Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Growth Rate | 5.26% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Automotive Collision Avoidance Systems Market Analysis by Mordor Intelligence

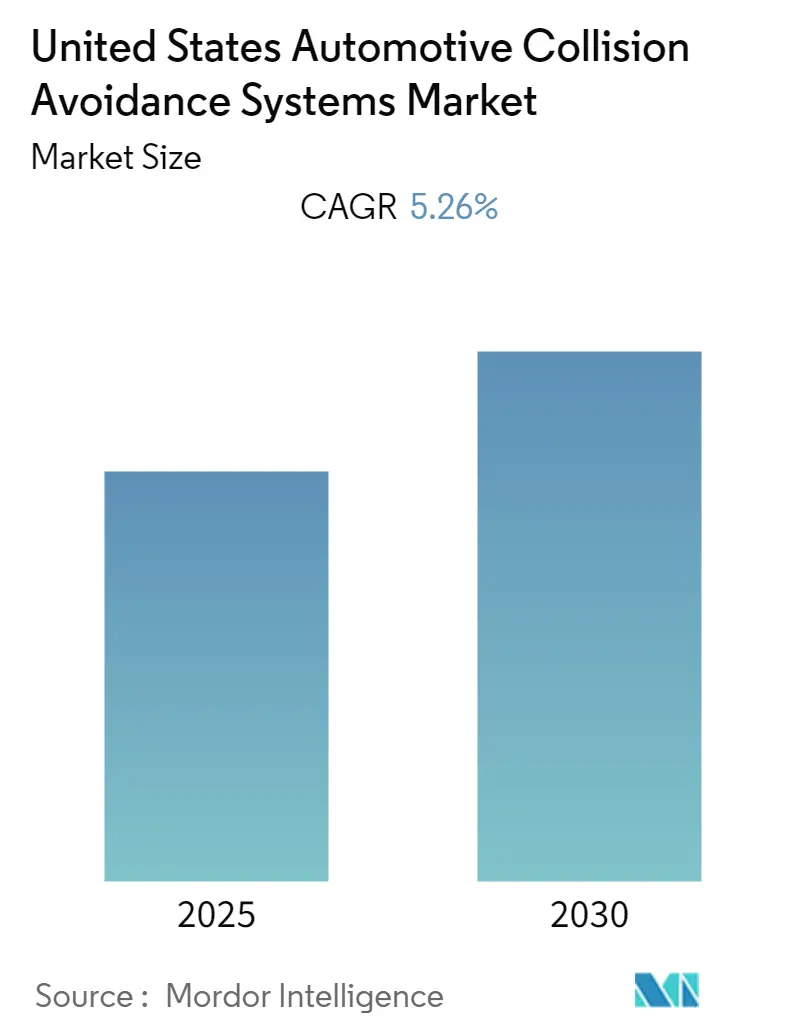

The United States Automotive Collision Avoidance Systems Market is expected to register a CAGR of 5.26% during the forecast period.

The United States automotive collision avoidance systems market is experiencing rapid technological evolution, driven by the increasing integration of advanced driver assistance systems (ADAS) across vehicle segments. Currently, over 60 million vehicles in the United States are equipped with ADAS technologies, marking a significant shift from these systems being exclusive to luxury vehicles to becoming standard features in entry-level models. This widespread adoption is reshaping the automotive safety systems landscape, with manufacturers increasingly incorporating sophisticated collision avoidance systems across their vehicle lineups.

Major automotive and technology companies are forming strategic partnerships to accelerate innovation in collision avoidance systems. A notable example is Ford's collaboration with Mobileye to enhance camera-based detection capabilities for driver-assist systems, including improved forward collision warning and pedestrian detection features. Continental's recent USD 122 million investment in a new radar sensor plant in Texas further demonstrates the industry's commitment to expanding domestic production capabilities for advanced automotive safety technology.

The market is witnessing significant advancement in autonomous vehicle technology integration. Waymo has successfully launched autonomous taxi services in Phoenix, Arizona, while Cruise has deployed vehicles without drivers in San Francisco for its robotic taxi service. These developments are particularly noteworthy as they represent practical applications of collision avoidance systems in real-world autonomous driving scenarios, setting new benchmarks for safety technology implementation.

