Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

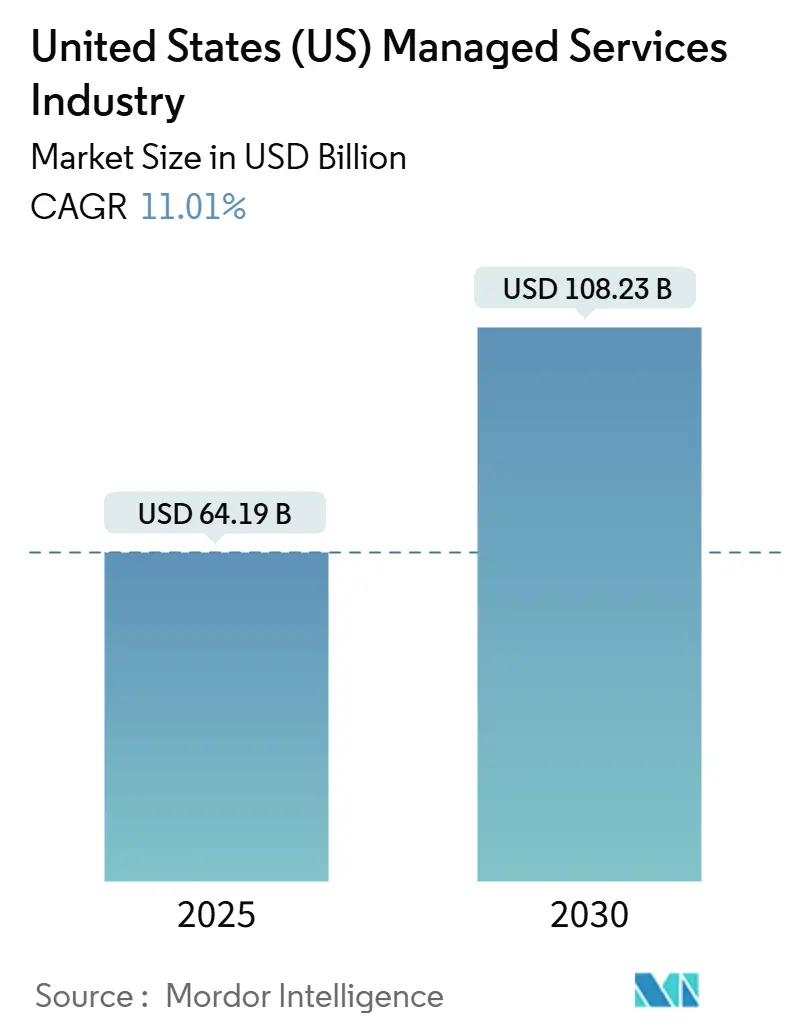

| Market Size (2025) | USD 64.19 Billion |

| Market Size (2030) | USD 108.23 Billion |

| Growth Rate (2025 - 2030) | 11.01% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States (US) Managed Services Industry Analysis by Mordor Intelligence

The United States managed services market size is estimated at USD 64.19 billion in 2025 and is forecast to reach USD 108.23 billion by 2030, reflecting an 11.01% CAGR. Expansion is propelled by enterprise migration to hybrid-cloud architectures, rising cyber-insurance prerequisites that make professional security oversight mandatory, and AI-Ops automation that lifts provider margins and service quality. Large private-equity inflows accelerate consolidation, while domestic data-sovereignty requirements favor providers that maintain U.S.-based operations. At the same time, acute skills shortages inflate labor costs and challenge smaller firms’ profitability. Together, these forces create a dynamic environment in which technological differentiation and regulatory expertise determine competitive success.

