| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 2.92 Billion |

| Market Size (2030) | USD 3.35 Billion |

| CAGR (2025 - 2030) | 2.77 % |

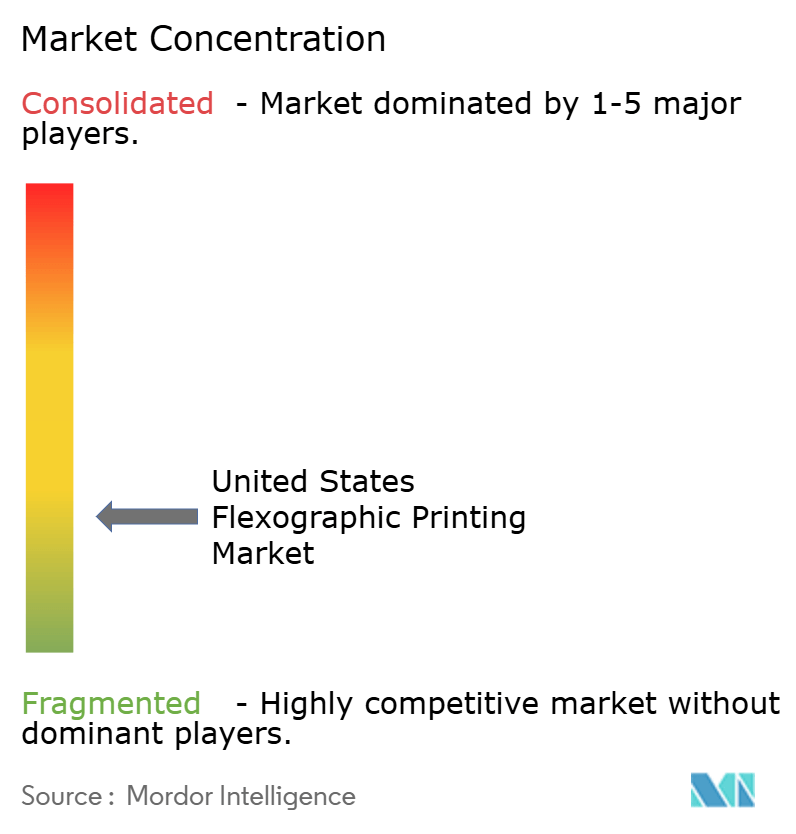

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

United States Flexographic Printing Market Analysis

The United States Flexographic Printing Market size is worth USD 2.92 Billion in 2025, growing at an 2.77% CAGR and is forecast to hit USD 3.35 Billion by 2030.

The flexographic printing industry is experiencing significant technological transformation driven by increasing automation and digitalization. The integration of Industry 4.0 technologies has revolutionized production workflows and quality control procedures, with manufacturers incorporating robotics and advanced CNC machining techniques into flexo press designs. This evolution is particularly evident in Taylor Corporation's July 2022 launch of an innovative hybrid press that combines digital UV inkjet technology with traditional flexographic printing, demonstrating the industry's move toward more sophisticated and efficient printing solutions.

The market is witnessing a notable shift toward sustainable and environmentally conscious practices, particularly in material selection and waste reduction. According to the Flexible Packaging Association, the US flexible packaging industry reached approximately USD 39 billion in sales in 2021, with a growing emphasis on recyclable and biodegradable materials. This trend is reflected in recent industry developments, such as UPM Raflatac's September 2022 announcement of a new terminal in Vancouver, WA, aimed at strengthening their network and expanding their sustainable labeling materials distribution capacity across North America.

The industry landscape is being reshaped by strategic investments and technological partnerships aimed at enhancing production capabilities and meeting evolving customer demands. A significant example is JohnsByrne's August 2022 acquisition of Heidelberg's newest CO2-neutral Speedmaster XL eight-color press, highlighting the industry's commitment to both technological advancement and environmental responsibility. These investments are driving improvements in print quality, with modern flexographic printing presses now capable of competing with offset and gravure printing through enhanced servo technology and superior tension control.

The industrial printing sector is adapting to changing consumer preferences and retail trends, particularly in the packaging printing industry. According to the US Census Bureau, retail trade sales and e-commerce value increased to USD 870.78 billion in 2021, driving demand for high-quality packaging solutions. This growth has led to increased adoption of advanced printing technologies that offer greater customization options and improved efficiency for both short and long production runs. The industry is responding with innovations in printing plate technology, ink systems, and press automation, enabling printers to deliver higher quality products while maintaining cost-effectiveness.

United States Flexographic Printing Market Trends

Enables Higher Production Speeds Within Reasonable Cost Overlay

Flexographic printing technology has revolutionized the package printing industry by offering unprecedented production speeds of up to 750 meters (2,000 feet) per minute while maintaining cost-effectiveness. The technology's ability to efficiently combine printing with almost any additional process into a single-pass operation provides significant economies of scale, making it an attractive option for both small and large-scale production runs. The advancement in efficiency and automation has transformed flexography from being purely a cost-effective printing method to one that can visually compete with any technology available in the market, while still maintaining its economic advantages through faster production enabled by quick-drying flexographic ink.

The integration of sophisticated automation and improved press control systems has significantly enhanced the operational efficiency of flexographic printing. Modern flexographic presses feature servo technology, better tension control, and advanced electronic systems that enable quick setup times, reduced waste, and minimal downtime between jobs. These technological improvements, combined with the ability to print on nearly any substrate including corrugated cardboard, cellophane, plastic, label stock, fabric, and metallic film, make flexographic printing particularly appealing for industrial applications such as the e-commerce industry, where both speed and versatility are crucial factors.

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand for UV-Curable Inks

The increasing environmental regulations in the United States have catalyzed a significant shift toward UV-curable inks in flexographic printing, primarily due to their zero volatile organic compound (VOC) emissions and superior performance characteristics. UV flexo inks offer remarkable advantages over traditional solvent-based or water-based alternatives, including instant curing capabilities, excellent adhesion properties across various substrates, and enhanced chemical resistance. The technology's ability to provide superior print quality, quick readiness for use, and fast running speeds has made it increasingly popular across multiple printing applications, from yogurt cups and tops to soup packets, flexible packaging, and even cigarette packs.

The market has witnessed substantial innovations in UV-curable ink technology, with manufacturers introducing new sustainable solutions. For instance, in May 2022, Siegwerk launched the SICURA Litho Pack ECO series, a sustainable UV offset ink series specifically designed for non-food paper and board applications, featuring high bio-renewable content. Additionally, hybrid UV inks, which contain either water or organic solvents, are gaining traction due to their ability to provide thinner dry layers and superior performance in packaging applications, particularly for corrugated boards and folding boxes. These technological advancements, coupled with the inks' ability to deliver consistent quality and improved production efficiency, continue to drive their adoption in the flexographic printing industry.

The Packaging Industry is Expected to Drive Demand for Both Equipment and Inks Category

The packaging industry's evolution, particularly in flexible packaging, has become a significant driver for flexographic printing equipment and ink demand. Flexible packaging represents approximately 20% of the total United States packaging industry, establishing itself as the second-largest packaging segment after corrugated paper. The industry's shift toward more sustainable and efficient packaging solutions has led to increased investments in flexographic printing technology, as it offers the versatility to handle various substrates while maintaining high-quality output and cost-effectiveness.

The demand for enhanced packaging functionality and quality has spurred technological advancements in flexographic printing equipment and inks. Companies are increasingly investing in new technologies and forming strategic partnerships to meet evolving market requirements. For instance, Label Tech's acquisition by Fortis Solutions Group in 2022 demonstrates the industry's focus on expanding geographical footprint and enhancing product offerings through flexographic printing capabilities. Additionally, the growing trend toward personalized, limited-run packaging has made flexographic printing platforms more appealing, as they offer the flexibility to handle both short and long production runs while maintaining consistent quality and cost-effectiveness across various packaging applications. This trend is further supported by the increasing demand for industrial label printing and packaging decoration solutions, which require the precision and adaptability that flexographic technology provides.

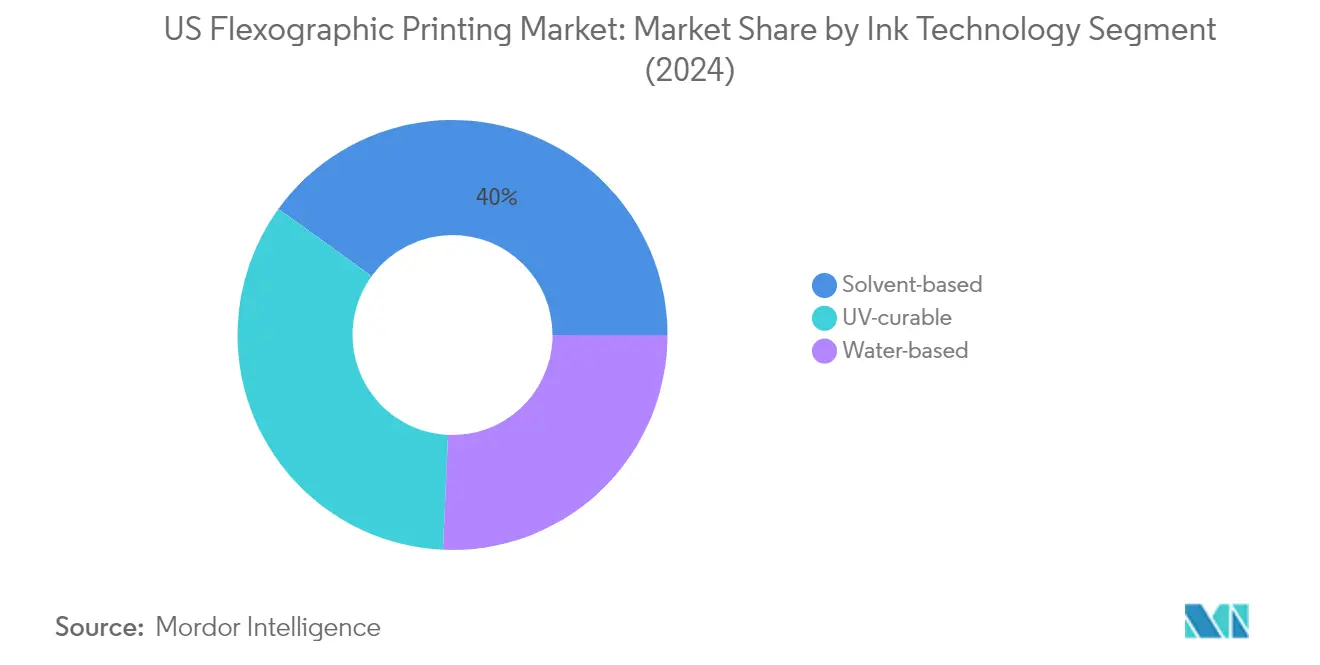

Segment Analysis: By Ink Technology

Solvent-based Segment in US Flexographic Printing Market

The solvent-based segment continues to dominate the US flexographic printing market, commanding approximately 40% market share in 2024. This significant market position is attributed to the segment's superior performance characteristics, including excellent resistance to chemical, mechanical, and external stresses compared to water-based alternatives. Solvent-based inks offer enhanced weather and wear resistance capabilities while maintaining compatibility with various surfaces and substrates, making them particularly valuable for packaging applications. The segment's strength is further reinforced by the high consumer demand for simple packaging solutions, customization flexibility, and lightweight properties. The introduction of green and bio-based ink solvents as substitutes for traditional petroleum-based solvents has helped address environmental concerns while maintaining performance standards.

UV-Curable Segment in US Flexographic Printing Market

The UV-curable segment is projected to exhibit the strongest growth trajectory in the US flexographic printing market, with an expected growth rate of approximately 4% during 2024-2029. This accelerated growth is driven by increasing environmental restrictions and the rising demand for volatile organic compounds (VOC) free printing inks. UV-cured inks offer significant advantages over conventional inks, including instant curing capabilities, superior print quality, and compatibility with both flexible and rigid packaging applications. The segment's growth is further supported by technological advancements in UV curing systems, which have enabled printers to improve print quality, increase productivity, and create safer press room environments. The adoption of hybrid UV inks containing water or organic solvents is gaining momentum, particularly in packaging applications for corrugated boards and folding boxes.

Remaining Segments in Ink Technology Market Segmentation

The water-based segment represents a crucial component of the US flexographic printing market, primarily driven by environmental considerations and specific application requirements. Water-based inks have gained significant traction in paper, cardboard, and textile printing applications, offering advantages such as stable viscosity and low volatile organic compound emissions. The segment has witnessed notable technological advancements, particularly in improving adhesion and wetting properties, which has expanded its applicability in flexible packaging applications. Recent developments in water-based ink formulations have also addressed traditional challenges related to drying time and substrate compatibility, making them increasingly viable for a broader range of printing applications.

Segment Analysis: By Application Type (Inks)

Packaging Segment in US Flexographic Printing Market

The packaging segment dominates the US flexographic printing market, commanding approximately 43% market share in 2024, while also demonstrating the strongest growth trajectory. This segment's prominence is driven by the increasing adoption of flexographic printing in various packaging applications, including flexible and rigid packaging solutions. The technology's ability to print on multiple substrates, combined with its cost-effectiveness for large-volume production, has made it particularly attractive for packaging manufacturers. The segment's growth is further supported by the rising e-commerce industry, which has intensified the demand for high-quality printed packaging materials. Additionally, the packaging segment benefits from flexographic printing's compatibility with environmentally friendly water-based inks, aligning with the increasing focus on sustainable packaging solutions in the United States.

Remaining Segments in Application Type (Inks)

The folding cartons segment represents a significant portion of the market, driven by the increasing demand for retail packaging and consumer goods. This segment benefits from flexographic printing's ability to deliver high-quality prints on paperboard materials while maintaining cost-effectiveness for large production runs. The tags and labels segment continues to be a crucial application area, particularly in industries such as food and beverage, pharmaceuticals, and consumer goods, where high-quality product identification and branding are essential. The paper-based printing segment, while smaller, maintains its importance in various commercial printing applications, particularly in sectors where traditional printing methods are preferred. These segments collectively contribute to the market's diversity and demonstrate the versatility of flexographic printing technology across different applications.

Segment Analysis: By Application (Equipment)

Narrow Web Segment in US Flexographic Printing Equipment Market

The Narrow Web segment dominates the US flexographic printing equipment market, commanding approximately 36% market share in 2024, while also exhibiting the strongest growth trajectory with a projected growth rate of around 3% during 2024-2029. This segment's prominence is attributed to its versatility in handling various printing applications, particularly in label printing and small-run flexible packaging. Narrow web printing offers superior solutions for businesses requiring quick label printing and other small-run applications, making it generally more accessible and cost-effective. The technology's ability to print on multiple substrates while maintaining high quality, combined with reduced VOC emissions through UV-curable inks, has strengthened its market position. The segment's growth is further driven by technological advancements in servo-based machines that enable faster setup times and improved task repeatability, allowing it to compete effectively even with shorter print runs where digital presses have traditionally held an advantage.

Remaining Segments in Equipment Applications Market

The Medium Web segment serves as a crucial bridge between narrow and wide web applications, offering optimal solutions for various packaging needs with web widths between 24 and 44 inches. Sheet-fed equipment provides specialized solutions for small and medium-sized print jobs, particularly suited for business cards, letterhead, stationery, and brochures. The Other Printing Equipment segment, which includes wide web printing applications, caters to high-volume production needs and is particularly effective for large-format packaging and industrial applications. Each of these segments serves distinct market needs, with Medium Web offering balanced solutions for medium-sized runs, Sheet-fed providing precision for specialized applications, and wide web equipment delivering high-speed, large-volume printing capabilities for industrial-scale operations.

Segment Analysis: By Phase (Equipment)

Post-Print Segment in US Flexographic Printing Market

The post-print segment continues to dominate the US flexographic printing market, holding approximately 76% market share in 2024. Post-print flexographic printing has established itself as the preferred choice for micro-flutes and corrugated printing, accommodating various substrates including coated, uncoated, and semi-coated materials. The segment's prominence is largely driven by its versatility in multi-color packaging applications and in-store displays, where water-based inks are applied directly onto corrugated materials through relief printing techniques using polymer relief plates. The technology's ability to deliver high-quality prints while maintaining cost-effectiveness has made it particularly attractive for packaging companies looking to enhance their operational capabilities. The segment's strong performance is further supported by the growing demand from end-user industries such as food and beverage and e-commerce, where corrugated and flexible packaging applications are extensively utilized.

Pre-Print Segment in US Flexographic Printing Market

The pre-print segment is emerging as the fastest-growing segment in the US flexographic printing market, projected to grow at approximately 3% during 2024-2029. This growth is primarily attributed to its ability to deliver high-quality finishes with low grammage, making it a cost-effective production method compared to other printing techniques. Pre-print flexographic printing is particularly effective for longer-run projects, especially when producing quantities of 10,000 or more boxes that require high-quality graphics to enhance brand identity at retail. The segment's growth is further accelerated by its capability to reduce the corrugated fluting effect found on most post-printed boxes while providing enhanced graphics at competitive pricing. The increasing adoption of pre-print flexo presses among end-users with bulk and high-volume demand, coupled with the shift in consumer expectations towards decorated outside packaging, continues to drive the segment's expansion in the market.

Segment Analysis: By End-User

Flexible Packaging Segment in United States Flexographic Printing Market

The flexible packaging segment dominates the United States flexographic printing market, commanding approximately 35% of the total market share in 2024. This segment's leadership position is driven by the increasing adoption of flexible packaging solutions across various industries, particularly in food and consumer goods sectors. The segment's growth is further bolstered by the rising demand for sustainable packaging options and the superior capabilities of flexographic printing in handling various flexible substrates. Flexible packaging applications benefit significantly from flexographic printing's ability to deliver high-quality prints on multiple materials while maintaining cost-effectiveness for both short and long production runs. The segment's prominence is also attributed to technological advancements in flexographic equipment, which have enhanced print quality and efficiency specifically for flexible packaging applications. Additionally, the growing e-commerce industry and changing consumer preferences towards convenient packaging solutions have further strengthened the position of flexible packaging in the flexographic printing market.

Remaining Segments in End-User Market

The United States flexographic printing market encompasses several other significant segments including label printing, folding cartons, print media, and other specialized applications. The labels segment maintains a strong presence in the market, particularly in industries such as pharmaceuticals, food and beverage, and consumer goods, where high-quality label printing is essential for brand recognition and regulatory compliance. Folding cartons represent another crucial segment, serving various packaging needs in retail and consumer products, while benefiting from flexographic printing's ability to deliver consistent quality on cardboard substrates. The print media segment, though smaller, continues to serve specific market needs in commercial printing applications. Other end-user applications include specialized printing requirements for industrial packaging, security printing, and various custom applications, each contributing to the market's diversity and overall growth. These segments collectively demonstrate the versatility and widespread adoption of flexographic printing technology across different industrial applications.

United States Flexographic Printing Industry Overview

Top Companies in United States Flexographic Printing Market

The flexographic printing market in the United States is characterized by continuous innovation and strategic developments from key players like DIC Corporation, Siegwerk Group, Flint Group, and BOBST Group. Companies are focusing on developing sustainable and environmentally friendly printing solutions, including water-based inks and energy-efficient printing equipment. The industry witnesses regular product launches incorporating advanced technologies like AI, machine learning, and IoT for enhanced automation and precision. Operational agility is demonstrated through investments in research and development, particularly in areas of UV-curable inks, digital integration, and hybrid printing solutions. Strategic partnerships and collaborations with technology providers are becoming increasingly common to strengthen market positions and expand service offerings. Companies are also expanding their geographical presence through acquisitions and establishing new production facilities to better serve regional markets and reduce delivery times.

Market Dominated by Global Technology Leaders

The United States flexographic printing market structure is characterized by the presence of both global conglomerates and specialized regional players, with international companies holding significant market share due to their technological capabilities and extensive distribution networks. The market shows moderate consolidation, with larger players leveraging their research capabilities and financial strength to maintain competitive advantages. The industry landscape is shaped by established manufacturers who have built strong relationships with end-users across various sectors, particularly in packaging printing and label printing.

The market has witnessed several strategic mergers and acquisitions aimed at expanding product portfolios and strengthening market presence. Companies are increasingly focusing on vertical integration to control quality and optimize costs throughout the value chain. Regional players maintain their relevance by offering specialized solutions and maintaining close customer relationships, while global players continue to expand their presence through strategic partnerships and acquisitions of local companies to enhance their market penetration and technical capabilities.

Innovation and Sustainability Drive Future Success

Success in the flexographic printing market increasingly depends on companies' ability to innovate while maintaining cost-effectiveness and environmental sustainability. Incumbent players are focusing on developing integrated solutions that combine traditional flexographic printing with digital technologies, while also investing in eco-friendly products to meet growing environmental concerns. Market leaders are strengthening their positions by offering comprehensive service packages, including technical support, training, and customized solutions, while also developing smart manufacturing capabilities to enhance operational efficiency.

For contenders looking to gain market share, the focus needs to be on developing specialized solutions for specific industry segments while building strong distribution networks. The market faces moderate substitution risk from digital printing technologies, making it crucial for companies to demonstrate the unique advantages of flexographic printing in terms of cost-effectiveness and versatility. Regulatory compliance, particularly regarding environmental standards and food safety requirements, continues to shape product development and market strategies. Companies that can effectively address these challenges while maintaining operational efficiency and product quality are likely to succeed in this evolving market landscape.

United States Flexographic Printing Market Leaders

-

DIC Corporation

-

SiegwerkGroup

-

Flint Group

-

Hubergroup USA Inc.

-

American Inks & Technology

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

United States Flexographic Printing Market News

- April 2024: Amcor announced a significant expansion of its North American printing and converting capabilities for the dairy market. This strategic move aims to support the growing demand for flexible packaging in the region.

- March 2024: Paper Converting Machine Company (PCMC), under BW Converting Solutions, announced the hosting of two free open houses at its Packaging Innovation Center in Green Bay, WI, from April 23 to 25, 2024. These events were open to newcomers and experts in packaging. Over the three days, the focus was on digital printing for flexible packaging and digital and flexo printing for the folding carton industry. Attendees gained valuable insights and information about the latest advancements and trends in digital printing technologies related to flexible packaging and folding carton production.

- January 2024: Catapult Print installed a new Nilpeter FA-26 press, furthering the company's goal of innovating printing processes and influencing the US market. The Nilpeter FA-26 is Catapult's eighth FA-Line press acquired in the past five years, and it is the first to have a 26-inch web width.

United States Flexographic Printing Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Enables Higher Production Speeds Within Reasonable Cost Overlay

- 5.1.2 Growing Demand for UV-curable Inks

- 5.1.3 The Packaging Industry Is Expected To Drive Demand For Both Equipment And Inks Category

-

5.2 Market Restraints

- 5.2.1 Advent of New Printing Technologies and Shift to Digital Mediums

6. MARKET SEGMENTATION

-

6.1 By Printing Ink

- 6.1.1 By Ink Technology

- 6.1.1.1 Water-based

- 6.1.1.2 Solvent-based

- 6.1.1.3 UV-curable

- 6.1.2 By Application Type

- 6.1.2.1 Packaging

- 6.1.2.1.1 Flexible

- 6.1.2.1.2 Rigid

- 6.1.2.2 Tags and Labels

- 6.1.2.3 Paper-based Printing

-

6.2 By Equipment

- 6.2.1 By Application Type

- 6.2.1.1 Narrow Web

- 6.2.1.2 Medium Web

- 6.2.1.3 Sheetfed

- 6.2.1.4 Other Printing Equipment

- 6.2.2 By Phase

- 6.2.2.1 Pre-print

- 6.2.2.2 Post-print

- 6.2.3 By End User

- 6.2.3.1 Folding Carton

- 6.2.3.2 Flexible Packaging

- 6.2.3.3 Labels

- 6.2.3.4 Print Media

- 6.2.3.5 Other End Users

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 DIC Corporation

- 7.1.2 Siegwerk Group

- 7.1.3 Flint Group

- 7.1.4 Hubergroup USA Inc.

- 7.1.5 American Inks & Technology

- 7.1.6 Inx International Ink Co.

- 7.1.7 Wikoff Color Corporation

- 7.1.8 ACTEGA GmbH

- 7.1.9 Zeller+Gmelin Corporation

- 7.1.10 Kolorcure Corporation

- 7.1.11 Comexi Group Industries SAU

- 7.1.12 Bobst Group SA

- 7.1.13 Heidelberger Druckmaschinen AG

- 7.1.14 Omet Americas Inc. (Omet Group)

- 7.1.15 MPS Systems BV

- 7.1.16 Mark Andy Inc.

- 7.1.17 Windmoller & Holscher KG

- 7.1.18 CMS Industrial Technologies LLC

- 7.1.19 Nilpeter USA Inc.

- *List Not Exhaustive

8. INVESTMENT OF THE MARKET

9. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

United States Flexographic Printing Market

Flexographic printing is a printing process that utilizes flexible plates formed of rubber or plastic. Each plate, with its lightly raised image, is wheeled on a cylinder and spread with fast-drying ink. The substance to be printed on, or the substrate, is passed between the print plate and the impression roller, which uses pressure to keep the substrate against the plate.

The United States flexographic printing market is segmented by printing ink (ink technology [water-based, solvent-based, and UV curable], application type [packaging {flexible and rigid}, tags and labels, and paper-based printing]), by equipment (application type [narrow web, medium web, sheetfed, and other printing equipment] and phase [pre-print and post-print], and end user [folding carton, flexible packaging, labels, print media, and other end users]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Printing Ink | By Ink Technology | Water-based | ||

| Solvent-based | ||||

| UV-curable | ||||

| By Application Type | Packaging | Flexible | ||

| Rigid | ||||

| Tags and Labels | ||||

| Paper-based Printing | ||||

| By Equipment | By Application Type | Narrow Web | ||

| Medium Web | ||||

| Sheetfed | ||||

| Other Printing Equipment | ||||

| By Phase | Pre-print | |||

| Post-print | ||||

| By End User | Folding Carton | |||

| Flexible Packaging | ||||

| Labels | ||||

| Print Media | ||||

| Other End Users | ||||

Need A Different Region or Segment?

Customize Now

United States Flexographic Printing Market Research Faqs

How big is the United States Flexographic Printing Market?

The United States Flexographic Printing Market size is worth USD 2.92 billion in 2025, growing at an 2.77% CAGR and is forecast to hit USD 3.35 billion by 2030.

What is the current United States Flexographic Printing Market size?

In 2025, the United States Flexographic Printing Market size is expected to reach USD 2.92 billion.

What years does this United States Flexographic Printing Market cover, and what was the market size in 2024?

In 2024, the United States Flexographic Printing Market size was estimated at USD 2.84 billion. The report covers the United States Flexographic Printing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United States Flexographic Printing Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

United States Flexographic Printing Market Research

Mordor Intelligence offers a comprehensive analysis of the flexographic printing industry. Our expertise spans both the commercial printing and industrial printing sectors. We cover the complete spectrum of flexo printing technologies, including relief printing processes, rotary printing systems, and specialized printing plate manufacturing. The report provides detailed insights into packaging printing trends, corrugated printing developments, and advances in industrial label printing technologies.

Stakeholders gain valuable insights through our report PDF, available for download. It examines crucial aspects of flexographic press operations, flexographic ink developments, and flexographic equipment innovations. The analysis includes both narrow web printing and wide web printing technologies. We also cover specialized applications in flexible packaging printing and package printing. Our research thoroughly examines packaging decoration techniques and emerging trends in label printing. This provides actionable intelligence for industry participants seeking to optimize their operations and strategic planning.