The industry is experiencing a shift toward comprehensive safety solutions that combine multiple sensing technologies. Tesla, for instance, has equipped all its Model 3, X, and S vehicles with hardware capable of full autonomy, including advanced collision avoidance systems features as standard equipment. This trend is prompting other manufacturers to follow suit, with companies like Daimler, BMW, and Ford announcing plans to incorporate autonomous emergency braking (AEB) systems as standard features in their upcoming models. The integration of multiple sensing technologies, including radar, LiDAR, cameras, and ultrasonic sensors, is creating more robust and reliable automotive sensor solutions.

United States Automotive Collision Avoidance Systems Market Trends and Insights

Growing Demand for Safety Features in Vehicles

The increasing emphasis on vehicle and passenger safety has become a primary driver for the United States automotive collision avoidance systems market. Currently, there are over 60 million vehicles in the United States equipped with Advanced Driver Assistance Systems (ADAS), demonstrating the widespread adoption of vehicle safety system technologies. These systems, which were previously only available in high-end models, are now being incorporated into entry-level vehicles, making safety features more accessible to a broader consumer base. The effectiveness of these safety systems is evident in the significant reduction of accidents, with blind spot warning technology showing a 23% decrease in lane-change collisions with injuries, while forward collision warning systems with automatic emergency braking have demonstrated a 20% reduction in front-to-rear crashes with injuries.

Major automotive manufacturers are responding to this growing demand by making collision avoidance features standard in their vehicles. Tesla is offering all its cars with automatic emergency braking (AEB) features as standard, while other automakers like Daimler, BMW, and Ford are following suit by planning to provide AEB in all their upcoming models. The integration of these safety systems goes beyond mere collision prevention, offering additional benefits such as improved traffic awareness, reduced insurance premiums, lower repair and maintenance costs, and increased fuel efficiency. Furthermore, the implementation of V2X (Vehicle-to-Vehicle) communication technology is enhancing these systems by enabling vehicles to share information about relative speeds, positions, directions of travel, and control inputs, creating a more comprehensive safety ecosystem.

Understand The Key Trends Shaping This Market

Download PDF

Technological Advancements and Innovation

The rapid pace of technological innovation in sensor technologies and artificial intelligence is revolutionizing the automotive collision avoidance systems market. Companies are continuously developing and improving various sensing technologies, including automotive radar, automotive lidar, camera, and ultrasonic sensors, to create more sophisticated and reliable safety systems. For instance, Velodyne Lidar Inc. has introduced the Velarray H800, a new solid-state LiDAR sensor specifically designed for automotive-grade performance and safe navigation in advanced driver assistance systems and autonomous mobility applications. Similarly, ZF Friedrichshafen AG has launched a new generation ADAS camera, the S-Cam 4.8, offering an expanded 100-degree field of view for enhanced automatic emergency braking, lane-keeping, and semi-automated vehicle functions.

Strategic partnerships and collaborations are further accelerating technological advancement in this sector. Notable examples include Ford Motor Company's collaboration with Mobileye to develop improved camera-based collision warning systems and pedestrian detection system capabilities for vehicles and pedestrians. Additionally, Verizon's partnership with HERE Technologies aims to develop next-generation technologies for vehicle and pedestrian safety using hyper-precise high-definition mapping and RTK technology. These collaborations are creating more sophisticated systems that combine multiple technologies, such as the integration of 5G networks with AI-powered collision avoidance systems, enabling faster response times and more accurate threat detection. The advancement in adaptive cruise control (ACC) technology is particularly noteworthy, as it has evolved to become an essential feature for future autonomous vehicle technology, automatically adjusting vehicle speed and maintaining safe following distances without driver intervention.

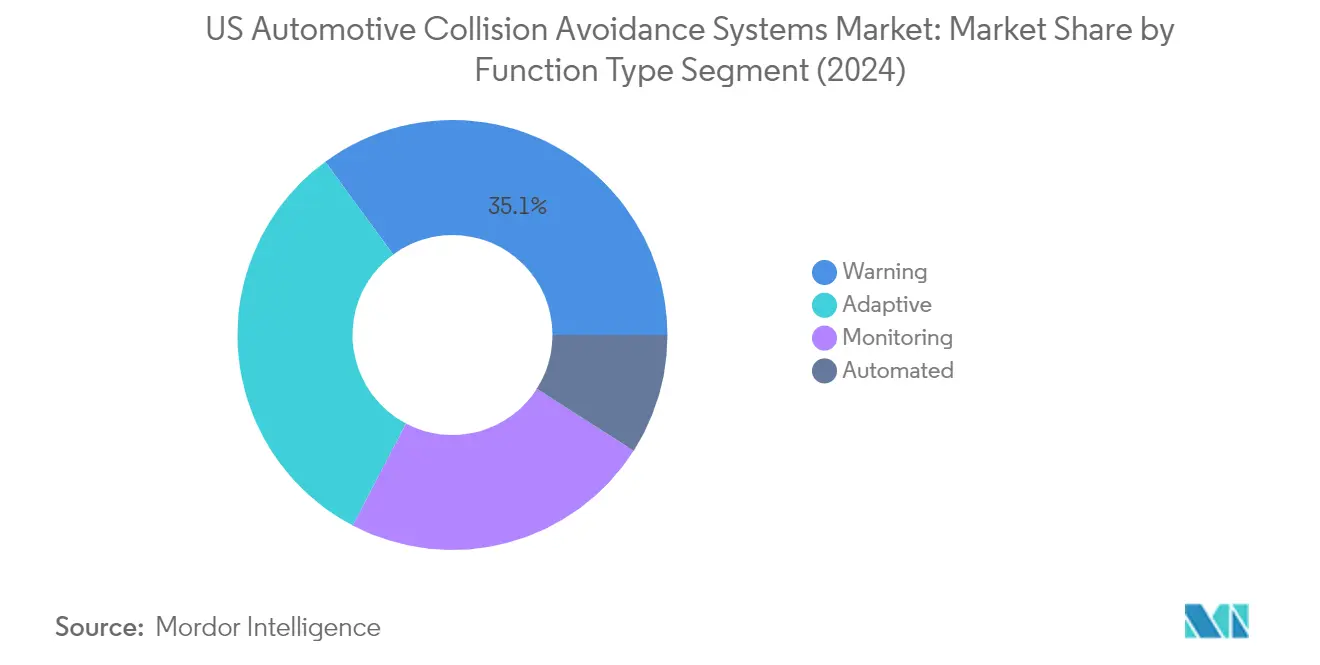

Segment Analysis: By Function Type

Warning Segment in US Automotive Collision Avoidance Systems Market

The Warning segment continues to dominate the US automotive collision avoidance systems market, holding approximately 32% market share in 2024. This segment's prominence is driven by the widespread adoption of essential warning systems like forward collision warning, lane departure warning, and blind spot detection systems. The National Highway Traffic Safety Administration's data highlights that these warning systems have demonstrated significant effectiveness in reducing accidents, with forward collision warning systems showing up to a 20% reduction in front-to-rear crashes with injuries. Major automotive manufacturers are increasingly incorporating these warning systems as standard features in their vehicle lineup, particularly in response to growing consumer awareness and demand for basic safety features.

Automated Segment in US Automotive Collision Avoidance Systems Market

The Automated segment is emerging as the fastest-growing segment in the market, projected to grow at approximately 5.4% during 2024-2029. This growth is primarily driven by rapid advancements in automated lighting systems, automated night vision capabilities, and rain-sensing technologies. The increasing integration of artificial intelligence and machine learning algorithms in these automated systems is enhancing their effectiveness in various driving conditions. Premium automotive manufacturers are particularly focusing on developing sophisticated automated systems that can adapt to different environmental conditions and driving scenarios, making these features more reliable and efficient for everyday use.

