| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 2.52 Billion |

| Market Size (2030) | USD 3.35 Billion |

| CAGR (2025 - 2030) | 5.86 % |

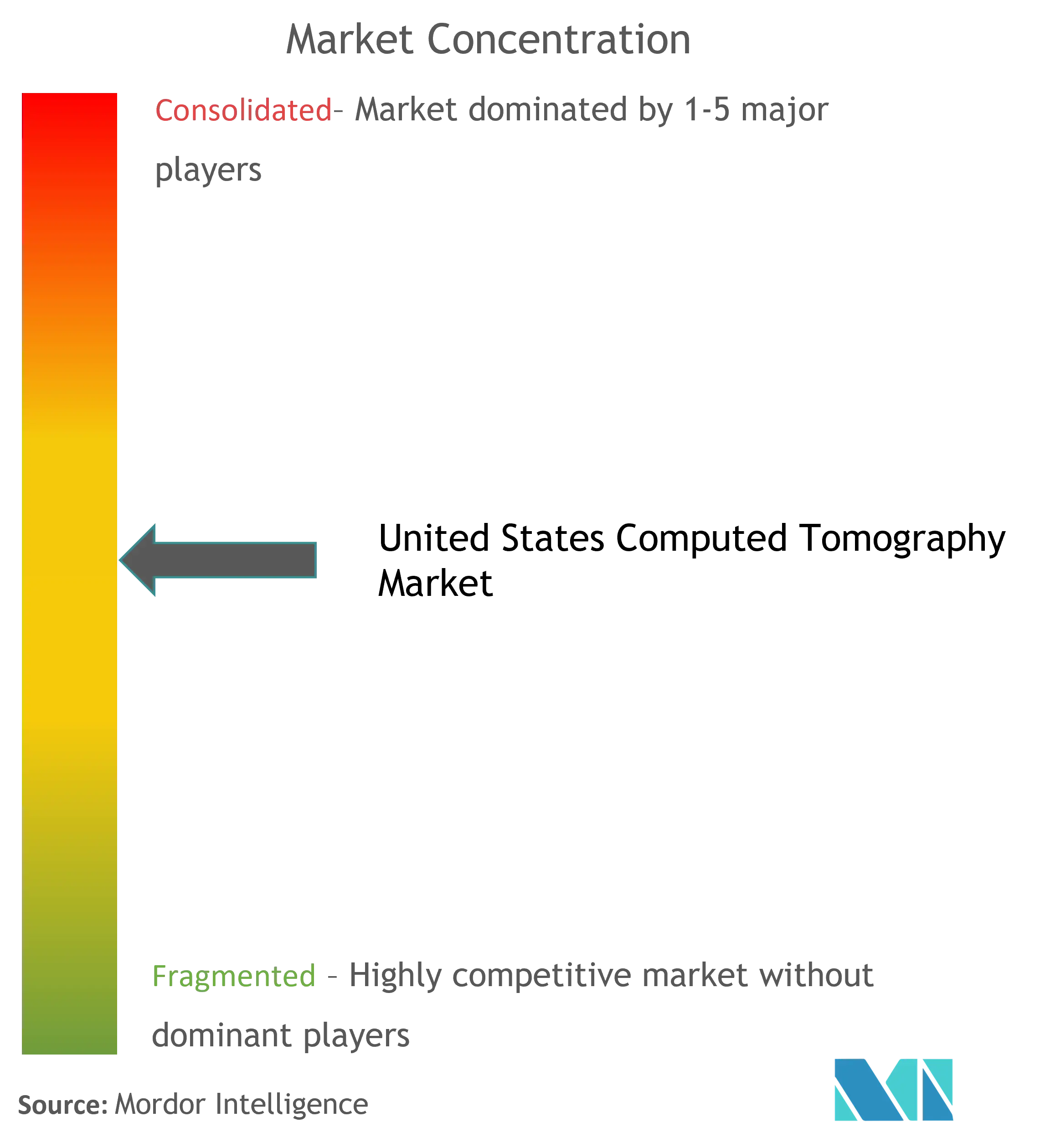

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

United States Computed Tomography Market Analysis

The United States Computed Tomography Market size is estimated at USD 2.52 billion in 2025, and is expected to reach USD 3.35 billion by 2030, at a CAGR of 5.86% during the forecast period (2025-2030).

The United States computed tomography industry is experiencing significant transformation driven by broader healthcare sector dynamics and technological innovation. According to the Centers for Disease Control and Prevention, chronic diseases are the primary drivers of the nation's USD 3.8 trillion annual healthcare costs, with 6 out of 10 adults living with at least one chronic condition. This healthcare burden is further amplified by demographic shifts, as the elderly population is projected to reach 84.813 million by 2050, creating increased demand for advanced diagnostic imaging solutions. The integration of artificial intelligence and machine learning into CT imaging systems has become a cornerstone of market evolution, enabling more precise diagnostics and improved patient outcomes. Healthcare providers are increasingly investing in modernizing their imaging infrastructure to accommodate these technological advances and meet growing patient needs.

The market landscape is being reshaped by significant technological breakthroughs and regulatory approvals. In September 2021, the FDA's approval of Siemens NAEOTOM Alpha marked a revolutionary advancement in CT imaging technology, introducing photon-counting detectors capable of measuring individual X-rays passing through patients' bodies. This innovation represents a significant leap forward from conventional systems that measure total energy from multiple X-rays simultaneously. The industry has witnessed a surge in research and development activities, with major players focusing on developing more efficient and patient-friendly medical imaging solutions. These advancements are particularly focused on reducing radiation exposure while maintaining or improving image quality.

Industry consolidation and strategic partnerships have emerged as key trends shaping the market dynamics. Major healthcare providers and imaging equipment manufacturers are forming alliances to enhance their service offerings and expand market reach. For instance, in 2023, several healthcare institutions have implemented advanced CT systems through strategic partnerships with leading manufacturers, focusing on improving diagnostic imaging capabilities and operational efficiency. These collaborations are particularly evident in the development and implementation of artificial intelligence-powered imaging solutions, which are transforming traditional CT scanning procedures.

The market is witnessing a paradigm shift towards preventive healthcare and early disease detection. Healthcare providers are increasingly adopting advanced computed tomography systems that offer superior diagnostic capabilities for early-stage disease identification. This trend is supported by the integration of data analytics and artificial intelligence, enabling more accurate and efficient diagnosis. The focus has shifted towards developing systems that can provide comprehensive health assessments while minimizing radiation exposure and improving patient comfort. These developments are particularly significant in oncology, cardiovascular, and neurological applications, where early detection can significantly impact treatment outcomes.

United States Computed Tomography Market Trends

Rising Prevalence of Chronic Diseases

The increasing burden of chronic diseases, particularly cardiovascular conditions, cancer, and orthopedic disorders, is driving significant demand for CT systems in the United States. According to the American Heart Association Research Report, heart disease remains a leading cause of mortality, accounting for one in seven deaths in the United States. The distribution of cardiovascular disease-related deaths shows a concerning pattern, with coronary heart disease leading at 43.8%, followed by stroke (16.8%), heart failure (9.0%), and high blood pressure (9.4%), necessitating advanced diagnostic imaging capabilities.

The rising cancer incidence has also become a crucial factor driving CT adoption. Studies at the University of California, Los Angeles have demonstrated that regular screening of at-risk populations can detect many cases of lung cancer much earlier, reducing mortality by 20-30%. This has led to the United States Preventive Services Task Force recommending annual CT screening for high-risk groups. The commitment to advancing cancer diagnostics is further evidenced by the National Institutes of Health's increased investment in cancer research, reaching USD 7,176 million in 2021, representing a significant rise from USD 7,035 million in 2020.

Understand The Key Trends Shaping This Market

Download PDF

Technological Advancements in CT Imaging

The computed tomography market is experiencing substantial growth driven by continuous technological innovations that enhance diagnostic radiology accuracy and improve patient care. Advanced features such as artificial intelligence integration, improved image resolution, and reduced radiation exposure are revolutionizing medical imaging capabilities. For instance, the introduction of the first fully mobile low-dose CT lung cancer screening program by the West Virginia University Health System, equipped with an AI-powered computed tomography scanner, demonstrates the industry's commitment to technological advancement and improved healthcare accessibility.

The evolution of CT technology has also led to the development of specialized systems with varying slice counts, from 16 to 320 slices, catering to different clinical needs. These advancements have enabled faster scan times, better image quality, and reduced radiation exposure, making CT scanning more efficient and safer for patients. The industry's focus on innovation is further demonstrated by the introduction of new features such as photon-counting CT scanners and advanced imaging analytics tools, which provide healthcare providers with more detailed and accurate diagnostic imaging information while maintaining patient safety and comfort.

Growing Healthcare Infrastructure and Investment

The robust healthcare infrastructure in the United States, supported by substantial investments in medical diagnostic equipment, continues to drive the computed tomography market forward. According to industry data, over 75 million CT scans are performed annually in the United States, highlighting the integral role of medical scanning in modern healthcare delivery. The presence of advanced healthcare facilities and the continuous expansion of imaging centers have created a strong foundation for market growth.

The healthcare sector's commitment to expanding access to advanced imaging services is evident through strategic partnerships and facility expansions. Major healthcare providers are increasingly investing in state-of-the-art CT equipment and establishing new imaging centers to meet growing patient needs. This infrastructure development is complemented by the presence of numerous diagnostic centers and specialized clinics, which collectively contribute to the market's expansion while ensuring widespread availability of CT scanning services across urban and rural areas.

Aging Population and Increasing Healthcare Needs

The demographic shift towards an aging population in the United States is significantly influencing the demand for computed tomography services. According to the Organisation for Economic Co-operation and Development data, individuals aged 65 and over constitute 16.89% of the total population, representing a substantial demographic requiring regular medical imaging services. This aging population is more susceptible to various health conditions, including cardiovascular diseases, orthopedic disorders, and cancer, driving the need for advanced diagnostic imaging.

The healthcare needs of the elderly population have led to increased utilization of CT scanning services across various medical specialties. The versatility of CT imaging in diagnosing age-related conditions, from cardiovascular diseases to orthopedic injuries, makes it an essential diagnostic tool in geriatric care. Healthcare providers are responding to this demographic trend by expanding their CT imaging capabilities and developing specialized protocols for elderly patients, ensuring comprehensive diagnostic services for this growing population segment.

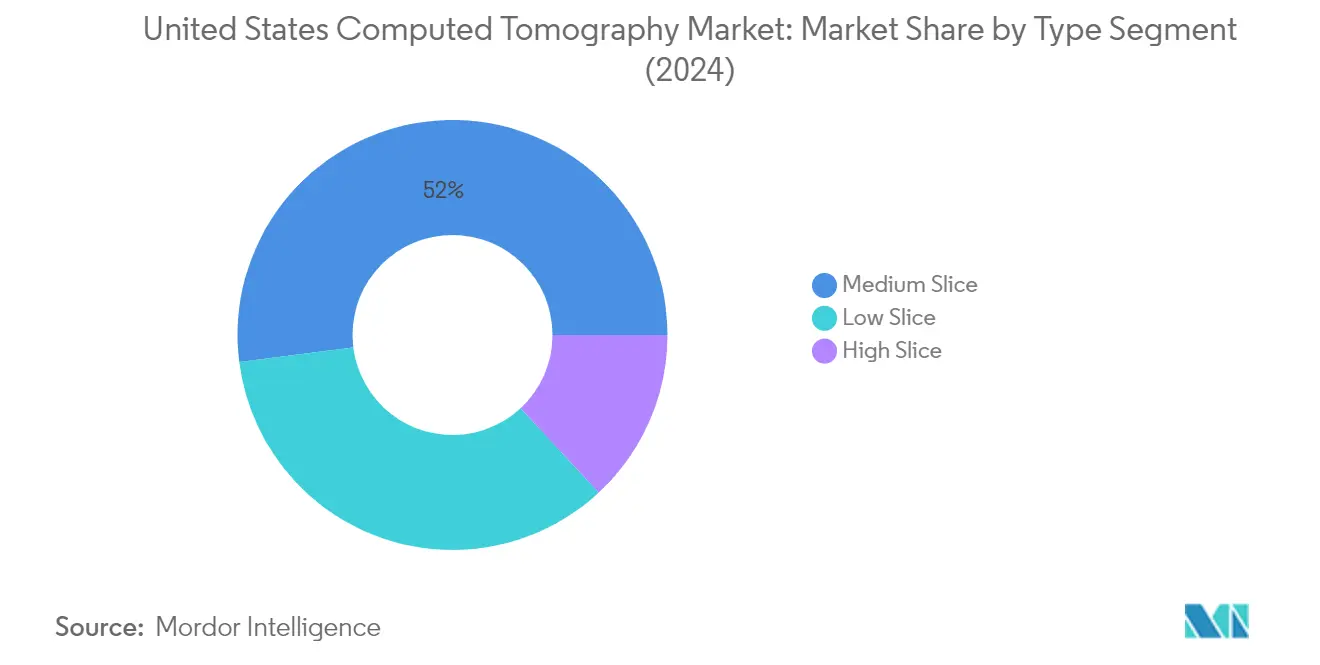

Segment Analysis: By Type

Medium Slice Segment in United States Computed Tomography Market

The Medium Slice segment, which includes 32-slice and 64-slice CT scanners, dominates the United States Computed Tomography market with approximately 52% market share in 2024. These systems are particularly valued for their versatility and optimal balance between imaging quality and cost-effectiveness. The 64-slice CT scanners within this segment are especially crucial as they provide physicians with enhanced visualization capabilities for soft tissue structures, tumors, and cysts, while also excelling in liver, lung, and coronary artery disease diagnosis. The segment's prominence is further strengthened by its ability to produce detailed cross-sectional images as thin as half a millimeter, ensuring highly accurate diagnostic imaging information. Additionally, these systems have demonstrated superior capabilities in handling patients with arrhythmias and various cardiovascular conditions, making them the preferred choice for both routine diagnostics and specialized cardiac CT imaging applications.

High Slice Segment in United States Computed Tomography Market

The High Slice segment, encompassing CT scanners with more than 128 slices, including 256, 320, and 640-slice variants, is experiencing significant growth in the United States market. This segment's expansion is driven by several technological advantages, including reduced scan times, increased patient throughput, and lower radiation doses. These advanced systems are particularly valuable for specialized applications in cardiology, neurology, oncology, gastroenterology, and pediatrics, offering non-invasive precise assessment capabilities. The segment's growth is further supported by its superior performance in handling challenging cases, including patients with obesity, pediatric patients who tend to move during scans, and those requiring advanced cardiovascular imaging. The enhanced imaging capabilities of high-slice systems, particularly in detecting micro-calcifications and providing more detailed anatomical information, make them increasingly essential for complex diagnostic imaging procedures and specialized medical applications.

Remaining Segments in CT Market by Type

The Low Slice segment, comprising 4 and 16-slice CT scanners, continues to play a vital role in the United States Computed Tomography market. These systems are particularly well-suited for higher-use facilities and everyday diagnostic imaging needs, especially in settings where scan time reduction is crucial. The 16-slice CT scanners have found their niche in urgent care centers and hospitals, offering a practical solution for routine imaging needs. While this segment may not lead in terms of technological sophistication, it maintains its relevance by providing cost-effective solutions for basic diagnostic imaging requirements, particularly in facilities that prioritize accessibility and operational efficiency over advanced imaging capabilities.

Segment Analysis: By Application

Oncology Segment in United States Computed Tomography Market

The oncology segment maintains its dominant position in the United States Computed Tomography market, accounting for approximately 30% of the total market share in 2024. This significant market share is primarily driven by the increasing adoption of CT scanning for cancer diagnosis, treatment planning, and monitoring treatment response. The segment's growth is further supported by technological advancements in CT imaging that enable more precise and early detection of various types of cancers. The rising investment in cancer research and development, particularly from the National Institutes of Health, continues to drive innovation in CT imaging applications for oncology. Additionally, the growing emphasis on preventive screening programs and the integration of artificial intelligence in CT-based cancer detection have strengthened the segment's market position.

Cardiovascular Segment in United States Computed Tomography Market

The cardiovascular segment is emerging as the fastest-growing application area in the United States Computed Tomography market, with an expected growth rate of approximately 6% during 2024-2029. This robust growth is primarily attributed to the increasing prevalence of cardiovascular diseases and the growing adoption of CT technology for cardiac CT imaging. The segment's expansion is further fueled by technological innovations in cardiac CT imaging, including the development of advanced visualization software and artificial intelligence-powered analysis tools. The rising demand for non-invasive diagnostic imaging procedures, coupled with the increasing awareness about early cardiovascular disease detection, is driving the adoption of cardiac CT scans. Moreover, the integration of CT imaging in emergency cardiac care and the development of specialized cardiac CT protocols are contributing to the segment's accelerated growth trajectory.

Remaining Segments in United States Computed Tomography Market by Application

The remaining segments in the market, including musculoskeletal, neurology, and other applications, continue to play vital roles in shaping the overall Computed Tomography landscape. The musculoskeletal segment maintains its strong presence due to the rising incidence of sports injuries and orthopedic conditions, while the neurology segment benefits from the increasing use of CT imaging in stroke diagnosis and neurological disorder assessment. The other applications segment, encompassing areas such as dental CT imaging and emergency medicine, contributes to market diversity through specialized CT applications. These segments are experiencing continuous technological improvements, including the integration of artificial intelligence and advanced visualization capabilities, which enhance their clinical utility and market relevance.

Segment Analysis: By End User

Hospitals Segment in United States Computed Tomography Market

The hospitals segment continues to dominate the United States Computed Tomography market, holding approximately 54% of the total market share in 2024. This significant market position is attributed to the robust healthcare infrastructure and the increasing adoption of advanced CT imaging technologies in hospital settings across the country. The segment's growth is primarily driven by the rising frequency of chronic diseases, growing elderly population requiring regular diagnostic imaging services, and the presence of better healthcare infrastructure in hospitals. According to recent healthcare statistics, the percentage of population aged 65 and over represents a significant portion of the total population in the United States, leading to increased demand for computed tomography services in hospitals. The segment's strong position is further reinforced by hospitals' ability to handle complex imaging procedures, their round-the-clock emergency services, and the integration of artificial intelligence technologies that automate and simplify time-consuming tasks, increasing operational efficiency and enabling more personalized patient care.

Diagnostic Centers Segment in United States Computed Tomography Market

The diagnostic centers segment is experiencing robust growth in the United States Computed Tomography market, with a projected growth rate of approximately 6% during 2024-2029. This impressive growth trajectory is driven by several key factors, including the increasing preference for outpatient diagnostic imaging services, shorter waiting times, and cost-effective imaging solutions. The segment's expansion is further supported by the rising prevalence of orthopedic diseases, cardiovascular disorders, and cancer, coupled with technological advancements in CT imaging. Diagnostic centers are increasingly adopting state-of-the-art CT scanning equipment and establishing partnerships with major healthcare providers to enhance their service offerings. The trend towards specialized imaging centers, particularly in urban and suburban areas, is contributing to the segment's growth, as these facilities focus on providing high-quality imaging services with reduced waiting times and more personalized attention to patients.

Remaining Segments in End User Market

The other end users segment, which includes ambulatory surgery centers (ASC), nursing homes, and specialty clinics, plays a vital role in the United States Computed Tomography market. These facilities are gaining prominence due to their ability to provide specialized care and convenient access to medical imaging services. Ambulatory surgery centers, in particular, are becoming increasingly popular as they offer outpatient procedures with minimal hospital stay requirements, thereby reducing overall treatment costs. Nursing homes and specialty clinics are also contributing to the market growth by providing dedicated imaging services for specific patient populations. The segment's importance is further emphasized by the growing trend towards outpatient care and the increasing preference for specialized medical facilities that can offer focused attention and expertise in specific areas of healthcare.

United States Computed Tomography Industry Overview

Top Companies in United States Computed Tomography Market

The United States computed tomography market features prominent players like GE Healthcare, Koninklijke Philips, Siemens Healthineers, Canon Medical Systems, and Fujifilm leading the competitive landscape. These companies are heavily investing in research and development to introduce innovative CT technologies, particularly focusing on AI-enabled clinical applications, improved image resolution, and reduced radiation exposure. The market is characterized by continuous product launches, with companies introducing advanced features like photon-counting detectors, spectral imaging capabilities, and intelligent software solutions. Strategic partnerships with healthcare providers and research institutions have become increasingly common, enabling companies to enhance their technological capabilities and expand market presence. Companies are also prioritizing operational efficiency through digital transformation initiatives and strengthening their service networks to provide comprehensive support to healthcare facilities.

Consolidated Market with Strong Global Players

The United States computed tomography market demonstrates a highly consolidated structure dominated by multinational conglomerates with diverse healthcare portfolios. These established players leverage their extensive research capabilities, robust distribution networks, and strong financial positions to maintain market leadership. The market exhibits significant barriers to entry due to high technological requirements, stringent regulatory standards, and substantial capital investments needed for product development and commercialization. Recent years have witnessed increased merger and acquisition activities, with larger companies acquiring specialized medical imaging technology firms to enhance their technological capabilities and expand their product offerings.

The competitive dynamics are shaped by the presence of both diversified healthcare technology companies and specialized medical imaging manufacturers. While global conglomerates like GE Healthcare and Siemens Healthineers benefit from their comprehensive healthcare solutions and established brand reputation, specialized players like Koning Corporation focus on developing niche technologies and innovative applications. The market has seen strategic collaborations between equipment manufacturers and healthcare providers, creating integrated solutions that combine imaging technology with clinical workflow optimization and data analytics capabilities.

Innovation and Integration Drive Market Success

Success in the computed tomography market increasingly depends on companies' ability to develop innovative technologies while ensuring cost-effectiveness and clinical value. Incumbent players are focusing on expanding their software capabilities, particularly in artificial intelligence and advanced visualization tools, to maintain their competitive advantage. The integration of CT systems with broader healthcare IT infrastructure and the development of specialized applications for different medical specialties have become crucial differentiators. Companies are also emphasizing the importance of user experience and workflow optimization, recognizing that operational efficiency and ease of use are significant factors in purchase decisions.

For emerging players and contenders, success lies in identifying underserved market segments and developing specialized solutions that address specific clinical needs. The growing emphasis on value-based healthcare creates opportunities for companies that can demonstrate superior clinical outcomes and cost-effectiveness. Regulatory compliance and quality assurance remain critical success factors, with companies needing to maintain robust quality management systems and stay ahead of evolving regulatory requirements. The increasing focus on radiation dose reduction and patient safety also influences competitive positioning, with companies investing in technologies that optimize image quality while minimizing radiation exposure. The role of medical diagnostic equipment in enhancing patient safety and clinical outcomes is becoming increasingly pivotal in this market.

United States Computed Tomography Market Leaders

-

Canon Medical Systems Corporation (Toshiba Corporation)

-

Koning corporation

-

GE Healthcare

-

Planmeca Group (Planmed OY)

-

Koninklijke Philips NV

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

United States Computed Tomography Market News

- In June 2022, Xoran Technologies, a United States-based company received a patent for a modular computed tomography (CT) system assembly. Together with our twenty and counting active patents, this ground-breaking cone beam CT arrangement opens up new possibilities. The innovation is just the start of a new line of point-of-care (POC) imaging equipment from Xoran.

- In March 2022, the OmniTom Elite from NeuroLogica Corp, a Samsung Electronics subsidiary, gained 510(k) approval. Without having to transfer essential patients to a different imaging department, the OmniTom Elite can deliver flexible, real-time mobile imaging to administer point-of-care CT.

United States Computed Tomography Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Diseases

- 4.2.2 Rising Geriatric Population

- 4.2.3 Increasing Technological Advancements

-

4.3 Market Restraints

- 4.3.1 Lack Of Proper Reimbursement And Stringent Regulatory Approval Procedures

- 4.3.2 High Cost of Equipment

-

4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

-

5.1 By Type

- 5.1.1 Low Slice

- 5.1.2 Medium Slice

- 5.1.3 High Slice

-

5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Neurology

- 5.2.3 Cardiovascular

- 5.2.4 Musculoskeletal

- 5.2.5 Other Applications

-

5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Centers

- 5.3.3 Other End Users

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Carestream Health

- 6.1.2 Canon Medical Systems Corporation (Toshiba Corporation)

- 6.1.3 Koning corporation

- 6.1.4 GE Healthcare

- 6.1.5 Neusoft Medical Systems Co. Ltd

- 6.1.6 Planmeca Group (Planmed OY)

- 6.1.7 Koninklijke Philips NV

- 6.1.8 Fujifilm Holdings Corporation

- 6.1.9 Siemens Healthineers AG

- 6.1.10 Stryker Corporation

- 6.1.11 Samsung Electronics Co., Ltd.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape Covers - Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

United States Computed Tomography Industry Segmentation

As per the scope of the report, computed tomography (CT) is an imaging process that customizes special X-ray equipment to generate a sequence of exhaustive images or scans of areas inside the body. It is also called computerized axial tomography (CAT) scanning, primarily used in cancer diagnosis. The United States Computed Tomography Market is segmented by Type (Low Slice, Medium Slice, and High Slice), Application (Oncology, Neurology, Cardiovascular, Musculoskeletal, and Other Applications), and End User (Hospitals, Diagnostic Centers, and Other End Users). The report offers the value (in USD million) for the above segments.

| By Type | Low Slice |

| Medium Slice | |

| High Slice | |

| By Application | Oncology |

| Neurology | |

| Cardiovascular | |

| Musculoskeletal | |

| Other Applications | |

| By End User | Hospitals |

| Diagnostic Centers | |

| Other End Users |

Need A Different Region or Segment?

Customize Now

United States Computed Tomography Market Research FAQs

How big is the United States Computed Tomography Market?

The United States Computed Tomography Market size is expected to reach USD 2.52 billion in 2025 and grow at a CAGR of 5.86% to reach USD 3.35 billion by 2030.

What is the current United States Computed Tomography Market size?

In 2025, the United States Computed Tomography Market size is expected to reach USD 2.52 billion.

Who are the key players in United States Computed Tomography Market?

Canon Medical Systems Corporation (Toshiba Corporation), Koning corporation, GE Healthcare, Planmeca Group (Planmed OY) and Koninklijke Philips NV are the major companies operating in the United States Computed Tomography Market.

What years does this United States Computed Tomography Market cover, and what was the market size in 2024?

In 2024, the United States Computed Tomography Market size was estimated at USD 2.37 billion. The report covers the United States Computed Tomography Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United States Computed Tomography Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

United States Computed Tomography Market Research

Mordor Intelligence provides a comprehensive analysis of the computed tomography (CT) industry, utilizing our extensive expertise in medical imaging and diagnostic radiology research. Our detailed report covers the entire spectrum of medical diagnostic equipment. This includes traditional computerized axial tomography and advanced 3D tomography systems. The analysis encompasses various technologies, including SPECT CT, PET CT, and CBCT (cone beam CT) systems. These insights are available in an easy-to-read report PDF format, ready for download.

The report offers stakeholders valuable insights into diagnostic imaging trends. It covers applications ranging from cardiac CT to dental CT and industrial CT implementations. Our analysis examines technological advancements in spiral CT, helical CT, and volumetric CT systems. We thoroughly evaluate medical scanning and radiological imaging developments. The comprehensive coverage of medical imaging technologies ensures that healthcare providers, manufacturers, and investors can make informed decisions based on detailed industry analysis and future market projections.