United States Car Loan Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 595.19 Billion |

| Market Size (2030) | USD 898.25 Billion |

| Growth Rate (2025 - 2030) | 5.28% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Car Loan Market Analysis by Mordor Intelligence

The United States car loan market stood at USD 595.19 billion in 2025 and is forecasted to reach USD 898.25 billion by 2030, advancing at a 5.28% CAGR. Sustained demand for passenger vehicles, the rapid shift toward digital origination, and expanding captive-lender programs underpin this growth. Artificial-intelligence underwriting is lifting approval rates for underserved borrowers and trimming processing costs, while federal and state incentives for electric vehicles (EVs) are lowering default risk and unlocking new product niches. Consolidation is accelerating across banks and fintechs as scale and data depth become decisive competitive advantages. On the risk side, sticky prime rates, rising delinquencies on ultra-long loans, and tightening capital rules compel lenders to refine pricing, shorten loan terms, and strengthen collections.

Key Report Takeaways

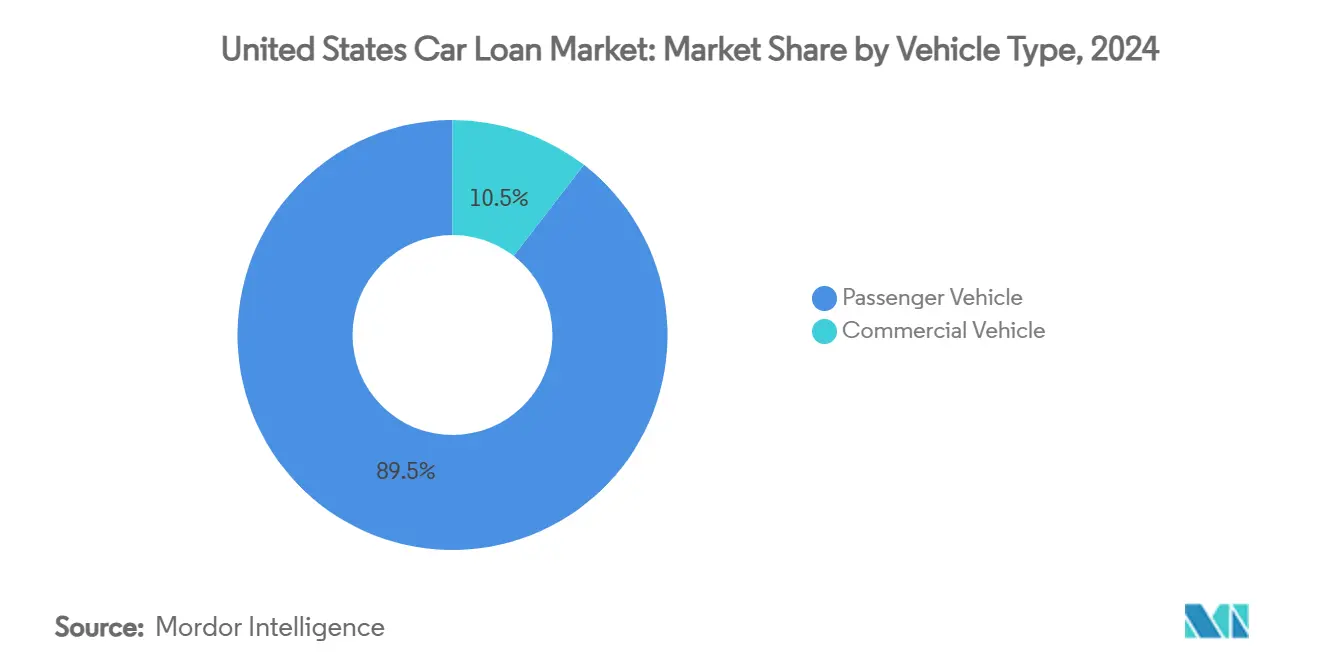

- By vehicle type, passenger vehicles led with an 89.53% share of the United States car loan market in 2024 and are projected to expand at a 5.77% CAGR through 2030.

- By ownership, used vehicles accounted for 63.12% of the United States car loan market share in 2024, and are forecasted to grow at a 6.68% CAGR to 2030.

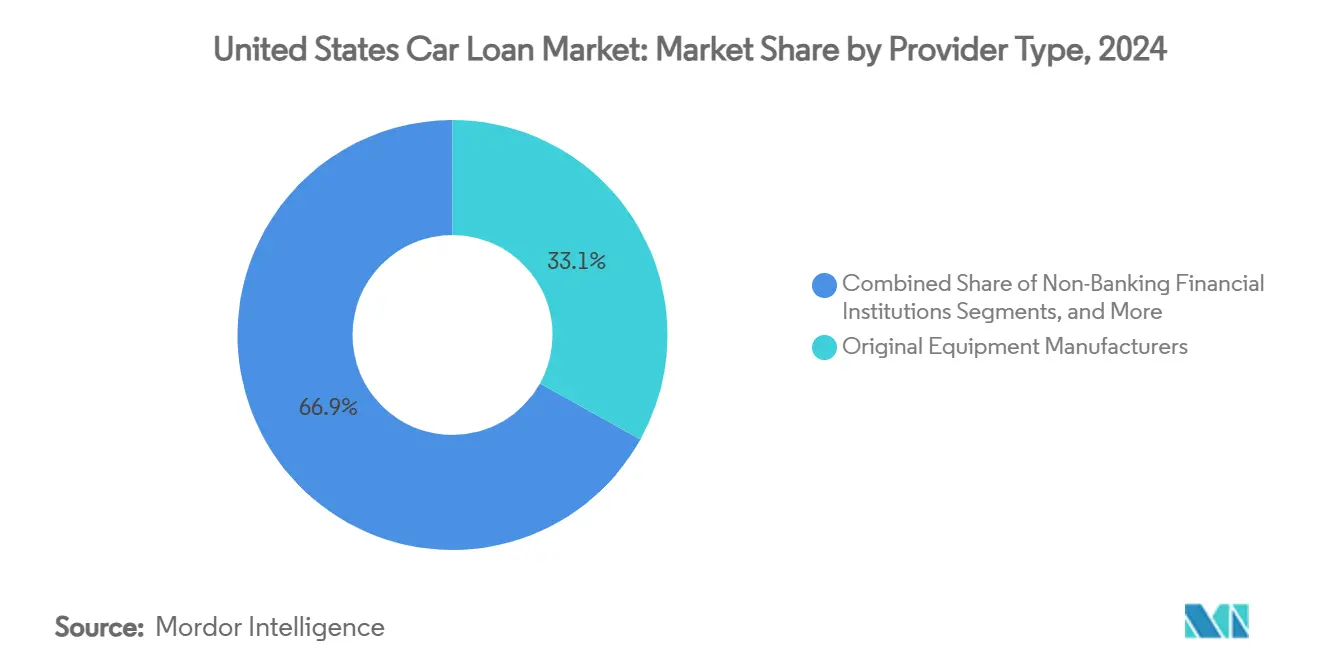

- By provider type, original equipment manufacturers held 33.07% of the United States car loan market in 2024; fintech lenders recorded the fastest 12.79% CAGR over 2025-2030.

- By tenure, loans longer than 5 years represented 53.32% of the United States car loan market size in 2024; loans shorter than 3 years are growing at a 7.12% CAGR.

United States Car Loan Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in captive-lender penetration post-inventory rebound | +0.8% | National, concentrated in OEM strongholds | Medium term (2-4 years) |

| Growing EV financing incentives & green-loan tax credits | +0.6% | National, early gains in California, Texas, Florida | Long term (≥ 4 years) |

| Digitization of loan origination & AI-driven underwriting | +0.9% | National, led by metropolitan areas | Short term (≤ 2 years) |

| Credit-union shift toward indirect auto lending | +0.4% | Regional, strongest in Midwest and Southeast | Medium term (2-4 years) |

| Used-car price volatility widening refinance volumes | +0.7% | National, amplified in high-cost coastal markets | Short term (≤ 2 years) |

| OEM subscription & buy-back guarantees lowering residual-value risk | +0.5% | National, pilot programs in urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in captive-lender penetration post-inventory rebound

Captive finance arms regained momentum as dealership inventory normalized, allowing promotional APRs that drove their share of new-vehicle funding to 58% in Q3 2024. Ford Credit will deploy a data-driven insights platform in 2025 to sharpen pricing and retention. General Motors’ choice to pause a bank-charter pursuit lets GM Financial focus capital on rate-subsidized programs, sustaining its edge. Competitive pressure pushes banks and credit unions to differentiate through faster approval cycles rather than lower rates. As OEM inventories rise, captives can selectively scale back incentives, protecting margins while holding volume leadership.

Growing EV financing incentives & green-loan tax credits

Federal tax credits extended under the Inflation Reduction Act and layered state rebates cut effective borrowing costs for qualifying EV buyers[1]U.S. Department of Energy, “Alternative Fuels Data Center,” energy.gov. EV borrowers display 29% lower default probabilities and enjoy interest rates 2.2 percentage points below internal-combustion peers. Lenders now tailor products that reflect battery-warranty terms and charging-network density. Nonetheless, used-EV prices fell 31.8% in 2024, prompting stricter loan-to-value caps. Sophisticated risk models linking mileage, battery health, and regional resale data are becoming prerequisites to scale this segment nationwide.

Digitization of loan origination & AI-driven underwriting

Digital originations climbed 29% year over year, a record high, as consumers embraced end-to-end online workflows. AI-based pricing engines can lift lender profitability by 34% through granular risk segmentation while broadening access for prime-borderline applicants. CarGurus and Chase now provide pre-qualified rates across 9,000 dealerships, mirroring shopper preferences to secure financing at home. Moody’s purchase of Numerated underscores how incumbents embed automation to retain share. With digital adoption up 165% since 2020, lenders lacking real-time decision tools risk rapid disintermediation.

Credit-union shift toward indirect auto lending

Credit unions pivot toward dealer-originated contracts to offset a direct-lending slowdown, though the National Credit Union Administration stresses enhanced due diligence standards. OneAZ’s Credit Flex Auto Program, backed by Open Lending, shows how partnerships deliver near-prime reach while maintaining cooperative pricing advantages. Regional unions enjoy strong Midwest and Southeast membership bases but face technology-investment hurdles. Sophisticated unions leverage indirect channels to preserve relevance, yet compliance complexity may widen the capability gap versus larger peers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sticky prime-rate environment elevating APRs | -1.2% | National, amplified in rate-sensitive markets | Short term (≤ 2 years) |

| Rising delinquency among long-term loans | -0.8% | National, concentrated in subprime segments | Medium term (2-4 years) |

| Higher capital-adequacy costs under Basel III endgame | -0.6% | National, banks >USD 100 billion assets | Medium term (2-4 years) |

| EV residual-value uncertainty pressuring loan-to-value caps | -0.4% | National, acute in EV-concentrated markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sticky prime-rate environment elevating APRs

The Federal Reserve’s 4.25%–4.5% policy band keeps average new-car payments at USD 749, straining buyer budgets. Forecast easing to 7% auto APR by year-end offers marginal relief. Subprime consumers bear the brunt as lenders narrow credit boxes, pushing many toward buy-here-pay-here lots. Dealers see shrinking promotional-rate allocations from captives, especially on entry-level models. The ongoing rate plateau compresses dealer reserve spreads and prompts banks to chase super-prime borrowers, intensifying competitiveness at the high end while sidelining riskier segments.

Rising delinquency among long-term loans

Subprime 60-day delinquencies reached 6.56% in January 2025, five times the prime levels. Payment extensions are now issued to nearly 4% of subprime accounts versus 0.8% for prime borrowers, yet these often deepen negative equity. Over 10% of borrowers rolled in average negative equity of USD 5,073 on new vehicles, amplifying loss-given-default severity[2]Consumer Financial Protection Bureau, “Data Point: Vehicle Trade-in Equity,” consumerfinance.gov. Federal Reserve studies link higher payments directly to default probability, spotlighting structural weaknesses in ultra-long loans. Tighter underwriting for 84-month terms is spreading as lenders prioritize asset quality over volume.

Segment Analysis

By Vehicle Type: Passenger vehicle financing sustains scale advantage

Passenger vehicles captured 89.53% share of the United States car loan market in 2024, with the segment poised to grow at a 5.77% CAGR over the forecast period. The United States car loan market benefits from standardized collateral, large dealer networks, and broad lender participation that compress spreads and support volume. Connected-car data is feeding new underwriting signals, helping captives tailor offers for loyalty and maintenance packages. Commercial-vehicle financing serves cyclical industries such as logistics and construction, demanding bespoke risk models and higher down-payment thresholds. Telematics adoption is lower among small fleets, but data-sharing mandates under the Infrastructure Investment and Jobs Act could equalize analytics quality. Passenger EV uptake accelerates data granularity, letting lenders track battery health and mileage in real time, further refining pricing.

Commercial financing growth trails the broader United States car loan market, yet margin potential remains attractive because line-haul trucks and last-mile vans carry higher ticket sizes and service revenues. Risk diverges by subsector; for-hire carriers correlate with freight indices, whereas municipal fleets present steadier cash flows. Banks leverage relationship accounts to win these deals, while fintech entrants focus on point-of-sale platforms targeting owner-operators. Collective experience suggests that default frequency is lower, but loss severity is higher due to asset depreciation curves. Thus, the commercialization of telematics and predictive maintenance data stands to reshape residual-value projections and securitization appetite over the forecast period.

By Ownership: Pre-owned segment leads value creation

Used-vehicle loans accounted for 63.12% of the United States car loan market in 2024 and are expanding at a 6.68% CAGR, above the overall United States car loan market. Buyers chase affordability as new-vehicle transaction prices remain elevated, and off-lease volumes inject late-model units with manufacturer warranties. Carvana’s Q1 2025 rebound highlighted consumer preference for digital, end-to-end purchasing, especially among near-prime shoppers. With 39% of all borrowers having negative equity, refinance activity centers on used-car portfolios where rate reductions can restore equity faster. EV depreciation raises caution; lenders set tighter 80% loan-to-value caps on three-year-old electrics versus 110% for comparable gasoline models.

New-vehicle lending, 36.88% of the United States car loan market size, relies on OEM-backed 0% APR events and loyalty rebates. Captives protect share through bundled service contracts that extend customer lifecycle value. However, Toyota’s pullback on incentives signals confidence that the supply-demand balance permits less aggressive financing. Fintech aggregators increasingly route prime borrowers directly to banks with instant approvals, eroding dealer finance penetration. As inventory normalizes, the used-to-new price gap should narrow, yet persistently high interest rates keep monthly payment spreads wide, preserving used-segment momentum.

By Provider Type: Technology reshapes competitive lines

Original-equipment financing arms held a 33.07% share of the United States car loan market in 2024, tapping proprietary customer and vehicle data to maintain underwriting precision. Banks compete on balance-sheet depth but suffer slower tech rollout, while fintechs outpace the market at a 12.79% CAGR by delivering frictionless interfaces and AI-driven approvals. TransUnion’s acquisition of Monevo underscores a data-network land-grab as credit marketplaces grow. Captives, meanwhile, prioritize customer lifetime value; Ford Credit’s analytics platform aims to upsell insurance and maintenance, extending wallet share.

Fintech lenders exploit cloud-native architecture to underwrite thin-file borrowers, charging risk-adjusted spreads that traditional players avoid. Partnerships proliferate; OneMain’s Foursight deal provides near-prime expansion without building new infrastructure. Banks counter by white-labeling digital origination portals to preserve dealer relationships. For investors, asset-backed securities backed by fintech pools attract demand due to granular performance data and rapid seasoning cycles, indicating growing institutional comfort with alternative underwriting frameworks.

Note: Segment shares of all individual segments available upon report purchase

By Tenure: Shorter maturities regain favor

Loans exceeding five years still commanded 53.32% of the United States car loan market in 2024, but face moderating demand as consumers weigh total-interest outlays. Median negative equity on 84-month loans was –USD 8,485, versus positive USD 7,783 on 36-month contracts, illustrating the drag of extended terms. The less than 3 years segment is the fastest-growing slice, advancing at a 7.12% CAGR. Lenders now embed tiered rate discounts, nudging borrowers toward quicker payoff schedules.

The United States car loan market size for the 3–5-year bracket remains resilient, balancing affordability and asset-life alignment. Subscription models also chip away at long-term loans by offering similar monthly costs with flexible exits. Banks and captives adjust residual curves accordingly, ensuring securitization pools remain within rating-agency tolerance. As monetary policy eases, lenders may ease pricing on shorter terms further, stimulating uptake among credit-aware consumers and bolstering portfolio health.

Geography Analysis

Regional dispersion within the United States car loan market reflects income differentials, regulatory regimes, and evolving mobility patterns. Coastal states, led by California and the Northeast corridor, register the highest average loan amounts due to elevated vehicle prices and early EV adoption that benefits from layered state rebates[3]U.S. Department of Energy, “State Policies for Electric-Vehicle Incentives,” energy.gov. These markets also exhibit stronger digital-originations penetration, reflecting higher broadband coverage and fintech density.

The Southeast and Texas corridors combine population influx and diversified manufacturing bases, sustaining robust loan demand across new and used segments. Credit-union penetration is notable in the Midwest, where cooperative traditions foster loyalty; the Federal Reserve notes credit-union consumer-credit share rose to 6% of nominal GDP. Midwest lenders now face heightened rivalry from national fintechs that bypass branch networks, expanding options for rural borrowers.

Mountain West and Plains regions display stable delinquency profiles tied to agricultural and energy cycles. Urban centers nationwide pilot subscription models; Autonomy’s Tesla program launched first in Los Angeles before spreading to Miami and Dallas. Conversely, rural buyers retain a preference for traditional ownership, though online portals increasingly service their financing needs. State privacy-law divergence remains a looming cost; Toyota Financial Services flagged the burden of managing 51 separate frameworks as lawmakers in 34 states weigh new standards. Lenders with centralized compliance teams are better positioned to absorb these hurdles, suggesting geography will continue to influence cost-to-serve and product design.

Competitive Landscape

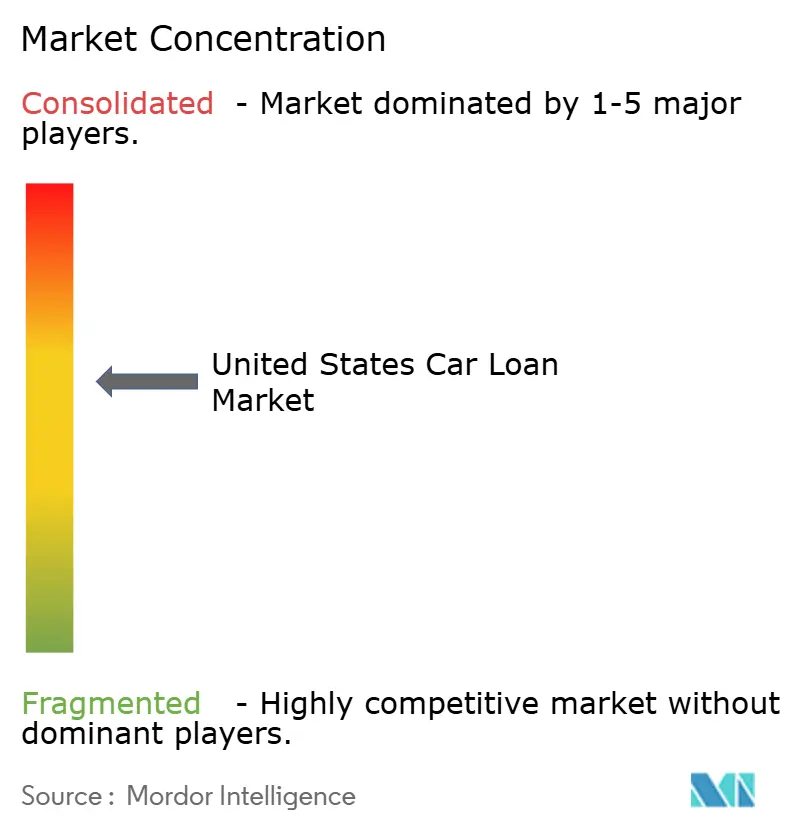

The United States car loan market features moderate concentration, with the top providers controlling a considerable share of the market. Captive lenders dominate new-car funding, while fintech platforms and credit unions carve niches in used and near-prime segments. Traditional banks juggle balance-sheet strength with rising technology costs. Consolidation defines strategic moves: Capital One’s USD 35.3 billion acquisition of Discover creates scale in payments and auto portfolios, signaling an arms race for data and network breadth.