Remaining Segments in Function Type Segmentation

The Adaptive and Monitoring segments also play crucial roles in the US automotive collision avoidance systems market. The Adaptive segment, which includes technologies like adaptive cruise control and adaptive lighting systems, is gaining significant traction among mid-range vehicle manufacturers. The Monitoring segment, encompassing various vehicle monitoring systems and driver attention detection technologies, continues to evolve with the integration of more sophisticated sensors and cameras. Both segments are witnessing continuous technological improvements and increased adoption across different vehicle categories, contributing to the overall advancement of vehicle safety systems.

Segment Analysis: By Technology Type

Radar Segment in US Automotive Collision Avoidance Systems Market

The automotive radar segment maintains its dominance in the US automotive collision avoidance systems market, commanding approximately 37% market share in 2024. This leadership position is attributed to radar's superior capabilities in detecting objects and measuring distances accurately in various weather conditions. Major automotive manufacturers are increasingly incorporating advanced radar systems in their vehicles for features like adaptive cruise control and emergency braking systems. The technology's reliability in harsh weather conditions and its ability to provide accurate distance measurements up to 500 meters make it particularly valuable for collision avoidance applications. Recent developments in automotive radar technology have led to more compact and cost-effective solutions, further driving their adoption across various vehicle segments.

Camera Segment in US Automotive Collision Avoidance Systems Market

The camera segment is emerging as the fastest-growing technology in the US automotive collision avoidance systems market, with projections indicating strong growth from 2024 to 2029. This growth is driven by significant advancements in image processing algorithms and increasing camera resolution capabilities. The segment's expansion is further supported by the rising integration of artificial intelligence and machine learning technologies, enabling more accurate object recognition and classification. Camera-based systems are becoming increasingly sophisticated, offering features like pedestrian detection, traffic sign recognition, and lane departure warning. The technology's versatility in supporting multiple safety functions simultaneously, combined with decreasing component costs, is making it an attractive option for automotive manufacturers looking to enhance their vehicle safety features.

Remaining Segments in Technology Type

The automotive lidar and ultrasonic segments continue to play crucial roles in the US automotive collision avoidance systems market. LiDAR technology offers precise 3D mapping capabilities and is particularly effective in autonomous driving applications, while ultrasonic sensors excel in short-range detection scenarios such as parking assistance and low-speed maneuvering. These technologies complement radar and camera systems, often working in conjunction to provide comprehensive safety coverage. The integration of multiple sensor types allows vehicles to maintain safety functions across various operating conditions and scenarios, creating redundancy and improving overall system reliability. Both segments are seeing continuous technological improvements, with manufacturers focusing on developing more compact and cost-effective solutions.

Segment Analysis: By Vehicle Type

Passenger Cars Segment in US Automotive Collision Avoidance Systems Market

The passenger cars segment dominates the US automotive collision avoidance systems market, commanding approximately 80% of the total market share in 2024, while also maintaining the highest growth trajectory with a projected growth rate of around 6% through 2029. This segment's dominance is primarily driven by increasing consumer demand for advanced safety features and the growing integration of collision avoidance technologies as standard equipment in new passenger vehicles. The implementation of stringent safety regulations and the Moving Forward Act, which mandates the inclusion of crash avoidance technologies in all new passenger vehicles, has further strengthened this segment's position. Major automakers are actively expanding their safety technology offerings, with companies like Ford and Mobileye collaborating to enhance camera-based detection capabilities for driver-assist systems. Additionally, the rising consumer awareness about vehicle safety and the increasing adoption of ADAS features across different price segments of passenger cars continue to fuel the segment's growth.

Commercial Vehicles Segment in US Automotive Collision Avoidance Systems Market

The commercial vehicles segment represents a crucial component of the US automotive collision avoidance systems market, with fleet operators increasingly recognizing the importance of advanced safety technologies in reducing accidents and operational costs. The segment has witnessed significant technological advancements, particularly in areas such as lane departure warning systems and video-based onboard safety monitoring systems, which have proven to be cost-effective solutions for fleet operations. Fleet managers are actively pushing for enhanced vehicle safety technologies in their vehicle orders, although some challenges persist in obtaining advanced safety features for certain work truck and van models that are typically ordered with basic trim packages. The integration of these safety technologies has shown a positive impact on the total cost of ownership by increasing residual values, making them increasingly attractive for commercial fleet operators. Furthermore, the growing emphasis on driver and road safety, coupled with the rising adoption of autonomous and semi-autonomous features in commercial vehicles, continues to drive innovation and implementation of collision avoidance systems in this segment.

United States Automotive Collision Avoidance Systems Market Geography Segment Analysis

United States Automotive Collision Avoidance Systems Market in California

California continues to lead the United States collision avoidance systems market, commanding approximately 11% of the total market share in 2024. The state's dominance is driven by its robust automotive ecosystem and progressive regulatory environment supporting advanced vehicle safety technologies. California's leadership in autonomous vehicle testing and development has created a conducive environment for collision avoidance system adoption. The presence of major technology companies and automotive innovation centers in Silicon Valley has fostered continuous advancement in sensor technologies and artificial intelligence algorithms essential for these systems. The state's high concentration of luxury vehicle sales, which typically feature advanced automotive safety systems as standard equipment, further strengthens market growth. Additionally, California's stringent vehicle safety regulations and environmental policies have encouraged automakers to incorporate more sophisticated collision avoidance technologies in their vehicles. The state's large population and high vehicle ownership rates, combined with increasing consumer awareness about vehicle safety, continue to drive sustained demand for these systems.

United States Automotive Collision Avoidance Systems Market in Ohio

Ohio emerges as the fastest-growing market for automotive collision avoidance systems, with a projected CAGR of approximately 5% from 2024 to 2029. The state's remarkable growth is attributed to its strong automotive manufacturing base and increasing integration of advanced safety technologies in locally produced vehicles. Ohio's strategic position in the automotive supply chain, with numerous Tier 1 and Tier 2 suppliers specializing in safety systems, has created a robust ecosystem for collision avoidance technology development. The state's proactive approach to embracing new automotive safety technologies, supported by various research institutions and testing facilities, has accelerated market expansion. The presence of major automotive research centers and testing grounds has facilitated rapid validation and implementation of new collision avoidance technologies. Furthermore, Ohio's diverse weather conditions have made it an ideal testing ground for developing and refining these systems under various environmental challenges. The state's focus on smart mobility initiatives and connected vehicle infrastructure has also created additional opportunities for market growth.

United States Automotive Collision Avoidance Systems Market in Texas

Texas represents a significant market for automotive collision avoidance systems, driven by its extensive transportation network and diverse vehicle fleet. The state's unique combination of urban and rural driving environments has created varied demands for different types of collision avoidance technologies. Texas's robust economy and large commercial vehicle sector have particularly influenced the adoption of advanced safety systems in fleet vehicles. The state's extensive highway system and high-speed driving conditions have emphasized the importance of forward collision warning and automatic emergency braking systems. The presence of major automotive manufacturing facilities and research centers has facilitated local innovation in collision avoidance technologies. Additionally, Texas's growing urban populations in cities like Houston, Dallas, and Austin have created increased demand for vehicles equipped with advanced safety features. The state's focus on reducing traffic accidents through technological solutions has further accelerated the adoption of these systems.

United States Automotive Collision Avoidance Systems Market in Florida

Florida's automotive collision avoidance systems market is characterized by its unique demographic composition and driving conditions. The state's large retirement community has created a specific demand for vehicles equipped with advanced safety features that enhance driver awareness and reaction time. Florida's high tourism activity has also influenced the rental car market to adopt vehicles with modern safety systems. The state's varied driving conditions, from dense urban areas to coastal highways, have necessitated diverse collision avoidance solutions. The prevalence of severe weather conditions has particularly driven demand for systems that can function effectively in challenging visibility situations. Florida's commitment to road safety improvements has led to increased awareness and adoption of collision avoidance technologies. The state's automotive dealerships and service centers have played a crucial role in educating consumers about the benefits of these safety systems. Additionally, Florida's growing population and increasing urbanization continue to drive market expansion.

