Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

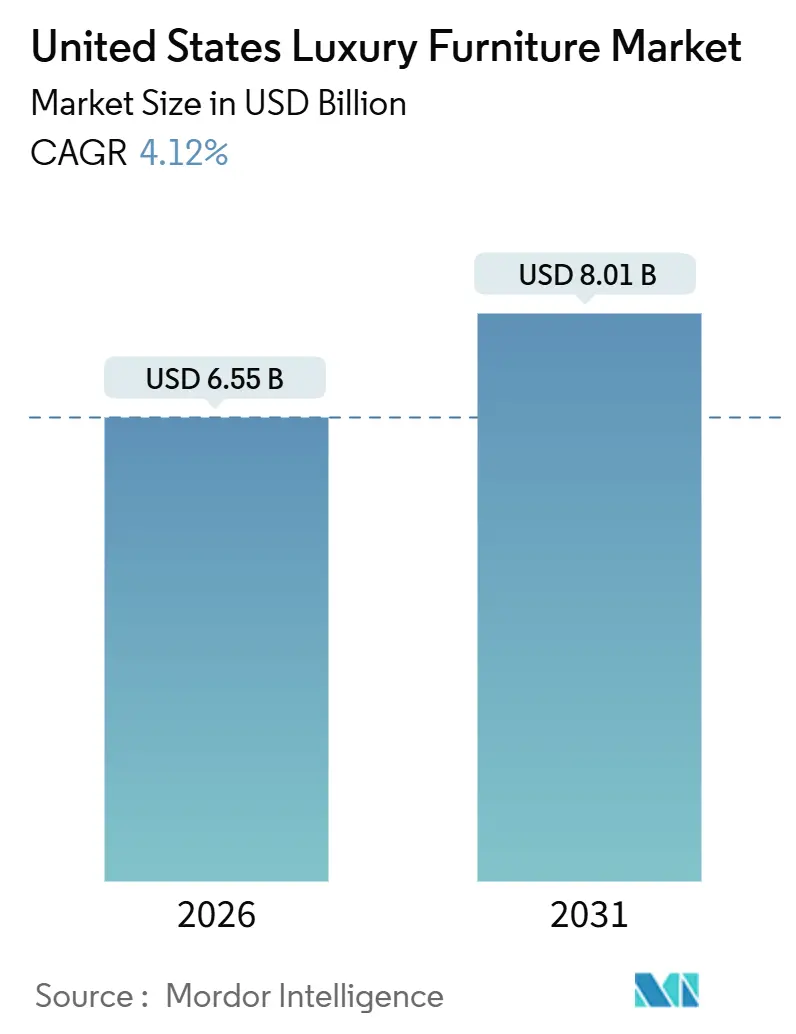

| Market Size (2026) | USD 6.55 Billion |

| Market Size (2031) | USD 8.01 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Luxury Furniture Market Analysis by Mordor Intelligence

The United States Luxury Furniture Market size is estimated at USD 6.55 billion in 2026, and is expected to reach USD 8.01 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031).

Affluent households are prioritizing furniture with craftsmanship, durability, and integrated technology over branding. Post-pandemic lifestyle changes, a focus on wellness, and the rise of outdoor living spaces are reshaping preferences, while sustainability expectations influence material choices. High-net-worth consumers demand immersive online tools, prompting manufacturers to adopt technologies like augmented reality (AR) and product-configuration software. Established brands maintain market share through vertically integrated supply chains, but authenticated resale and "quiet luxury" aesthetics challenge traditional pricing models. As wealth concentration grows and homes become multifunctional spaces, the market will focus on increasing wallet share within a resilient customer base.

Key Report Takeaways

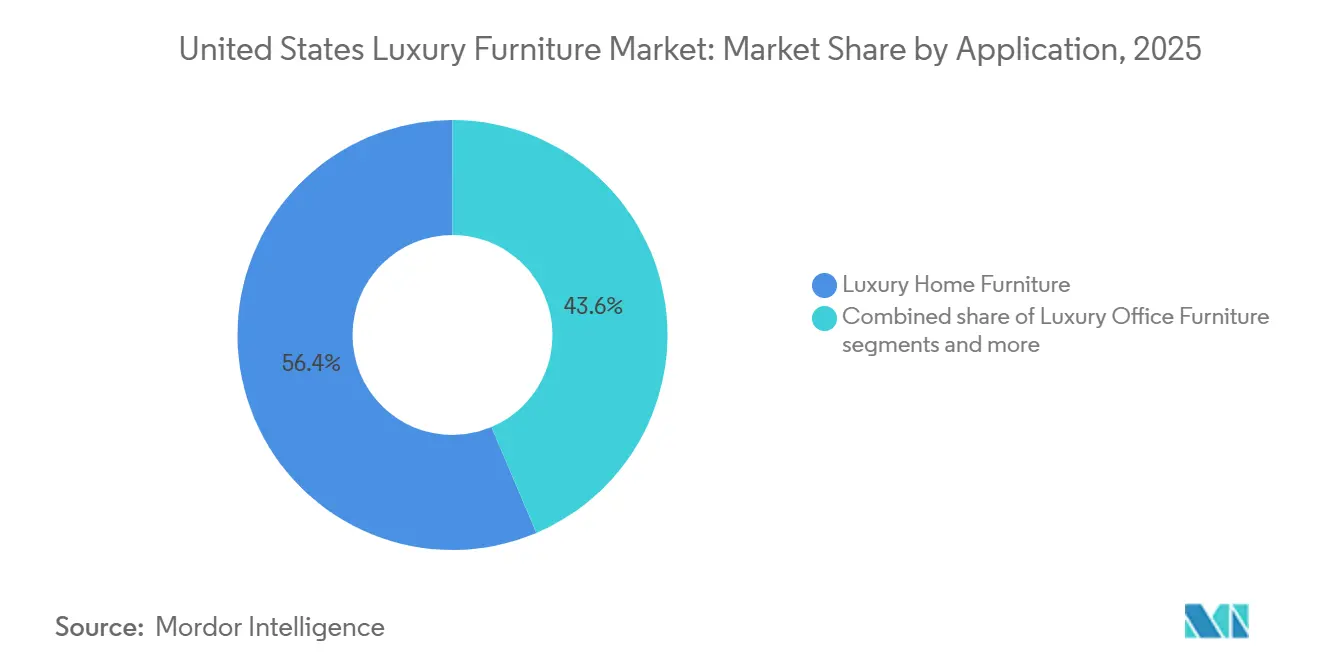

- By application, luxury home furniture accounted for 56.38% of the United States luxury furniture market share in 2026, while the outdoor and patio category is forecast to expand at a 9.17% CAGR through 2031.

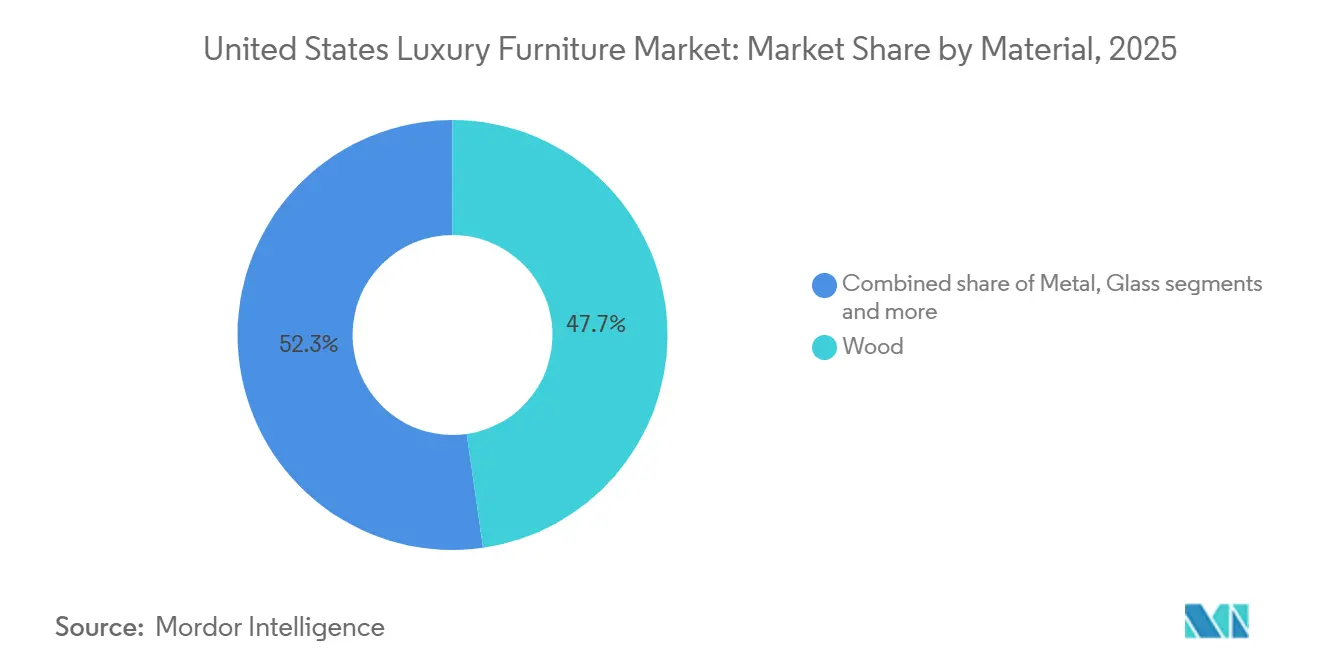

- By material, wood held 47.74% of the United States luxury furniture market size in 2026, whereas sustainable and green materials are projected to grow at a 9.82% CAGR through 2031.

- By distribution channel, B2C retail captured 66.75% of the United States luxury furniture market size in 2026, while online flagship stores are expected to advance at a 13.39% CAGR through 2031.

- By geography, the South commanded 35.38% of the United States luxury furniture market share in 2026, whereas the West region is set to post the fastest 8.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Luxury Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising population of ultra‑high‑net‑worth households | +1.2% | Nationwide, with the strongest concentration in major metros across the West and Northeast | Long term (≥ 4 years) |

| Increasing demand for premium outdoor living environments | +0.9% | Predominantly in the South and West, especially Sunbelt regions | Medium term (2–4 years) |

| Acceleration of smart‑home technology upgrades | +0.7% | Initially in Western tech hubs, expanding into urban centres in the Northeast | Medium term (2–4 years) |

| Growing influence of the “quiet luxury” aesthetic | +0.5% | Nationwide, with early adoption in coastal metropolitan areas | Short term (≤ 2 years) |

| Greater availability of ESG‑driven real‑estate financing | +0.4% | National, with the strongest traction in LEED‑focused commercial developments | Long term (≥ 4 years) |

| Growth of luxury e‑commerce and augmented‑reality shopping tools | +0.6% | Nationwide, with the fastest uptake among digitally native consumer groups | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Rising population of ultra‑high‑net‑worth households

Between 2024 and 2025, affluent families with net worths exceeding USD 30 million experienced significant growth. This increase has driven strong demand, largely unaffected by fluctuations in mortgage-rate cycles, sustaining a resilient luxury market. These buyers, concentrated in coastal technology hubs and select Sunbelt regions, frequently replace luxury items and commission bespoke pieces. They rely on interior designers, family offices, and wealth advisors to guide purchases toward brands with artisanal craftsmanship and transparent supply chains. Manufacturers failing to establish direct relationships with these influencers risk commoditization as Ultra-High-Net-Worth (UHNW) consumers prefer curated, exclusive portfolios. This trend highlights the importance of exclusivity and long-term service commitments in attracting and retaining UHNW clientele.

Increasing demand for premium outdoor living environments

In Texas, Florida, Arizona, and California, high-end patios, decks, and poolside areas are becoming key design features. Homeowners prioritize modular seating, weather-resistant hardwoods, and solution-dyed textiles for year-round functionality without compromising aesthetics. This trend aligns with the wellness movement, emphasizing outdoor spaces for entertaining and meditation as part of personal health routines. Suppliers managing longer lead times for teak, powder-coated aluminum, and marine-grade finishes achieve strong profit margins. They also educate consumers on maintenance practices to preserve colorfastness and structural integrity across multiple seasons. Outdoor spaces are increasingly viewed as extensions of indoor living, blending style with durability.

Acceleration of smart‑home technology upgrades

Wireless charging surfaces, hidden cable routing, and app-controlled seating ergonomics are becoming standard features for West Coast technophiles. Embedded sensors now track posture, ambient light, and sleep metrics, enabling subscription-based wellness insights driven by data analytics. Manufacturers must develop in-house Internet of Things (IoT) expertise or collaborate with technology platform providers to remain competitive. Seamless firmware updates and robust data security are critical for maintaining customer trust and ensuring product functionality. This shift redefines traditional product life cycles, emphasizing software support as much as physical durability for brand loyalty. The integration of IoT capabilities blurs the line between hardware and software, creating new challenges and opportunities for manufacturers.

Greater availability of ESG‑driven real‑estate financing

Institutional lenders increasingly attach interest-rate discounts to LEED (Leadership in Energy and Environmental Design) or WELL certification milestones, cascading sustainability mandates down to furnishing specifications[1].U.S. Green Building Council, “LEED Certification Standards and Requirements,” USGBC.ORG FSC-certified wood, low-VOC adhesives, and third-party verified recycled content are becoming table-stakes in commercial and, increasingly, upscale residential projects[2]Forest Stewardship Council, “FSC Certification in the United States,” FSC.ORG. Suppliers that demonstrate chain-of-custody documentation and Business and Institutional Furniture Manufacturer's Association (BIFMA) compliance enjoy accelerated procurement cycles and lower reputational risk[3]Business and Institutional Furniture Manufacturers Association, “Sustainability Standards for Furniture,” BIFMA.ORG. Smaller vendors, however, face higher per-unit testing costs, intensifying consolidation pressure as scale becomes essential to absorb certification overhead.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vacancy rates across commercial real estate | −0.8% | National, highest in the Northeast and Midwest cores | Short term (≤ 2 years) |

| Persistent supply‑chain delays for specialty and rare materials | −0.5% | Nationwide, especially import-dependent categories | Medium term (2–4 years) |

| Expansion of authenticated resale marketplaces is reducing demand for new premium goods | −0.4% | National, concentrated in dense metropolitan areas | Long term (≥ 4 years) |

| Expansion of luxury e-commerce & AR-enabled shopping experiences | |||

| Source: Mordor Intelligence | |||

Rising vacancy rates across commercial real estate

Remote and hybrid work models have increased vacancy rates in central business districts (CBDs) to over 20%. This trend has disrupted the consistent demand for contract office furniture, including desks, conference tables, and modular storage. Employers now prioritize collaborative lounges over high-density cubicles, reducing seat counts despite higher per-seat spending. Contract manufacturers are shifting focus to the hospitality sector and premium home-office niches to address changing market demands. Shorter production run-lengths and increased customization requirements are adding complexity to manufacturing schedules. These adjustments are necessary to remain competitive in the evolving market landscape shaped by workplace transformations.

Persistent supply‑chain delays for specialty and rare materials

Geopolitical tensions and stricter export regulations have extended lead times for Brazilian rosewood and premium Italian hides significantly. Smaller artisans without multi-year supply contracts face challenges like compressed margins or stock shortages during critical selling seasons. Many forward-thinking brands are exploring certified plantation hardwoods, mushroom-based leather alternatives, and recycled metals to mitigate supply chain risks. These brands must invest in rigorous testing to ensure new materials match the performance of traditional ones. Certified plantation hardwoods offer a sustainable alternative, but their adoption requires careful evaluation to meet client expectations. Mushroom-based leather alternatives are gaining traction, though their durability and scalability remain under scrutiny. Recycled metals provide an eco-friendly option, but brands must validate their quality to maintain customer trust.

Segment Analysis

By Application: Residential Dominance Meets Hospitality Resurgence

Luxury home furniture is projected to account for 56.38% of 2025 revenue in the United States, driven by remote work normalization and increased second-home ownership. Chairs and sofas have shorter replacement cycles, while beds, wardrobes, and built-in storage command higher transaction values despite longer usage. Dining tables have regained importance with the return of in-person entertaining, with extendable formats outperforming static designs. Outdoor lounges, dining sets, and cabanas now feature artisanal joinery and premium finishes, positioning outdoor spaces as year-round living extensions. Luxury hospitality furniture is recovering, supported by boutique hotel openings requiring visually appealing, durable designs that withstand commercial use without compromising aesthetics.

Office demand remains subdued, but executives outfitting high-end home workspaces sustain demand for ergonomic chairs and height-adjustable desks. Hospitality buyers prioritize FSC-certified timber, recycled metal frames, and CAL-117 compliant fabrics, favoring suppliers with documented compliance. Institutional segments like private education and concierge healthcare provide stable demand with long procurement cycles and low consumer sentiment sensitivity. The United States luxury furniture market diversifies its application mix, balancing cyclical residential spending with steady professional and institutional orders.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Sustainability Premiums Reshape Sourcing

Wood held a 47.74% market share in 2026, while sustainable and green materials are expected to grow at a 9.82% CAGR through 2031, exceeding the growth rate of the United States luxury furniture market by over 2.5 times. FSC-certified hardwoods like walnut and white oak meet environmental audit standards, and plantation-grown teak fulfills outdoor furniture needs without causing deforestation. Recycled aluminum and powder-coated steel frames support minimalist designs with strong strength-to-weight ratios, especially for cantilevered structures. Glass, valued for its reflective properties, enhances space perception in compact urban settings. Full-grain leather from Scandinavian tanneries remains a status symbol for executive seating, though vegan alternatives, such as mycelium and pineapple leaf-based materials, are gaining popularity among sustainability-focused buyers.

Manufacturers leveraging bio-based composites and closed-loop recycling programs gain early-mover advantages with ESG-focused institutional clients while reducing supply chain risks linked to geopolitical instability. Transparent lifecycle assessments, carbon footprint disclosures, and chain-of-custody documentation strengthen brand credibility and enable premium pricing strategies in the United States luxury furniture market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Digital Flagships Redefine Retail

B2C retail represented 66.75% of 2026 sales, while online flagship stores are expected to grow at a 13.39% CAGR through 2031, nearly three times the market rate. Physical showrooms are evolving into experiential hubs with design libraries, hospitality zones, and augmented-reality screens for real-time customization of fabrics, finishes, and dimensions. Home-center chains are adding curated luxury sections, but their limited advisory services hinder growth among ultra-high-net-worth (UHNW) shoppers. Specialty stores, despite higher real estate costs, excel in personalized consultations and premium logistics, often serving as local hubs for in-home trials and post-sale services.

The United States luxury furniture market relies on B2B channels, including hospitality, corporate, and institutional contracts, which require CAD-ready specifications, compliance with regulations, and volume-based pricing. Digitally native companies challenge traditional players with direct-to-consumer configurations, shorter lead times, and transparent pricing, pushing incumbents to refine value propositions and streamline operations. As omnichannel ecosystems mature, data orchestration - linking augmented reality interactions, showroom visits, and post-purchase services - has become critical for sustaining customer lifetime value in the United States luxury furniture market.

Geography Analysis

The South accounts for 35.38% of 2026 revenue, driven by population growth from higher-cost coastal metros, favorable tax policies, and strong residential construction in Texas, Florida, and the Carolinas. Outdoor living trends increase demand for weather-resistant teak lounges, modular pergolas, and fire-pit seating, leveraging the region's warm climate. Lower freight costs from Gulf Coast ports improve margins on imported hardwoods and finished goods, solidifying the South's role in the United States luxury furniture market.

The West is set to achieve an 8.98% CAGR through 2031, supported by technology-sector wealth in California and the Pacific Northwest, which drives high-value property renovations. Consumers favor minimalist, technology-integrated furniture aligned with Silicon Valley's design ethos. California's strict indoor air quality rules boost adoption of low-VOC finishes and FSC-certified materials. Rapidly evolving smart-home standards shorten product replacement cycles, benefiting brands offering firmware updates and modular components.

The Northeast and Midwest, while contributing smaller shares, remain vital due to legacy wealth and design institutions. Cities like New York, Boston, and Washington, D.C., prefer European craftsmanship and classic designs. Chicago and Minneapolis serve as Midwestern hubs where affluent consumers support specialty retailers and cabinetmakers despite manufacturing challenges. Aging housing stock in both regions sustains demand for remodeling, particularly for built-in storage and custom millwork. Slower population growth and high office vacancies limit expansion, requiring targeted strategies to address fragmented distribution and ensure premium service.

Competitive Landscape

The luxury furniture market in the United States is moderately concentrated, with multibrand groups, heritage brands, and digitally native companies addressing overlapping customer preferences. Established players utilize vertically integrated supply chains to ensure raw material availability and manage lead times effectively. They invest in proprietary design studios to safeguard intellectual property and maintain a competitive edge in the market. Key strategies include expanding into high-growth Sunbelt metropolitan areas and scaling augmented reality (AR) visualization platforms for enhanced customer engagement. Companies are also acquiring internet-first brands targeting younger, high-income demographics to diversify their customer base. Additionally, wellness-focused collections featuring posture-sensing technology and volatile organic compound (VOC)-free finishes address health, sustainability, and technology trends.

Disruptors are gaining market share by adopting transparent pricing, fast drop-shipping, and influencer-driven marketing that bypasses traditional wholesale channels. Many of these disruptors operate asset-light models, outsourcing production to specialized workshops while focusing on digital infrastructure and community engagement. Competitive differentiation increasingly relies on data analytics, with leaders integrating customer relationship management (CRM) systems and artificial intelligence (AI)-driven recommendation tools. These tools accelerate design cycles and enhance cross-selling opportunities, providing a significant advantage in the competitive landscape. By leveraging these strategies, disruptors challenge traditional players and reshape the dynamics of the luxury furniture market. Their innovative approaches continue to attract younger, tech-savvy consumers seeking personalized and efficient solutions.

Compliance with Business and Institutional Furniture Manufacturers Association (BIFMA) sustainability standards, Leadership in Energy and Environmental Design (LEED) contribution credits, and circular economy benchmarks influences contract awards. These factors raise entry barriers and strengthen the competitive advantage of large-scale operators in the United States luxury furniture market. Major players benefit from adhering to these standards, which align with growing consumer demand for sustainable and eco-friendly products. By meeting these benchmarks, companies secure contracts and establish themselves as leaders in the market. The focus on sustainability also enhances brand reputation and fosters long-term customer loyalty. As the market evolves, adherence to these standards will remain critical for maintaining a competitive edge.

United States Luxury Furniture Industry Leaders

RH (Restoration Hardware)

Williams-Sonoma Inc. (Pottery Barn, West Elm)

MillerKnoll (Herman Miller, Knoll, Design Within Reach)

Steelcase Inc.

Haworth Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: IKEA announced two new Arizona locations - a Scottsdale Plan & Order point and a 75,000-square-foot small-format Phoenix store opening in 2026 - to test hybrid selling that bridges online design sessions with on-site sample validation. Management highlighted Phoenix’s millennial migration as a catalyst and confirmed the concept will carry select luxury-adjacent collaborations such as the Marimekko-inspired textile line, signalling IKEA’s intent to nibble at affordable-luxury segments previously unchallenged.

- July 2024: Herman Miller unveiled a bamboo-fiber upholstery option for the iconic Eames Lounge Chair and Ottoman, claiming a 35% cut in material carbon footprint while preserving tensile strength and colorfastness. The company’s material scientists spent three years perfecting a proprietary resin blend that prevents fiber fray during long-term seating compression. Early field feedback notes a subtly softer hand feel that appeals to buyers seeking both luxury and ecological responsibility.

- May 2024: HNI Corporation disclosed the closure of its Hickory, North Carolina, facility, impacting 200 employees, as part of a broader initiative to reduce capacity amid soft commercial demand. The company will redirect production to high-automation plants in Iowa, generating an expected USD 35 million in annual savings that will fund residential product innovation. Local economic-development agencies have begun job-retraining programs for displaced skilled artisans, illustrating ripple effects of restructuring within the luxury furniture market.

United States Luxury Furniture Market Report Scope

The United States luxury furniture market is examined in this study through a comprehensive lens that captures its structural dynamics, evolving consumer preferences, and the macroeconomic forces shaping demand across residential, commercial, and institutional environments. The scope covers the full value chain - from raw materials and design innovation to manufacturing, distribution, and end‑use adoption - while assessing how trends such as quiet luxury, smart‑home integration, ESG‑aligned interiors, and the rise of UHNW households are redefining premium furniture consumption. The analysis spans all major product categories, materials, and distribution channels, offering a segmented view of market performance and growth potential across the Northeast, Midwest, South, and West regions of the United States.

The study also evaluates competitive intensity, strategic movements of leading brands, and the influence of digital transformation, including AR‑enabled shopping and luxury e‑commerce expansion. It incorporates market drivers, restraints, and emerging opportunities - such as wellness‑centric ergonomic design and the surge in luxury outdoor living - to provide a forward‑looking perspective. By integrating market sizing, forecasts, trend analysis, and detailed company profiles, the report equips manufacturers, retailers, investors, and stakeholders with actionable insights to navigate the evolving landscape of the United States luxury furniture market. The Report Offers Market Size and Forecasts for the United States Luxury Furniture Market are Provided in Terms of Value (USD) for all the Above Segments.

By Application

| Luxury Home Furniture | Chairs and Sofas |

| Tables (Side, Coffee, Dressing, etc.) | |

| Beds | |

| Wardrobes | |

| Dining Tables / Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture (Bathroom, Outdoor, etc.) | |

| Luxury Office Furniture | Chairs |

| Tables | |

| Storage Cabinets | |

| Desks, Sofas and Other Soft Seating | |

| Other Office Furniture | |

| Luxury Hospitality Furniture | |

| Other Applications (Educational Furniture, Healthcare Furniture, Retail Malls, Government Offices, etc.) |

By Material

| Wood |

| Metal |

| Glass |

| Leather |

| Plastic and Other Synthetics |

| Sustainable / Green Materials |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online Flagship Store | |

| Other Distribution Channels | |

| B2B / Project |

By Geography

| Northeast |

| Midwest |

| South |

| West |

| By Application | Luxury Home Furniture | Chairs and Sofas |

| Tables (Side, Coffee, Dressing, etc.) | ||

| Beds | ||

| Wardrobes | ||

| Dining Tables / Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture (Bathroom, Outdoor, etc.) | ||

| Luxury Office Furniture | Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks, Sofas and Other Soft Seating | ||

| Other Office Furniture | ||

| Luxury Hospitality Furniture | ||

| Other Applications (Educational Furniture, Healthcare Furniture, Retail Malls, Government Offices, etc.) | ||

| By Material | Wood | |

| Metal | ||

| Glass | ||

| Leather | ||

| Plastic and Other Synthetics | ||

| Sustainable / Green Materials | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online Flagship Store | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Geography | Northeast | |

| Midwest | ||

| South | ||

| West | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the United States luxury furniture market?

The market was valued at USD 6.55 billion in 2026 and is forecast to reach USD 8.01 billion by 2031.

Which application segment generates the most revenue?

Luxury home furniture leads, contributing 56.38% of 2026 sales.

Which material category is growing the fastest?

Sustainable and green materials are expanding at an 9.82% CAGR through 2031.

Which sales channel is expected to gain the most ground?

Online flagship stores are projected to grow at a 13.39% CAGR as AR visualization tools boost digital conversion.

Which U.S. region shows the fastest market growth?

The West region is forecast to post an 8.98% CAGR through 2030, driven by technology-sector wealth and smart-home adoption.

How are brands responding to the rise of authenticated resale?

Many offer trade-in programs, limited-edition drops, and modular designs to maintain relevance and capture residual value.