| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| CAGR | 4.20 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

US Caps and Closure Market Analysis

The US Caps and Closure Market is expected to register a CAGR of 4.2% during the forecast period.

The United States caps and closures industry is experiencing significant transformation driven by evolving consumer preferences and technological advancements in packaging solutions. The integration of nanotechnology in convenience food manufacturing has revolutionized critical functions, including preservation procedures, container sealing methods, and finished goods processing. This technological evolution has particularly impacted the food packaging sector, where advanced packaging closure systems are becoming increasingly sophisticated to meet modern consumption patterns. The industry has witnessed a notable shift towards smart packaging solutions, with manufacturers incorporating features like NFC-enabled closures and tamper-evident closure technologies to enhance product security and consumer engagement.

Environmental sustainability has emerged as a crucial factor shaping the industry landscape, with stringent regulations significantly influencing product development and manufacturing processes. In California, the implementation of Assembly Bill 2779 has mandated specific requirements for plastic bottle caps, requiring manufacturers to either develop California-specific bottles with tethered caps or create different packaging solutions for other U.S. markets. This regulatory environment has prompted manufacturers to invest in eco-friendly alternatives and sustainable production methods, leading to innovations in biodegradable materials and recyclable container closure systems.

The pharmaceutical and healthcare sectors continue to drive significant innovations in the caps and closures market, particularly in child-resistant and senior-friendly pharmaceutical closure solutions. Manufacturers are developing sophisticated closure systems that combine safety features with ease of use, responding to both regulatory requirements and consumer needs. The industry has witnessed the emergence of advanced closure technologies that incorporate features such as anti-counterfeiting measures and smart monitoring capabilities, particularly important for prescription medications and over-the-counter products.

The beverage industry remains a key influencer in market dynamics, with manufacturers focusing on convenience and functionality in closure designs. The trend towards premium packaging solutions has led to innovations in closure systems that enhance product differentiation and brand identity. Manufacturers are increasingly investing in research and development to create closures that not only provide proper bottle sealing and preservation but also offer enhanced user experience through features like easy-open mechanisms and resealable capabilities. This focus on consumer convenience has resulted in the development of various specialized closure solutions, including sports caps, flip-top closures, and dispensing systems designed for specific beverage categories.

US Caps and Closure Market Trends

The Increased Demand for Innovative Solutions from Different End Users

The caps and closures market is experiencing significant transformation driven by end-user demands for innovative solutions across multiple industries. According to the American Chemistry Council, the substantial investment of USD 24.9 billion in plastic products out of a total USD 37.8 billion investment in plastic resins demonstrates the strong industrial commitment to innovation in packaging solutions. This innovation wave is particularly evident in the anti-counterfeiting segment, where manufacturers are incorporating advanced technologies into their closure designs. For instance, in May 2019, Guala Closures introduced the groundbreaking smart closure e-WAK technology, the first NFC aluminum closure that enables wine bottles to become connected devices. This smart closure technology embeds a chip within the closure that can be scanned by smartphones, providing consumers with authentication certificates and detailed product information, addressing the growing demand for product verification and enhanced consumer engagement.

The market is witnessing a surge in innovation focused on consumer convenience and sustainability requirements. Companies like Borealis are leading this transformation with products such as BorPure RF777MO, based on their proprietary Borstar Nucleation Technology (BNT), specifically designed for flip-top closure caps. This innovation enables manufacturers to reduce cycle times by more than 10% through fast crystallization behavior, while simultaneously lowering energy consumption and overall CO2 footprint. The beverage industry, in particular, has been at the forefront of demanding innovative closure solutions, with the Wine Institute of America reporting production of almost 1 billion gallons of wine in 2017. This has led to the development of sophisticated bottle closure systems that not only preserve product quality but also enhance the consumer experience through features such as easy-opening mechanisms and tamper-evident designs. Additionally, the International Bottled Water Association (IBWA) reported bottled water sales of USD 18.5 billion, highlighting the massive demand for innovative beverage closure solutions in the beverage sector, with the average American consuming 167 plastic bottles of water annually.

Understand The Key Trends Shaping This Market

Download PDF

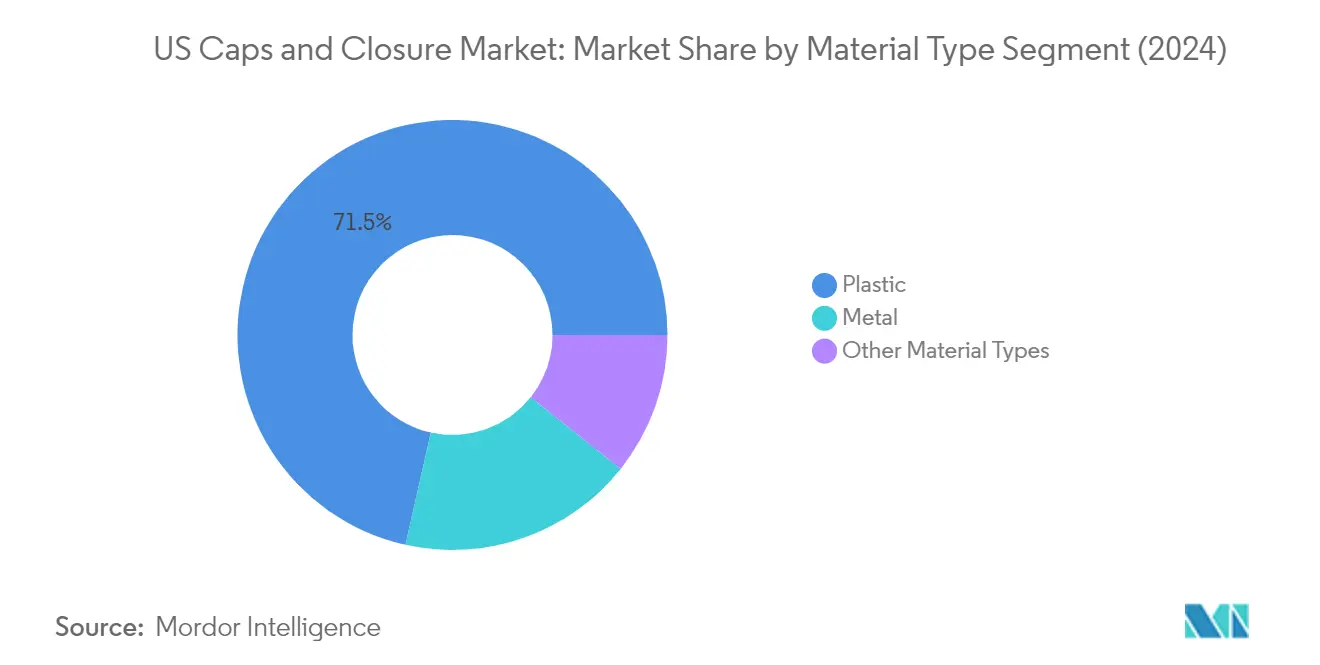

Segment Analysis: By Material Type

Plastic Segment in US Caps and Closure Market

The plastic closure segment continues to dominate the US caps and closure market, accounting for approximately 72% of the total market share in 2024. This significant market position is driven by plastic's versatile properties, including excellent tensile strength, chemical resistance, and cost-effectiveness compared to other materials. The segment's growth is particularly strong in beverage packaging applications, where PET and HDPE plastic closures are widely used for water bottles, carbonated drinks, and dairy products. Manufacturers are increasingly focusing on sustainable plastic closure solutions, with many companies developing recyclable and lightweight closure designs to meet environmental regulations and consumer preferences. The segment has also seen substantial innovation in smart packaging solutions, with companies incorporating features like tamper-evidence, child-resistance, and enhanced barrier properties into their plastic closure designs.

Remaining Segments in Material Type Segmentation

The metal closure and other materials segments play crucial complementary roles in the US caps and closure market. Metal closures maintain their significance in premium packaging applications, particularly in the wine and spirits industry, where they provide superior sealing properties and enhance brand perception through decorative options. The other materials segment, which includes cork, rubber, and glass closures, serves specialized applications in various industries. Cork closures continue to be important in the wine industry, while rubber closures find applications in pharmaceutical and laboratory settings. These segments are experiencing ongoing innovation in areas such as tamper-evidence features, sustainable materials, and enhanced functionality to meet evolving industry requirements and consumer preferences.

Segment Analysis: By End-User Industry

Beverage Segment in US Caps and Closure Market

The beverage segment continues to dominate the US caps and closure market, accounting for approximately 59% of the total market share in 2024. This significant market position is driven by the increasing demand for bottled water, carbonated soft drinks, alcoholic beverages, and dairy products. The segment's growth is particularly notable in the bottled water category, where changing consumer preferences toward healthier beverage options have led to increased consumption. The adoption of innovative closure solutions, such as sports caps and tethered caps that comply with sustainability regulations, has further strengthened this segment's position. Major beverage manufacturers are increasingly focusing on sustainable packaging solutions and smart closure technologies that enhance consumer convenience while maintaining product freshness and safety. The segment has also witnessed significant developments in terms of tamper-evident features and child-resistant closures, particularly in the alcoholic beverage category.

Remaining Segments in US Caps and Closure Market

The pharmaceutical and healthcare segment represents the second-largest portion of the market, driven by the increasing demand for child-resistant closures and tamper-evident packaging solutions. The food segment maintains a substantial presence in the market, with applications ranging from condiments to preserved foods, requiring various closure solutions that ensure product freshness and safety. The cosmetics and toiletries segment, while smaller in market share, continues to drive innovation in premium closure solutions and dispensing systems. The other end-user industries, including automotive cleaners, paints and coatings, and chemicals, contribute to market diversity through specialized closure requirements and safety features. Each of these segments plays a crucial role in driving technological advancements and material innovations in the caps and closure industry, particularly in areas such as sustainability and consumer convenience.

US Caps and Closure Industry Overview

Top Companies in US Caps and Closure Market

The US caps and closure market features prominent players like Amcor, Berry Global, Silgan Closures, Aptar Group, and Bericap Holdings leading the industry through continuous innovation and strategic expansion. These companies are heavily investing in research and development to create advanced closure solutions incorporating features like child resistance, tamper-evident closures, and sustainability. The focus on operational excellence is evident through automation initiatives and manufacturing facility upgrades across the country. Companies are increasingly adopting technologies like near-field communications (NFC) and smart packaging solutions to enhance product functionality and consumer engagement. Strategic partnerships and licensing agreements have become common practices to expand product portfolios and access new technologies, while geographical expansion through new manufacturing facilities helps companies optimize their distribution networks and better serve regional markets.

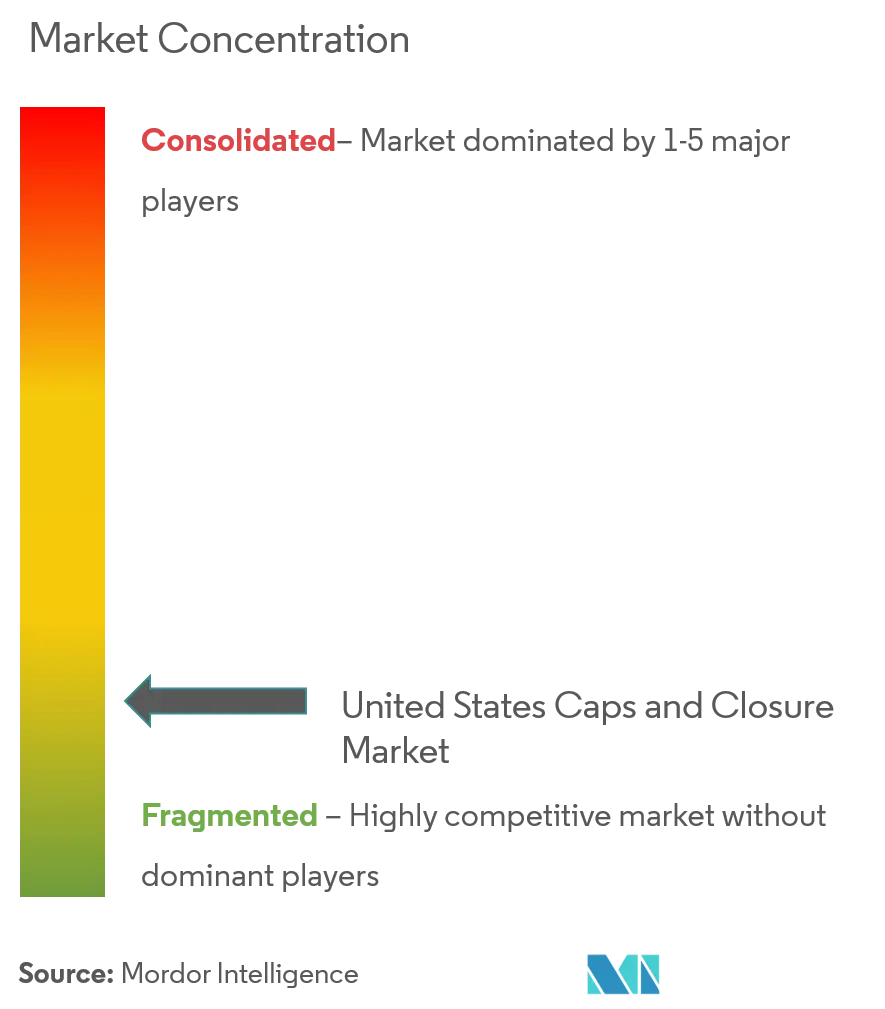

Consolidated Market with Strong M&A Activity

The US caps and closure market exhibits a highly fragmented competitive landscape with a mix of global conglomerates and specialized regional players. The larger multinational corporations leverage their extensive resources, established distribution networks, and diverse product portfolios to maintain market dominance, while specialized players focus on niche segments and custom solutions. Market consolidation is primarily driven by larger players acquiring smaller, specialized manufacturers to expand their technological capabilities and market reach. The industry has witnessed significant merger and acquisition activities, with companies like Berry Global completing strategic acquisitions to strengthen their market position and expand their product offerings.

The market dynamics are characterized by intense competition among established players, with barriers to entry remaining moderately high due to capital requirements and technical expertise needed for manufacturing operations. Companies with integrated operations, from raw material procurement to end-product manufacturing, tend to have stronger market positions. The presence of strong customer relationships and brand recognition plays a crucial role in maintaining market share, while the ability to offer innovative solutions and maintain cost competitiveness determines long-term success in the market.

Innovation and Sustainability Drive Future Growth

Success in the US caps and closure market increasingly depends on companies' ability to align with evolving consumer preferences and regulatory requirements. Market incumbents are focusing on developing sustainable solutions, including bio-based materials and recyclable designs, to address growing environmental concerns. Investment in advanced manufacturing technologies and digital solutions is becoming crucial for maintaining competitive advantage. Companies are also strengthening their position through vertical integration and strategic partnerships with raw material suppliers to ensure supply chain stability and cost efficiency.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized solutions. The focus on end-user industries with high growth potential, such as pharmaceuticals and personal care, offers opportunities for market expansion. Companies must navigate increasing regulatory pressures regarding plastic usage and recycling while maintaining product performance and safety standards. The ability to offer innovative closure solutions that address specific industry challenges, combined with efficient production processes and strong customer relationships, will be critical for long-term success in the market. Companies are also exploring packaging closures and container closures innovations to meet diverse industry needs, including dispensing closures options that enhance user convenience and product integrity.

US Caps and Closure Market Leaders

-

Albea SA

-

Silgan Holdings Inc.

-

Amcor PLC

-

Closure Systems International Inc. (CSI)

-

AptarGroup Inc. (AptarGroup)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

US Caps and Closure Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Porters 5 Force Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 The Increased Demand for Innovative Solutions from Different End Users.

-

5.2 Market Restraints

- 5.2.1 Stringent Regulation on Manufacturers Pertaining to Environmental Degradation

6. MARKET SEGMENTATION

-

6.1 By Material Type

- 6.1.1 Plastic

- 6.1.1.1 PET

- 6.1.1.2 PP

- 6.1.1.3 HDPE and LDPE

- 6.1.1.4 Other Plastics

- 6.1.2 Metal

- 6.1.3 Other Material Types

-

6.2 By End-User Industry

- 6.2.1 Beverage (Bottled Water, Beer, Dairy, RTD, Wine, Spirits, etc.)

- 6.2.2 Food

- 6.2.3 Pharmaceutical and Healthcare

- 6.2.4 Cosmetics and Toiletries

- 6.2.5 Other End-user Industries (Automotive Cleaners, Paints and Coatings, Chemicals, etc.)

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Albéa S.A.

- 7.1.2 Silgan Closures

- 7.1.3 Amcor Plc

- 7.1.4 Closure Systems International

- 7.1.5 Aptar Group Inc.

- 7.1.6 Bericap Holdings

- 7.1.7 Berry Global Inc.

- 7.1.8 Coral Products Plc

- 7.1.9 Crown Holdings Inc.

- 7.1.10 Tetra Pak International Sa

- 7.1.11 Mjs Packaging

- 7.1.12 O. Berk Company Llc

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OUTLOOK OF THE MARKET

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

US Caps and Closure Industry Segmentation

US caps and closures market studies various segment that are part of manufacturing different types of plastic, metal caps and closures, and end user segment. The end-user industry of the US caps and closure market include beverage, food, pharmaceuticals and healthcare, cosmetics and toiletries, and other end users, such as automotive cleaners, paints and coatings, chemicals, among others.

| By Material Type | Plastic | PET |

| PP | ||

| HDPE and LDPE | ||

| Other Plastics | ||

| Metal | ||

| Other Material Types | ||

| By End-User Industry | Beverage (Bottled Water, Beer, Dairy, RTD, Wine, Spirits, etc.) | |

| Food | ||

| Pharmaceutical and Healthcare | ||

| Cosmetics and Toiletries | ||

| Other End-user Industries (Automotive Cleaners, Paints and Coatings, Chemicals, etc.) |

Need A Different Region or Segment?

Customize Now

US Caps and Closure Market Research FAQs

What is the current US Caps and Closure Market size?

The US Caps and Closure Market is projected to register a CAGR of 4.2% during the forecast period (2025-2030)

Who are the key players in US Caps and Closure Market?

Albea SA, Silgan Holdings Inc., Amcor PLC, Closure Systems International Inc. (CSI) and AptarGroup Inc. (AptarGroup) are the major companies operating in the US Caps and Closure Market.

What years does this US Caps and Closure Market cover?

The report covers the US Caps and Closure Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the US Caps and Closure Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

US Caps and Closure Market Research

Mordor Intelligence provides a comprehensive analysis of the caps and closure industry. We leverage decades of consulting expertise in packaging technologies. Our detailed report examines various closure types, including plastic closure and metal closure systems. It also covers screw cap technologies and advanced container sealing solutions. The analysis spans traditional bottle closure mechanisms to innovative dispensing closure and tamper evident closure systems. This offers deep insights into bottle sealing technologies and emerging trends in the packaging closure sector.

Stakeholders across the value chain benefit from our detailed examination of container closure applications. This includes beverage closure systems, closures for pharmaceuticals, and specialized jar closure solutions. The report explores various designs, from crown closure and flip top closure to push pull closure and snap on closure mechanisms. It is available as an easy-to-download report PDF. Our analysis encompasses twist off closure technologies and innovative developments in the bottle caps and closures industry. We offer actionable insights for manufacturers, suppliers, and end-users seeking to optimize their closure solutions.