United States Automotive Collision Avoidance Systems Market in Other States

The remaining states in the United States demonstrate varying levels of adoption and growth in automotive collision avoidance systems, each influenced by their unique geographic, economic, and regulatory environments. States like New York have shown strong adoption rates in urban areas where complex traffic conditions necessitate advanced safety features such as lane departure warning and blind spot detection. The northeastern states generally demonstrate higher adoption rates due to their dense population centers and challenging weather conditions. Midwestern states benefit from their strong automotive manufacturing heritage and testing infrastructure. Western states show increasing adoption rates driven by their tech-savvy populations and focus on innovative transportation solutions. The market development in these regions is further supported by state-specific safety regulations, consumer preferences, and local automotive industry presence. The varying pace of infrastructure development and economic conditions across these states continues to shape the regional adoption patterns of collision avoidance technologies.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in United States Automotive Collision Avoidance Systems Market

The market is characterized by continuous product innovation across sensing technologies, particularly in radar, LiDAR, and camera-based systems. Companies are actively pursuing strategic partnerships with technology firms and automotive manufacturers to enhance their autonomous driving capabilities. Major players are expanding their manufacturing footprint, particularly evident in Continental's Texas facility expansion and Aptiv's increased production capacity. Research and development investments are heavily focused on integrating multiple functionalities into unified platforms, with companies like Bosch and Delphi leading breakthrough innovations in automotive sensor fusion technology. The industry is witnessing a strong trend toward developing scalable solutions that can be implemented across different vehicle segments, while simultaneously working on cost optimization to make these systems more accessible for mass-market vehicles.

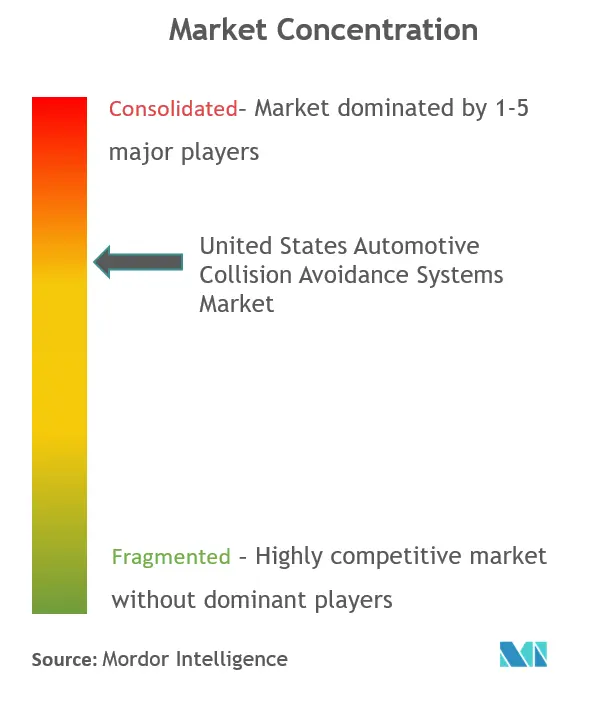

Consolidated Market Led By Global Players

The competitive landscape is dominated by well-established global automotive technology conglomerates, with the top four manufacturers capturing approximately seventy percent of the market share. Continental AG, Delphi Automotive (now Aptiv), Robert Bosch, and ZF Friedrichshafen AG have established themselves as market leaders through their comprehensive product portfolios and strong relationships with major automotive manufacturers. These companies leverage their extensive research and development capabilities, global manufacturing presence, and long-standing industry expertise to maintain their competitive positions. The market has witnessed significant consolidation through strategic acquisitions, notably ZF's acquisition of WABCO and Intel's acquisition of Mobileye, indicating a trend toward technology integration and capability enhancement.

The market structure is characterized by high entry barriers due to the substantial technological expertise and capital requirements needed to develop and manufacture automotive collision avoidance systems. Companies are increasingly forming strategic alliances and joint ventures to share development costs and accelerate innovation cycles. The competitive dynamics are further shaped by the presence of specialized players like Mobileye and Autoliv, who have carved out strong positions in specific technology segments while competing with full-range suppliers. The industry has seen a notable shift toward vertical integration, with major players expanding their capabilities across the value chain to strengthen their market positions.

Innovation and Integration Drive Market Success

Success in this market increasingly depends on companies' ability to develop integrated solutions that combine multiple sensing technologies while maintaining cost competitiveness. Incumbent players are focusing on strengthening their technological capabilities through increased research and development investments and strategic acquisitions of innovative startups. Companies are also emphasizing the development of scalable platforms that can be easily adapted across different vehicle segments and price points. The ability to establish strong partnerships with automotive manufacturers and maintain high-quality standards while meeting stringent safety regulations has become crucial for maintaining market position.

For new entrants and smaller players, success lies in identifying and focusing on specific technological niches where they can develop superior solutions. Companies need to balance the increasing end-user demand for advanced safety features with cost considerations, particularly as automotive manufacturers seek to incorporate these systems in mid-range vehicles. The regulatory environment continues to play a crucial role in shaping market dynamics, with companies needing to stay ahead of evolving safety standards and requirements. The risk of substitution remains relatively low due to the critical nature of vehicle safety systems, but companies must continuously innovate to maintain their competitive edge and meet changing customer preferences. The integration of automotive safety technology is crucial for meeting these demands.

United States Automotive Collision Avoidance Systems Industry Leaders

-

Continental AG

-

Robert Bosch

-

ZF Friedrichshafen AG

-

Mobileye

-

Denso

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

June 2020: Continental AG invested USD 120 million to establish a new ADAS system manufacturing plant in Texas. In September 2020, it collaborated with AEye to enhance its LiDAR technology-based product range.

November 2020: Robert Bosch GmbH joined forces with Hunter Engineering to offer advanced driver assistance systems in North America.

January 2021: Denso Corporation partnered with Aeva, a US-based LiDAR and perception systems company, to develop cutting-edge sensing and perception systems.

United States Automotive Collision Avoidance Systems Market Report Scope

Automotive collision avoidance systems are advanced safety technologies designed to prevent or mitigate accidents on the road. They use various sensors and communication tools to monitor the surroundings and provide warnings or automatic interventions to help drivers avoid potential collisions with other vehicles, pedestrians, or obstacles.

The United States automotive collision avoidance systems market is segmented by function type (adaptive, automated, monitoring, and warning), technology type (radar, LiDAR, camera, and ultrasonic), vehicle type (passenger cars and commercial vehicles), and state (California, Texas, Florida, New York, Ohio, and rest of the United States).

The report offers market size and forecasts for the US automotive collision avoidance systems in volume and value (USD) for all the above segments.

Function Type

| Adaptive |

| Automated |

| Monitoring |

| Warning |

Technology Type

| Radar |

| LiDAR |

| Camera |

| Ultrasonic |

Vehicle type

| Passenger Cars |

| Commercial Vehicles |

State

| California |

| Texas |

| Florida |

| New York |

| Ohio |

| Rest of the United States |

| Function Type | Adaptive |

| Automated | |

| Monitoring | |

| Warning | |

| Technology Type | Radar |

| LiDAR | |

| Camera | |

| Ultrasonic | |

| Vehicle type | Passenger Cars |

| Commercial Vehicles | |

| State | California |

| Texas | |

| Florida | |

| New York | |

| Ohio | |

| Rest of the United States |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current United States Automotive Collision Avoidance Systems Market size?

The United States Automotive Collision Avoidance Systems Market is projected to register a CAGR of 5.26% during the forecast period (2025-2030)

Who are the key players in United States Automotive Collision Avoidance Systems Market?

Continental AG, Robert Bosch, ZF Friedrichshafen AG, Mobileye and Denso are the major companies operating in the United States Automotive Collision Avoidance Systems Market.

What years does this United States Automotive Collision Avoidance Systems Market cover?

The report covers the United States Automotive Collision Avoidance Systems Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United States Automotive Collision Avoidance Systems Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: