Data Center Construction Market Size")

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 14.35 Billion |

| Market Size (2030) | USD 21.43 Billion |

| CAGR (2025 - 2030) | 8.36 % |

| Market Concentration | Medium |

Major Players Data Center Construction Market Major Players")

*Disclaimer: Major Players sorted in no particular order |

United States (US) Data Center Construction Market Analysis

The United States Data Center Construction Market size is estimated at USD 14.35 billion in 2025, and is expected to reach USD 21.43 billion by 2030, at a CAGR of 8.36% during the forecast period (2025-2030).

The United States continues to dominate the global data center market landscape, with infrastructure expansion reaching unprecedented levels to meet surging digital demands. As of 2024, the country hosts 5,381 United States data centers, representing a net increase from the previous year's count of 5,375, reinforcing its position as the world's largest data center market. This expansion is driven by the rapid evolution of digital infrastructure needs, including the rise of artificial intelligence, edge computing, and the increasing adoption of cloud-based services across industries.

The energy consumption patterns of data centers are undergoing significant transformation, particularly in major hubs like Northern Virginia, which recorded a remarkable power consumption of 2.6 GW in 2023. This substantial energy requirement is reflected in operational costs, with data centers typically allocating between 30% and 50% of their operational expenditure to electricity. The industry is responding through innovative power management solutions and sustainable energy initiatives, as evidenced by recent partnerships between data center operators and renewable energy providers.

The emergence of AI-intensive workloads is dramatically reshaping data center infrastructure requirements. Traditional server racks requiring 10-14 kW are being replaced by AI-ready racks demanding 40-60 kW, necessitating significant upgrades to power and cooling systems. This shift is driving a comprehensive transformation in data center construction and design, with projections indicating that overall data center power consumption in the United States will surge from 17 GW in 2022 to approximately 35 GW by 2030.

The healthcare sector's digital transformation is catalyzing substantial demand for data center infrastructure. Recent studies indicate that telemedicine adoption has become mainstream, with 62% of visits conducted via video and 38% via telephone. This digital health revolution is expected to continue expanding, supported by increasing healthcare expenditure projections reaching USD 6.751 trillion by 2030, up from USD 4.29 trillion in 2021, driving the need for robust data center infrastructure to handle the growing volume of digital health records and real-time medical data.

United States (US) Data Center Construction Market Trends

Growing Cloud Applications, AI, and Big Data

The rapid adoption of cloud applications, artificial intelligence, and big data analytics is fundamentally transforming the data center construction market in the United States. Around 74% of US infrastructure decision-makers have reported adopting containers within Platform-as-a-Service (PaaS) environments, whether on-premises or in public clouds. This trend is further accelerated by the surge in Everything-as-a-Service (XaaS) demand, which witnessed a remarkable 42% year-over-year growth in the first half of 2022, primarily driven by the widespread adoption of hybrid work models requiring cloud-based tools and technologies.

Major technology companies are making substantial investments to support this growth. In March 2024, Google announced significant investments in data center construction across multiple locations, including Kansas City and Northern Virginia, specifically to strengthen its cloud and artificial intelligence capabilities. Similarly, AWS invested USD 35 billion in 2024 to build multiple cloud data center campuses in Virginia by 2040. These investments reflect the growing demand for advanced computing infrastructure capable of supporting AI workloads and compute demands, with companies increasingly focusing on developing facilities that can handle the intensive processing requirements of modern cloud applications and AI systems.

Understand The Key Trends Shaping This Market

Download PDF

Rising Adoption of Hyperscale Data Centers

The hyperscale data center segment is experiencing unprecedented growth in the United States, driven by the increasing demand for large-scale computing infrastructure. The United States has emerged as one of the key centers for IoT and big data, necessitating hyperscale data center development to protect and process the massive amounts of data being generated. The adoption of IoT-based devices is rapidly increasing across various sectors, including manufacturing, shipping, healthcare, and lifestyle, creating substantial demand for hyperscale facilities.

Recent developments highlight this trend, with significant investments in hyperscale infrastructure. In January 2024, Meta Platforms Inc. invested USD 800 million in a massive 700,000-square-foot data center campus in Indiana's River Ridge Commerce Center, with operations expected to commence by 2026. Additionally, in December 2023, Digital Realty and Blackstone formed a joint venture to develop large-scale data centers with a total capacity of 500 MW across three top-tier markets in Europe and North America, representing a total investment of USD 7 billion. These developments demonstrate the industry's commitment to meeting the growing demand for hyperscale facilities, particularly in regions with favorable conditions such as access to renewable energy sources and robust power infrastructure.

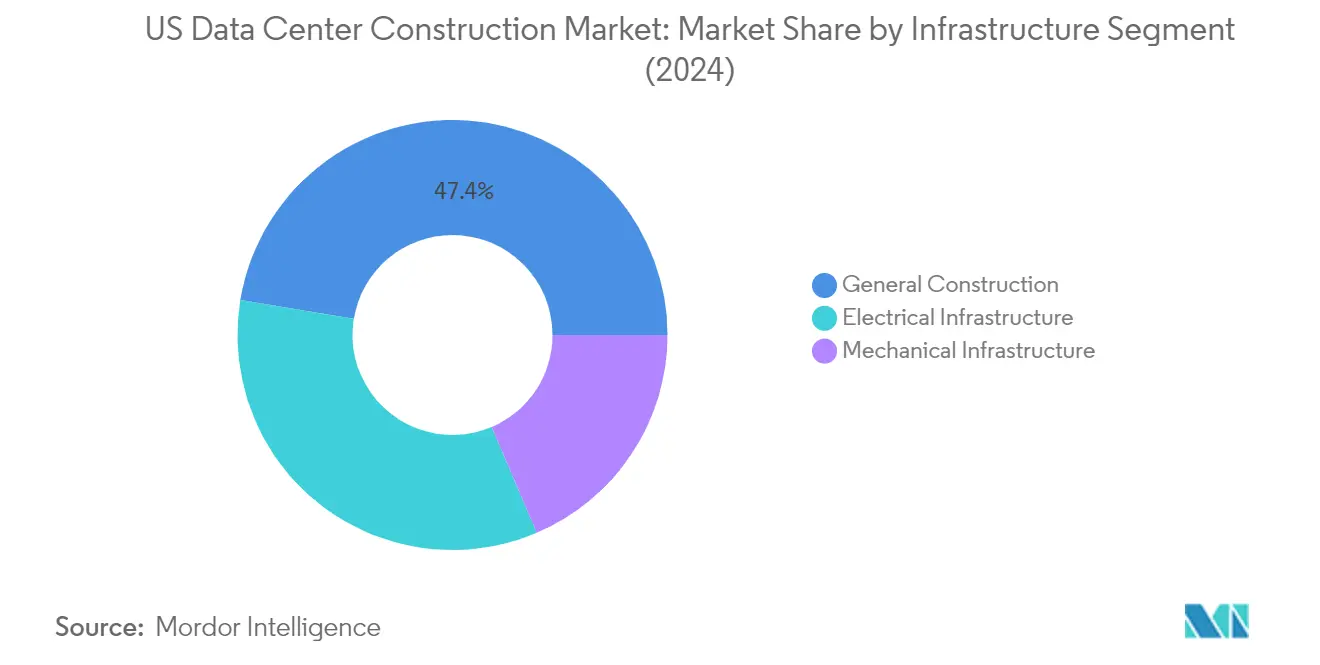

Segment Analysis: Infrastructure

General Construction Segment in US Data Center Construction Market

General construction represents the largest segment in the US data center construction market, commanding approximately 47% market share in 2024. This segment encompasses critical aspects like multi-level security infrastructure, perimeter fencing, anti-intrusion systems, dual authentication entry mechanisms, biometric security, and comprehensive video surveillance systems. The dominance of this segment is driven by increasing investments in data center security infrastructure, with major operators implementing advanced security protocols including real-time branch circuit monitoring for temperature and humidity control. The segment's growth is further bolstered by rising demand for both brownfield and greenfield projects, with most facilities aiming to attain LEED and Uptime Institute certifications according to Tier III standards.

Electrical Infrastructure Segment in US Data Center Construction Market

The electrical infrastructure segment is emerging as the fastest-growing segment in the US data center construction market, projected to grow at approximately 7% from 2024 to 2029. This robust growth is primarily driven by the increasing adoption of UPS systems, power distribution units, and other critical electrical components essential for maintaining uninterrupted data center operations. The segment's expansion is further fueled by the rising demand for reliable power backup solutions, especially in hyperscale data center facilities where power requirements are increasingly becoming more complex and demanding. The growth is also supported by innovations in power distribution technologies and the integration of smart power management systems that enhance overall data center efficiency and reliability.

Remaining Segments in Infrastructure

The mechanical infrastructure segment plays a vital role in the US data center construction market, encompassing crucial components such as cooling systems, racks, and other mechanical infrastructure elements. This segment is particularly significant in addressing the growing demands for efficient thermal management solutions in modern data center architecture. The segment's importance is underscored by the increasing adoption of advanced cooling technologies, including both air and liquid cooling systems, as well as the implementation of energy-efficient mechanical solutions. The continuous evolution of data center designs and the growing emphasis on sustainability have made mechanical infrastructure an indispensable component in ensuring optimal data center performance and reliability.

Segment Analysis: By Tier Type

Tier III Segment in US Data Center Construction Market

The Tier III segment dominates the US data center construction market, commanding approximately 53% market share in 2024. This significant market presence is driven by enterprises preferring Tier III data center facilities for their superior uptime and redundancy measures compared to lower tiers. Tier III facilities are concurrently maintainable, allowing for planned maintenance of power and cooling systems without disrupting computer hardware operations, offering N+1 availability. Major technology hubs like Northern Virginia and Phoenix host the maximum number of Tier III data centers in the country, with prominent providers including Equinix Inc., Digital Realty Trust Inc., Stack Infrastructure, and Quality Technology Services leading the segment's growth through continuous expansion and innovation in their facilities.

Tier IV Segment in US Data Center Construction Market

The Tier IV segment is experiencing the fastest growth in the US data center construction market, with a projected CAGR of approximately 12% from 2024 to 2029. This robust growth is driven by increasing demands for fault-tolerant infrastructure, particularly from sectors requiring the highest levels of reliability and security. Tier IV data center architecture is designed with 2N+1 redundancy for every process and data protection stream, ensuring no single outage or error can shut down the system. The segment's growth is further fueled by the rising adoption of hyperscale colocation services by major cloud providers and the increasing focus on computing solutions that demand the highest levels of reliability and security.

Remaining Segments in Tier Type Market Segmentation

The Tier I and Tier II segment represents the basic and entry-level data center infrastructure in the market. These tiers primarily cater to small and medium-sized businesses with basic redundancy requirements and cost-sensitive operations. While Tier I offers fundamental infrastructure with single power and cooling paths, Tier II provides slightly improved reliability with some redundant components. Though these segments play a crucial role in serving specific market needs, particularly for startups and smaller organizations requiring basic data center capabilities, they represent a smaller portion of the overall market as most enterprises opt for higher tier facilities with better reliability and redundancy features.

Segment Analysis: By End User

IT and Telecommunications Segment in US Data Center Construction Market

The IT and telecommunications segment dominates the US data center construction market, commanding approximately 47% of the total market share in 2024. This significant market position is driven by the massive demand from IT companies and telecom providers for data center infrastructure and storage capabilities. Major tech giants in the region, including cloud service providers and telecommunications companies, are making substantial investments in data center building to support their expanding operations. The segment's growth is further fueled by the increasing adoption of cloud services, artificial intelligence, and advanced technologies across the industry. The proliferation of 5G networks, IoT devices, and digital transformation initiatives has created an unprecedented demand for robust data center infrastructure, making this segment crucial for the overall market development.

Healthcare Segment in US Data Center Construction Market

The healthcare segment is emerging as the fastest-growing sector in the US data center construction market, projected to expand at approximately 12% CAGR from 2024 to 2029. This remarkable growth is primarily driven by the increasing digitization of healthcare records, the proliferation of telemedicine services, and the adoption of advanced technologies like IoT in healthcare applications. The sector's rapid digital transformation, coupled with strict regulatory requirements for data security and privacy, is creating substantial demand for specialized data center facilities. The integration of artificial intelligence in healthcare, growing implementation of electronic health records (EHR), and the rise of connected medical devices are further accelerating the need for robust data center infrastructure in the healthcare sector.

Remaining Segments in US Data Center Construction Market

The remaining segments in the market include Banking, Financial Services, and Insurance (BFSI), Government and Defense, and Other End Users, each contributing significantly to the market's diversity. The BFSI sector continues to drive demand through digital banking initiatives and fintech innovations, while the Government and Defense sector focuses on secure and compliant data center facilities for sensitive information storage. The Other End Users segment, which includes manufacturing, retail, and media and entertainment industries, is witnessing increased adoption of data center solutions driven by digital transformation initiatives and the growing need for data storage and processing capabilities across various industrial applications.

United States (US) Data Center Construction Market Overview

Top Companies in US Data Center Construction Market

The US data center construction market features prominent data center construction companies such as IBM Corporation, Schneider Electric, DPR Construction, Fortis Construction, Hensel Phelps, HITT Contracting, AECOM, and Turner Construction, among others. These data center construction companies are increasingly focusing on sustainable and energy-efficient construction practices, incorporating advanced technologies like artificial intelligence, robotics, and Building Information Modeling (BIM) in their operations. Strategic partnerships and collaborations with technology providers have become crucial for delivering innovative solutions, while investments in research and development are driving the adoption of modular and prefabricated construction techniques. Companies are expanding their geographical presence through new office locations and strengthening their capabilities in specialized areas such as hyperscale facilities and edge data centers. The emphasis on digital transformation and automation has led to enhanced project delivery methods, improved operational efficiency, and better risk management practices across the industry.

Market Dominated by Established Construction Giants

The US data center construction market exhibits a moderately consolidated structure with a mix of large multinational construction conglomerates and specialized data center contractors. The established players leverage their extensive experience, financial strength, and comprehensive service portfolios to maintain their market positions, while regional contractors focus on developing expertise in specific geographic markets or specialized construction services. The market has witnessed significant merger and acquisition activities as companies seek to expand their technical capabilities, geographic reach, and client base, particularly in emerging areas like edge computing and sustainable construction.

The competitive dynamics are characterized by high barriers to entry due to the specialized nature of data center construction, substantial capital requirements, and the need for established relationships with key stakeholders. Large construction firms are increasingly forming strategic alliances with technology providers, engineering firms, and equipment manufacturers to offer end-to-end solutions. The market also sees active participation from real estate investment trusts (REITs) and private equity firms, contributing to the overall market consolidation through strategic investments and acquisitions of construction capabilities.

Innovation and Sustainability Drive Future Success

Success in the US data center construction market increasingly depends on companies' ability to deliver sustainable, energy-efficient facilities while incorporating cutting-edge technologies and construction methods. Market leaders are investing heavily in developing expertise in areas such as renewable energy integration, advanced cooling systems, and modular construction techniques. Companies are also focusing on building strong relationships with cloud service providers, technology companies, and other major end-users while developing specialized solutions for different market segments such as hyperscale, colocation, and edge facilities.

The competitive landscape is evolving with increasing emphasis on operational excellence, risk management, and the ability to adapt to changing market demands. Companies that can demonstrate expertise in areas such as artificial intelligence infrastructure, edge computing, and sustainable construction practices are better positioned to capture market share in the data center industry by company. The regulatory environment, particularly regarding environmental sustainability and energy efficiency, is becoming more stringent, requiring companies to invest in green building capabilities and certification programs. Success also depends on the ability to manage complex supply chains, maintain strong relationships with subcontractors and suppliers, and deliver projects efficiently despite potential market disruptions.

United States (US) Data Center Construction Market Leaders

-

AECOM

-

Whiting-turner Contracting Company

-

Jacobs Solutions Inc.

-

DPR Construction

-

Skanska USA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

United States (US) Data Center Construction Market News

- In February 2024, in Caldwell County outside of Austin, Texas, Prime Data Centers proposed to construct a USD 1.3 billion data center complex. Such investments from the data center providers will create more demand for DC construction players in the near future.

- In November 2023, H5 Data Centres announced the expansion of its downtown San Antonio edge data center at 100 Taylor Street as a national colocation and wholesale data center provider. Up to 340 cabinets and up to 1.5 MW of additional UPS capacity will be enabled by the Tier III expansion of colocation space in Turnkey. In 2023, five new telecommunications operators were deploying infrastructure on the data center campus to drive continued growth of the network-rich ecosystem.

United States (US) Data Center Construction Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Growing Cloud Applications, AI, and Big Data

- 4.2.1.2 Rising Adoption of Hyperscale Data Centers

- 4.2.2 Market Restraints

- 4.2.2.1 Increase in Real Estate Costs

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

-

4.4 Key United States Data Center Construction Statistics

- 4.4.1 Number of Data Centers in the United States

- 4.4.2 Data Center Under Construction in the United States, in MW

- 4.4.3 Average Capex and Opex for the United States Data Center Construction

- 4.4.4 Data Center Power Capacity Absorption, in MW, Selected Cities, United States

- 4.5 Assessment of Impact of COVID-19 on the Market

5. MARKET SEGMENTATION

-

5.1 By Infrastructure

- 5.1.1 Electrical Infrastructure

- 5.1.1.1 UPS Systems

- 5.1.1.2 Other Electrical Infrastructure

- 5.1.2 Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.2 Racks

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.3 General Construction

-

5.2 By Tier Type

- 5.2.1 Tier-I and -II

- 5.2.2 Tier-III

- 5.2.3 Tier-IV

-

5.3 By End User

- 5.3.1 Banking, Financial Services, and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles*

- 6.1.1 AECOM

- 6.1.2 Whiting-turner Contracting Company

- 6.1.3 Jacobs Solutions Inc.

- 6.1.4 DPR Construction

- 6.1.5 Skanska USA

- 6.1.6 Balfour Beatty US

- 6.1.7 Hensel Phelps

- 6.1.8 McCarthy Building Companies Inc.

- 6.1.9 Gilbane Building Company

- 6.1.10 Brasfield & Gorrie LLC

7. INVESTMENT ANALYSIS

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

United States (US) Data Center Construction Market Industry Segmentation

The data center construction market involves data center planning, design, and physical construction. This includes developing facilities that house information technology infrastructure, such as servers, storage systems, networking equipment, and related components. The market encompasses various services and products related to the construction and outfitting of data centers, ranging from architectural and engineering services to installing specialized systems for power, cooling, and security.

The US data center construction market is segmented by infrastructure (electrical infrastructure [UPS systems, and other electrical infrastructure], mechanical infrastructure [cooling systems, racks, and other mechanical infrastructure], and general construction), tier type (tier-I and II, tier-III, and tier-IV), and end user (banking, financial services, and insurance, IT and telecommunications, government and defense, healthcare, and other end users). The report offers market forecasts and size in terms of value in USD for all the above segments.

| By Infrastructure | Electrical Infrastructure | UPS Systems | |

| Other Electrical Infrastructure | |||

| Mechanical Infrastructure | Cooling Systems | ||

| Racks | |||

| Other Mechanical Infrastructure | |||

| General Construction | |||

| By Tier Type | Tier-I and -II | ||

| Tier-III | |||

| Tier-IV | |||

| By End User | Banking, Financial Services, and Insurance | ||

| IT and Telecommunications | |||

| Government and Defense | |||

| Healthcare | |||

| Other End Users | |||

Need A Different Region or Segment?

Customize Now

United States (US) Data Center Construction Market Research FAQs

How big is the US Data Center Construction Market?

The US Data Center Construction Market size is expected to reach USD 14.35 billion in 2025 and grow at a CAGR of 8.36% to reach USD 21.43 billion by 2030.

What is the current US Data Center Construction Market size?

In 2025, the US Data Center Construction Market size is expected to reach USD 14.35 billion.

Who are the key players in US Data Center Construction Market?

AECOM, Whiting-turner Contracting Company, Jacobs Solutions Inc., DPR Construction and Skanska USA are the major companies operating in the US Data Center Construction Market.

What years does this US Data Center Construction Market cover, and what was the market size in 2024?

In 2024, the US Data Center Construction Market size was estimated at USD 13.15 billion. The report covers the US Data Center Construction Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the US Data Center Construction Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

United States (US) Data Center Construction Market Research

Mordor Intelligence provides comprehensive industry analysis and market outlook for the United States data center construction market, offering detailed insights into data center infrastructure, data center architecture, and data center facility developments. Our industry research encompasses market size, growth trends, and competitive landscape analysis of leading data center construction companies, with particular focus on sustainable data center construction and hyperscale data center construction initiatives. The report pdf includes strategic market segmentation, detailed statistics, and future market forecasts, enabling stakeholders to make informed decisions about their investments in data center development and data center expansion projects.

Our consulting expertise extends beyond traditional market research to provide comprehensive solutions for the US data center industry. We assist clients with technology scouting for advanced data center engineering solutions, conduct feasibility analysis for new data center construction projects, and provide detailed competition assessment of data center contractors. Our services include B2B surveys to understand emerging data center construction trends, project feasibility analysis for edge data center construction initiatives, and strategic guidance for data center design and construction optimization. Through data aggregation and advanced analytics, we help stakeholders navigate complex decisions regarding data center renovation and modernization projects, ensuring alignment with industry best practices and regulatory requirements.