation of renewable energy capacity, which is likely going to replace the costly and hazardous nuclear energy in the country.

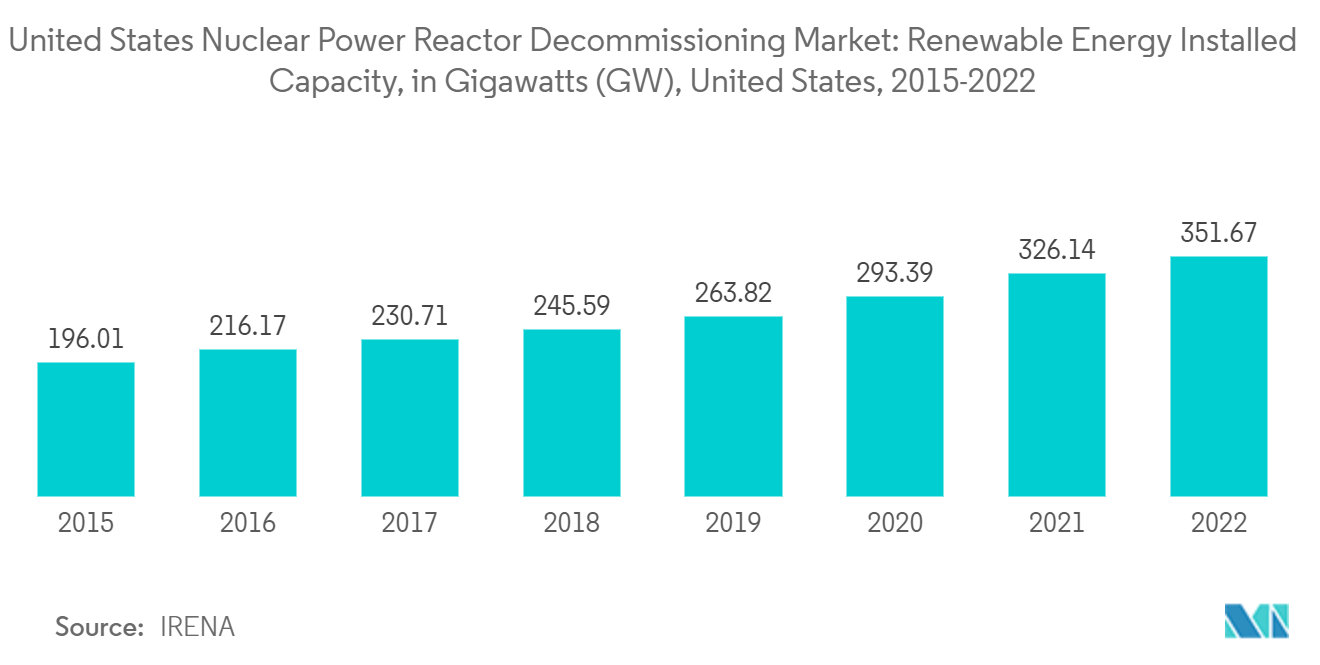

- In 2021, the country's total renewable energy installation capacity was 351.67 gigawatts (GW), which was more than the installed capacity of 2020, 326.14 gigawatts (GW). Moreover, the country is expected to increase the renewable energy mix from 19% in 2021 to 38% in 2050, thus surpassing energy from coal, nuclear, and natural gas. This is likely to drive the nuclear power reactor decommissioning market in the country.

- Solar power has become more accessible and prevalent in the United States than ever before. In the last decade alone, solar power has experienced an average annual growth rate of 42%. Since the last decade, solar installations in the country have grown thirtyfold. The total installed capacity in the United States reached 121.4 GW in 2021, representing an increase of about 26.2% compared to the previous year's value.

- According to the data from the Solar Energy Industries Association (SEIA), around 5 GW of solar PV capacity is expected to be installed in Indiana by 2026, ranking the state's pipeline as the sixth-largest in the country. On the other hand, SEIA estimates that Nevada will install more than 4 GW over the same period, making the state the seventh-largest in terms of solar PV pipelines.

- However, wind power capacity in the United States grew rapidly in 2021, with 13.4 gigawatts of new capacity added and USD 20 billion invested. Cumulative wind capacity by the end of 2021 was nearly 136 gigawatts (GW). The country has targets to produce around 20% of its electricity from wind energy by 2030 and achieve net zero emissions by 2050; its wind energy is expected to grow during the forecast period.

Hence, owing to the above points, increasing renewable energy is expected to drive the United States nuclear power reactor decommissioning market during the forecast period.