Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 97.13 Billion |

| Market Size (2031) | USD 133.87 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Cold Chain Logistics Market Analysis by Mordor Intelligence

The US Cold Chain Logistics Market size is estimated at USD 97.13 billion in 2026, and is expected to reach USD 133.87 billion by 2031, at a CAGR of 6.63% during the forecast period (2026-2031).

Automation roll-outs, pharmaceutical temperature-control sophistication, and stricter sustainability mandates are reshaping network design, capital allocation, and service differentiation. Traditional food-focused operators face margin compression as energy costs rise, while specialized pharmaceutical logistics providers command premium pricing by offering ultra-low-temperature capabilities with near-zero tolerance for excursions. Surface transportation remains dominant for food volumes, yet airfreight demand is accelerating where cell and gene therapies require overnight delivery and cryogenic handling. Regional shifts are equally notable, with the Southeast maintaining the largest capacity base, the Southwest emerging as a high-growth nexus tied to US-Mexico trade, and rail-integrated inland hubs gaining favor as shippers hedge against trucking volatility.

Key Report Takeaways

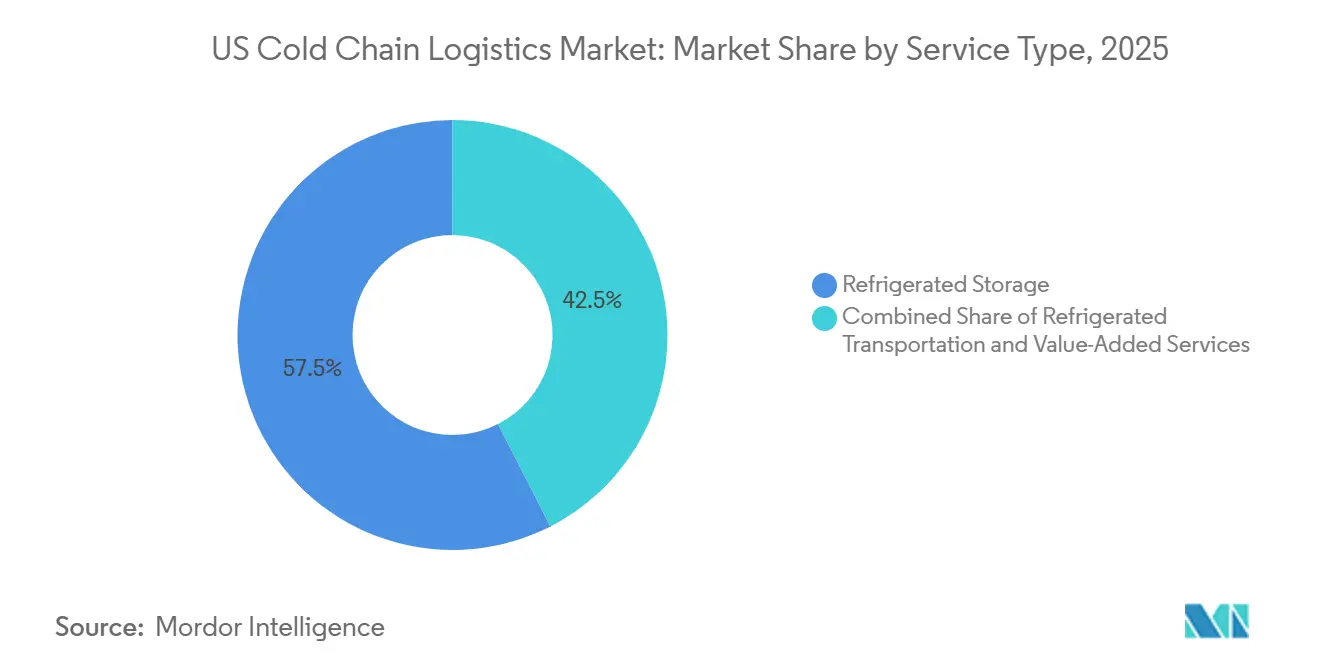

- By service type, refrigerated storage held 57.53% of the US cold chain logistics market share in 2025, while air transportation is forecast to post the fastest 13.23% CAGR through 2031.

