Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 15.19 Billion |

| Market Size (2030) | USD 19.97 Billion |

| Growth Rate (2025 - 2030) | 5.63% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Construction Chemicals Market Analysis by Mordor Intelligence

The United States Construction Chemicals Market size is estimated at USD 15.19 billion in 2025, and is expected to reach USD 19.97 billion by 2030, at a CAGR of 5.63% during the forecast period (2025-2030). Multiple federal infrastructure programs, tightening building codes, and rapid digitalization of job-site workflows are sustaining demand even as volatile petroleum inputs and labor shortages weigh on margins. Federal procurement preferences for low-carbon materials are accelerating the shift toward bio-based admixtures and low-VOC coatings, while investments in data centers and semiconductors are expanding the addressable market for high-performance flooring systems. Climate resilience legislation, particularly in hurricane-prone states, is driving higher specification rates for waterproofing membranes that can withstand wind-driven rain and hydrostatic pressure. At the same time, vertical integration moves by large producers are compressing distributor margins yet providing downstream contractors with more predictable supply in an otherwise strained logistics environment.

Key Report Takeaways

- By product, waterproofing solutions commanded 34.85% of the US construction chemicals market size in 2024. The same are poised for the fastest 6.15% CAGR during the outlook period.

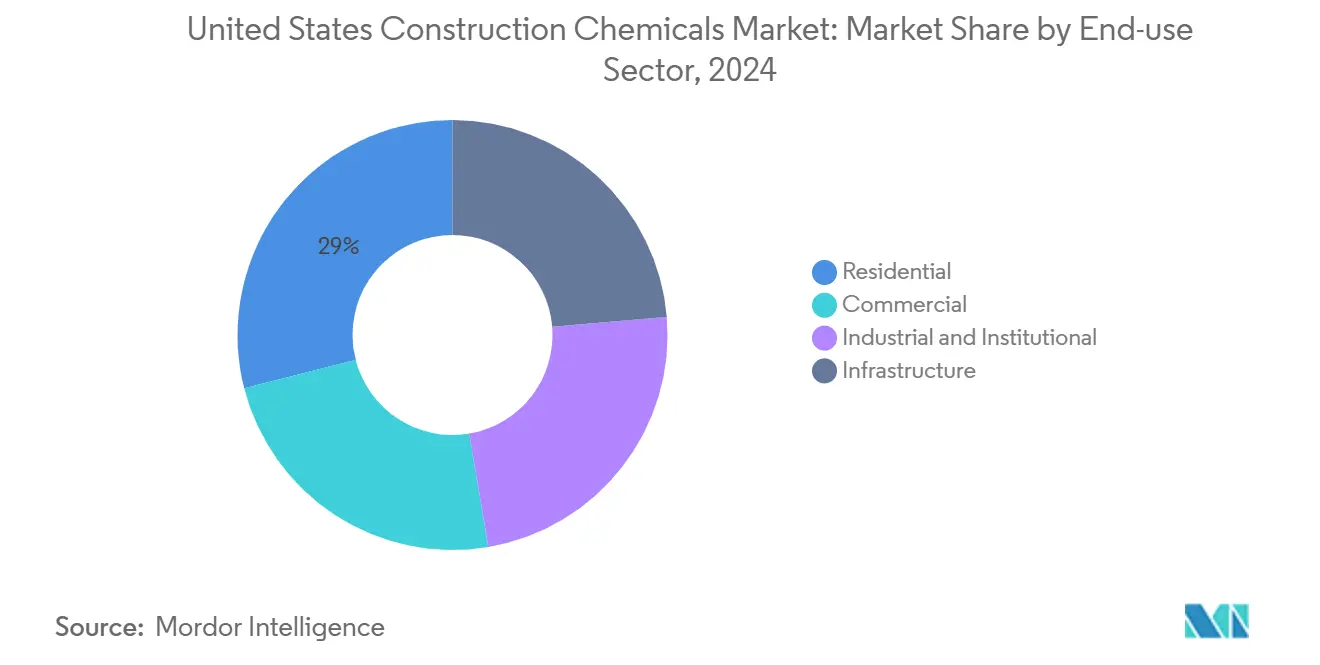

- By end-use sector, the residential segment accounted for a 28.99% share of the US construction chemicals market in 2024 and is projected to grow at a 6.29% CAGR through 2030.

United States Construction Chemicals Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-bill funded mega-projects | +1.2% | National, concentrated in Southeast and Southwest | Medium term (2-4 years) |

| Housing-start rebound and repair backlog | +0.9% | National, strongest in Texas, Florida, North Carolina | Short term (≤ 2 years) |

| Shift toward high-performance and green admixtures | +0.7% | National, early adoption in California and Northeast | Long term (≥ 4 years) |

| Code-driven uptake of waterproofing and protective coatings | +0.8% | National, accelerated in coastal and seismic zones | Medium term (2-4 years) |

| Data-center boom fueling specialty flooring demand | +0.6% | Concentrated in Virginia, Texas, California, Oregon | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Infrastructure-Bill Funded Mega-Projects

Federal spending channeled through the Infrastructure Investment and Jobs Act is accelerating demand for high-durability admixtures, corrosion-resistant coatings, and crystalline waterproofing systems that extend bridge and tunnel service life by more than six decades. Contractors undertaking rail realignments and port expansions increasingly specify low-shrinkage superplasticizers that improve pumpability on congested sites. Suppliers with mobile batching laboratories are winning multi-year supply agreements because continuous mix verification is now written into many public contracts. Regional clusters around interstate corridors enable manufacturers to shorten lead times, lower freight costs, and provide onsite technical training that mitigates application errors.

Housing-Start Rebound and Repair Backlog

Single-family permits are rising in tandem with declining mortgage rates, while a USD 574.3 billion home-improvement sector is pushing pent-up repair work into 2025[1]Master Builders Solutions, “MasterEase 5000 Water-Reducing and Conditioning Admixture,” master-builders-solutions.com. The dual flow of new builds and retrofits favors multi-purpose waterproofing membranes, low-VOC sealants, and crack-bridging repair mortars that enable occupied-building renovations without lengthy shutdowns. The US construction chemicals market continually benefits from do-it-yourself channels where smaller packaging formats and color-matched sealants produce repeat consumer purchases. Distributors that bundle moisture-barrier products with surface treatments are capturing higher basket values because homeowners frequently tackle insulation, flooring, and façade upgrades in a single project cycle.

Shift Toward High-Performance and Green Admixtures

Sustainability benchmarks embedded in LEED, CALGreen, and municipal low-carbon ordinances are catalyzing broad adoption of bio-based superplasticizers such as Sika’s next-generation ViscoCrete range, which cuts petrochemical content without sacrificing slump retention[2]Sika, “Next Generation Bio-Based Chemical Admixtures for Concrete,” usa.sika.com. Mapei’s MAPECUBE line allows higher supplementary cementitious material ratios while maintaining compressive strength, reducing embodied carbon by roughly one-quarter. Manufacturers with robust research and development pipelines now co-design mixes with ready-mix producers, integrating hydration-kinetic software to predict early-age strength and optimize curing windows. The US construction chemicals market thereby positions low-carbon concrete as a mainstream rather than niche solution.

Code-Driven Uptake of Waterproofing and Protective Coatings

Hurricane-exposed coastlines and inland flood plains are subject to tightened International Building Code provisions that enforce enhanced moisture-management layers. Crystalline waterproofing systems capable of autogenous crack healing dominate podium slabs and substructures because they eliminate secondary membrane installations while extending design life by 60 years. Updated ACI durability classifications mandate chloride-threshold performance in parking structures, fueling demand for epoxy-urethane hybrid coatings that tolerate de-icing salt attack. The US construction chemicals market sees insurers insisting on documented coating selection, moving liability upstream to material suppliers and enforcing third-party testing protocols.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petroleum-derived raw material prices | -0.8% | National, acute impact on Gulf Coast manufacturers | Short term (≤ 2 years) |

| Tightening VOC and toxic-chemical regulations | -0.5% | National, strictest in California and Northeast | Medium term (2-4 years) |

| Skilled applicator shortage for advanced systems | -0.7% | National, most severe in Southeast and Southwest | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Petroleum-Derived Raw-Material Prices

Epoxy-resin prices rose in 2025 amid logistics bottlenecks, widening bid-price spread for flooring contractors, and forcing escalator clauses into fixed-sum contracts. Smaller regional blenders lacking hedging mechanisms face working-capital pinch points as payment cycles stretch, prompting consolidation within the US construction chemicals market. Some manufacturers are reformulating toward bio-based diluents and reclaimed PET polyols to cushion margin swings, though supply volumes remain limited. Raw-material volatility also complicates public-project budgeting because many states lock annual appropriations well before bid openings, creating a mismatch between funding and procurement costs.

Skilled Applicator Shortage for Advanced Systems

The industry must onboard about 439,000 additional workers in 2025 to meet scheduled workloads, yet apprenticeship enrollments trail retirements, particularly in niche segments such as structural-strengthening composites. High-performance coatings often require dew-point monitoring, plural-component spraying, and holiday-testing equipment unfamiliar to general paint crews. This labor crunch hampers the US construction chemicals market penetration of premium systems that rely on meticulous application for warranty validity. Suppliers have responded with two-day installer-certification courses and augmented-reality guidance that overlay mixing ratios and spray patterns in real time, although widespread adoption remains in early stages.

Segment Analysis

By Product: Waterproofing Solutions Reinforce Envelope Durability

Waterproofing solutions generated the largest share of the United States construction chemicals market at 34.85% in 2024 and are expected to expand at a 6.15% CAGR through 2030. This dominance reflects code-mandated continuous air barriers and insurance-driven moisture control upgrades in both commercial and residential builds. Liquid-applied membranes are outpacing sheet goods because spray application seamlessly wraps complex penetrations, eliminating seams that can become failure points. Rising hurricane frequency encourages builders in coastal ZIP codes to choose elastomeric membranes tested to withstand 10,000 fatigue cycles, a feature that commands a 15% price premium yet lowers lifetime repair expense.

Seamless membrane uptake benefits one-part, moisture-cure polyurethane chemistries that tolerate damp substrates common in fast-track schedules. Contractors report that new low-odor formulations enable interior application without the need for negative-pressure tents, thereby expanding usage to subterranean parking decks. Sustainability metrics matter too, and water-borne acrylic membranes with 35% recycled content now qualify for federal tax incentives on public housing projects. With the EPA exploring stricter solvent cutoffs, producers are investing in silyl-terminated polyether backbones that combine flexibility with ultralow VOC outputs. Together, these dynamics position waterproofing systems to preserve the leading title in the United States construction chemicals market through the forecast horizon.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-Use Sector: Residential Dominance Drives Growth

The residential segment generated the largest share of demand, capturing 28.99% of the US construction chemicals market in 2024 and sustaining the fastest projected 6.29% CAGR as deferred pandemic repairs converge with new home starts. Younger buyers tend to gravitate toward high-efficiency envelopes that incorporate low-VOC elastomeric coatings to seal microcracks and reduce HVAC loads. Over the forecast horizon, the US construction chemicals market size for residential waterproofing membranes is expected to grow as Sun Belt municipalities adopt stricter moisture-barrier codes to counteract intensified rainfall events.

Product packaging trends indicate a shift toward contractor-friendly pails with integral dosing lids, facilitating job-site admixture additions without the need for field scales. Leading suppliers bundle crystalline admixtures with repair mortars, creating turnkey “dry-basement” kits that tackle both new foundations and retrofit scenarios. Consumer-facing brands leverage big-box retail visibility while maintaining professional-grade SKUs for multifamily builders that require submittal documentation and third-party durability testing.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Coastal states exhibit the most pronounced uptake of chloride-resistant admixtures and high-build elastomeric coatings because salt spray accelerates concrete and steel degradation. Florida municipalities now require enhanced permeability indices in structural concrete mixes, elevating polycarboxylate-based water-reducers to default specification. Interior Frost-belt markets demand air-entrainment control and rapid-set patching compounds that accommodate freeze-thaw cycling.

The Sun Belt anchors residential momentum; Texas alone accounted for more than one-tenth of single-family starts in 2024, driving incremental demand for slab-on-grade moisture barriers that mitigate vapor transmission into flooring assemblies. The US construction chemicals market presence in California is shaped by the nation’s toughest VOC thresholds, compelling suppliers to develop ultra-low-emission polymers to retain shelf placement.

Data-center concentrations in Northern Virginia’s “Fiber Alley,” Central Texas, and the Pacific Northwest create tight regional cycles for antistatic flooring installers. Suppliers operate temporary blending hubs near these clusters to synchronize deliveries with accelerated construction schedules. In the Midwest, state departments of transportation specify slag-rich concrete mixes to lower embodied carbon, supporting higher-dosage accelerator formulations that offset slower early-age strength in colder climates. Federal highway renewal allocations have increased demand for high-bond repair grouts capable of accommodating cyclic dynamic loads on expansion joints.

Competitive Landscape

The market remains moderately concentrated. Technology investment is the dominant competitive lever. Leading producers channel up to 4% of sales into R&D focused on low-VOC resins and carbon-minimized admixtures to stay ahead of EPA directives. Regulatory compliance proficiency differentiates market leaders; companies with robust toxicology teams can certify formulations swiftly under changing VOC or substance-of-concern rules, allowing them to retain shelf space when competitors’ products are delisted.

United States Construction Chemicals Industry Leaders

-

Sika AG

-

MAPEI S.p.A.

-

RPM International Inc.

-

Saint-Gobain

-

HOLCIM

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Sika acquired HPS North America, integrating building-finishing materials and waterproofing solutions to accelerate expansion in the US finishing segment.

- February 2025: Saint-Gobain finalized its USD 1.025 billion purchase of Fosroc, bringing 3,000 employees and 20 plants into its global construction-chemicals network while reinforcing US waterproofing and admixture ranges.

United States Construction Chemicals Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, Surface Treatment Chemicals, Waterproofing Solutions are covered as segments by Product.

By Product

| Adhesives | Hot-Melt |

| Reactive | |

| Solvent-borne | |

| Water-borne | |

| Anchors and Grouts | Cementitious Fixing |

| Resin Fixing | |

| Concrete Admixtures | Accelerator |

| Air-Entraining | |

| Super-plasticizer | |

| Retarder | |

| Shrinkage-Reducer | |

| Viscosity-Modifier | |

| Plasticizer | |

| Other Types | |

| Concrete Protective Coatings | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyurethane | |

| Other Resins | |

| Flooring Resins | Acrylic |

| Epoxy | |

| Polyaspartic | |

| Polyurethane | |

| Other Resins | |

| Repair and Rehabilitation Chemicals | Fiber-Wrapping Systems |

| Injection Grouting | |

| Micro-concrete Mortars | |

| Modified Mortars | |

| Rebar Protectors | |

| Sealants | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| Surface-Treatment Chemicals | Curing Compounds |

| Mold-Release Agents | |

| Other Types | |

| Waterproofing Solutions | Chemicals |

| Membranes |

By End-User Sector

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| By Product | Adhesives | Hot-Melt |

| Reactive | ||

| Solvent-borne | ||

| Water-borne | ||

| Anchors and Grouts | Cementitious Fixing | |

| Resin Fixing | ||

| Concrete Admixtures | Accelerator | |

| Air-Entraining | ||

| Super-plasticizer | ||

| Retarder | ||

| Shrinkage-Reducer | ||

| Viscosity-Modifier | ||

| Plasticizer | ||

| Other Types | ||

| Concrete Protective Coatings | Acrylic | |

| Alkyd | ||

| Epoxy | ||

| Polyurethane | ||

| Other Resins | ||

| Flooring Resins | Acrylic | |

| Epoxy | ||

| Polyaspartic | ||

| Polyurethane | ||

| Other Resins | ||

| Repair and Rehabilitation Chemicals | Fiber-Wrapping Systems | |

| Injection Grouting | ||

| Micro-concrete Mortars | ||

| Modified Mortars | ||

| Rebar Protectors | ||

| Sealants | Acrylic | |

| Epoxy | ||

| Polyurethane | ||

| Silicone | ||

| Other Resins | ||

| Surface-Treatment Chemicals | Curing Compounds | |

| Mold-Release Agents | ||

| Other Types | ||

| Waterproofing Solutions | Chemicals | |

| Membranes | ||

| By End-User Sector | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| Residential | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- END-USE SECTOR - Construction chemicals consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of construction chemical products such as concrete admixtures, repair and rehabilitation chemicals, flooring resins, waterproofing solutions, anchors and grouts, adhesives and sealants, and surface treatment chemicals is considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF