United States (US) Industrial Sensors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

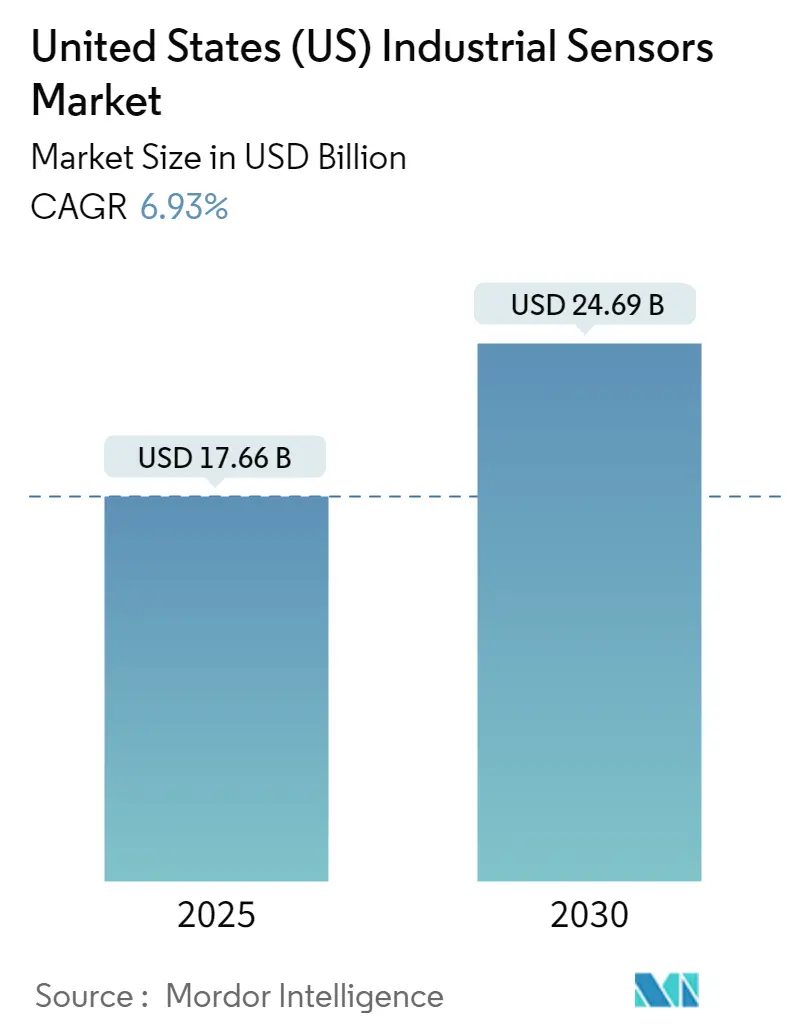

| Market Size (2025) | USD 17.66 Billion |

| Market Size (2030) | USD 24.69 Billion |

| Growth Rate (2025 - 2030) | 6.93% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States (US) Industrial Sensors Market Analysis by Mordor Intelligence

The United States Industrial Sensors Market size is estimated at USD 17.66 billion in 2025, and is expected to reach USD 24.69 billion by 2030, at a CAGR of 6.93% during the forecast period (2025-2030).

The US industrial sensors landscape is experiencing significant transformation driven by the broader push toward industrial automation sensors and digital transformation. The manufacturing sector is witnessing unprecedented changes as industries adopt more sophisticated and integrated industrial IoT sensors technologies to enhance operational efficiency and productivity. According to the American Chemistry Council, US chemical industry investment linked to domestic supplies of natural gas and natural gas liquids has topped USD 200 billion as of May 2022, indicating substantial infrastructure development requiring advanced sensing solutions. This investment surge has created increased demand for various types of manufacturing sensors across manufacturing facilities, particularly in process monitoring and control applications.

The energy sector has emerged as a crucial growth driver for industrial sensors, with significant investments in clean energy infrastructure. US investment in clean energy reached USD 141 billion in 2022, representing a substantial increase from previous years and creating new opportunities for sensor deployments in renewable energy installations. The automotive industry has also shown remarkable advancement in sensor adoption, with the US auto industry producing approximately 10.06 million motor vehicles in 2022 according to OICA, each requiring multiple sophisticated sensors for various applications including safety systems, emission controls, and performance monitoring.

The chemical and manufacturing industries continue to drive innovation in sensor technologies, particularly in harsh environment applications. The US chemical industry production index reached 95.5 in 2022, demonstrating recovery and growth in a sector that heavily relies on precise sensing and measurement capabilities. Manufacturing facilities are increasingly implementing advanced smart factory sensors networks to enable real-time monitoring, quality control, and process optimization, with particular emphasis on developing sensors that can withstand extreme conditions while maintaining accuracy and reliability.

Recent technological innovations have focused on developing more intelligent and integrated sensor solutions. In September 2023, Baker Hughes launched its latest hydrogen-rated pressure sensors, designed to offer longer-term stability and withstand harsh environments, particularly for applications in gas turbines and hydrogen filling stations. Similarly, in March 2023, ABB announced an investment of USD 20 million to increase production capacity at its North American headquarters and manufacturing facility in Michigan, demonstrating the growing demand for advanced sensor technologies. These developments highlight the industry's focus on creating more robust and versatile sensing solutions capable of meeting evolving industrial requirements.

United States (US) Industrial Sensors Market Trends and Insights

Growing Adoption of IoT Leading to Demand for Sensing Components

The increasing adoption of IoT in the United States can be attributed to factors like rapid digitalization, technological advancements, and government initiatives aimed at promoting digital transformation and Industry 4.0. With the high adoption rate of connected devices and sensors and the enabling of M2M communication, there has been an exponential increase in the data points generated in the manufacturing industry. According to the Global System for Mobile Communications Association, North America's total number of consumer and industrial Internet of Things (IoT) connections is forecast to grow to 5.4 billion by 2025, indicating the massive scale of IoT adoption.

The Industrial Internet of Things has enabled industries to rethink business models, generating actionable information and knowledge from IIoT devices. Companies are actively deploying industrial IoT sensors in IoT devices to boost their performance. For instance, in May 2023, iMatrix Systems launched a range of temperature and humidity sensors designed specifically for food storage, transport monitoring, pharmaceutical, and agriculture applications. The consistent and reliable performance of sensors has led assets in heavy industrial operations to drive critical daily metrics, with manufacturers constantly monitoring the uptime of assets along their production lines through IIoT integration.

Growing Emphasis on the Use of Predictive Maintenance and Remote Monitoring

The growing importance of predictive maintenance and remote monitoring in manufacturing facilities has been increasing competition among various end-users, driving market growth. Although the global automotive sector witnessed a recession in the past two years, the number of sensors utilized in the industry has increased, especially MEMS pressure sensors, which have seen significant adoption in the smart automotive sector. For instance, in June 2023, Embraer Services & Support launched a new version of its Aircraft Health Analysis and Diagnosis (AHAD) system, enabling airlines and customers to monitor their aircraft for potential maintenance issues before they become critical problems.

Remote monitoring services are gaining prominence as they offer several advantages, such as early assessment to improve equipment reliability and availability, prevention of unplanned shutdowns, easy monitoring of machines that are difficult to access, and reduced unexpected downtimes and failures. In March 2023, ProMinent launched Dulcolevel, an IIoT-compatible radar level sensor that provides continuous information on tank liquid levels, ensuring timely refills without procedure interruption and simplifying chemical inventory management. The integration of such advanced monitoring capabilities has become crucial for modern businesses implementing high-quality predictive maintenance programs, offering increased assurance and flexibility while optimizing operational efficiency.

Segment Analysis: By Connectivity

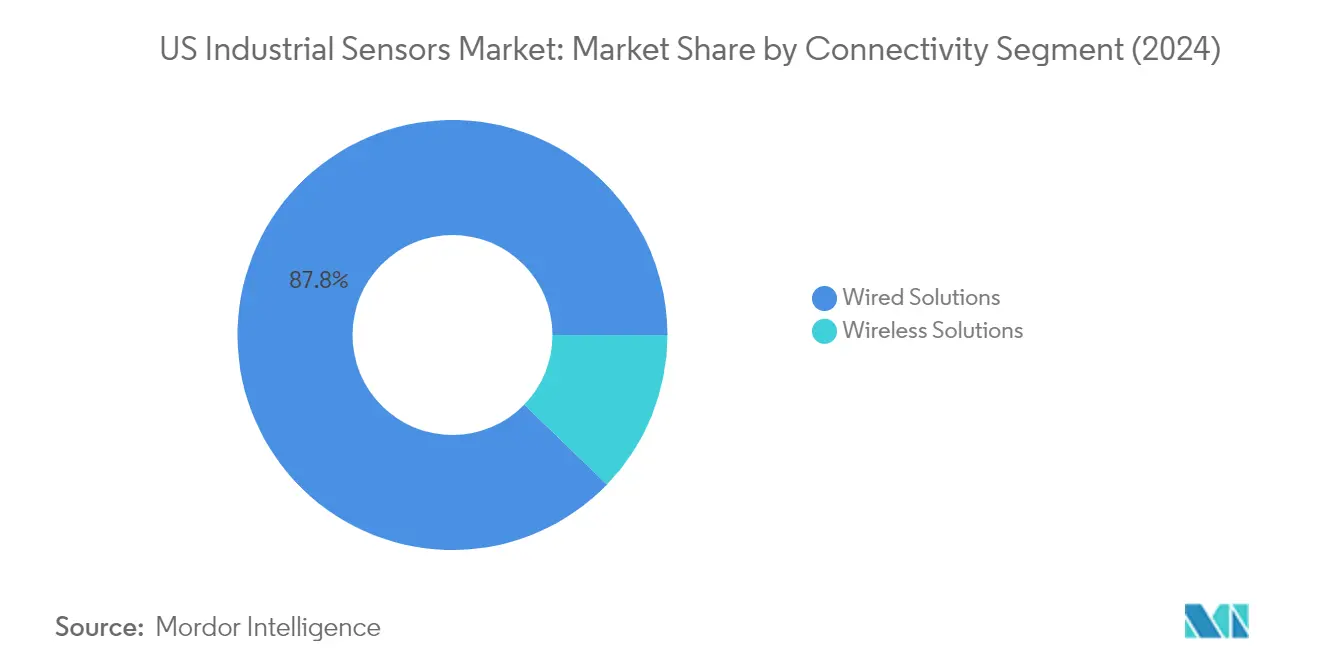

Wired Solutions Segment in US Industrial Sensors Market

The wired solutions segment continues to dominate the US industrial sensors market, holding approximately 88% market share in 2024. This significant market position is attributed to the segment's proven reliability and consistent data transmission capabilities in industrial environments. Wired sensor solutions offer stable and secure connections, reducing the risk of data interception or tampering, which is crucial for critical industrial applications. The availability of advanced data analytics tools has enabled more efficient and effective sensor data analysis, with these tools processing large volumes of data collected by wired industrial sensors to provide valuable insights for decision-making and process optimization. These sensors can also be connected to cloud platforms, allowing centralized data storage, analysis, and access, enabling real-time monitoring and remote management of industrial processes, improving efficiency and reducing downtime. The segment's strong performance is further supported by its widespread adoption across various industries, including manufacturing, power generation, and chemical processing, where reliable and precise measurements are essential for operational success.

Wireless Solutions Segment in US Industrial Sensors Market

The wireless solutions segment is emerging as the fastest-growing segment in the US industrial sensors market, with a projected growth rate of approximately 12% during the forecast period 2024-2029. This rapid growth is driven by the increasing demand for flexible and easily deployable sensor networks in industrial environments. Wireless sensors offer several advantages over traditional wired sensors, including faster installation time, lower costs, and minimal disruption to existing infrastructure. They can help improve operations in process plants by providing real-time data on various parameters without the need for extensive wiring. The segment's growth is further accelerated by the rising adoption of Industrial Internet of Things (IIoT) technologies, with customers showing increased interest in IoT gas detectors and other wireless sensing solutions. The continuous monitoring capabilities of wireless sensors, particularly in energy consumption tracking and asset condition monitoring, are making them increasingly attractive to industrial users looking to optimize their operations and reduce maintenance costs.

Segment Analysis: By Type

Pressure Sensors Segment in US Industrial Sensors Market

The industrial pressure sensors segment has established itself as the dominant force in the US industrial sensors market, commanding approximately 27% market share in 2024. These sensors have become increasingly crucial across various industries, particularly in the automotive, healthcare, and industrial automation sectors. The segment's prominence can be attributed to the growing adoption of MEMS industrial pressure sensors in smart automotive applications and the increasing demand for pressure monitoring in industrial processes. The development of advanced pressure sensor technologies, including piezoresistive and capacitive sensors, has further strengthened their position in the market. Major manufacturers are focusing on developing innovative solutions, as evidenced by Baker Hughes' launch of hydrogen-rated pressure sensors in 2023, designed to offer enhanced stability in harsh environments. The segment's growth is also driven by the expanding applications in respiratory monitoring, tire pressure monitoring systems, and industrial automation.

Remaining Segments in US Industrial Sensors Market by Type

The US industrial sensors market encompasses several other significant segments, including industrial flow sensors, industrial temperature sensors, industrial level sensors, industrial gas sensors, and other specialized sensors. Industrial flow sensors play a vital role in monitoring and controlling fluid dynamics across various industries, particularly in the oil and gas, chemical processing, and water management sectors. Industrial temperature sensors have become indispensable in maintaining optimal operating conditions and ensuring safety across manufacturing processes. Industrial level sensors are crucial for inventory management and process control in industries ranging from petrochemicals to food and beverage. Industrial gas sensors, while representing a smaller market share, are essential for safety monitoring and environmental compliance. The "other sensors" category, including industrial proximity sensors, industrial photoelectric sensors, and vibration sensors, continues to evolve with the advancement of Industry 4.0 and IoT technologies, offering innovative solutions for predictive maintenance and automation applications.

Competitive Landscape

Top Companies in US Industrial Sensors Market

The US industrial sensors market features prominent players like Texas Instruments, TE Connectivity, Honeywell International, Rockwell Automation, and ABB, among others, driving innovation and competition. Companies are increasingly focusing on developing smart industrial sensor solutions with IoT capabilities and enhanced precision for Industry 4.0 applications, while also expanding their product portfolios through strategic R&D investments. Market leaders are strengthening their positions through continuous product launches incorporating advanced technologies like MEMS and wireless connectivity features. The competitive landscape is characterized by companies pursuing strategic partnerships and collaborations to enhance their technological capabilities and market reach. Operational agility is being achieved through investments in modern manufacturing facilities and digital transformation initiatives, while geographic expansion is primarily driven by new facility establishments and strategic acquisitions to serve growing industrial demand centers.

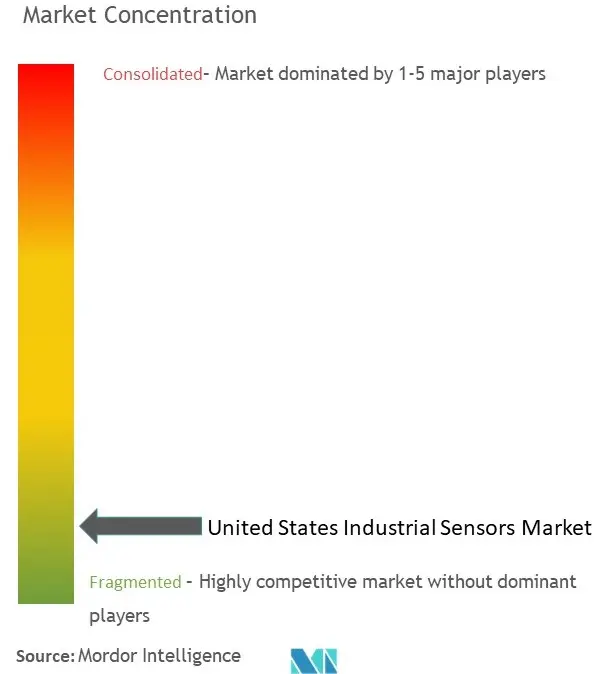

Consolidated Market Led By Global Conglomerates

The US industrial automation sensor market structure exhibits a relatively consolidated nature dominated by large multinational conglomerates with diverse product portfolios and extensive manufacturing capabilities. These established players leverage their strong R&D capabilities, broad distribution networks, and long-standing customer relationships to maintain their market positions. The market is characterized by the presence of both diversified industrial technology companies that offer sensors as part of their broader automation solutions, as well as specialized sensor manufacturers focusing on specific technologies or applications.

The competitive dynamics are shaped by ongoing merger and acquisition activities as larger players seek to acquire innovative technologies and expand their market presence. Companies are increasingly pursuing vertical integration strategies to strengthen their supply chain control and manufacturing capabilities. Regional players and specialized sensor manufacturers are finding opportunities through a focus on niche applications and custom solutions, while global players continue to expand their presence through strategic partnerships and local manufacturing investments to better serve the US market.

Innovation and Customer Focus Drive Success

Success in the US factory automation sensor market increasingly depends on companies' ability to innovate and adapt to rapidly evolving technological requirements while maintaining strong customer relationships. Market leaders are focusing on developing comprehensive sensor solutions that integrate seamlessly with industrial IoT platforms and provide enhanced data analytics capabilities. Companies are investing in research and development to create more precise, reliable, and energy-efficient sensors while also expanding their service offerings to include predictive maintenance and remote monitoring capabilities.

Future market success will require companies to address growing end-user demands for customization and application-specific solutions while maintaining cost competitiveness. The ability to navigate regulatory requirements, particularly in sensitive industries like automotive and aerospace, will become increasingly important. Companies must also focus on building robust distribution networks and technical support capabilities to serve diverse industrial applications effectively. The development of sustainable and environmentally friendly sensor solutions, along with the ability to provide comprehensive after-sales support and training, will become crucial differentiating factors in maintaining competitive advantage.

United States (US) Industrial Sensors Industry Leaders

TE Connectivity Ltd

Omega Engineering Inc.

Honeywell International Inc.

Rockwell Automation Inc.

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2023 - KROHNE, Inc. announced to showcase a wide range of its industry-leading water and wastewater products, including the latest version of the OPTISONIC 6300 clamp-on ultrasonic flowmeter at WEFTEC 2023. Likewise, in January 2023, the company announced to exhibit products for food and beverage production at the Food Processing Expo 2023, which includes the OPTISONIC 6300P ultrasonic clamp-on flowmeter, the WATERFLUX 3070 electromagnetic water meter, and the OPTIFLUX 2000 electromagnetic flow sensor.

- January 2023 - Bosch Sensortec has introduced a range of new sensors at CES 2023, including an AI-enabled sensor and a next-generation magnetometer. The new BMP585 barometric pressure sensors enable a range of altitude tracking in harsh conditions, such as for wearables for swimming. The new sensor claims ultra-low power consumption for extended battery life, high accuracy, and low noise.

United States (US) Industrial Sensors Market Report Scope

Industrial sensors are devices that may sense changes in the environment and provide an output signal with respect to input or change in the environment. These sensors can sense physical input, such as light, heat, motion, moisture, pressure, or any other entity, and respond by producing an output on display or transmitting the information in electronic form for further processing.

The scope of the study includes the different types of sensors used in Industrial applications, with the prominent industries in the scope being chemicals and petrochemicals, oil and gas, water and wastewater, food and beverage, power, aerospace and military, life sciences, and other end-user industries in the United States. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period. The study further analyzes the overall impact of macroeconomic trends on the ecosystem.

The United States Industrial Sensors Market is Segmented by connectivity (wired solutions, wireless solutions), by type (flow sensors, temperature sensors, level sensors, pressure sensors, gas sensors). The report offers market forecasts and size in value (USD) for all the above segments.

| Wired Solutions |

| Wireless Solutions |

| Flow Sensors | Market Overview |

| End-user Industry | |

| Temperature Sensors | Market Overview |

| End-user Industry | |

| Level Sensors | Market Overview |

| End-user Industry | |

| Pressure Sensors | Market Overview |

| End-user Industry | |

| Gas Sensors | Market Overview |

| End-user Industry | |

| Other Sensors |

| By Connectivity | Wired Solutions | |

| Wireless Solutions | ||

| By Type | Flow Sensors | Market Overview |

| End-user Industry | ||

| Temperature Sensors | Market Overview | |

| End-user Industry | ||

| Level Sensors | Market Overview | |

| End-user Industry | ||

| Pressure Sensors | Market Overview | |

| End-user Industry | ||

| Gas Sensors | Market Overview | |

| End-user Industry | ||

| Other Sensors | ||

Key Questions Answered in the Report

How big is the US Industrial Sensors Market?

The US Industrial Sensors Market size is expected to reach USD 17.66 billion in 2025 and grow at a CAGR of 6.93% to reach USD 24.69 billion by 2030.

What is the current US Industrial Sensors Market size?

In 2025, the US Industrial Sensors Market size is expected to reach USD 17.66 billion.

Who are the key players in US Industrial Sensors Market?

TE Connectivity Ltd, Omega Engineering Inc., Honeywell International Inc., Rockwell Automation Inc. and Siemens AG are the major companies operating in the US Industrial Sensors Market.

What years does this US Industrial Sensors Market cover, and what was the market size in 2024?

In 2024, the US Industrial Sensors Market size was estimated at USD 16.44 billion. The report covers the US Industrial Sensors Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the US Industrial Sensors Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.