| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 51.81 Billion |

| Market Size (2030) | USD 100.42 Billion |

| CAGR (2025 - 2030) | 14.15 % |

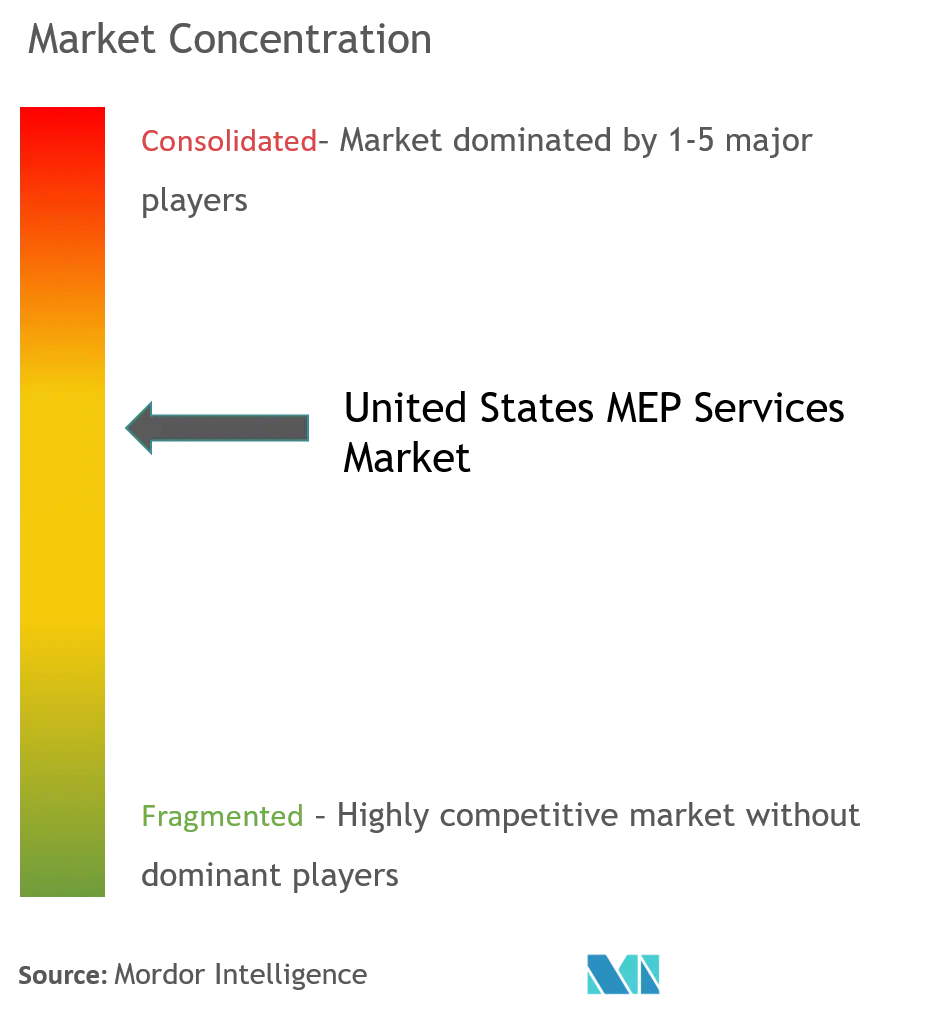

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

MEP Services Market Major Players")

MEP Services Market Size")

US MEP Services Market Analysis

The United States MEP Services Market size is estimated at USD 51.81 billion in 2025, and is expected to reach USD 100.42 billion by 2030, at a CAGR of 14.15% during the forecast period (2025-2030).

The MEP services industry is experiencing a significant transformation driven by the growing emphasis on sustainable building practices and energy efficiency. According to the US Green Building Council, buildings currently account for 39% of total carbon dioxide emissions, pushing the industry toward more environmentally conscious solutions. This has led to increased adoption of energy-efficient MEP systems and sustainable design practices across new construction and renovation projects. The integration of renewable energy solutions and smart building technologies has become a cornerstone of modern MEP service offerings, with service providers increasingly focusing on developing comprehensive sustainability strategies for their clients.

The technological landscape of MEP services continues to evolve with the widespread adoption of Building Information Modeling (BIM) and advanced design tools. Design services have emerged as a crucial revenue stream, with industry reports indicating that 58% of revenue from major MEP firms is generated from design services. The integration of automation, artificial intelligence, and cloud-based solutions has revolutionized how MEP systems are designed, installed, and maintained. These technological advancements have enabled more precise planning, better coordination between different building systems, and improved operational efficiency.

Energy management has become a central focus in the MEP services sector, driven by increasing awareness of building energy consumption patterns. According to the US Energy Information Administration, HVAC systems alone account for 35% of total building energy consumption in commercial buildings, while lighting systems contribute 11%. This has led to a growing demand for smart MEP solutions that can optimize energy usage through advanced controls, monitoring systems, and predictive maintenance capabilities. Service providers are increasingly incorporating energy modeling and analysis tools to help clients achieve their energy efficiency goals while maintaining optimal building performance.

The infrastructure modernization initiatives across the United States are creating substantial opportunities for MEP service providers. Major projects such as the Denver International Airport renovation and New York City transit upgrades are driving demand for sophisticated MEP solutions. The industry is witnessing a shift toward modular and prefabricated MEP components, which offer benefits such as reduced installation time, improved quality control, and better cost efficiency. This trend is particularly evident in large-scale commercial and institutional projects where complex MEP systems need to be integrated seamlessly with existing infrastructure while minimizing disruption to ongoing operations.

US MEP Services Market Trends

Growing Emphasis on Outsourcing of MEP Services to Focus on Core Offering

The construction industry's complexity and scale, with over 733,000 employers and 7 million employees in the United States, has created a strong imperative for specialized MEP service providers outsourcing. Construction companies are increasingly dependent on dedicated MEP services firms to provide comprehensive designs using advanced technologies such as Building Information Modeling (BIM) and 3D printed building solutions. This shift is primarily driven by the stringent licensing requirements for design professionals and installation contractors, which significantly increase the operational costs for construction activities. The requirement for Registered Design Professional (RDP) certification for MEP design services approval has further incentivized construction contractors to outsource these specialized services, allowing them to focus on other critical aspects of their projects.

The technical sophistication required in modern construction projects has made outsourcing MEP services increasingly attractive from both efficiency and cost perspectives. MEP service providers offer benefits such as collaborative 3D models, accurate cost estimations, shop drawing capabilities, clash detection and resolution, and comprehensive project scheduling. These providers are continuously upgrading their technological capabilities with trends such as 3D printing, which are often beyond the scope of in-house MEP teams. The delivery services maintain strict adherence to quality standards, including dedicated mechanical, plumbing, and electrical codes, ensuring compliance while reducing the burden on construction companies to maintain specialized expertise in these areas.

Understand The Key Trends Shaping This Market

Download PDF

Steady Demand from Commercial and Healthcare Institutions

The healthcare sector's recognition of operational inefficiencies, with studies indicating approximately 25% of healthcare spending being characterized as inefficient, has created a substantial demand for mechanical, electrical, and plumbing services. Healthcare facilities require specialized MEP solutions due to their complex departmental requirements, ranging from operating theaters to specialized treatment areas. The critical nature of healthcare infrastructure has led to increased investment in MEP construction services to ensure optimal facility design, particularly in areas affecting patient care such as internal air quality, temperature control, and specialized equipment support systems. This demand is further amplified by the US Green Building Council's findings that buildings contribute to 39% of total carbon dioxide emissions, pushing healthcare facilities to adopt more sustainable and efficient MEP solutions.

Commercial establishments are increasingly investing in MEP construction services to achieve sustainability goals and operational efficiency. The trend toward smart buildings has created new opportunities for MEP companies to implement energy-efficient solutions across various commercial facilities. These solutions encompass advanced HVAC frameworks, water usage optimization, and dynamic building designs that address both environmental concerns and operational efficiency. Commercial facilities are particularly focused on reducing energy consumption across heating, ventilation, and air conditioning (HVAC) systems, which typically account for 35% of total building energy usage, and lighting systems, which constitute approximately 11% of energy consumption.

Evolving Business Models and Nature of Collaboration Between Firms and Service Vendors

The MEP sector is witnessing a fundamental shift in business models, characterized by strategic partnerships and technological integration. Notable collaborations, such as the partnership between eVolve MEP and ENGworks Global, are establishing new industry content standards and improving interoperability for MEP subcontractors, technology providers, and building product manufacturers. These partnerships are driving innovation in construction virtual design (VDC) and content creation, while also focusing on developing Revit-based BIM software specifically for MEP construction. The evolution of service delivery models has also led to the adoption of Software as a Service (SaaS) solutions, where engineering companies can access sophisticated tools through more manageable monthly subscriptions rather than traditional licensing models.

The industry is experiencing a significant transformation in how MEP services companies deliver through the integration of advanced technologies and collaborative approaches. The adoption of 4D and 5D Building Information Modeling (BIM) technologies is enabling more sophisticated project planning and execution, considering various site constraints such as working methods, equipment capacity, time, and material schedules. This technological evolution is complemented by the implementation of Robotic Total Stations (RTS) for work tracking and model referencing, creating a more integrated and efficient service delivery system. These advancements are fostering closer collaboration between MEP industries and their clients, enabling more comprehensive solutions that address both immediate project needs and long-term operational efficiency.

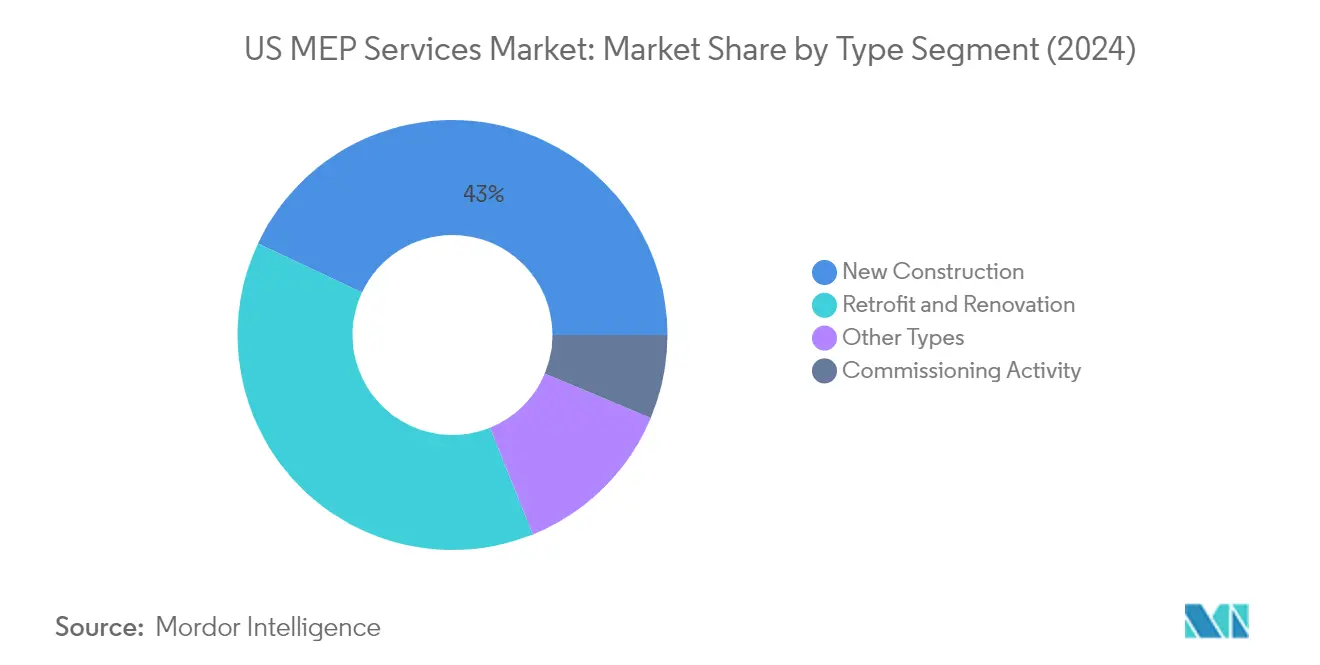

Segment Analysis: By Type

New Construction Segment in US MEP Services Market

The new construction segment dominates the US MEP services market, accounting for approximately 43% of the total market value in 2024. This segment's prominence is driven by the steady growth in construction spending across various sectors, including commercial, healthcare, and educational institutions. The engineering and construction industry is witnessing significant transformation with the adoption of smart technologies, modular construction methods, and evolving government regulations pushing companies to adapt to disruption and rethink possibilities. MEP construction firms are positioned as active participants in building a smart, connected future, with particular emphasis on sustainable development and energy efficiency in new constructions. The segment's growth is further supported by various infrastructure upgrade initiatives and the expansion of smart city mega-projects across the United States.

Remaining Segments in US MEP Services Market by Type

The retrofit and renovation segment represents a significant portion of the market, focusing on improving existing building performance through enhanced energy efficiency, increased staff productivity, and reduced maintenance costs. The commissioning activity segment plays a crucial role in ensuring that newly constructed buildings and their systems meet clients' expectations through systematic verification and documentation processes. The other types segment encompasses specialized services for data centers, research facilities, and multi-dwelling buildings, addressing unique requirements such as critical infrastructure support, specialized environmental controls, and complex system integration needs. Each of these segments contributes to the market's comprehensive service offering, meeting diverse client needs across different phases of building lifecycle management.

Segment Analysis: By End-User Vertical

Healthcare Segment in US MEP Services Market

The healthcare segment has emerged as a dominant force in the US MEP services market, commanding approximately 17% of the total market share in 2024. This significant market position is driven by the increasing complexity of healthcare facilities requiring specialized MEP mechanical and MEP electrical solutions for optimal facility design and operation. Healthcare facilities demand robust MEP systems due to their critical nature, where factors like internal air quality, proper ventilation, and uninterrupted power supply directly impact patient care and safety. The sector's prominence is further reinforced by the ongoing expansion and modernization of healthcare infrastructure across the United States, with facilities incorporating advanced MEP technologies to ensure efficient operation of specialized equipment and maintain stringent healthcare environment standards.

Public Spaces and Institutions Segment in US MEP Services Market

The public spaces and institutions segment is demonstrating remarkable growth potential in the US MEP services market, with projections indicating a robust growth trajectory of approximately 17% during the forecast period 2024-2029. This accelerated growth is primarily attributed to the increasing focus on modernizing public infrastructure, including transportation hubs, government facilities, and social institutions. The segment's growth is further propelled by the rising adoption of smart building technologies in public spaces, requiring sophisticated MEP systems for enhanced energy efficiency and operational effectiveness. The integration of digital transformation initiatives in public buildings, coupled with the emphasis on sustainable and energy-efficient solutions, continues to drive the demand for advanced MEP services in this sector.

Remaining Segments in End-User Vertical

The US MEP services market encompasses several other significant segments, including commercial offices, educational institutions, industrial establishments & warehouses, and other commercial entities. The commercial offices segment is characterized by its focus on energy-efficient building systems and smart building technologies. Educational institutions demonstrate steady demand driven by campus modernization and sustainability initiatives. The industrial MEP services segment is marked by the need for specialized MEP design services for industrial facilities and automated warehouses. Other commercial entities, including data centers and research facilities, contribute significantly to the market with their unique requirements for precision engineering and advanced MEP systems.

US MEP Services Industry Overview

Top Companies in US MEP Services Market

The US MEP services market features prominent players like Jacobs Engineering, HDR Inc., Arup Group, AECOM, and WSP Group leading the competitive landscape through comprehensive service portfolios. These MEP companies in USA are actively pursuing technological innovation through the integration of Building Information Modeling (BIM), 3D modeling capabilities, and advanced design software to enhance project delivery efficiency. Market leaders are increasingly focusing on sustainable and energy-efficient solutions, particularly in green building initiatives and LEED certification projects. Companies are strengthening their positions through strategic acquisitions and partnerships to expand geographical presence and service capabilities, while simultaneously investing in specialized expertise across various sectors including healthcare, commercial, and data centers. The competitive dynamics are further shaped by investments in digital transformation, with companies developing integrated platforms for project management and client collaboration.

Market Structure Shows Dynamic Competitive Environment

The US MEP services market exhibits a moderately fragmented structure with both global engineering conglomerates and specialized local players competing for market share. The landscape is characterized by a mix of large multinational firms that offer end-to-end engineering solutions and regional specialists that focus on specific market segments or geographical areas. Market consolidation is actively occurring through strategic mergers and acquisitions, with larger firms acquiring smaller specialized companies to enhance their service offerings and expand their geographical footprint. The competitive environment is further intensified by the presence of employee-owned firms that leverage their organizational structure to foster innovation and maintain high service quality.

The market demonstrates strong merger and acquisition activity, particularly focused on expanding MEP services capabilities and gaining access to new geographical markets or specialized expertise. Companies are increasingly pursuing strategic partnerships to complement their existing capabilities and create comprehensive solution offerings. The competitive dynamics are influenced by the growing trend of firms seeking to provide integrated services that combine traditional mechanical, electrical, and plumbing services with emerging technologies and sustainable solutions. Market players are also focusing on developing long-term relationships with government entities and private sector clients, while simultaneously expanding their presence in high-growth sectors such as healthcare and data centers.

Innovation and Adaptability Drive Future Success

Success in the MEP services market increasingly depends on firms' ability to adapt to evolving technological requirements and sustainability demands. Companies must invest in developing specialized expertise across various sectors while maintaining operational flexibility to address diverse client needs. The competitive landscape is being shaped by the growing emphasis on sustainable building practices and energy efficiency, requiring firms to develop innovative solutions that align with these requirements. Market players need to focus on building strong relationships with key stakeholders while simultaneously investing in digital capabilities to enhance service delivery and project management efficiency.

Future market success will be determined by companies' ability to navigate regulatory requirements while maintaining cost competitiveness and service quality. Firms must develop strategies to address the increasing concentration of end-users in specific sectors while maintaining diversification across multiple market segments. The competitive environment is influenced by the need to balance specialized expertise with broad service capabilities, particularly as clients seek integrated solutions providers. Companies must also focus on talent retention and development while investing in new technologies and sustainable practices to maintain their competitive edge. The ability to provide value-added services while managing operational costs will be crucial for both established players and new entrants in the market.

US MEP Services Market Leaders

-

Jacobs Engineering Group Inc.

-

HDR Inc

-

Arup Group

-

AECOM

-

MEP Engineering

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

US MEP Services Market News

- February 2021 - Bowman Consulting Group, Ltd., acquired KTA Group, Inc. KTA is a forty-person engineering firm with core expertise in mechanical, electrical, and plumbing engineering, commissioning third-party plan review, and lighting design. The move supports Bowman's continued growth and substantially broadens its scope of service offerings.

- May 2021 - AECOM, which is an infrastructure consulting firm, announced that it was selected to provide program management services for Phase 1 of the USD 3.5 billion Dallas Independent School District (DISD) 2020 Bond Program, which was the company's fourth consecutive contract with the district. The company has previously provided program management services for DISD's 2002, 2008, and 2015 Bond Programs. The company will provide oversight and coordination of designers, consultants, contractors, and vendors and estimating, scheduling, and program control services on the projects encompassing the construction of new facilities and upgrades to the existing facilities.

US MEP Services Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Design and Engineering Services Industry

- 4.4 Current Employment Index of MEP Engineers in the United States

- 4.5 Impact of Technological Advancements on the MEP Services Industry (CAD, BIM, MEP Software, etc.)

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Growing Emphasis on Outsourcing of MEP Services to Focus on Core Offering

- 5.1.2 Steady Demand from Commercial and Healthcare Institutions

- 5.1.3 Evolving Business Models and Nature of Collaboration between Firms and Service Vendors

-

5.2 Market Restraints

- 5.2.1 Operational Challenges in High Market Concentration and Growing Demand for End-to-end Offering Affect Smaller Firms

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 New Construction

- 6.1.2 Retrofit & Renovation

- 6.1.3 Commissioning Activity

- 6.1.4 Other Types

-

6.2 By End-user Vertical

- 6.2.1 Healthcare

- 6.2.2 Commercial Offices

- 6.2.3 Educational Institutions

- 6.2.4 Public Spaces and Institutions

- 6.2.5 Industrial establishments & Warehouses

- 6.2.6 Other Commercial entities (Data centers, Research, etc.)

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Jacobs Engineering Group Inc.

- 7.1.2 HDR Inc

- 7.1.3 Arup Group

- 7.1.4 AECOM

- 7.1.5 MEP Engineering

- 7.1.6 Stantec Inc.

- 7.1.7 Affiliated Engineers Inc.

- 7.1.8 Macro Services

- 7.1.9 WSP Group

- 7.1.10 AHA Consulting

- 7.1.11 Burns Engineering

- 7.1.12 Wiley Wilson

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

US MEP Services Industry Segmentation

MEP Services encompasses the design, engineering, consulting, and maintenance-related activities provided by engineering firms across a wide range of end-user verticals. The study's scope includes MEP services provided to new and renovated installations in a wide range of end-user verticals, such as healthcare, industrial facilities, commercial offices, public buildings, educational institutions, and other verticals. The study tracks the impact of COVID-19 on the overall industry landscape.

| By Type | New Construction |

| Retrofit & Renovation | |

| Commissioning Activity | |

| Other Types | |

| By End-user Vertical | Healthcare |

| Commercial Offices | |

| Educational Institutions | |

| Public Spaces and Institutions | |

| Industrial establishments & Warehouses | |

| Other Commercial entities (Data centers, Research, etc.) |

Need A Different Region or Segment?

Customize Now

US MEP Services Market Research FAQs

How big is the United States (US) MEP Services Market?

The United States (US) MEP Services Market size is expected to reach USD 51.81 billion in 2025 and grow at a CAGR of 14.15% to reach USD 100.42 billion by 2030.

What is the current United States (US) MEP Services Market size?

In 2025, the United States (US) MEP Services Market size is expected to reach USD 51.81 billion.

Who are the key players in United States (US) MEP Services Market?

Jacobs Engineering Group Inc., HDR Inc, Arup Group, AECOM and MEP Engineering are the major companies operating in the United States (US) MEP Services Market.

What years does this United States (US) MEP Services Market cover, and what was the market size in 2024?

In 2024, the United States (US) MEP Services Market size was estimated at USD 44.48 billion. The report covers the United States (US) MEP Services Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United States (US) MEP Services Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

United States (US) MEP Services Market Research

Mordor Intelligence delivers a comprehensive analysis of the mechanical electrical and plumbing (MEP) services industry. We leverage our extensive expertise in MEP market research and consulting. Our detailed report examines the evolving landscape of MEP services across the United States. It encompasses commercial MEP services, industrial MEP services, and MEP services in buildings. As a leading MEP service provider analysis firm, we offer detailed insights into MEP systems, MEP construction, and emerging trends in the US MEP sector.

The report provides stakeholders with actionable intelligence on MEP companies in USA and their service offerings, including MEP design services and MEP retrofitting services. Our analysis covers key aspects of mechanical electrical and plumbing services delivery, from MEP construction services to specialized commercial MEP applications. The report, available as an easy-to-download PDF, includes detailed MEP data and MEP statistics. These details benefit industry participants, from MEP services companies to investors exploring opportunities in the MEP sector. Our comprehensive coverage extends to MEP services in buildings and emerging trends in MEP industries, providing valuable insights for strategic decision-making.