Technology is the primary competitive lever. AI engines that slice risk pools into micro-segments promise 34% higher profitability. Moody’s purchase of Numerated secures origination IP critical for bank clients integrating automation. Subscription offerings pose a longer-term channel threat by bypassing financing altogether, prompting captives to experiment with bundled mobility packages.

EV financing represents a white-space opportunity. Lower default rates and policy incentives attract lenders, yet residual-value volatility demands battery analytics and conservative advance rates. Credit unions seek indirect-lending alliances to regain relevance, but compliance overhead could accelerate attrition among smaller institutions. Overall, the market rewards scale, data science, and agile compliance postures.

United States Car Loan Industry Leaders

-

Ally Financial Inc.

-

Bank of America Corp.

-

Toyota Financial Services

-

Capital One Financial Corp.

-

Ford Motor Credit Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Capital One Financial Corp. closed its USD 35.3 billion purchase of Discover Financial Services, pledging more than USD 265 billion in inclusive lending capacity.

- April 2025: Hyundai Motor America rolled out the Customer Assurance program, locking in MSRP until 2 Jun 2025 amid investment commitments totaling USD 21 billion.

- January 2025: CarGurus and Chase introduced pre-qualification across 9,000 dealerships through the CarGurus digital marketplace.

- November 2024: Moody’s Corporation acquired Numerated Growth Technologies to strengthen its Lending Suite platform.

United States Car Loan Market Report Scope

A car loan is the funds that one borrows from a lender for the sole purpose of purchasing a car. Lenders like banks and non-banking financial companies (NBFCs) offer auto finance to consumers in the form of new and used car loans.

The study gives a brief description of the United States car loan market and includes details on interest rates, type of loans offered, and car loan products & services. The United States car loan market is segmented by vehicle type, ownership, provider type, and tenure. By vehicle type, the market is segmented into passenger vehicles and commercial vehicles. By ownership, the market is segmented by new vehicles and used vehicles. By provider type, the market is segmented by banks, non-bank financial companies, car manufacturers, and others. Others include fintech companies. By tenure, the market is segmented into less than three years, 3-5 years, and more than 5 years.

The report offers market size and forecasts for the United States car loan market in value (USD) for all the above segments.

| Passenger Vehicle |

| Commercial Vehicle |

| New Vehicles |

| Used Vehicles |

| Banks |

| Non-Banking Financial Institutions |

| Original Equipment Manufacturers |

| Other Provider Types (Fintech Companies) |

| Less than 3 Years |

| 3-5 Years |

| More than 5 years |

| By Vehicle Type | Passenger Vehicle |

| Commercial Vehicle | |

| By Ownership | New Vehicles |

| Used Vehicles | |

| By Provider Type | Banks |

| Non-Banking Financial Institutions | |

| Original Equipment Manufacturers | |

| Other Provider Types (Fintech Companies) | |

| By Tenure | Less than 3 Years |

| 3-5 Years | |

| More than 5 years |

Key Questions Answered in the Report

What is the current value of the United States car loan market?

The market is valued at USD 595.19 billion in 2025, with a projected rise to USD 898.25 billion by 2030.

Which vehicle category attracts the most financing?

Passenger vehicles dominate, securing 89.53% market share in 2024 due to their broad consumer appeal.

Why are used-vehicle loans growing faster than new-vehicle loans?

Used vehicles captured 63.12% of the market share in 2024 and are projected to grow at a 6.68% CAGR because affordability pressures remain high and off-lease supply is plentiful.

How are rising delinquencies affecting lenders?

Delinquencies on 84-month loans, particularly among subprime borrowers, push lenders to tighten underwriting and favor shorter terms to control risk.

What role do fintech companies play in auto finance?

Fintech lenders expand market reach with digital origination and AI underwriting, advancing at a 12.79% CAGR and challenging traditional banks.

How is EV adoption influencing auto-loan products?

EV borrowers show 29% lower default rates and qualify for lower rates, but lenders adjust loan-to-value caps to manage uncertain residual values.

Page last updated on: