United States Commercial Vinyl Floor Covering Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

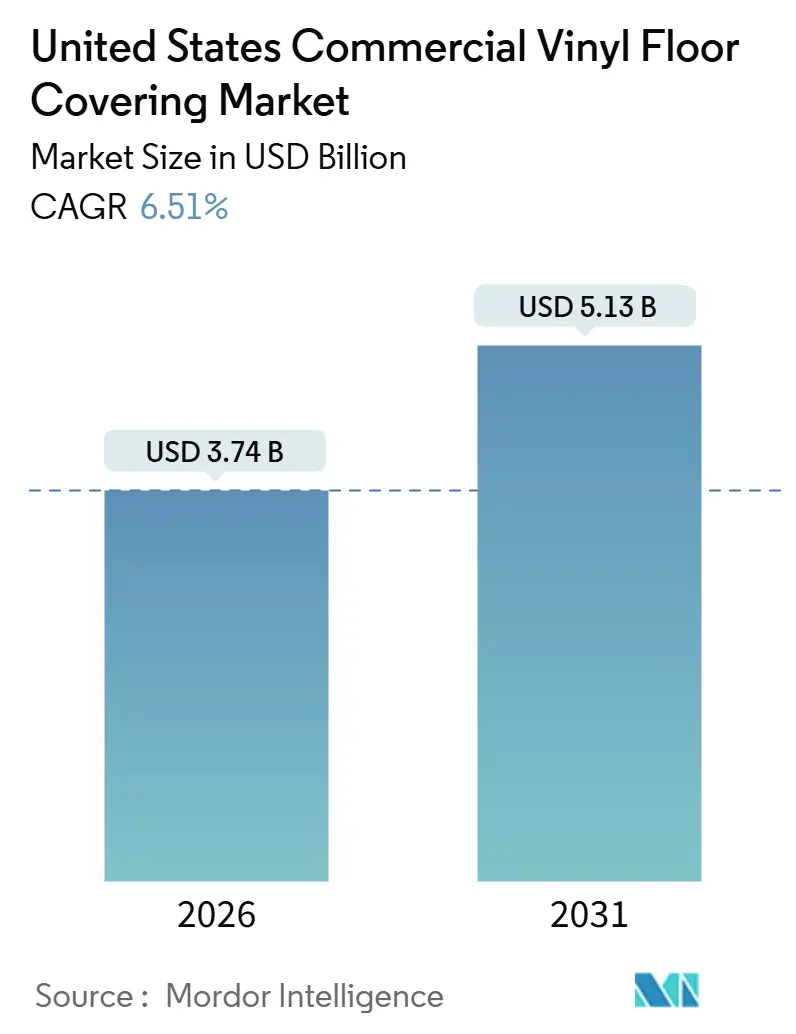

| Market Size (2026) | USD 3.74 Billion |

| Market Size (2031) | USD 5.13 Billion |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