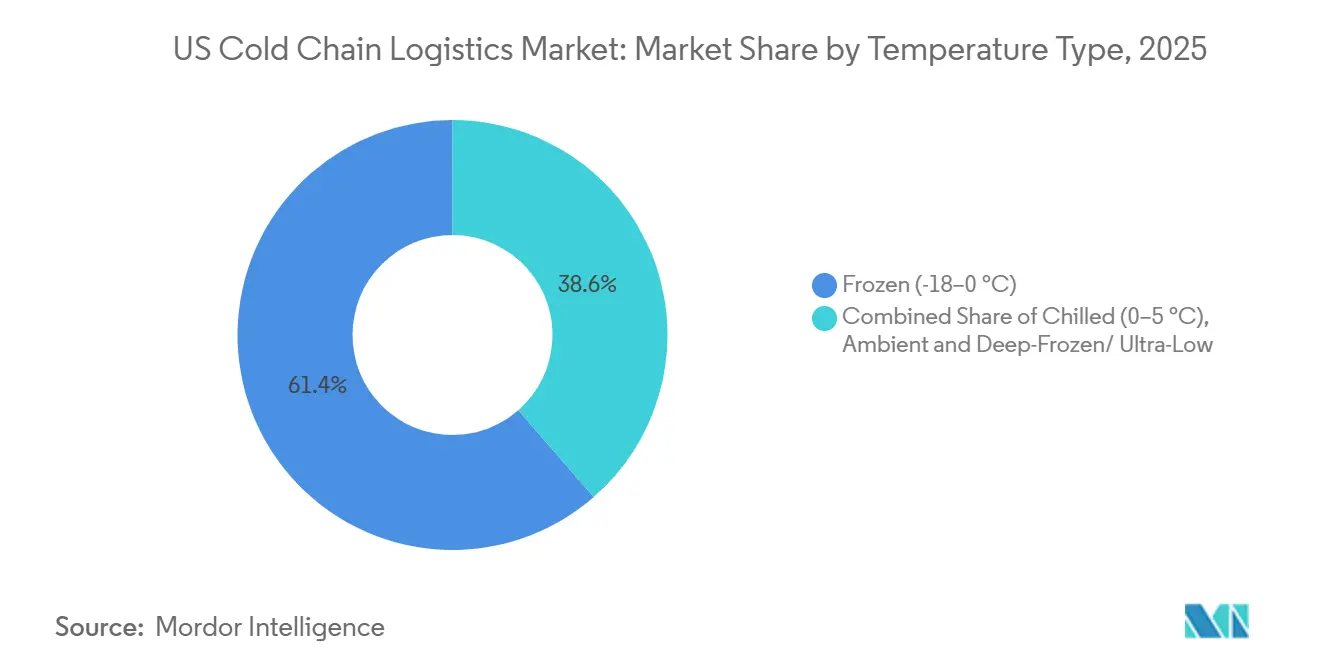

- By temperature band, the frozen segment accounted for 61.42% of the US cold chain logistics market size in 2025, whereas deep-frozen and ultra-low storage is projected to expand at an 11.87% CAGR to 2031.

- By application, meat and poultry led with 22.63% of the US cold chain logistics market size in 2025; vaccines and clinical trial materials record the highest projected 14.11% CAGR through 2031.

- By region, the Southeast captured 34.17% of the US cold chain logistics market share in 2025, while the Southwest is advancing at an 11.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-grocery & Meal-Kit Volumes Surge | +1.6% | National, concentrated in the top 50 metro areas | Medium term (2-4 years) |

| Pharma Biologics & Cell-Gene Therapy Boom | +1.9% | Northeast corridor, expanding to Southeast | Long term (≥ 4 years) |

| Port-Adjacent Automated Mega-Warehouses | +1.2% | Gulf Coast, Pacific Northwest, Mid-Atlantic | Long term (≥ 4 years) |

| Rail-Integrated Inland Cold Hubs (CPKC) | +0.8% | Midwest, Southwest | Medium term (2-4 years) |

| ESG-Linked Financing Accelerates Upgrades | +0.7% | National | Medium term (2-4 years) |

| USDA Food-Waste Mandate Pressure | +0.5% | National, strongest in California | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Grocery and Meal-Kit Volumes Surge

Online grocery penetration reached 17% of food retail in 2025, and temperature-controlled last-mile delivery complexity expanded faster than ambient e-commerce[1].Prologis, “The E-commerce Boom Isn’t Over,” prologis.com Individual order dispersion across neighborhoods is forcing micro-fulfilment centers with multi-zone rooms to locate within 10 miles of dense households, inflating real-estate costs in urban cores where vacancy stands near 6.9%. Meal-kit providers add sequencing pressure by cross-docking frozen proteins, chilled produce, and ambient items inside four-hour windows to meet delivery promises. Together, these models lift demand for flexible, small-footprint facilities that can pick, pack, and dispatch within narrow cut-offs. Operators able to integrate route optimization software with real-time refrigeration monitoring have captured new contracts, even as profit margins tighten for legacy facilities lacking value-added capabilities. Growth remains strongest in the top 50 metro areas, reinforcing a hub-and-spoke distribution build-out rather than national uniformity.

Pharma Biologics and Cell-Gene Therapy Boom

Personalized medicines such as CAR-T require point-to-point cryogenic transport, validated storage below -150 °C, and rapid release back to treatment centers, shifting emphasis from bulk storage to patient-specific orchestration. DHL’s commitment to invest EUR 1 billion (USD 1.17 billion) in healthcare logistics across the Americas by 2030 underscores the profitability of premium temperature-controlled lanes. The economic calculus differs from food: a single deviation can erase USD 500,000 in biologics value, compared to USD 5,000 for produce. Consequently, shippers prioritize redundant power, real-time telemetry, and chain-of-custody blockchain, selecting providers on compliance record rather than lowest rate. Capacity shortfalls in Boston, Philadelphia, and Raleigh have spurred speculative ultra-low builds despite 3-4× higher construction costs, signaling sustained demand tailwinds.

Port-Adjacent Automated Mega-Warehouses

Automation and proximity to seaports are converging as developers erect facilities exceeding 500,000 ft² with AS/RS capable of handling 10,000-plus pallet slots under multiple temperature regimes. Lineage’s USD 40 million investment in two automated Gulf Coast complexes demonstrates labor arbitrage benefits near ports where wage premiums for sub-zero work top 30% and turnover eclipses 40% annually. Port adjacency trims dwell time for seafood and produce imports, improving shelf life and lowering demurrage. For operators, the model unlocks power-optimization through dense racking and reduces headcount by up to 70%, keeping operating cost per pallet competitive despite higher capital outlay. Automation readiness is becoming a prerequisite for securing ESG-linked financing that discounts interest rates for demonstrable energy savings.

Rail-Integrated Inland Cold Hubs

Canadian Pacific Kansas City’s intermodal network now offers door-to-door refrigerated container service from Mexican farms to Midwest hubs at a 30-40% cost advantage over trucking, albeit with two-day longer transit windows suited to frozen cargos. Facilities adjoining rail sidings require dedicated lifts, genset charge points, and throughput scales that few mid-sized operators can afford, creating natural entry barriers. Shippers accept modest latency to secure rate stability amid driver shortages and diesel volatility. As volumes scale, inland hubs in Kansas City and San Antonio gain critical mass, diversifying geographic capacity away from coastal bottlenecks. This modal shift supports regional cold chain resilience but demands close inventory management to reconcile slower freight cycles with retail replenishment rhythms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HFC Phase-Down Retrofit Costs | -1.1% | National, acute in the Northeast and the Midwest | Medium term (2-4 years) |

| Labor Scarcity in Sub-Zero Operations | -0.8% | National, the most severe in the Southwest and Southeast | Short term (≤ 2 years) |

| Power-Price Volatility Risk | -0.6% | Texas, California, Northeast | Medium term (2-4 years) |

| Port & Canal Climate Disruptions | -0.4% | Gulf Coast, Mid-Atlantic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HFC Phase-Down Retrofit Costs

EPA rules compel operators to replace high-GWP refrigerants such as R-404A, raising conversion costs to USD 2-4 million per site while production caps tighten 40% by 2028[2]IIAR, “HFC Phase-Down Guidance,” iiar.org. Facilities constructed in the 2000s retain useful structural life yet face escalating refrigerant prices that have tripled since 2024. Smaller owners struggle to amortize engineering studies and downtime, accelerating consolidation as they exit scale players who spread costs across multiple locations. Retrofit timing also collides with broader capacity expansion plans, forcing capital rationing and delaying other modernization projects.

Labor Scarcity in Sub-Zero Operations

Turnover in freezer zones exceeds 40% annually as workers endure -20 °C environments; wage premiums expanded from 15% in 2020 to nearly 30% by 2025, surpassing productivity gains. Automation mitigates handling but cannot replace maintenance, quality, and dock functions requiring human intervention. The scarcity intensifies in high-growth Sun Belt markets like Phoenix and Dallas, where worker familiarity with deep-freeze conditions is limited. Training costs and attrition squeeze margins, prompting operators to pilot augmented-reality maintenance aids and heated PPE to improve retention.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Automation Reshapes Storage Economics

Refrigerated storage captured 57.53% of the US cold chain logistics market share in 2025, reflecting the pivotal role fixed infrastructure plays in linking producers and consumers. Within this segment, automated public warehouses are gaining share as food companies outsource specialists who distribute fixed costs across multiple tenants. Private storage remains critical for pharmaceuticals, where compliance and security justify single-tenant models. Road transport retains volume leadership, yet capacity headwinds from driver shortages and fuel volatility are steering long-haul frozen goods toward rail-intermodal solutions that offer 30-40% savings. Airfreight’s 13.23% CAGR through 2031 embodies a parallel network optimized for high-value, low-volume therapies that tolerate neither delay nor temperature deviation, cementing premium yields for carriers and handlers. Value-added services - kitting, labeling, and quality testing - have grown by double digits, diversifying revenue streams beyond storage and haulage.

Automation’s impact is multifaceted. Facilities employing AS/RS systems operate with up to 70% fewer floor workers and deliver higher throughput per ft³, mitigating wage inflation and labor scarcity. Energy efficiency gains of 10-15% stem from compact racking and reduced infiltration. As a result, investors funnel capital toward projects exceeding 40 million ft³, supported by ESG-linked financing. Conversely, legacy manual facilities struggle to fund HFC conversions and technology retrofits, pushing industry consolidation as scale operators acquire sub-scale warehouses to redevelop them into automated nodes.

By Temperature Type: Ultra-Cold Drives Investment

The frozen band (-18 °C to 0 °C) accounted for 61.42% of the US cold chain logistics market size in 2025, anchoring traditional frozen food distribution. Operators face rising energy costs and refrigerant phase-down expenses, prompting trials of a “3-degree shift” to -15 °C that promises 10–15% power savings while maintaining food safety[3]Food Logistics, “3-Degree Shift in Frozen Storage,” foodlogistics.com. Chilled storage (0–5 °C) supports fresh produce and dairy with faster turnover and higher spoilage sensitivity, demanding granular demand forecasts and just-in-time replenishment.

Deep-frozen and ultra-low facilities below -20 °C are projected to grow at 11.87% CAGR as mRNA vaccines and cell therapies proliferate. These sites demand redundant cascade refrigeration, liquid nitrogen backups, and validated monitoring systems, driving capital intensity to three times conventional frozen builds. Capacity bottlenecks in biotech corridors have inflated lease rates by 40% versus food-grade space. Ambient-controlled rooms (15-25 °C) are a modest but rising niche for products like chocolate and specialty chemicals, offering energy savings but requiring dehumidification and tight thermal envelopes to avoid excursions.

By Application: Pharmaceutical Premium Pricing

Meat and poultry led with 22.63% share in 2025, leveraging well-established farm-to-retail corridors and specialized blast-freezing infrastructure. Growth, however, moderates as consumers pivot toward fresh and prepared alternatives, curbing utilization in facilities dependent on bulk frozen protein. Fish and seafood benefit from aquaculture imports routed through Gulf Coast ports, necessitating port-adjacent cold storage equipped for rapid transloading and repackaging. Dairy and frozen desserts maintain resilient demand, though rising plant-based alternatives call for distinct temperature and humidity regimes.

Vaccines and clinical trial materials, advancing at a 14.11% CAGR through 2031, now form a parallel premium tier in the US cold chain logistics market size. GDP-compliant providers command lease rates up to USD 22 per ft² in Boston compared to USD 8-12 for food-grade space, reflecting the value at risk. Fruits and vegetables logistics are evolving under federal food-waste targets that push for ethylene-scrubbing systems and IoT freshness sensors. Ready-to-eat meals ride meal-kit demand, necessitating multiproduct assembly lines within temperature-graded docks. Specialty chemicals represent a stable, smaller slice, but their stringent temperature windows make them sticky clients for compliant operators.

Geography Analysis

The Southeast dominated with 34.17% market share in 2025, driven by Latin American produce inflows via Florida, seafood through Gulf ports, and Georgia’s poultry processing base. Population migration into Atlanta, Charlotte, and Nashville is fueling retail cold chain expansion, while hurricane risk spurs investment in elevated structures, hurricane-rated cladding, and on-site generators. Lease rates and land values have climbed as operators compete for infill plots capable of two-hour e-commerce delivery.

The Southwest is projected to expand at an 11.02% CAGR to 2031, anchored by Texas, where cross-border nearshoring, population growth, and petrochemical demand converge. Laredo and El Paso crossings channel increasing refrigerated cargo from Mexican produce regions. Grid instability under ERCOT forces developers to budget USD 3-5 million for redundant power systems on top of standard construction costs. Phoenix and Tucson serve as fast-growing secondary nodes, yet water scarcity raises long-term sustainability questions for desert agriculture feeding these facilities.

The Northeast hosts the densest concentration of biotech and pharmaceutical firms, making Boston, New Jersey, and Philadelphia epicenters for ultra-low-temperature projects with lease premiums exceeding USD 20 per ft². Aging infrastructure in the Midwest, where Illinois and Wisconsin house major meat and dairy processors, requires simultaneous refrigerant retrofits and automation upgrades, straining capital budgets. The West remains a study in contrast: California’s robust agricultural output and Asia-facing ports propel demand, yet aggressive environmental regulations and peak-power pricing challenge operator economics. Public grants such as the California Energy Commission’s retrofit funding mitigate some capital pressure, signaling a policy environment that rewards early adopters of natural refrigerants.

Regulatory Landscape

US cold chain logistics operations are governed by FDA requirements under the Food Safety Modernization Act (FSMA), including the Sanitary Transportation of Human and Animal Food provisions (21 CFR Part 1, Subpart O). These rules cover shipper and carrier responsibilities, sanitary equipment conditions, and temperature-control procedures during transit. A major compliance milestone occurred on January 20, 2026, when FDA's Food Traceability Final Rule (21 CFR Part 1, Subpart S) compliance deadline took effect for foods on the Food Traceability List, tightening recordkeeping and systems integration requirements around critical tracking events and key data elements across cold storage and transportation handoffs.

Beyond food safety, operators also align with international and domestic equipment standards for perishable transport. USDA Agricultural Marketing Service involvement in ATP-related certification can apply to international perishable movements. At the federal logistics level, the Department of Transportation's supply chain resilience work, including data-driven bottleneck programs such as FLOW, increases scrutiny of dwell times and infrastructure constraints at ports and inland nodes that affect temperature-controlled freight performance. This reinforces the shift toward auditable visibility and standardized data exchange across the cold chain.

Value Chain Analysis

The US cold chain value chain begins with producers and processors (including meat, poultry, dairy, seafood, produce, and pharma manufacturers) moving temperature-sensitive goods into pre-cooling, consolidation, and packaging steps. For pharma, this can also include qualified packout and chain-of-custody controls. Goods then pass through refrigerated storage (public and dedicated/private), cross-docking, and value-added services such as blast freezing, labeling, kitting, inspection, and quality holds, before entering refrigerated transportation via road (dominant for domestic food flows), rail intermodal for longer-haul frozen lanes, and air for high-value, time-critical biologics.

Port terminals, reefer container availability, and drayage handoffs can add dwell time and increase excursion risk when monitoring and appointment discipline are weak. Asset owners and operators, including large national warehouse platforms, compete alongside 3PLs, parcel integrators, and specialty healthcare logistics providers. The competitive emphasis is shifting toward data visibility, exception management, and validated processes, not capacity alone. Industry coordination bodies such as the Global Cold Chain Alliance provide technical guidance and advocacy, while US DOT supply chain initiatives focus on diagnosing freight bottlenecks that can cascade into cold chain disruptions. Recent capital strategies also point to platform scaling through partnerships, including Americold's May 2026 USD 1.3 billion joint venture with EQT to own and operate cold storage facilities across North America.

Competitive Landscape

Lineage Logistics and Americold collectively control a majority of national refrigerated warehouse cubic footage, establishing quasi-oligopolistic leverage in key metros. Their scale enables multi-facility customer contracts, diversified energy hedging, and accelerated automation rollouts, creating cost positions smaller competitors cannot match. Second-tier operators respond by specializing: some pivot to GDP-compliant pharma services, others serve ethnic food distributors requiring bespoke handling, and a few focus on last-mile urban facilities where mega-warehouse footprints are impractical.

Technology adoption delineates winners from laggards. Leading providers deploy IoT telemetry, machine-learning demand forecasts, and blockchain traceability, providing clients with shipment-level visibility that reduces spoilage claims. The Global Cold Chain Alliance reported its members expanded capacity to 8.16 billion ft³ in 2025, yet the number of operators shrank, illustrating capacity growth via consolidation rather than new entrants[4]Global Cold Chain Alliance, “2025 Global Top 25 List,” gcca.org . Parcel integrators UPS and FedEx are investing heavily in healthcare cold chain lanes, leveraging existing air networks to offer end-to-end solutions that traditional warehouse operators struggle to match. Private-equity funding remains active, channeling capital into greenfield mega-projects in port and inland rail nodes, further intensifying competition for mid-tier independents.

US Cold Chain Logistics Industry Leaders

Lineage Logistics Holdings, LLC

Americold Logistics, LLC

United States Cold Storage, Inc.

Interstate Warehousing

FreezPak Logistics

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Automation-led capacity additions and upgrades are a concrete whitespace as operators look for productivity gains amid labor scarcity and high energy intensity. The recent project mix shows where capital is concentrating: NewCold's February 2026 Phase 3 expansion announcement in Lebanon, Indiana (USD 500 million, automation-led), its fully automated frozen facility opening at McDonough, Georgia (125,000 pallet positions), and Lineage's March 2026 completion of an 84,000-square-foot expansion in Louisville, Kentucky (about 10,400 pallet positions). Together, these projects point to sustained demand for high-throughput, multi-tenant and dedicated networks that reduce manual handling, improve inventory accuracy, and support tighter cutoffs for retail and foodservice replenishment.

Opportunity is also emerging through investment structures that combine institutional funding with operational execution. Americold's May 2026 USD 1.3 billion joint venture with EQT, covering 12 US facilities (about 124 million cubic feet and over 400,000 pallet positions), illustrates a model where capital targets cold storage as mission-critical infrastructure while established operators run day-to-day activities. On the demand side, large-format, dedicated distribution builds, such as H-E-B's July 2026 plan advancement for a USD 175 million refrigerated warehouse at its San Antonio campus, indicate ongoing network build-out around high-growth population corridors and border-adjacent trade lanes. Compliance and refrigerant transition requirements add another modernization track, since EPA actions under the AIM Act and FSMA traceability obligations increase the value of operators that can pair refrigeration upgrades with digital traceability, telemetry, and auditable cold chain controls.

Recent Industry Developments

- June 2026: Americold opened an integrated cold chain import-export hub at Port Saint John in New Brunswick, developed with DP World and Canadian Pacific Kansas City (CPKC). The site links port operations with rail connectivity and temperature-controlled handling, tightening the interface between international trade gateways and inland distribution for perishable cargo.

- May 2026: Americold announced a USD 1.3 billion North American cold storage joint venture with EQT, contributing 12 facilities totaling about 124 million cubic feet and over 400,000 pallet positions into the platform. The structure pairs institutional capital with an established operator model, supporting portfolio scale and facility modernization while managing balance-sheet intensity.

- May 2025: Lineage Logistics announced a USD 1 billion expansion with Tyson Foods, adding 49 million ft3 via acquisition and committing to two automated builds totaling 80 million ft3. The move strengthened Lineage's ability to serve high-volume protein supply chains and accelerated automation deployment to offset labor constraints in sub-zero operations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers paid logistics services that keep goods within a controlled temperature range during storage, handling, and transportation inside the United States, including related value-added cold handling.

Scope exclusions: We exclude dry-ice courier parcels handled only within hospital campuses.

Segmentation Overview

- By Service Type

- Refrigerated Storage

- Refrigerated Transportation

- Road

- Rail

- Sea

- Air

- Value-Added Services

- By Temperature Type

- Chilled (0–5 °C)

- Frozen (-18–0 °C)

- Ambient

- Deep-Frozen / Ultra-Low (More than 20 °C)

- By Application

- Fruits & Vegetables

- Meat & Poultry

- Fish & Seafood

- Dairy & Frozen Desserts

- Bakery & Confectionery

- Ready-to-Eat Meals

- Pharmaceuticals & Biologics

- Vaccines & Clinical Trial Materials

- Chemicals & Specialty Materials

- Other Perishables

- By Region (United States)

- Northeast

- Midwest

- Southeast

- Southwest

- West

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping the cold chain footprint in the United States and linking it to measurable activity in food, life sciences, and temperature-sensitive chemicals. To anchor the demand side, we referred to public series and guidance from sources such as the USDA and FDA, along with data from the US Census Bureau, the Bureau of Transportation Statistics, and the Energy Information Administration for freight and operating context.

We then cross-checked service intensity and mix using sources such as trade association publications, carrier and warehouse operator filings, investor presentations, and reputable press coverage of capacity additions and network expansions. Where it helped validate company scale and shipment exposure, we also used paid subscriptions focused on company financials and intelligence, as well as shipment-level import and export tracking for cold-handled commodities. The desk sources listed here are illustrative, and many other public and paid references were used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with refrigerated warehouse operators, temperature-controlled carriers, 3PLs, shippers, and cold chain packaging and monitoring participants, so we could test pricing, utilization, and service mix assumptions. Since this is a US-only market, coverage was balanced across major production and consumption corridors, and insights were re-checked across food and beverage and life sciences demand patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 19% | |

| Mid tier: 45% | Functional/Unit leaders: 27% | |

| Smaller Players: 21% | Managers: 54% |

Market-Sizing & Forecasting

Sizing used a top-down build where the cold chain demand pool was reconstructed from temperature-sensitive throughput and freight activity, and then translated into service revenues through observable rate and mix assumptions. To keep it practical, we used check calculations in parallel, such as sampled warehouse revenue per pallet position, lane-based refrigerated transport spend checks, and ASP times volume approximations for key service lines, and totals were adjusted when gaps appeared.

Inputs that mattered most included refrigerated warehouse capacity additions and utilization ranges, reefer truck and trailer availability signals, typical storage and handling rate progression, fuel and electricity cost pass-through behavior, and the share of perishable and pharma volumes that require controlled-temperature handling versus ambient alternatives. Forecasting relied mainly on scenario analysis tied to expected shifts in food distribution patterns, life sciences shipment growth, and cost-driven pricing behavior, with assumptions confirmed and tempered through expert feedback. Where bottom-up checks could not cover smaller regional operators, we filled gaps using modeled revenue per facility and per mile benchmarks that were validated through interviews.

Data Validation & Update Cycle

Outputs were checked against independent signals, such as cold storage capacity trends, freight activity indicators, and observed pricing movement, and then reviewed for outliers by a second analyst before sign-off. When a result moved too far from these external anchors, we re-opened the drivers, re-tested assumptions with follow-up calls, and corrected the model before freezing the final number.

Reports are refreshed annually, and interim updates are made when material events occur, such as major capacity openings, sharp energy or fuel shifts, or regulatory actions that change handling practices. Before delivery, a fresh data pass is completed so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's United States Cold Chain Logistics Market Size Versus Other Published Estimates

Published market sizes for US cold chain logistics can vary widely, even when the topic sounds identical, because the scope lines and revenue capture rules are not the same. Differences usually come from what is counted as logistics revenue, how storage versus transport is bundled, and which years and pricing assumptions are used.

The main gap comes from whether value-added cold services and multi-mode refrigerated moves are included as part of logistics spend, where Mordor Intelligence counts these only when they are delivered as paid, third-party cold chain services within the United States and tied to measured throughput and rate checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 97.13 B (2026) | |

| Industry Association A | USD 85.00 B (2024) | Often reflects member-reported refrigerated warehousing and selected handling fees, which can undercount outsourced refrigerated transport spend and cross-service bundling, and it may not normalize rates to a single pricing period. |

| Trade Journal B | USD 116.85 B (2024) | Commonly applies broader cold chain definitions that blend logistics with adjacent categories like cold storage real estate or equipment-related revenues, and may use aggressive price escalation without matching it to utilization and throughput checks. |

The spread in the table is explained mostly by what gets treated as logistics revenue versus adjacent cold chain activity, and by how pricing is carried forward between years. By tying the total to repeatable operating drivers like capacity, utilization, service mix, and rate movement, the estimate stays traceable and easier to re-check as market conditions change.

Key Questions Answered in the Report

How large is the US cold chain logistics market in 2026?

It reached USD 97.13 billion in 2026 and is forecast to grow to USD 133.87 billion by 2031.

Which service type leads the US cold chain logistics market?

Refrigerated storage held a 57.53% share in 2025, underpinned by its role as the primary buffer between production and retail.

What is the fastest-growing temperature band?

Deep-frozen and ultra-low storage below -20 °C is projected to post an 11.87% CAGR through 2031, driven by mRNA vaccines and cell therapies.

Which region is expanding most rapidly?

The Southwest, led by Texas, is advancing at an 11.02% CAGR to 2031 owing to cross-border trade and population growth.

Who are the dominant players?

Lineage Logistics and Americold control a majority of national refrigerated warehouse capacity, creating a quasi-duopoly in many metros.

Page last updated on: