| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 6.76 Billion |

| Market Size (2030) | USD 8.79 Billion |

| CAGR (2025 - 2030) | 5.40 % |

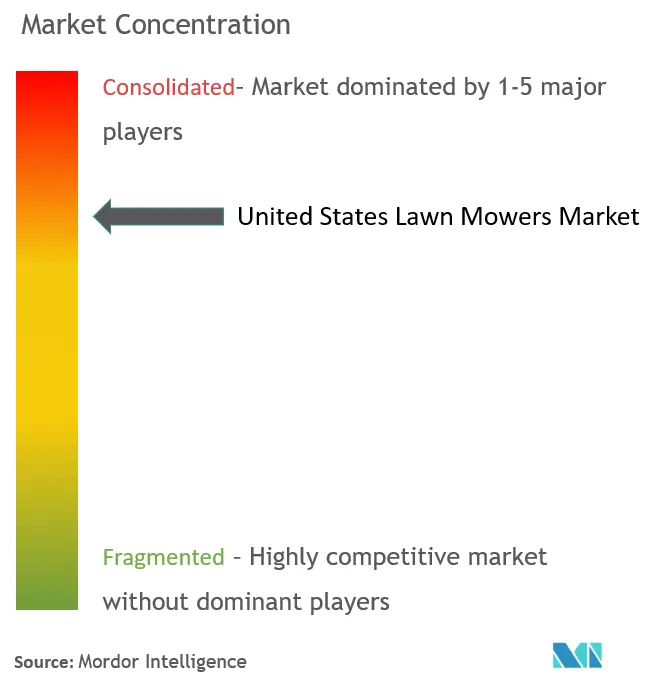

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

United States Lawn Mowers Market Analysis

The US Lawn Mowers Market size is estimated at USD 6.76 billion in 2025, and is expected to reach USD 8.79 billion by 2030, at a CAGR of 5.4% during the forecast period (2025-2030).

The US lawn mowers industry continues to evolve with changing consumer preferences and lifestyle patterns, particularly in suburban and urban areas. Consumer engagement in lawn care equipment and gardening activities remains robust, with participation rates reaching 80% in 2022, indicating strong market fundamentals. The average household spending on garden equipment and gardening activities has shown significant growth, reaching $616 in 2022, representing a $74 increase from the previous year. This trend reflects the growing importance Americans place on outdoor space maintenance and aesthetics, driving sustained demand for lawn care equipment.

The commercial segment of the lawn mowers market is experiencing substantial growth, driven by the expansion of recreational facilities and sports venues. The presence of approximately 16,000 golf courses in 2022, combined with a 12% year-over-year increase in golf participation to 119 million players, has created a strong demand for professional lawn mower maintenance equipment. This growth in recreational facilities has prompted manufacturers to develop more efficient and specialized mowing solutions tailored to commercial applications.

The industry is witnessing a significant shift towards sustainable and environmentally conscious solutions, with manufacturers increasingly focusing on developing eco-friendly alternatives. Major industry players are actively expanding their electric and battery-powered product lines, as evidenced by John Deere's 2023 launch of their first all-electric lawn mower, the Z370R Electric Ztrak. Similarly, Stanley Black & Decker's Craftsman brand introduced several new electric lawn mower products in 2023, demonstrating the industry's commitment to sustainability.

Infrastructure development and urban planning initiatives are creating new opportunities for market growth. The U.S. government's planned investment of USD 1,781.2 billion for commercial and residential construction activities, including parks, indicates strong potential for market expansion. This investment is complemented by innovations in lawn mower technology, such as AriensCo's 2023 launch of the IKON ONYX zero-turn lawn mower with a 52-inch deck, showcasing the industry's response to evolving market demands with advanced features and improved efficiency.

United States Lawn Mowers Market Trends

Rising Demand for Landscaping Maintenance

The demand for landscaping maintenance services has seen significant growth, driven by increasing consumer spending on lawn and garden activities. According to the National Gardening Survey 2023, household spending on lawn and gardening activities reached an average of $616 in 2022, representing a substantial increase of $74 from 2021. This rise in spending reflects the growing importance Americans place on maintaining their outdoor spaces, with participation in lawn and gardening activities remaining exceptionally high at 80% of households. The presence of extensive recreational facilities further drives the need for professional landscaping maintenance, with the United States hosting approximately 16,000 golf courses as of 2022.

The commercial landscaping sector has experienced substantial growth due to increasing demand from various segments, including suburban lawns, golf courses, sports fields, and public parks. This is evidenced by the rising popularity of golf-related activities, with over one-third of the US population aged 5 and above engaging in golf-related activities, whether playing on courses, following the sport through media, or participating in off-course activities. The National Golf Foundation reported that golf participation reached 119 million people in 2022, marking a 12% increase from the previous year. This surge in recreational facility usage has created a consistent demand for professional-grade landscaping equipment and lawn maintenance equipment across the country.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Adoption of Green Spaces and Green Roofs

The adoption of green spaces and green roofs has gained significant momentum across the United States, driven by environmental sustainability initiatives and urban planning requirements. Cities are increasingly implementing mandatory green roof policies, with San Francisco leading the way by requiring 15-30% of roof space in new construction projects to incorporate green roofs. These initiatives are supported by government funding, as demonstrated by the National Park Service's distribution of $192 million to local communities through the Outdoor Recreation Legacy Partnership (ORLP) grant program in 2022, which enables urban communities to create new outdoor recreation spaces and reinvigorate existing parks.

State and local governments are actively promoting the expansion of green spaces through various initiatives and funding programs. For instance, in 2022, California's local and state leaders granted nearly $15 million specifically for the expansion of outdoor facilities. The Northeast and Western regions of the country have emerged as leaders in green space implementation, with cities like Washington DC maintaining substantial green roof areas exceeding 245,000 square meters. These green spaces serve multiple environmental benefits, including improving air and water quality, reducing heat build-up, mitigating the heat island effect, and decreasing soil runoff, while also providing aesthetic benefits that enhance urban living environments.

Technological Advancements Drive Market Growth

The lawn maintenance industry has witnessed significant technological evolution with the integration of smart monitoring systems, artificial intelligence (AI), and machine learning capabilities into modern lawn care equipment. Major manufacturers are investing heavily in research and development to enhance product features, incorporating advanced technologies such as laser vision, lawn mapping, smart navigation, and self-emptying capabilities. For example, in 2022, The Toro Company introduced an innovative robotic lawn mower that utilizes cameras instead of LiDAR for its positioning system, eliminating the need for periphery wire while improving obstacle detection capabilities.

Recent product launches demonstrate the industry's commitment to technological innovation. In May 2023, AriensCo launched the IKON ONYX, a sophisticated zero-turn lawn mower featuring a 52-inch deck equipped with a 23-horsepower Kawasaki FR691V engine, showcasing the integration of advanced engineering in modern lawn maintenance equipment. Additionally, manufacturers are focusing on developing smart features that enhance user experience and operational efficiency. These innovations include automated height adjustment systems, smart monitoring capabilities that adapt to cutting conditions, and mobile app integration that allows users to control and schedule mowing operations remotely, representing a significant advancement in turf maintenance equipment technology.

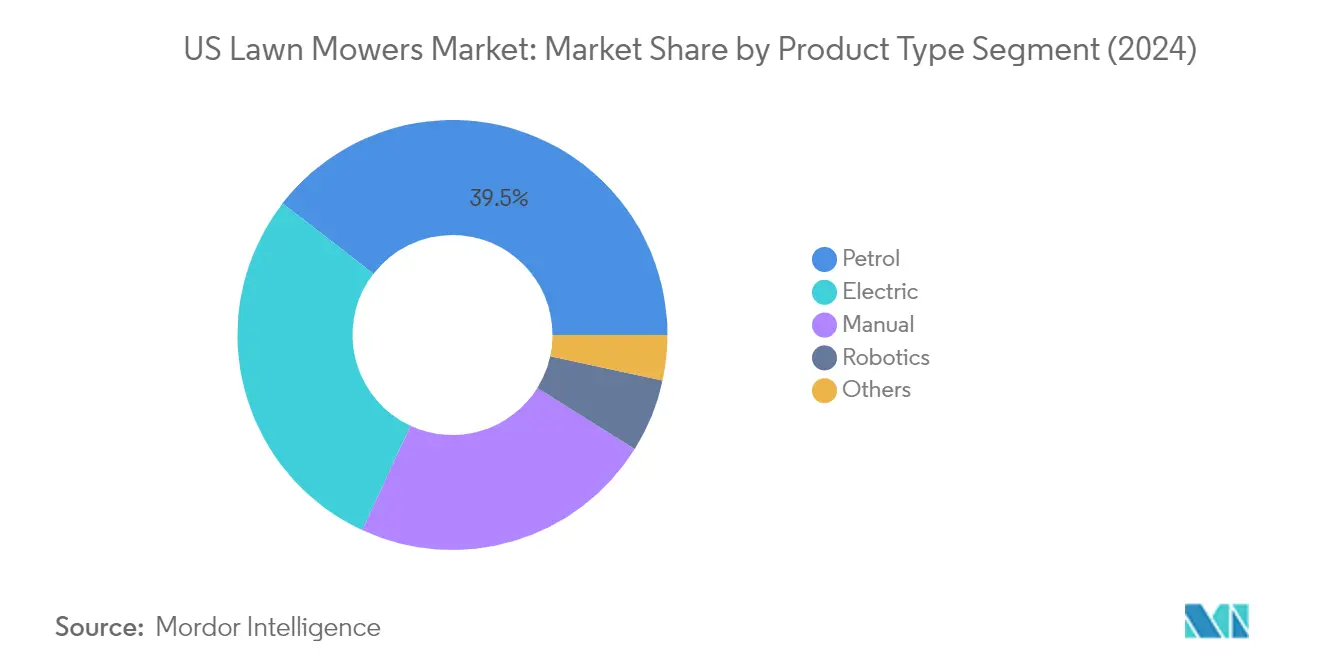

Segment Analysis: Product Type

Petrol Segment in US Lawn Mowers Market

The gas lawn mower segment continues to dominate the US lawn mower market, holding approximately 40% market share in 2024. Petrol lawn mowers remain the preferred choice for both residential and commercial applications due to their superior power output and high-grade cutting-edge performance. These mowers are particularly well-suited for large lawn areas, featuring both push-powered and self-propelled variants that offer exceptional mobility and coverage. The segment's strength is further reinforced by the durability of these machines, which are built using professional-grade components, including corrosion-resistant chassis and aluminum construction, resulting in lower maintenance and servicing costs. The robust nature of petrol mowers makes them especially popular among professional landscaping services and property maintenance companies that require reliable equipment for continuous heavy-duty operation.

Robotic Segment in US Lawn Mowers Market

The robotic lawn mower segment is experiencing remarkable growth, projected to expand at approximately 7% during 2024-2029, emerging as the fastest-growing category in the market. This impressive growth is driven by rapid technological advancements in artificial intelligence, the Internet of Things (IoT), and machine learning capabilities. Modern robotic mowers are incorporating sophisticated features such as GPS navigation, smart scheduling, rain sensors, and automated docking systems, making them increasingly attractive to tech-savvy consumers. The segment's growth is further accelerated by the rising demand for automated lawn maintenance solutions that offer convenience and time savings. Manufacturers are continuously innovating with features like lawn mapping, barrier recognition systems, and lawn memory technologies, making these devices more efficient and user-friendly.

Remaining Segments in Product Type

The electric lawn mower, manual, and other segments each play significant roles in shaping the US lawn mower market landscape. Electric lawn mowers are gaining popularity due to their environmental friendliness and lower operational costs, particularly in residential areas where noise reduction is a priority. Manual mowers continue to serve an important niche in the market, especially for small lawns and environmentally conscious consumers who prefer non-motorized options. The 'others' category, which includes alternative fuel-powered mowers such as battery-operated and hybrid models, represents emerging technologies that are gradually gaining acceptance in the market. These segments collectively offer diverse options to meet varying consumer preferences and specific lawn maintenance requirements across different property sizes and types.

Segment Analysis: By End User

Commercial/Government Segment in US Lawn Mowers Market

The commercial lawn mower segment dominates the US lawn mower market, holding approximately 60% market share in 2024. This significant market presence is driven by the extensive demand from golf courses, sports fields, schools, and public parks across the country. According to the US Department of Energy, turf grass represents the nation's largest irrigated crop, covering more than 40 million acres, which necessitates consistent maintenance using commercial lawn mowers. The segment's growth is further supported by government initiatives focusing on expanding outdoor spaces, particularly evident in states like California, where substantial investments are being made in public park improvements. The commercial sector's dominance is also reinforced by the presence of approximately 16,000 golf courses in the United States, creating a constant demand for professional-grade lawn mowing equipment. Major manufacturers are responding to this demand by introducing innovative commercial-grade products with advanced features, enhancing operational efficiency and productivity for professional users.

Residential Segment in US Lawn Mowers Market

The residential lawn mower segment is projected to experience the highest growth rate of approximately 5.5% during the forecast period 2024-2029. This accelerated growth is primarily attributed to the increasing focus on backyard beautification and rising consumer spending on lawn and garden activities. The segment's expansion is supported by the growing adoption of smart and automated lawn mowing solutions among homeowners, particularly in suburban areas. The trend is further amplified by the rising popularity of electric and robotic mowers in residential applications, driven by their convenience and environmental benefits. According to recent industry data, participation in lawn and gardening activities remains exceptionally high, with 80% of households actively engaged in these activities. The segment's growth is also bolstered by manufacturers' focus on developing user-friendly, technologically advanced products specifically designed for residential users, including features like smart monitoring and automated operation capabilities.

United States Lawn Mowers Industry Overview

Top Companies in US Lawn Mowers Market

The US lawn mower market is characterized by the strong presence of established players like Deere & Company, Stanley Black & Decker, The Toro Company, and Kubota Corporation leading the competitive landscape. Companies are heavily investing in product innovation, particularly in robotic and electric lawn mowers, with advanced features like AI integration, smart monitoring, and machine learning capabilities becoming increasingly prevalent. Strategic partnerships have emerged as a key trend, with companies collaborating with retailers, technology providers, and distribution networks to enhance market reach. Operational agility is demonstrated through the development of comprehensive product portfolios spanning residential and commercial lawn mower segments, while manufacturing facilities are being optimized for lean production. Market expansion strategies have focused on acquisitions of specialized manufacturers, particularly those with a strong regional presence or innovative technology capabilities, allowing larger players to quickly enter new market segments and geographical areas.

Consolidated Market with Strong Brand Dominance

The US lawn mower market exhibits a consolidated structure dominated by large multinational conglomerates with diverse product portfolios and established brand recognition. These major players leverage their extensive manufacturing capabilities, robust distribution networks, and significant research and development resources to maintain their market positions. The presence of both global equipment manufacturers and specialized lawn care equipment producers creates a dynamic competitive environment, with global players offering comprehensive solutions while specialized manufacturers focus on niche market segments and innovative technologies.

Merger and acquisition activities have been instrumental in shaping the market landscape, with larger companies actively acquiring smaller, innovative manufacturers to expand their technological capabilities and market reach. This consolidation trend has particularly focused on companies with a strong regional presence or specialized product offerings, such as robotic mower manufacturers or those with established dealer networks in specific geographical areas. The market also sees strategic partnerships between manufacturers and retailers, creating exclusive distribution channels and strengthening market presence.

Innovation and Distribution Drive Market Success

Success in the US lawn mower market increasingly depends on companies' ability to innovate while maintaining strong distribution networks and after-sales service capabilities. Manufacturers must focus on developing environmentally friendly products, particularly battery-powered and autonomous solutions, while maintaining competitive pricing strategies. The ability to offer comprehensive product lines that cater to both residential and commercial segments, combined with strong dealer networks and efficient supply chain management, has become crucial for maintaining market share. Companies must also invest in digital capabilities, including e-commerce platforms and connected product features, to meet evolving consumer preferences.

For new entrants and smaller players, success lies in identifying and exploiting niche market segments while building strong relationships with dealers and distributors. The focus should be on developing specialized products with unique features or targeting specific geographic regions where larger players have less presence. Companies must also consider potential regulatory changes regarding emissions and noise levels, which could impact product development strategies. The risk of substitution remains relatively low due to the essential nature of garden equipment, but companies must continue to innovate to maintain their competitive edge and address changing consumer preferences for sustainable and technologically advanced solutions.

United States Lawn Mowers Market Leaders

-

Deere & Co.

-

Stanley Black & Decker

-

The Toro Company

-

Kubota Corporation

-

American Honda Motor Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

United States Lawn Mowers Market News

- September 2023: John Deere announced a new strategic partnership with EGO and parent company Chervon, a leading global provider to the Outdoor Power Equipment (OPE) and Power Tool industries. The agreement allows the brands to provide homeowners with EGO battery-powered lawn care solutions through John Deere dealers.

- May 2023: AriensCo’s Ariens brand launched the IKON ONYX, a custom zero-turn lawnmower with a 52-inch deck.

- March 2022: AriensCo partnered with country music entertainer and Army veteran Craig Morgan to represent its Gravely commercial lawnmower brand and Ariens.

US Lawn Mowers Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Demand For Landscaping Maintenance

- 4.2.2 Adoption of Green Spaces and Green Roofs

-

4.3 Market Restraints

- 4.3.1 Shortage of Labor In Landscaping

- 4.3.2 High Maintenance Cost of Lawn Mowers

-

4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Product Type

- 5.1.1 Manual

- 5.1.2 Electric

- 5.1.3 Petrol

- 5.1.4 Robotics

- 5.1.5 Other Product Types

-

5.2 End User

- 5.2.1 Residential

- 5.2.2 Commercial/Government

6. COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

-

6.3 Company Profiles

- 6.3.1 Ariensco

- 6.3.2 Deere & Company

- 6.3.3 American Honda Motor Co. Inc.

- 6.3.4 Husqvarna Group

- 6.3.5 Kubota Corporation

- 6.3.6 Makita Corporation

- 6.3.7 Stanley Black & Decker

- 6.3.8 Yamabiko Corporation

- 6.3.9 The Toro Company

- 6.3.10 Stihl Group

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

United States Lawn Mowers Industry Segmentation

A lawn mower, also known as a grass cutter, is a machine used to cut grass in agriculture, gardening, landscaping, and horticulture. This machine has one or more revolving blades to cut the grass. The United States lawn mowers market is segmented by product type and end user. By product type, the market has been segmented into manual, electric, petrol, robotics, and other product types. By end user, the market has been bifurcated into residential and commercial/government. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Product Type | Manual |

| Electric | |

| Petrol | |

| Robotics | |

| Other Product Types | |

| End User | Residential |

| Commercial/Government |

Need A Different Region or Segment?

Customize Now

US Lawn Mowers Market Research FAQs

How big is the US Lawn Mowers Market?

The US Lawn Mowers Market size is expected to reach USD 6.76 billion in 2025 and grow at a CAGR of 5.40% to reach USD 8.79 billion by 2030.

What is the current US Lawn Mowers Market size?

In 2025, the US Lawn Mowers Market size is expected to reach USD 6.76 billion.

Who are the key players in US Lawn Mowers Market?

Deere & Co., Stanley Black & Decker, The Toro Company, Kubota Corporation and American Honda Motor Co. Inc. are the major companies operating in the US Lawn Mowers Market.

What years does this US Lawn Mowers Market cover, and what was the market size in 2024?

In 2024, the US Lawn Mowers Market size was estimated at USD 6.39 billion. The report covers the US Lawn Mowers Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the US Lawn Mowers Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

US Lawn Mowers Market Research

Mordor Intelligence provides a comprehensive analysis of the lawn mower industry. We leverage our extensive experience in tracking garden equipment and landscaping equipment trends. Our detailed report covers a wide range of products, including riding lawn mower and electric lawn mower technologies, as well as gas lawn mower and reel mower solutions. The analysis also includes robotic lawn mower innovations, cordless lawn mower developments, and emerging autonomous lawn mower technologies. This information is available in an easy-to-download report PDF format.

This strategic report offers invaluable insights for stakeholders in both the commercial lawn mower and residential lawn mower segments. It is useful for manufacturers, distributors, and end-users of professional lawn mower equipment. Our analysis covers push lawn mower systems and advanced grass cutter technologies. It examines the entire ecosystem of lawn care equipment and turf maintenance equipment. The report provides actionable intelligence on garden mower trends, grass mower innovations, and lawn maintenance equipment developments. This enables businesses to make informed decisions in this dynamic market landscape.