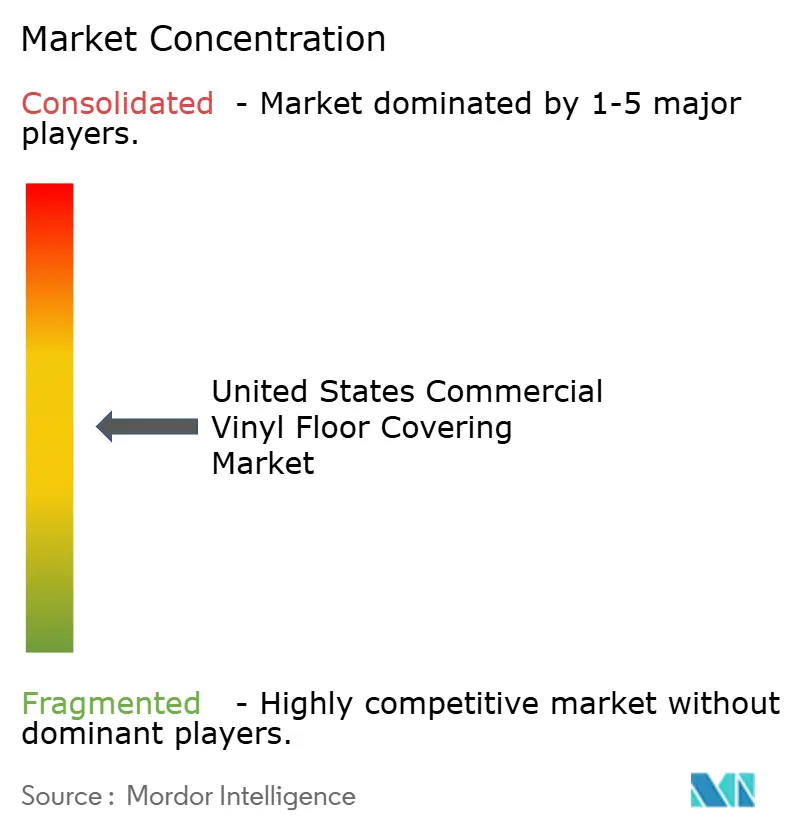

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Commercial Vinyl Floor Covering Market Analysis by Mordor Intelligence

The United States commercial vinyl floor covering market size stands at USD 3.74 billion in 2026 and is projected to reach USD 5.13 billion by 2031, reflecting a 6.51% CAGR through the forecast period. Renovation-led demand is stabilizing specification pipelines as owners upgrade legacy facilities to meet indoor air quality targets and lifecycle cost goals, even as some new-build categories experience mixed momentum. Domestic capacity additions are reshaping sourcing decisions as buyers balance tariff exposure against delivery reliability and documentation requirements under forced labor enforcement. Product innovation is unlocking higher-value specifications in healthcare, education, and hospitality, where performance, maintenance, and emissions credentials shape procurement outcomes. Certification programs and evolving air quality standards are reinforcing low-emission resilient options in clinical and public spaces, while channel strategies continue to blend distributor expertise with digital tools for smaller retrofits.

Key Report Takeaways

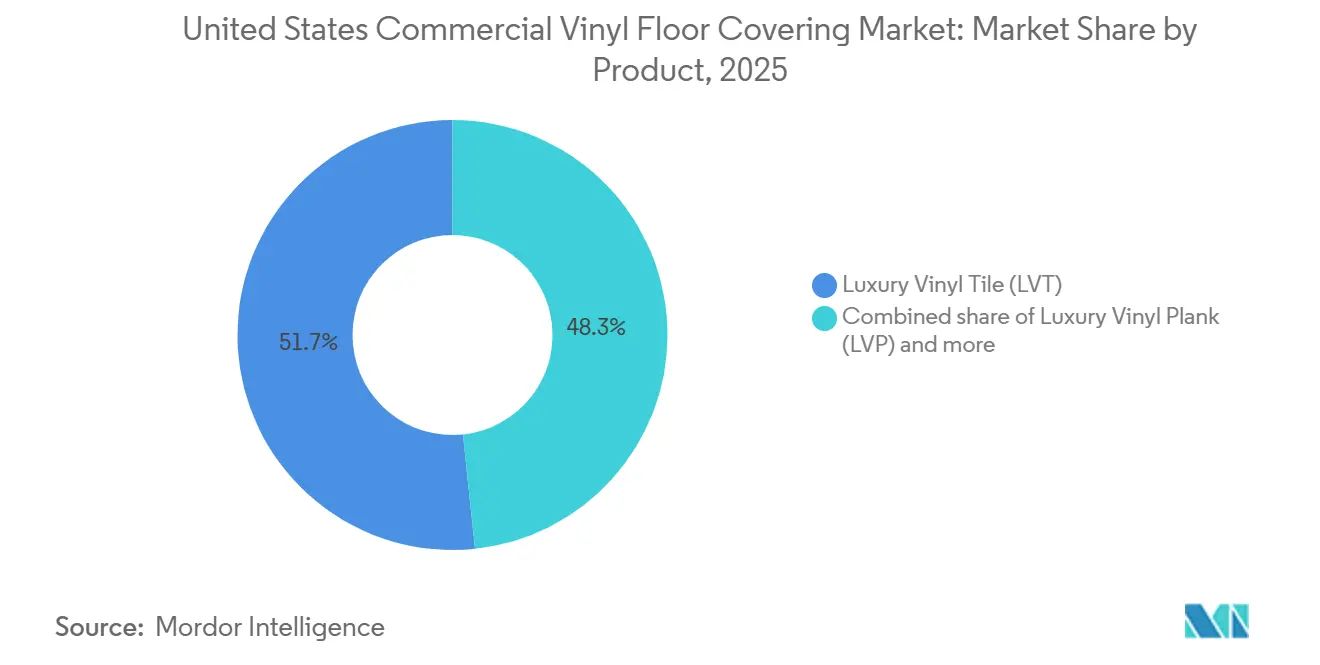

- By product type, luxury vinyl tile led with 51.67% of the United States commercial vinyl floor covering market share in 2025 and is forecast to expand at a 9.65% CAGR through 2031.

- By installation method, glue-down held 53.26% of the United States commercial vinyl floor covering market size in 2025, while interlocking vinyl tiles are the fastest growing at an 8.77% CAGR through 2031.

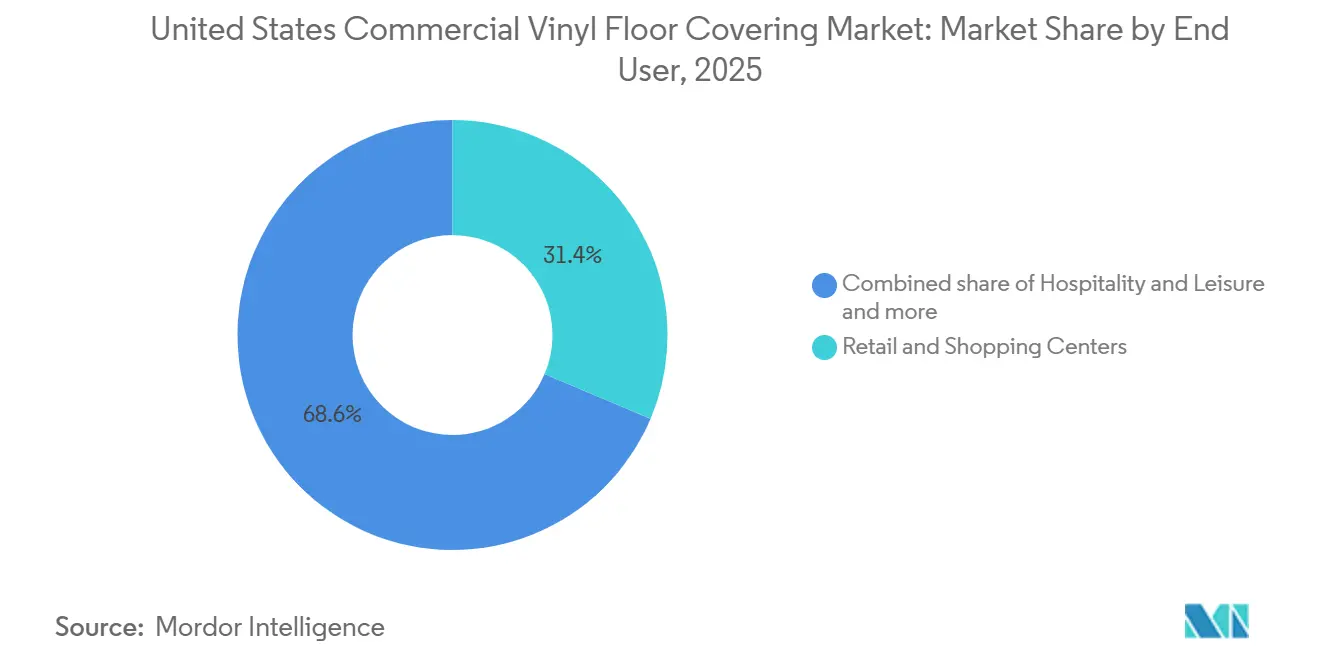

- By end user, retail and shopping centers commanded 31.37% of the United States commercial vinyl floor covering market share in 2025, and hospitality and leisure is projected to post the highest growth at a 9.98% CAGR through 2031.

- By construction type, new construction accounted for 64.35% of the United States commercial vinyl floor covering market share in 2025, and remodeling or retrofit activity is set to grow at a 9.24% CAGR through 2031.

- By distribution channel, specialized distributors and dealers held 72.38% of the United States commercial vinyl floor covering market share in 2025, and online or e-commerce platforms are expected to expand at a 9.64% CAGR through 2031.

- By geography, the Southeast led with 26.35% of the United States commercial vinyl floor covering market share in 2025, while the West is the fastest growing with an 8.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Commercial Vinyl Floor Covering Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming commercial renovation demand | +1.8% | National, with early gains in the Northeast retrofit corridors | Medium term (2-4 years) |

| Accelerating adoption of LVT/LVP for aesthetics and speed | +2.3% | National, strongest in Southeast retail and hospitality hubs | Short term (≤ 2 years) |

| Durable, low-maintenance floors in high-traffic venues | +1.5% | National, concentrated in the Midwest healthcare and education clusters | Medium term (2-4 years) |

| Shift to PVC-free rigid-core ahead of EPA review | +0.6% | West Coast, with spillover to the Northeast | Long term (≥ 4 years) |

| Antimicrobial and acoustic surfaces for IAQ mandates | +1.2% | National, acute in Southeast and West healthcare expansion markets | Short term (≤ 2 years) |

| Increasing Demand for Durable and Low-Maintenance Flooring Solutions | +2.3% | National, with heightened demand in Midwest healthcare facilities and Southeast retail corridors | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Booming Commercial Renovation Demand

The United States commercial construction spending experienced volatility in 2025, with retrofit programs supporting replacement cycles as owners preferred fast-install solutions for occupied spaces. Census data showed an 8.2% year-over-year decline in commercial categories in July 2025, driving a shift toward retrofits that reduce downtime and labor complexity. Institutional stakeholders anticipate measured growth into 2026, with architects projecting cautious improvement in resilient flooring demand. The United States commercial vinyl floor covering market benefits from click-fit rigid core and sheet solutions, which minimize disruption in healthcare upgrades and public facilities. Procurement decisions remain focused on balancing speed, emissions credentials, and lifecycle costs amid financing-sensitive planning cycles.

Accelerating Adoption of LVT and LVP for Aesthetics and Speed

Manufacturers are increasing the United States' capacity with investments in rigid core construction, advanced texturing, and rapid installation systems to address schedule and labor constraints. Shaw’s USD 90 million expansion in Ringgold, Georgia, enhances SPC and LVT output, emboss textures, and dimensional stability for loose-lay performance in fast-paced commercial settings. Digital print resolution and PVC-free products meet demands for durability, design variation, and low emissions within short installation windows. These innovations drive competitiveness in the United States commercial vinyl floor covering market, where specifiers prioritize speed, fewer pattern repeats, and strong wear layers for retail, office, and hospitality. Certifications and FloorScore testing ensure suitability for sensitive environments.

Preference for Durable, Low-Maintenance Floors in High-Traffic Venues

Healthcare, education, and public facilities require surfaces that tolerate frequent cleaning, rolling loads, and high foot traffic while maintaining hygiene and air quality standards. Clinical environments combine ventilation requirements with surface choices that reduce pathogen persistence and support cleaning protocols that are consistent with nursing and infection prevention guidance. Resilient floors that meet low-emission benchmarks and come with relevant certifications are helping facility teams comply with procurement checklists tied to LEED, WELL, and school facilities programs. In the United States commercial vinyl floor covering market, sheet and homogeneous vinyl continue to defend share in rooms where seams and transitions must be minimized, and rigid core options are expanding in corridors and common areas when fast turnover is critical. Product families supported by credible indoor air quality testing and health-oriented certifications align with post-pandemic requirements in public-facing venues.

Shift Toward PVC-Free Rigid-Core in Anticipation of EPA Vinyl-Chloride Review

Corporate sustainability goals and product stewardship are driving PVC-free resilient platforms with circular designs and take-back programs. Shaw’s EcoWorx Resilient exemplifies this trend, offering recyclability and a verified carbon profile aligned with green building standards. Flooring companies are advancing digital designs and eco-friendly chemistries, reducing environmental impact. Specifiers prioritize compliance with Title VI for composite wood, emphasizing credible documentation. In the United States commercial vinyl floor covering market, emissions credentials and circular end-of-life solutions are key differentiators. Projects also value antimicrobial and acoustic features for IAQ and occupant comfort. Resilient surfaces meeting air quality, noise, and durability standards remain crucial, especially in clinics and classrooms with frequent renovations[1]SCSGLOBALSERVICES.COM https://www.scsglobalservices.com/middle-east/services/floorscore..

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PVC-resin and additive price volatility | -0.7% | National, acute pressure in regions dependent on imported feedstock | Short term (≤ 2 years) |

| Tightening United States VOC and sustainability rules | -0.5% | California, and OTC states in the Northeast and Mid-Atlantic | Long term (≥ 4 years) |

| Tariffs and forced-labor import restrictions | -1.2% | National, most severe for importers reliant on China and Vietnam supply | Short term (≤ 2 years) |

| Shortage of skilled glue-down installers | -0.8% | National, most acute in rural Midwest and Southeast counties | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PVC-Resin and Additive Price Volatility

Raw material costs remain a budgeting headwind for resilient flooring procurement, and producers continue to calibrate price lists to reflect input and logistics dynamics. Large United States manufacturers have communicated steps to defend margins and cash flow through footprint optimization, product mix shifts, and pricing actions where necessary. Buyers prioritize stable lead times and transparent surcharges, and several domestic players positioned their portfolios as a more predictable option during periods of currency and freight variability. The United States commercial vinyl floor covering market is also seeing specification guardrails that reduce installation waste and extend lifecycles, which helps offset material inflation with lower maintenance and fewer replacements. As pricing signals evolve, supply agreements that balance cost stability with service levels are becoming central to long-horizon projects in public and private sectors.

Tariff and Forced-Labor Import Restrictions Disrupting Supply Chains

Forced labor enforcement has tightened import scrutiny for products linked to high-risk regions, leading buyers to favor vetted suppliers and domestic production where documentation is clearer. Federal agencies reported significant escalations in enforcement and detentions under the Uyghur Forced Labor Prevention Act, motivating supply chain shifts and more rigorous material traceability. In parallel, Canada imposed 25% tariffs on a defined list of United States products, including selected floor coverings, starting February 2025, highlighting a bilateral trade friction that procurement teams monitor when placing cross-border orders. Flooring groups with domestic capacity and transparent sourcing have sought to differentiate on reliability and lead time stability as import risk increased. The United States commercial vinyl floor covering market continues to adapt through supplier diversification, more direct OEM relationships, and closer alignment with compliance programs across vendor networks[2]CANADA.CA https://www.canada.ca/en/department-finance/news/2025/02/list-of-products-from-the-united-states-subject-to-25-per-cent-tariffs-effective-february-4-2025.html..

Segment Analysis

By Product Type: Rigid Core Leads as Sheet Solutions Hold Clinical Ground

Luxury vinyl tile (LVT) accounts for 51.67% of 2025 demand and is expected to grow at 9.65% through 2031, driven by rigid core formats in retail, office, and hospitality projects requiring quick installation and durability. Advanced printing and texturing enhance LVT’s premium appeal in high-traffic venues. Sheet vinyl remains vital in clinical settings, minimizing seams and ensuring cleanliness for infection control. In the United States, LVT dominates image-sensitive upgrades, with wood visuals, large formats, and easy replacement boosting tenant satisfaction. Certified low emissions and LEED or WELL documentation are now standard in institutional bids.

Domestic capacity expansions improve lead times and product variety for rigid core families. United States investments in SPC and LVT cater to hospitality and retail owners managing heavy loads and frequent updates. PVC-free resilient platforms and circular design commitments are driving material health goals. Homogeneous and specialty solutions are defending critical zones like operating rooms and clean corridors, balancing rapid installation, emissions compliance, and total ownership costs across diverse building types.

Note: Segment shares of all individual segments available upon report purchase

By Installation Method: Interlocking Formats Gain Momentum on Labor and Schedule Needs

Glue-down installations accounted for 53.26% of demand in 2025, while interlocking vinyl tiles are projected to grow at 8.77% through 2031. Click-fit systems address schedule compression and installer availability, enabling faster room turnover, lower odor profiles, and phased work in occupied retrofits. Healthcare and food service sectors rely on glue-down sheets for monolithic performance and consistent adhesion under frequent cleaning. The United States commercial vinyl floor covering market is shifting toward a mix of loose-lay and locking systems for renovations, with glue-down remaining essential for clinical and heavy-wet zones. New-build projects often combine methods, with installers chosen based on traffic, substrate, and maintenance needs.

Domestic manufacturing investments focus on interlocking and rigid core lines. Plant upgrades add emboss-in-register textures and stability layers, enhancing loose-lay performance in high-use areas. Modularity supports targeted replacements after localized damage without adhesives. The industry balances practical installation, emissions compliance, and sound control. Click-lock adoption is expected to grow in offices, retail conversions, and hospitality renovations, prioritizing quick reopening.

By End User: Retail Holds Share, Hospitality and Healthcare Drive Upgrades

Retail and shopping centers dominate with a 31.37% share in 2025, driven by the adoption of rigid core and resilient formats to manage heavy foot traffic and daily cleaning. Hospitality is expected to grow the fastest at 9.98% through 2031, as hotels upgrade with durable, moisture-resistant wood-like visuals. Healthcare focuses on emissions, cleanability, and monolithic installations in critical areas, aligning with infection control and ventilation standards. Education facilities favor resilient solutions for high-use areas like corridors and cafeterias, prioritizing maintenance simplicity and lifecycle costs. The United States commercial vinyl floor covering market reflects these trends, with sector-specific demands for installation speed, air quality, and service life.

Hospitals and schools emphasize low-emission certifications and products that withstand frequent disinfection without intensive polishing, contributing to building program credits. Hotels prioritize quick room turnovers and modular replacements, while retailers balance design consistency with impact and scratch resistance in high-traffic zones. The United States market adapts with differentiated sub-families, including LVT, sheet, and specialty resilient options, to meet diverse end-user needs. Vendors offering strong documentation, sample support, and installation guidance are well-positioned to compete in these segments.

Note: Segment shares of all individual segments available upon report purchase

By Construction Type: Retrofit Gains Share While New Builds Remain Foundational

New construction accounted for 64.35% of 2025 activity, while remodeling and retrofitting are projected to grow at 9.24% through 2031 as owners focus on adaptive reuse and modernization. Uneven momentum across commercial categories in 2025 highlights the need for targeted upgrades to reduce downtime and retain tenants. Retrofit projects favor interlocking and loose-lay options for quick installations, while healthcare and industrial new builds rely on glue-down sheet and homogeneous solutions for performance. The United States commercial vinyl floor covering market balances fast-cycle retrofits with steady new-build pipelines, tailoring product and method choices to project requirements.

Increased SPC and LVT output from domestic plants improves availability for renovation-heavy customers and reduces lead time risks. Suppliers offer flexible color and pattern options with service programs that meet brand standards, enabling multi-site owners to maintain visual consistency during phased updates. These capabilities are critical for retail and hospitality renovations. Investments in speed and low-emission solutions for occupied retrofits further strengthen the market, helping procurement teams align product selection with schedules and lifecycle goals.

By Distribution Channel: Specialized Distributors Hold Share as Digital Complements Grow

Specialized distributors and dealers held a 72.38% share in 2025, driven by the need for technical support, submittal management, and installer networks in complex projects and institution-led procurements. Direct sales channels cater to large accounts requiring design services, factory support, and reliable delivery schedules. E-commerce is projected to grow at 9.64% through 2031, supported by smaller retrofit jobs and tenant improvements, where click systems and virtual visualization simplify selection and installation. The United States commercial vinyl floor covering market integrates digital tools to accelerate discovery and sampling for targeted projects while maintaining high-touch distribution. Documentation-heavy projects still rely on distributors for emissions, safety, and compliance submissions.

Manufacturers are enhancing turnkey support to complement distributor capabilities. Custom color labs and national installer programs align with chains seeking brand-directed specifications and consistent field performance. Domestic footprints mitigate cross-border logistics and tariff risks, with companies promoting this stability as a value proposition. Incremental channel shifts are expected as digital ordering grows for smaller projects, while large institutional and enterprise projects favor specialist-led coordination. Combining online sampling with on-site technical advisory proves most effective for complex bids.

Geography Analysis

The Southeast accounted for 26.35% of regional demand in 2025, driven by healthcare, logistics, and industrial programs. It remains a key destination for resilient specifications in new builds and retrofits. Projects in Florida, Georgia, and the Carolinas combine public and private work, leveraging resilient flooring for durability and low maintenance. Despite office submarket vacancies, healthcare and public spaces continued specifying sheet and LVT for performance. Regional investments favor United States-made options, prioritizing lead time and compliance. Domestic capacity expansions align with project pipelines, emphasizing speed, consistency, and certified emissions testing.

The West is projected to grow at an 8.84% CAGR through 2031, supported by sustainability goals, data center infrastructure, and public-private upgrades. California’s focus on emissions and material health drives demand for low-emission, resilient, and PVC-free options with credible certifications. Manufacturers with sustainable platforms and take-back programs gain traction in LEED and wellness-focused projects. The United States commercial vinyl floor covering market benefits from these mandates, with owners seeking products meeting strict documentation and performance standards. Regional portfolios, including hospitality and public infrastructure upgrades, prioritize quick installations and predictable maintenance.

The Midwest and Northeast maintained steady institutional volume in 2025, led by education, healthcare, and public projects emphasizing lifecycle value and air quality. Growth pockets are expected into 2026, with public agencies prioritizing emissions-tested, resilient surfaces. These regions prefer products with clear installation guidance, durable wear layers, and verified documentation to meet procurement standards. Owners and specifiers align platform choices with program goals, balancing acoustic comfort, cleanability, and budgets. Established suppliers with credible testing and environmental claims are favored, reducing risks in large public and institutional bids[3]American Institute of Architects, “January 2025 Consensus Construction Forecast,” American Institute of Architects, aia.org.

Competitive Landscape

The United States commercial vinyl floor covering market is driven by major players leveraging manufacturing scale, diverse brand portfolios, and multi-channel strategies, including distributors, direct enterprise accounts, and digital sampling. Companies are increasing domestic SPC and LVT production to enhance availability and reduce import reliance amid forced-labor enforcement and tariff fluctuations. Emphasis on PVC-free options, circular programs, and carbon transparency aligns with sustainability goals. The market prioritizes design versatility, quick installation, and compliance documentation, favoring firms that integrate innovation, supply chain resilience, and verified credentials for institutional and hospitality projects.

Shaw's USD 90 million investment in its Ringgold, Georgia, plant will double SPC and LVT capacity by 2026, adding embossing and stability features for improved loose-lay performance. Manufacturers are advancing PVC-free platforms, with Shaw’s EcoWorx Resilient earning the 2025 Edison Award for circular design innovation[4]Shaw Industries, “EcoWorx Resilient Flooring Receives 2025 Edison Award for Innovation,” Shaw Industries, shawinc.com. Flooring companies are enhancing print resolution, surface protection, and manufacturing processes to extend wear life and reduce environmental impact. These efforts strengthen credibility with owners seeking low-maintenance solutions and verified emissions, particularly in clinical and educational settings. Suppliers combining speed, durability, and environmental performance are gaining market preference.

Leading brands are focusing on cost management and portfolio optimization. Mohawk implemented structural savings and margin protection measures, while others reported slight regional softness but steady North American activity. Channel strategies now pair full-service distributors with digital sampling and color customization to address complex institutional bids and smaller retrofits. Vendors refining price-value propositions and expanding service offerings to mitigate project risks are well-positioned. Companies maintaining domestic production, robust documentation, and reliable delivery retain competitive advantages in bids emphasizing compliance, scheduling, and emissions.

United States Commercial Vinyl Floor Covering Industry Leaders

Mohawk Industries

Shaw Industries Group

Armstrong Flooring

Tarkett SA

Mannington Mills

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EcoWorx Resilient flooring by Shaw Industries, recognized for its circular design, won the 2025 Edison Award. This PVC-free, fully recyclable platform features a documented embodied carbon profile.

- October 2024: Shaw Industries is investing USD 90 million in Plant RP, Ringgold, Georgia, to expand SPC and LVT resilient flooring capacity by 2026. The project will introduce new emboss textures and enhance dimensional stability for loose-lay applications.

United States Commercial Vinyl Floor Covering Market Report Scope

The United States commercial vinyl floor covering market refers to resilient flooring solutions designed for use in high-traffic commercial environments such as retail, hospitality, healthcare, education, and public infrastructure. The market is driven by demand for durable, low-maintenance, and design-flexible products, with increasing emphasis on sustainability, PVC-free alternatives, and performance features such as antimicrobial and acoustic enhancements.

The market is segmented by product type, installation method, end user, construction type, distribution channel, and geography. By product type, it includes luxury vinyl tile (LVT) with subcategories such as stone plastic composite (SPC) and wood plastic composite (WPC), luxury vinyl plank (LVP), sheet vinyl, and other formats, including VCT and resilient vinyl-backed rubber hybrids. By installation method, the market covers self-adhesive vinyl tiles, glue-down, interlocking vinyl tiles, and other installation techniques. By end user, the market spans hospitality and leisure, retail and shopping centers, healthcare facilities, education, corporate offices, public and government buildings, and other commercial users. By construction type, the market is divided into new construction and remodeling or retrofit activity. By distribution channel, the market includes direct sales from manufacturers to contractors or end-users, specialized distributors and dealers, and online or e-commerce platforms. By geography, the market is segmented into the Northeast, the Midwest, the Southeast, the Southwest, and the West.

The report provides market size and forecasts in value (USD) for all these segments, along with insights into trends, innovations, regulatory frameworks, competitive dynamics, and future opportunities shaping the United States commercial vinyl floor covering industry.

| Luxury Vinyl Tile (LVT) | Stone Plastic Composite (SPC) |

| Wood Plastic Composite (WPC) | |

| Luxury Vinyl Plank (LVP) | |

| Sheet Vinyl | |

| Others (VCT, Resilient Vinyl-Backed Rubber Hybrid) |

| Self-Adhesive Vinyl Tiles |

| Glue-Down |

| Interlocking Vinyl Tiles |

| Others |

| Hospitality & Leisure |

| Retail & Shopping Centers |

| Healthcare Facilities |

| Education |

| Corporate Offices |

| Public & Government Buildings |

| Other Commercial Users |

| New Construction |

| Remodeling / Retrofit |

| Direct Sales (Manufacturer to Contractor/End-User) |

| Specialized Distributors & Dealers |

| Online / E-commerce Platforms |

| Northeast |

| Midwest |

| Southeast |

| Southwest |

| West |

| By Product Type | Luxury Vinyl Tile (LVT) | Stone Plastic Composite (SPC) |

| Wood Plastic Composite (WPC) | ||

| Luxury Vinyl Plank (LVP) | ||

| Sheet Vinyl | ||

| Others (VCT, Resilient Vinyl-Backed Rubber Hybrid) | ||

| By Installation Method | Self-Adhesive Vinyl Tiles | |

| Glue-Down | ||

| Interlocking Vinyl Tiles | ||

| Others | ||

| By End User | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Remodeling / Retrofit | ||

| By Distribution Channel | Direct Sales (Manufacturer to Contractor/End-User) | |

| Specialized Distributors & Dealers | ||

| Online / E-commerce Platforms | ||

| By Geography | Northeast | |

| Midwest | ||

| Southeast | ||

| Southwest | ||

| West |

Key Questions Answered in the Report

What is the current size and growth outlook of the United States commercial vinyl floor covering market?

The United States commercial vinyl floor covering market size is USD 3.74 billion in 2026 and is projected to reach USD 5.13 billion by 2031 at a 6.51% CAGR, supported by renovation-led demand and domestic capacity expansion.

Which product types are leading specifications across commercial buildings in the United States?

Luxury vinyl tile leads with a 51.67% share in 2025 and is forecast to grow at 9.65% through 2031 as rigid core platforms gain traction in retail, office, and hospitality upgrades.

How are installation methods evolving in U.S. commercial projects?

Glue-down remains prevalent with 53.26% in 2025 for clinical and heavy-use zones, while interlocking tiles are the fastest growing at 8.77% as owners favor quick-turn retrofits that minimize downtime.

Which end users are driving demand for resilient flooring in the United States?

Retail and shopping centres lead at 31.37% of 2025 demand, and hospitality is expected to grow the fastest at 9.98% through 2031, with healthcare and education maintaining steady specifications tied to emissions and cleanability.

How are compliance and sustainability influencing specifications in the United States?

Low-emission certifications like FloorScore and PVC-free resilient platforms with circular design are increasingly favoured in healthcare, education, and high-performance buildings with LEED and wellness goals.

What regions present the strongest opportunities for the United States commercial vinyl floor covering market?

The Southeast leads with a 26.35% share, and the West is the fastest growing with an 8.84% CAGR, driven by sustainability mandates, data centre infrastructure, and ongoing upgrades across public and private assets.