Market Size of US HVAC Field Device Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

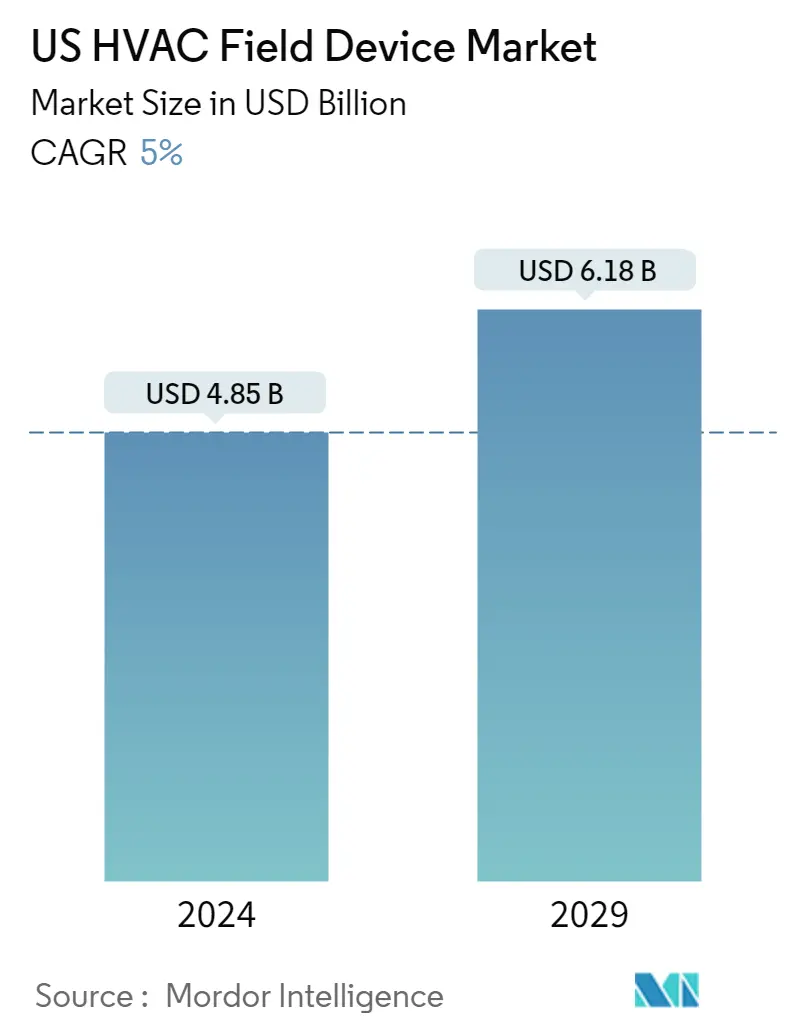

| Market Size (2024) | USD 4.85 Billion |

| Market Size (2029) | USD 6.18 Billion |

| CAGR (2024 - 2029) | 5.00 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

US HVAC Field Device Market Analysis

The US HVAC Field Device Market size is estimated at USD 4.85 billion in 2024, and is expected to reach USD 6.18 billion by 2029, growing at a CAGR of 5% during the forecast period (2024-2029).

The increasing construction activity, availability of high-efficiency systems, and extreme climatic conditions favor the system installation of HVAC equipment across the facilities in the country, thereby driving the growth of the HVAC field devices market. Additionally, the presence of prominent manufacturers, such as Siemens, Johnson Controls, and others, is complementing the North American market's growth in the future.

- HVAC in a commercial building usually consumes more energy than any other activity in the building. Energy standards and building codes have significantly steered the design of energy-efficient buildings over the past decade. For instance, the US Green Building Council's (USGBC) Leadership in Energy and Environmental Design Green Building Rating System has raised awareness of the need for building designs that use energy efficiently.

- As such, several states in the country have mandated the use of the LEED rating system for government buildings. Such initiatives indicate the importance of energy conservation in buildings. Since HVAC equipment is among the primary energy users in buildings, efficient air-handling units and air distribution systems can help save significant amounts of energy, reduce operating costs, and comply with widely used energy standards and building codes.

- As awareness and implementation of smart cities develop, consumers are expected to increase their spending on connected home appliances like thermostats and controllers. For instance, according to the Consumer Technology Association (CTA), connected home product revenue is increasing in the United States from 2018 to 2022. In 2020, connected home products in the United States were estimated to generate a revenue of USD 5.1 billion and reach USD 5.94 billion. This is making the vendors of HVAC solutions offer or enhance their product portfolios with the latest updates related to multi-device connectivity. Such developments are anticipated to offer lucrative opportunities for the HVAC field device market players in the United States.

- Heating, ventilation, and air conditioning (HVAC) are essential in the design of medium- to large industrial buildings and in regulating conditions within the manufacturing facility with respect to temperature and humidity by deploying an HVAC system for different manufacturing units. HVAC equipment is essential in the manufacturing sector to ensure the comfort and safety of workers as well as the proper functioning of manufacturing equipment.

- For instance, the food and beverage (F&B) industry, which comes under FMCG, requires extensive use of a hygienic, dust-free, pollutant-free environment and effective cooling to ensure optimal processing of highly perishable products with no damage to the final product. With the expanding manufacturing sector, various industrial infrastructures for producing highly vulnerable industries such as chemicals, pharmaceuticals, food, and beverages are also increasing.

- As a result, the market for refrigeration equipment is expanding rapidly due to factors including rising frozen food consumption and a growing population. According to the American Frozen Food Institute (AFFI), frozen food sales were expected to increase by 8.6% to reach USD 72.2 billion in 2022. The rising demand from the industrial sector in the United States is likely to boost the growth of the studied market.

- On the flip side, high energy consumption is expected to restrain the United States HVAC field devices market growth during the forecast period. Major entities in the commercial segment, such as retail complexes, hostels, entertainment centers, and others, typically rely on centralized HVAC systems for space conditioning.

- As per the International Energy Agency (IEA) and the US Department of Energy, around 25-35% of electricity consumption is due to HVAC systems. According to the same source, a large part (20%-60%) of this energy consumption is contributed by parasitic energy use (energy used to power fans and pumps used for transferring heating and cooling). Thus, centralized HVAC systems have burdened energy bills despite being more efficient (in terms of energy units' consumption per unit area of space conditioned) than unitary systems. However, rapid technological advancements are anticipated to offer a significant boost to the growth of the studied market.

- The pandemic significantly influenced the HVAC industry, as demand for the systems observed a significant drop during the initial months, owing to lockdown restrictions and businesses refraining from investing in new equipment. Due to the pandemic, many construction projects were halted across the world. The reduction in construction activities across the commercial, residential, and industrial sectors temporarily dampened the demand for HVAC systems, including air handling units. Moreover, amid the pandemic, labor shortages across HVAC manufacturing sectors delayed the production of HVAC equipment.

- However, the pandemic highlighted the importance of ventilation, which was a prominent factor driving the demand for HVAC equipment. The American Society of Heating, Refrigerating, and Air-Conditioning Engineers recommended strategies to mitigate COVID-19 transmission, eventually boosting demand across the United States. Hence, the future growth trajectory is projected to be firm.

US HVAC Field Device Industry Segmentation

A field device controls local operations like opening and closing valves and breakers, collecting data from sensor systems, and monitoring the local environment for alarm conditions.

The United States HVAC field device market is segmented by type (control valve, balancing valve, PICV, damper HVAC, damper actuator HVAC), sensors (environmental sensors, multisensors, air quality sensors, occupancy and lighting sensors), and end-user industry (commercial, residential, and industrial). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type | |

| Control Valve | |

| Balancing Valve | |

| PICV | |

| Damper HVAC | |

| Damper Actuator HVAC |

| By Sensors | |

| Environmental Sensors | |

| Multi Sensors | |

| Air Quality Sensors | |

| Occupancy & Lighting | |

| Other Sensors |

| By End-user Industry | |

| Commercial | |

| Residential | |

| Industrial |

US HVAC Field Device Market Size Summary

The United States HVAC field device market is poised for significant growth, driven by increasing construction activities, the availability of high-efficiency systems, and the need to address extreme climatic conditions. The market is supported by the presence of major manufacturers like Siemens and Johnson Controls, which are enhancing the market's expansion. The demand for energy-efficient HVAC systems is further propelled by stringent energy standards and building codes, such as those set by the US Green Building Council. These regulations encourage the adoption of energy-efficient designs, which are crucial for reducing energy consumption and operational costs in commercial buildings. The rise of smart cities and connected home appliances also contributes to the market's growth, as consumers increasingly invest in advanced HVAC solutions that offer multi-device connectivity and improved energy management.

The HVAC field device market in the United States is also influenced by the expanding manufacturing sector, which requires efficient HVAC systems to maintain optimal working conditions and ensure the safety and comfort of workers. Industries such as food and beverage, chemicals, and pharmaceuticals drive the demand for refrigeration and HVAC equipment. However, high energy consumption remains a challenge, with centralized HVAC systems contributing significantly to electricity usage. Despite this, rapid technological advancements and the shift towards electrification and decarbonization present opportunities for market growth. The market is moderately consolidated, with key players engaging in strategic partnerships and innovations to enhance their product offerings and market presence. Regulatory measures and consumer preferences for energy-efficient solutions are expected to further boost the demand for HVAC field devices in the coming years.

US HVAC Field Device Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Technology Snapshot

-

1.4 Value Chain Analysis

-

1.5 Assessment of Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Type

-

2.1.1 Control Valve

-

2.1.2 Balancing Valve

-

2.1.3 PICV

-

2.1.4 Damper HVAC

-

2.1.5 Damper Actuator HVAC

-

-

2.2 By Sensors

-

2.2.1 Environmental Sensors

-

2.2.2 Multi Sensors

-

2.2.3 Air Quality Sensors

-

2.2.4 Occupancy & Lighting

-

2.2.5 Other Sensors

-

-

2.3 By End-user Industry

-

2.3.1 Commercial

-

2.3.2 Residential

-

2.3.3 Industrial

-

-

US HVAC Field Device Market Size FAQs

How big is the US HVAC Field Device Market?

The US HVAC Field Device Market size is expected to reach USD 4.85 billion in 2024 and grow at a CAGR of 5% to reach USD 6.18 billion by 2029.

What is the current US HVAC Field Device Market size?

In 2024, the US HVAC Field Device Market size is expected to reach USD 4.85 billion.