US Cold Chain Logistics Top Companies

-

FedEx Logistics

-

XPO Logistics

-

CH Robinson Worldwide

-

Expeditors

-

Americold Logistics

*Disclaimer: Top companies sorted in no particular order

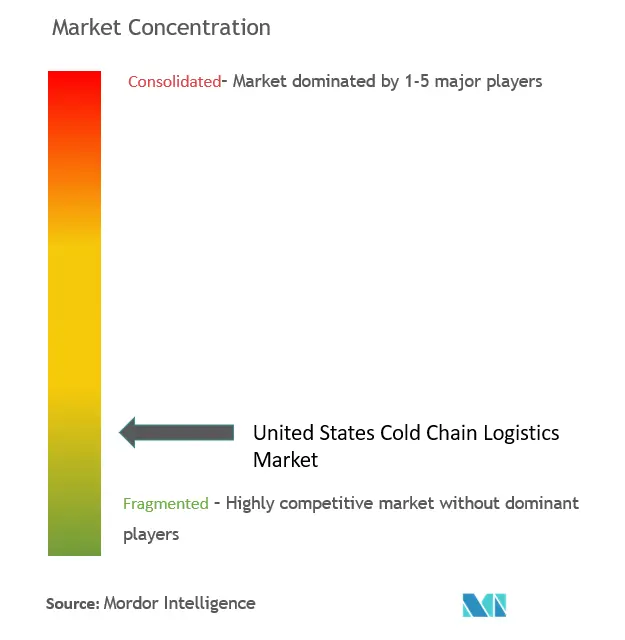

US Cold Chain Logistics Market Concentration

US Cold Chain Logistics Company List

-

FedEx

-

XPO Logistics

-

CH Robinson Worldwide

-

JB Hunt

-

Expeditors

-

Total Quality Logistics

-

Americold Logistics

-

Burris Logistics

-

Prime Inc.

-

Lineage Logistics

-

Arc Best

-

Stevens Transport

-

DHL Supply Chain

-

United States Cold Storage

-

DB Schenker

-

Covenant Transportation Services*

Specific to US Cold Chain Logistics Market

Need More Details On Market Players And Competitors?

Download PDF