Key Report Takeaways

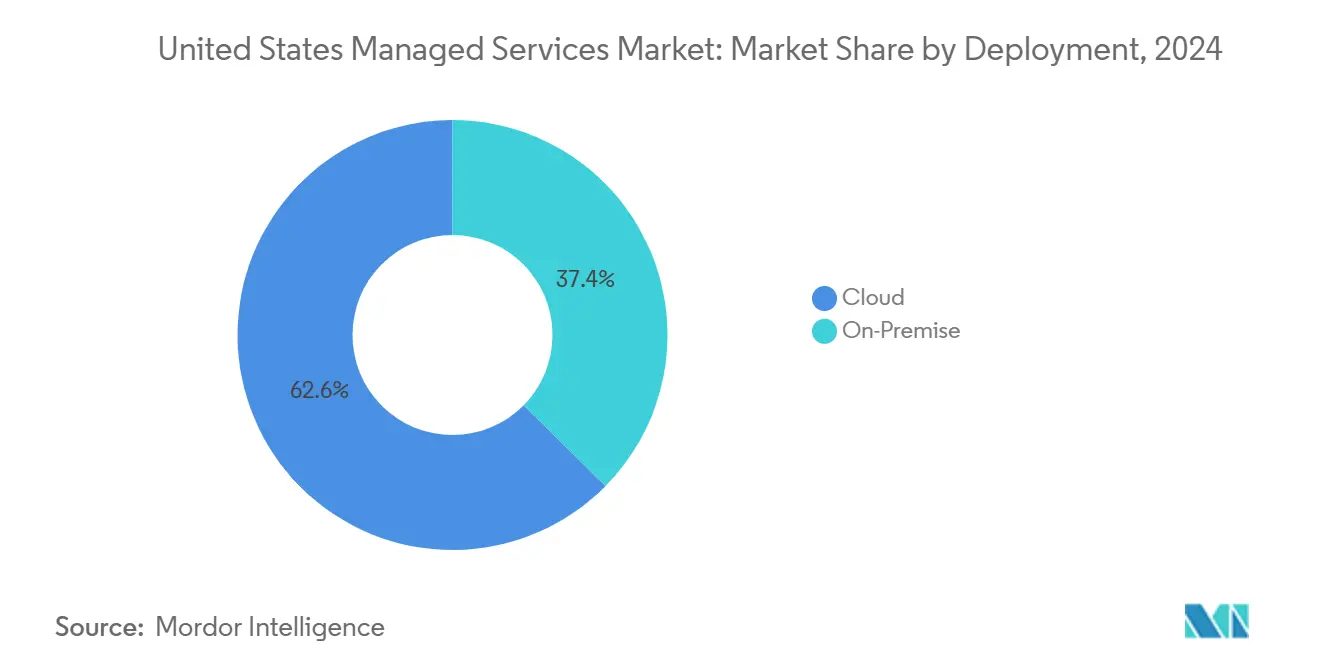

- By deployment, cloud deployment led with 62.6% revenue share in 2024, and the segment is expanding at a 13.1% CAGR through 2030.

- By service type, managed security services held 28.5% of the United States managed services market share in 2024, while managed mobility is projected to grow at an 11.3% CAGR through 2030.

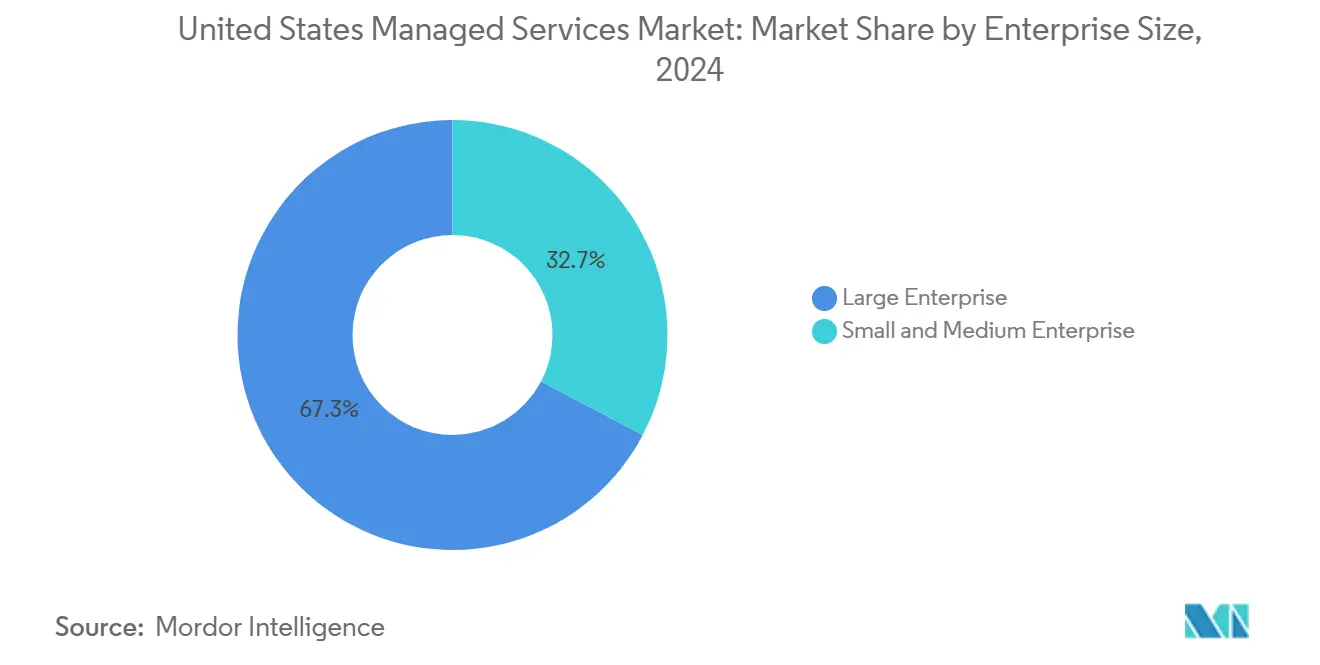

- By enterprise size, large enterprises accounted for 67.3% share of the United States managed services market size in 2024; small and medium enterprises are expanding at a 12.7% CAGR through 2030.

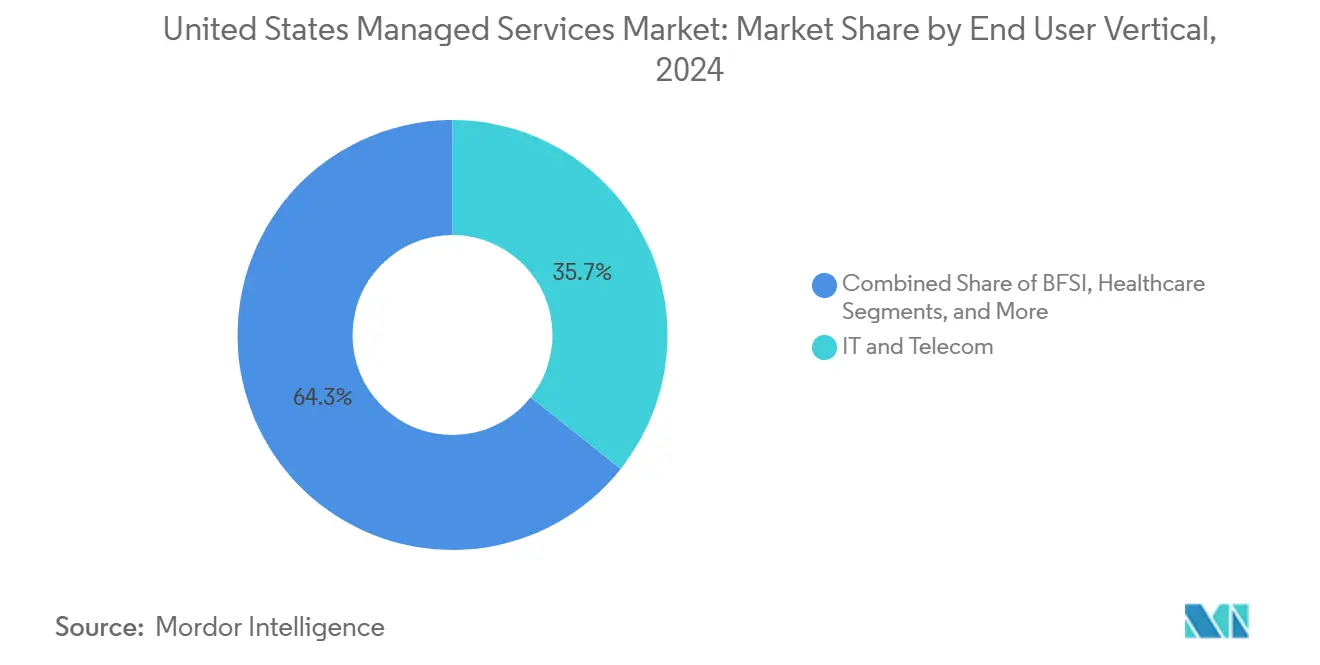

- By end-user vertical, IT and telecom captured 35.7% revenue share in 2024, whereas healthcare is advancing at an 11.7% CAGR through 2030.

United States (US) Managed Services Industry Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing enterprise shift toward hybrid-cloud management | +2.8% | National, tech hubs | Medium term (2-4 years) |

| Surge in multi-cloud complexity driving demand for centralized MSPs | +2.1% | Global, enterprise markets | Short term (≤ 2 years) |

| Rapid escalation of cyber-insurance prerequisites | +1.9% | National, regulated industries | Short term (≤ 2 years) |

| SME preference for OPEX-based IT | +1.7% | National, SMB markets | Long term (≥ 4 years) |

| Edge-computing rollouts in U.S. manufacturing hubs | +1.4% | Regional, manufacturing centers | Medium term (2-4 years) |

| AI-Ops automation boosting MSP margins | +1.2% | National, early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Growing Enterprise Shift Toward Hybrid-Cloud Management

Hybrid-cloud adoption forces organizations to orchestrate workloads across public and private environments, creating demand for specialized managed services. Microsoft’s alliance with Oracle and Lumen Technologies illustrates the integration complexity enterprises face when operating multiple clouds.[1]Tom Burt, “Microsoft Expands Oracle Interconnect to New Regions,” Microsoft, microsoft.comCoca-Cola’s USD 1.1 billion, five-year pact with Microsoft—maintained alongside its AWS footprint—underscores how enterprise multi-cloud strategies necessitate external management expertise. MSPs capture recurring high-margin revenue by positioning hybrid-cloud management as strategic enablement rather than cost containment, elevating their role in enterprise digital-transformation roadmaps.

Surge in Multi-Cloud Complexity Driving Demand for Centralized MSPs

An estimated 89% of U.S. enterprises now use more than one cloud, amplifying security, cost-optimization, and data-portability challenges that exceed internal IT capacity.[2]“Multi-Cloud Management Survey 2024,” Cloud4C, cloud4c.com Verizon Business has embedded multi-cloud management in its network-as-a-service portfolio to address these pain points. MSPs gain advantage by remaining platform-agnostic, mitigating vendor lock-in and appealing to regulated sectors that demand data-sovereignty assurances. Resulting scale requirements spur sector consolidation as smaller firms unable to fund multi-cloud R&D become acquisition targets for platform providers.

Rapid Escalation of Cyber-Insurance Prerequisites

Insurers now require controls such as continuous monitoring to issue cyber policies, expanding demand for managed security services. The average breach cost of USD 4.45 million elevates professional security management to a non-discretionary spend category, especially after the SEC mandated incident disclosure within four business days.[3]Kevin Breen, “SEC Cybersecurity Rules Explained,” Cado Security, cadosecurity.comMSPs that bundle compliance-ready security frameworks into standard offerings enjoy resilient revenue even during macroeconomic slowdowns.

SME Preference for OPEX-Based IT

Cash-flow-constrained SMEs accelerate adoption of subscription-priced IT, fueling the fastest-growing customer segment. Managed IT packages priced from USD 150 to USD 400 per user monthly deliver enterprise-grade capabilities without capital outlay. Healthcare clinics, for example, obtain HIPAA-compliant electronic medical records via MSPs rather than investing in on-premise infrastructure. Providers respond with verticalized bundles that command premium pricing while enhancing customer retention.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills shortage inflates U.S. MSP labor costs | -1.8% | National, tech centers | Short term (≤ 2 years) |

| Vendor lock-in fears among regulated industries | -1.2% | National, BFSI and healthcare | Medium term (2-4 years) |

| Rising compliance burden from SEC cybersecurity rules | -0.9% | National, public companies | Short term (≤ 2 years) |

| Data-sovereignty pushback on offshore NOC models | -0.7% | National, critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skills Shortage Inflates U.S. MSP Labor Costs

High demand for cloud, cybersecurity, and AI specialists drives wage inflation that erodes margins; 87% of MSPs report insufficient AI expertise to satisfy clients. Larger providers invest in automation and training partnerships to offset labor scarcity, widening the competitive gap versus smaller firms and intensifying consolidation pressures.

Vendor Lock-In Fears Among Regulated Industries

Banks and healthcare systems resist single-vendor dependencies that complicate regulatory oversight. Requirements for HIPAA and FFIEC compliance compel MSPs to demonstrate multi-platform capabilities and robust exit clauses, increasing service-delivery complexity and dampening margins. Niche providers with sector-specific compliance expertise seize share by mitigating lock-in risk for regulated clients.

Geography Analysis

Demand for managed services is nationwide but clusters around technology, finance, and manufacturing corridors. Silicon Valley, Seattle, and Austin emphasize cloud optimization and AI-Ops, while New York and Charlotte generate compliance-focused projects for financial institutions. Manufacturing hubs in the Midwest and Southeast adopt managed edge services to support Industry 4.0 initiatives; BMW’s Spartanburg private-5G deployment and Hyundai’s USD 7.6 billion Georgia Metaplant exemplify this regional trend.

Healthcare systems across all regions rapidly outsource IT operations to meet Centers for Medicare & Medicaid Services (CMS) mandates on electronic health records and patient-data security. Federal and state agencies are expanding managed-security contracts, yet procurement hurdles limit smaller providers’ participation. Data-sovereignty concerns, especially in critical-infrastructure states, strengthen the competitive position of providers that operate domestic network operations centers.

Segment Analysis

By Deployment: Cloud Dominance Accelerates

Cloud deployment held 62.6% of the United States managed services market share in 2024, and the segment is forecast to expand at a 13.1% CAGR to 2030. This growth pushes the United States managed services market size for cloud-based offerings toward the USD 108 billion overall forecast value. Cloud’s popularity stems from elastic scaling, integrated security features, and quick implementation. Partnerships such as Microsoft-Oracle expand interoperability, while AWS and NVIDIA’s generative-AI collaboration showcases how cloud platforms evolve to host advanced workloads.

On-premise and hybrid solutions remain relevant in regulated sectors that require domestic data processing. Providers are layering edge-computing nodes onto cloud deployments to support latency-sensitive manufacturing use cases. The trend deepens client reliance on MSP expertise in orchestrating distributed environments and strengthens recurring revenue streams tied to performance-based SLAs.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Service Type: Security Leadership Drives Innovation

Managed security services held 28.5% of the United States managed services market share in 2024, reflecting inelastic demand linked to cyber-insurance and regulatory mandates. Managed mobility, although smaller, is projected to register an 11.3% CAGR through 2030, underscoring enterprise priorities around workforce enablement. Cross-selling opportunities arise as mobility projects invariably require integrated security controls.

Data-center management continues to provide steady revenue by supporting hybrid-cloud deployments, while unified-communications packages evolve into collaboration suites combining voice, video, and AI-enabled transcription. Providers differentiate through proprietary AI-Ops platforms that predict incidents and automate remediation, elevating service quality and protecting margins amid labor cost inflation.

By Enterprise Size: SME Growth Acceleration

Large enterprises captured 67.3% of the United States managed services market size in 2024 and continue to procure custom AI-Ops and compliance bundles. SMEs, however, are climbing at a 12.7% CAGR and represent the fastest-expanding revenue pool. Subscription models priced per user make enterprise-grade cybersecurity and cloud management attainable for smaller entities.

Distinct go-to-market strategies emerge: MSPs chasing large accounts invest in dedicated service teams, whereas SME-focused providers pursue standardized, highly automated delivery that supports volume growth without proportional labor expansion. Vertical specialization—particularly in healthcare and professional services—helps smaller MSPs defend margins against mass-market competitors.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Vertical: Healthcare Transformation Leads

IT and telecom customers commanded 35.7% of 2024 revenue thanks to early cloud and network modernization. Healthcare, advancing at an 11.7% CAGR, is reshaping demand profiles as hospitals digitize patient records and deploy telehealth platforms. Independent Health’s partnership with NTT DATA illustrates how managed service contracts elevate operational performance while meeting rigorous compliance standards.

Banking and financial services maintain steady reliance on MSPs for cyber-threat monitoring and regulatory reporting. Retailers increasingly outsource omnichannel infrastructure, and manufacturers adopt managed edge solutions to support 5G-enabled factories. These sector-specific trends intensify competition around compliance knowledge and specialized toolsets rather than pricing alone.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Competitive Landscape

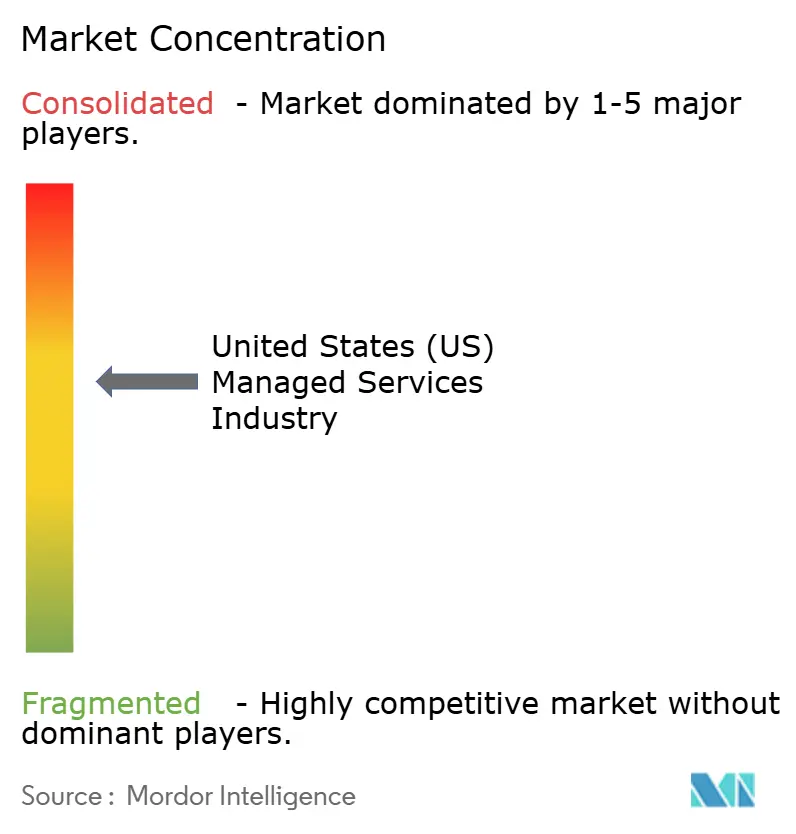

Roughly 40,000 companies participate in the United States managed services market, keeping concentration low despite brisk M&A activity. Private-equity-backed roll-ups by Ntiva, Fulcrum IT, and New Charter Technologies raised sector deal volume an estimated 50% in 2024. Fragmentation favors providers that can differentiate via proprietary automation or vertical compliance offerings.

Cybersecurity capabilities have become table stakes; acquisitions such as PDI Technologies’ purchase of MSSP Nuspire extend service portfolios to meet insurer and regulator standards. AI-native entrants like CoSupport AI automate ticket resolution and customer communications, reducing cost-to-serve. Hyperscale cloud vendors now bundle managed services directly, challenging traditional MSPs but also opening partnering models for co-branded delivery.

Competitive success hinges on balancing advanced technology adoption with specialized human expertise. Providers that master AI-Ops, maintain domestic data centers, and hold deep vertical knowledge capture premium pricing and stronger client retention, while under-capitalized firms gravitate toward merger or exit.

United States (US) Managed Services Market Leaders

-

Accenture plc

-

ATandT Inc.

-

CDW Corporation

-

Cisco Systems Inc.

-

Cognizant Technology Solutions

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: NWN Corporation acquired InterVision Systems, expanding customer-experience and cybersecurity portfolios.

- April 2025: Netrio and Success Computer Consulting bought PCA Technology Group, strengthening SMB coverage.

- April 2025: One Source acquired CT Solutions to broaden managed-IT reach.

- February 2025: New Charter Technologies purchased Verus, its first 2025 deal focused on co-managed services.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the United States managed services market as the recurring revenue that third-party providers earn for continuously operating, monitoring, and optimizing clients' IT infrastructure, networks, security stacks, and collaboration workloads under subscription or outcome-based contracts.

(Scope exclusions) One-off consulting projects, break-fix support, cloud-license resale margins, and any services delivered outside U.S. borders are left out.

Segmentation Overview

- By Deployment

- On-premise

- Cloud

- By Service Type

- Managed Data Center

- Managed Security

- Managed Communications

- Managed Network

- Others

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By End-user Vertical

- BFSI

- IT and Telecom

- Healthcare

- Entertainment and Media

- Retail

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted expert interviews and online surveys with MSP executives, CIOs in BFSI, healthcare, retail, and manufacturing, regional channel partners, and cybersecurity consultants across every U.S. census division. These discussions clarified adoption triggers, average seat volumes, and price-escalation norms, filling data gaps revealed during desk work.

Desk Research

We began with government datasets, Bureau of Labor Statistics ICT spending tables, the U.S. Census Quarterly Services Survey, and International Trade Administration shipment codes, which ground the demand pool in hard economic signals. Industry groups such as CompTIA, the National Cybersecurity Alliance, and the Telecommunications Industry Association supplied penetration ratios and median contract pricing. Company 10-Ks, earnings calls, and reputable press feeds enriched provider-level splits, while paid repositories like D&B Hoovers and Dow Jones Factiva helped us cross-check revenue lines and M&A activity. The sources named illustrate our desk research lattice; many additional public and proprietary references were consulted for completeness.

Market-Sizing & Forecasting

A top-down demand pool starts with national IT services outlay, then applies outsourcing propensity, hybrid-cloud workload share, and managed security uptake to size the addressable pie. Selective bottom-up checks, supplier roll-ups, sampled ASP × managed-device counts, and data-center footprint audits are used to validate and tune totals. Core variables feeding our multivariate regression include cybersecurity incident counts, 5G private-network deployments, SME IT hiring gaps, MSP seat-price indices, and cloud-migration ratios. Scenario analysis layers macro or regulatory shocks onto the base case before final numbers are locked.

Data Validation & Update Cycle

Outputs pass three analyst reviews; outliers spark re-engagement with sources, and any material event, large M&A, new cyber mandate, or federal stimulus, triggers an interim refresh. Full rebuilds occur annually, so clients always receive the latest view.

Why Mordor's US Managed Services Baseline Commands Reliability

Published figures differ because firms track unlike service mixes, apply varied currency conversions, and refresh their models on dissimilar cadences.

Key gap drivers we observe are the folding in of project-based services, inclusion of Canadian and Mexican revenue within 'U.S.' totals, and optimistic escalation factors that lack primary validation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 64.19 B (2025) | Mordor Intelligence | - |

| USD 88.13 B (2024) | Global Consultancy A | Bundles hosted MIS and resale margins; scant primary inquiry |

| USD 93.88 B (2024) | Industry Association B | Counts advisory projects; omits long-tail MSPs |

| USD 130.11 B (2024) | Trade Journal C | Uses North America scope; aggressive CAGR without device-level checks |

The comparison shows that by anchoring to verifiable U.S. recurring revenue, reconciling top-down and bottom-up signals, and refreshing inputs through live market conversations, Mordor provides a balanced, transparent benchmark that decision-makers can trust.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the United States managed services market?

It stands at USD 64.19 billion in 2025 and is forecast to reach USD 108.23 billion by 2030.

Which deployment model dominates managed services in the United States?

Cloud deployment leads with 62.6% revenue share and is projected to expand at a 13.1% CAGR through 2030.

Why are managed security services growing so quickly?

Cyber-insurance mandates and stringent SEC disclosure rules make professional security oversight non-negotiable, driving 28.5% market share for managed security services in 2024.

What regions in the United States show the strongest demand for managed services?

Technology corridors in California and Washington emphasize cloud management, financial centers in New York and Charlotte demand compliance support, and manufacturing hubs in the Midwest and Southeast adopt edge-driven managed services.

Page last updated on: