| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 2.07 Billion |

| Market Size (2030) | USD 2.89 Billion |

| CAGR (2025 - 2030) | 6.84 % |

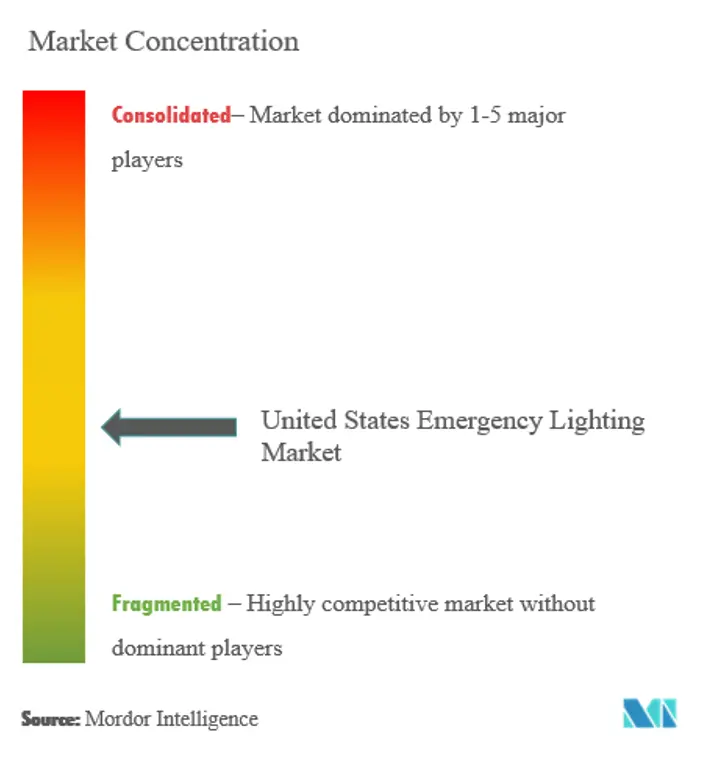

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

US Emergency Lighting Market Analysis

The United States Emergency Lighting Market size is estimated at USD 2.07 billion in 2025, and is expected to reach USD 2.89 billion by 2030, at a CAGR of 6.84% during the forecast period (2025-2030).

The United States emergency lighting industry is experiencing significant transformation driven by extensive infrastructure development and construction activities. The American Institute of Architects projects continued growth in construction spending over the next five years, with the non-residential construction market anticipated to grow by 2.4%. This growth is further supported by the government's recent allocation of $6 billion for federal building modernization, creating substantial opportunities for emergency lighting installations. The construction sector's expansion has prompted manufacturers to develop more sophisticated and integrated emergency lighting solutions that align with modern building requirements and safety standards.

Technological innovation is reshaping the emergency lighting landscape, with a notable shift toward connected and digital solutions. Industry leaders are increasingly incorporating IoT capabilities and wireless control systems into their emergency lighting products, enabling remote monitoring, automated testing, and predictive maintenance. These smart building solutions are particularly gaining traction in industrial and commercial facilities, where safety and maintenance are persistent concerns. The integration of mesh functionality in wireless emergency systems has emerged as a significant trend, allowing thousands of units to be connected and synchronized within the same network across large buildings.

The market is witnessing substantial consolidation through strategic mergers and acquisitions, reflecting the industry's maturation and need for technological advancement. A notable example is the January 2023 acquisition of ECCO Safety Group by Clarience Technologies, which expanded the company's portfolio of safety and emergency lighting solutions. Similarly, significant investments are being directed toward developing new capabilities and incorporating advanced technologies, as evidenced by recent acquisitions in the LED driver and power quality segments by major industry players.

The power distribution infrastructure in the United States is undergoing a significant transformation, supported by the government's $2 trillion infrastructure plan, which includes $100 billion specifically allocated for upgrading and expanding the country's electrical transmission system. This massive infrastructure investment is creating new opportunities for emergency lighting systems, particularly in critical facilities and power distribution buildings. The focus on grid modernization and the goal of achieving zero emissions by 2025 is driving the adoption of more sophisticated emergency lighting solutions that can integrate with smart grid applications and support sustainable building operations.

US Emergency Lighting Market Trends

Increase in Need for Energy-Efficient Lighting Systems and Favorable Government Regulations

The United States government's aggressive stance on energy efficiency and sustainability has become a major driver for the emergency lighting market. The Biden administration's commitment to reducing carbon pollution by 50-52% by 2030 compared to 2005 levels has created a strong regulatory framework supporting energy-efficient lighting solutions. This national determination under the Paris Agreement has led to the implementation of various policies and standards that mandate the adoption of energy-efficient lighting systems, including emergency lighting. According to the Department of Energy (DOE), commercial buildings consume approximately 22.5 kWh per square foot, with lighting accounting for roughly 7 kWh per square foot, making it the second-highest energy consumer after refrigeration and equipment.

The National Fire Protection Association's (NFPA) Life Safety Code 101 has established stringent requirements for emergency lighting in commercial buildings, mandating specific brightness levels and uniformity ratios. These regulations require emergency light fixtures to maintain a minimum of 6.5 lux throughout their operation period and a uniformity ratio not exceeding 40:1, pushing building owners and operators to invest in advanced, energy-efficient emergency lighting solutions. The integration of LED technology in industrial environments has demonstrated energy savings of up to 70%, making it an increasingly attractive option for facility managers looking to reduce operational costs while meeting regulatory requirements. Additionally, the development of specialty LED drivers and control modules has enabled advanced features such as remote maintenance, monitoring, dimming, and power metering, further driving the adoption of energy-efficient emergency lighting systems.

Understand The Key Trends Shaping This Market

Download PDF

Declining Prices of LED Products

The continuous decline in LED product prices, coupled with technological advancements, has significantly accelerated the adoption of LED-based emergency lighting solutions. The development of sophisticated LED drivers and control modules has made it possible to integrate advanced features while maintaining cost-effectiveness, making LED emergency lighting systems more accessible to a broader range of applications. This price reduction has been particularly beneficial for building owners undertaking retrofitting projects, as smart LED luminaires with onboard wireless communications now present a cost-effective approach to upgrading existing emergency lighting infrastructure.

The evolution of connected systems and Internet of Things (IoT) integration has further enhanced the value proposition of LED emergency lighting solutions. The incorporation of wireless technology and mesh functionality has enabled the creation of large-scale networks capable of connecting thousands of units to a single gateway, making it particularly suitable for extensive commercial and industrial installations. These connected systems offer enhanced capabilities such as remote monitoring, self-testing features, and automated maintenance scheduling, which help reduce operational costs and improve system reliability. The integration of LED technology with security systems has also improved emergency lighting testing procedures, with indicators displaying red or green signals for system readiness, as required by standards such as CSA C22.2 NO. 141 in North America, making compliance monitoring more efficient and cost-effective.

Segment Analysis: By Type

Centrally Supplied Segment in US Emergency Lighting Market

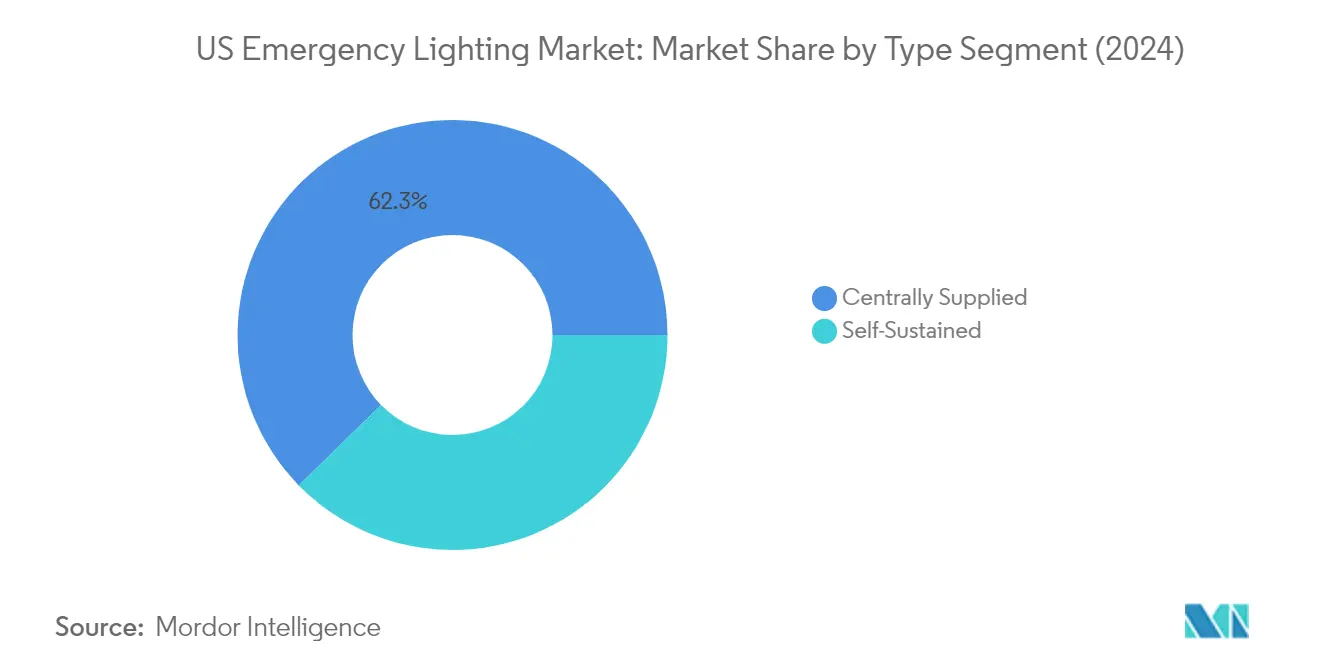

The centrally supplied segment dominates the United States emergency lighting market, holding approximately 62% market share in 2024. This segment's prominence is driven by its superior advantages for large-scale installations, particularly in multi-story office buildings and extensive commercial complexes. Centrally supplied systems offer significant benefits, including maximized battery life of typically ten years or more, simplified maintenance procedures, and enhanced resilience to temperature fluctuations since monitoring and regulation only need to be done at one centralized location. These systems are particularly favored in projects where emergency luminaires number in the hundreds, as they provide completely unobtrusive emergency lighting while offering long-term cost advantages. The segment's strength is further reinforced by its ability to operate at various voltage levels, from 24V to above 240V, making it versatile for different application requirements.

Self-Sustained Segment in US Emergency Lighting Market

The self-sustained emergency lighting segment is experiencing the fastest growth in the market, projected to grow at approximately 7% from 2024 to 2029. This growth is primarily driven by the segment's appeal to small and medium-sized businesses due to its cost-effectiveness and simpler installation requirements. The segment's expansion is further supported by technological advancements in LED integration and the development of sophisticated self-testing capabilities. Modern self-sustained systems now feature addressable automatic function and duration tests, helping building managers ensure compliance without the hassle of manual testing. The integration of smart technologies, including automated monitoring systems and mobile application connectivity, is enhancing the segment's appeal. Additionally, the development of more efficient battery technologies and improved power management systems is making these units increasingly reliable and maintenance-friendly.

Segment Analysis: By End User

Commercial Segment in US Emergency Lighting Market

The commercial segment maintains its dominant position in the United States emergency lighting market, accounting for approximately 43% of the total market value in 2024. This substantial market share is primarily driven by stringent government regulations, particularly the National Fire Protection Association's (NFPA) Life Safety Code 101, which mandates emergency egress lighting and exit path lighting in all commercial buildings. The Department of Energy's requirements for energy-efficient commercial emergency lighting solutions have also spurred the adoption of advanced emergency lighting systems in office buildings, restaurants, retail stores, and other commercial establishments. The segment's growth is further supported by the ongoing construction and renovation of commercial buildings across the United States, creating continuous demand for emergency lighting solutions that comply with safety standards while offering energy efficiency.

Healthcare Segment in US Emergency Lighting Market

The healthcare segment is emerging as the fastest-growing sector in the United States emergency lighting market, projected to grow at approximately 8% during the forecast period 2024-2029. This accelerated growth is driven by the critical nature of emergency lighting in healthcare facilities, where uninterrupted operations and safe evacuation procedures are paramount. The increasing focus on patient safety, stringent healthcare facility regulations, and the growing number of hospitals and medical centers are contributing to this segment's rapid expansion. Healthcare facilities are increasingly adopting advanced emergency backup lighting systems that comply with both the American National Standards Institute (ANSI) requirements and specific healthcare facility codes, ensuring reliable illumination during power outages and emergency situations.

Remaining Segments in End User Segmentation

The industrial, educational, and other end-user segments collectively form a significant portion of the US emergency lighting market, each serving unique requirements and applications. The industrial segment focuses on specialized emergency lighting solutions for hazardous environments such as manufacturing plants, warehouses, and chemical facilities. The educational segment encompasses schools and universities, where safety regulations mandate specific emergency escape lighting requirements for evacuation routes and common areas. Other end-users, including government buildings and utility facilities, require customized emergency pathway lighting solutions that meet specific operational and safety requirements while adhering to federal and state regulations.

US Emergency Lighting Industry Overview

Top Companies in United States Emergency Lighting Market

The United States emergency lighting market features several prominent players, including Acuity Brands, Eaton Corporation, ABB, Hubbell Incorporated, Signify, Legrand, and Emerson Electric. These companies are actively pursuing product innovation through advanced LED technologies and smart lighting solutions, with significant investments in research and development to create energy-efficient and connected emergency LED lighting systems. Operational agility is demonstrated through strategic manufacturing facility locations and robust distribution networks across the country. Companies are increasingly focusing on strategic partnerships and acquisitions to strengthen their market positions, particularly in emerging technologies and regional expansion. The industry is witnessing a strong trend toward developing hybrid solutions and IoT-enabled products, while also emphasizing sustainability and environmental compliance in product development and manufacturing processes.

Consolidated Market with Strong Global Players

The United States emergency lighting market is characterized by a consolidated structure dominated by large multinational conglomerates with diverse product portfolios. These major players leverage their extensive manufacturing capabilities, established distribution networks, and strong brand recognition to maintain their market positions. The market demonstrates high barriers to entry due to significant capital requirements, established customer relationships, and complex regulatory compliance needs. Merger and acquisition activities are prevalent, with companies actively pursuing strategic acquisitions to expand their technological capabilities and market reach.

The competitive landscape is further shaped by the presence of specialized regional players who focus on specific market segments or geographic areas. These companies often compete through specialized product offerings and local market expertise. The market has witnessed several notable acquisitions, particularly focusing on companies with advanced technological capabilities in LED and smart lighting solutions. Companies are increasingly pursuing vertical integration strategies to maintain control over their supply chains and enhance their competitive positioning.

Innovation and Adaptability Drive Market Success

Success in the emergency lighting market increasingly depends on companies' ability to innovate and adapt to changing technological landscapes and customer requirements. Incumbent players are focusing on developing comprehensive solution portfolios that integrate advanced technologies like IoT connectivity and smart monitoring systems. Companies are also investing in strengthening their distribution networks and after-sales service capabilities to maintain their competitive edge. The market shows a growing emphasis on customization capabilities and energy efficiency, with companies developing products that meet specific end-user requirements while complying with evolving energy standards.

For contenders looking to gain market share, focusing on niche market segments and developing specialized solutions offers a viable strategy. The market presents opportunities for companies that can effectively address the growing demand for sustainable and energy-efficient lighting solutions. Success also depends on building strong relationships with key stakeholders in commercial, industrial, and institutional sectors. Regulatory compliance remains a critical factor, with companies needing to stay ahead of evolving safety standards and energy efficiency requirements. The ability to provide comprehensive solutions that integrate emergency signage and exit sign systems with broader building management systems is becoming increasingly important for market success.

US Emergency Lighting Market Leaders

-

Acuity brands Inc.

-

EATON CORPORATION plc

-

ABB Ltd

-

Hubbell Inc.

-

Signify Holding

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

US Emergency Lighting Market News

- June 2021 - Eaton acquired Cobham Mission Systems. Cobham is a manufacturer of air-to-air refueling systems, environmental systems, and actuation, primarily for defense markets. This acquisition will help to expand Eaton Aerospace's fuel systems offerings and other defense-related offerings.

- June 2020 - Emerson Appleton released a safe and economical solution for retrofitting a plant's legacy HID lighting system to an energy-efficient LED system. The Appleton Contender LED Luminaires offer an energy savings of up to 65% compared to HID lighting. With the low-profile design, these luminaires provide lighting options for low clearance areas.

US Emergency Lighting Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Technology Snapshot

- 4.3 Industry Value Chain Analysis

-

4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

-

4.5 Market Drivers

- 4.5.1 Increase in Need for Energy-efficient Lighting Systems and Favorable Government Regulations

- 4.5.2 Declining Prices of LED Products

-

4.6 Market Challenges

- 4.6.1 High Initial Investment and Development of Alternative Technologies

- 4.7 Regulations and Policies

- 4.8 Impact of COVID-19 on the Emergency Lighting Market

- 4.9 Qualitative Analysis of the Market by Application (Stand-by vs Escape Route - Anti-panic and Signage)

5. MARKET SEGMENTATION

-

5.1 Type

- 5.1.1 Self-sustained

- 5.1.2 Centrally Supplied

-

5.2 End User

- 5.2.1 Commercial

- 5.2.2 Industrial

- 5.2.3 Educational

- 5.2.4 Healthcare

- 5.2.5 Other End Users

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles*

- 6.1.1 Acuity Brands Inc.

- 6.1.2 Eaton Corporation PLC

- 6.1.3 ABB Ltd

- 6.1.4 Hubbell Incorporated

- 6.1.5 Signify NV (Including Cooper Lighting Solutions)

- 6.1.6 Legrand SA

- 6.1.7 Emerson Electric Co.

- 6.1.8 Encore Lighting

- 6.1.9 Myers Emergency Power Systems

- 6.1.10 Larson Electronics

- 6.1.11 Cree Inc.

- 6.1.12 Digital Lumens Inc.

7. INVESTMENT ANALYSIS

8. FUTURE OF THE MARKET

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

US Emergency Lighting Industry Segmentation

Scope for emergency lighting - The revenue includes emergency lamps, luminaries (LED/fluorescence), and lighting accessories, such as power packs, monitoring systems, sensing modules, and lighting test switches. Different products include escape lighting (signage lighting and anti-panic lighting) and stand-by lighting (high-risk task lighting). The study also includes coverage on key end-user domains of emergency lighting and geographies.

| Type | Self-sustained |

| Centrally Supplied | |

| End User | Commercial |

| Industrial | |

| Educational | |

| Healthcare | |

| Other End Users |

Need A Different Region or Segment?

Customize Now

US Emergency Lighting Market Research FAQs

How big is the United States Emergency Lighting Market?

The United States Emergency Lighting Market size is expected to reach USD 2.07 billion in 2025 and grow at a CAGR of 6.84% to reach USD 2.89 billion by 2030.

What is the current United States Emergency Lighting Market size?

In 2025, the United States Emergency Lighting Market size is expected to reach USD 2.07 billion.

Who are the key players in United States Emergency Lighting Market?

Acuity brands Inc., EATON CORPORATION plc, ABB Ltd, Hubbell Inc. and Signify Holding are the major companies operating in the United States Emergency Lighting Market.

What years does this United States Emergency Lighting Market cover, and what was the market size in 2024?

In 2024, the United States Emergency Lighting Market size was estimated at USD 1.93 billion. The report covers the United States Emergency Lighting Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United States Emergency Lighting Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

United States Emergency Lighting Market Research

Mordor Intelligence provides a comprehensive analysis of the emergency lighting industry. We combine extensive research methodology with deep market insights. Our latest report examines crucial segments, including industrial emergency lighting, commercial emergency lighting, and residential emergency lighting applications. The analysis covers essential components such as emergency LED lighting, emergency luminaire systems, and emergency light fixture installations. These detailed insights are available in an easy-to-read report PDF format, ready for download.

The report offers stakeholders valuable intelligence on safety lighting trends, emergency signage requirements, and exit sign regulations across various sectors. Our analysis encompasses backup lighting solutions, emergency escape lighting systems, and emergency egress lighting specifications. It also examines evacuation lighting standards and emergency pathway lighting requirements. The research details emergency illumination technologies, including emergency backup lighting systems and specialized applications for emergency exit lighting. These insights provide actionable information for industry participants.