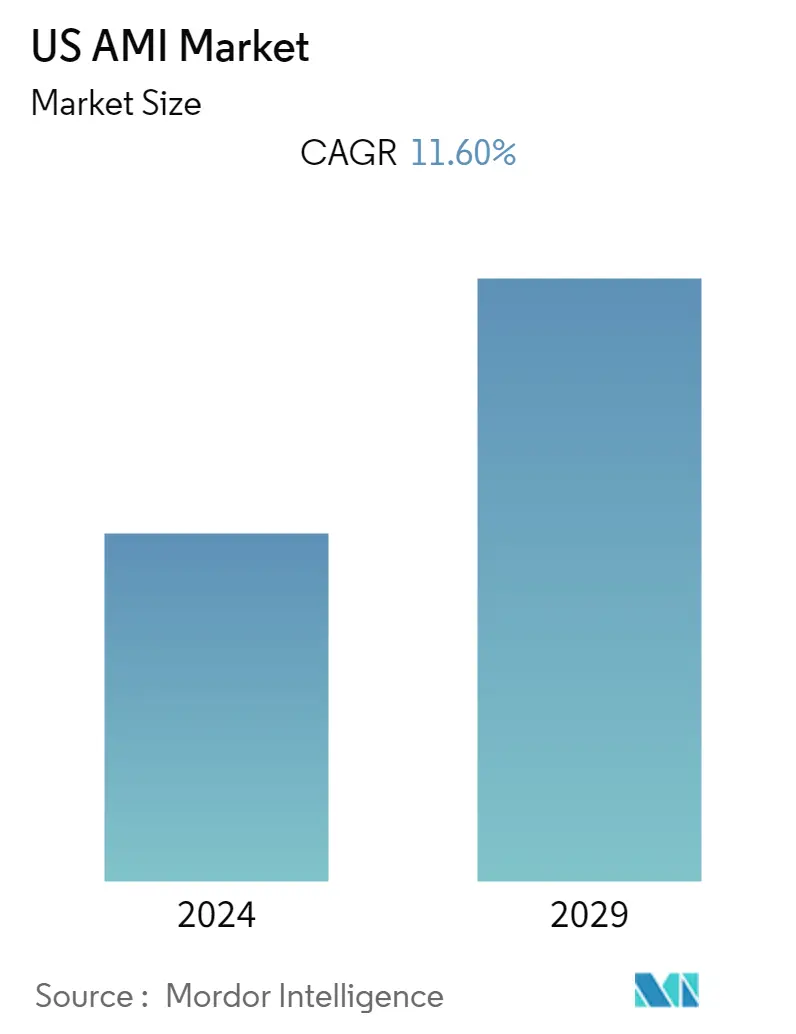

Market Size of US AMI Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | 11.60 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

US Advanced Metering Infrastructure (AMI) Market Analysis

The United States Advanced Metering Infrastructure (AMI) Market is expected to register a CAGR of 11.6% during the forecast period. Smart Meters represent a transformative technology for the utility industry. These technologically advanced meters provide greater insight into the usage of energy. Smart Meters have been employed as a part of advanced metering infrastructure development initiatives worldwide.

- The development of an integrated, IT-enabled power grid and other pattern analysis support software benefits users greatly. This kind of grid, also known as a "smart grid," aids in increasing distributed production while lowering costs, fostering energy efficiency, and improving the overall security and dependability of the production, transmission, and distribution system. AMI must be used in all smart grid initiatives.

- The COVID-19 outbreak has boosted market growth because the energy and utility sectors provide critical services, forcing the industry to reconsider how it conducts business and interacts with both its employees and customers. However, as the pandemic impacted industrial and commercial work sites and altered load patterns, utilities' critical role in supplying energy to society changed.

- The United States is the region's key player, with the largest driver of the smart meters market, due to the American Recovery and Reinvestment Act (ARRA), which included funding for the Smart Grid Investment Grant (SGIG) program. The high demand for smart meters will drive the demand for the Advanced Metering Infrastructure market in the United States.

- The number of houses in the United States represents the potential market scope for utilities providing gas, and as new homes are built, sales of smart gas meters are expected to rise. Manufacturers of smart gas meters in the United States are hoping to capitalize on this opportunity as demand grows.

- As more new homes are built, an increasing proportion of them will have smart meters installed as part of AMI, extending its widespread adoption. According to the Institute for Electric Innovation, 107.0 million smart meters will be installed in the United States by the end of 2020. Furthermore, according to EEI, AMI will be available to nearly 70% of US customers by 2021.

- Furthermore, the American Recovery and Reinvestment Act (ARRA) funding for the Smart Grid Investment Grant (SGIG) program has bolstered the United States' advanced metering infrastructure. The widespread use of AMI in newly constructed homes is expected to fuel demand for smart meters in the country.

- However, Advanced Metering Infrastructure (AMI) project implementation success is far more difficult to achieve than technology success and should be the primary focus of any utility embarking on an AMI journey. Failure to meet schedule milestones, failure to meet utility expectations and requirements, poor coordination of necessary implementation tasks, and a lack of readiness to accept the organizational changes imposed by AMI systems are all common challenges for AMI projects.

US Advanced Metering Infrastructure (AMI) Industry Segmentation

Advanced Metering Infrastructure (AMI) facilitates two-way communication and gives system operators an IT-enabled interface with consumers in both the residential and commercial sectors. Another key driver for adopting AMI and smart grid technology is reducing energy theft. The residential, commercial, and industrial sectors use AMI's various products and services, including smart meters, meter communication infrastructure, and data management.

The scope of the report covers various segments that are segmented by type (smart metering devices, solutions, services), and end-user (residential, commercial, industrial). The study also indicates the impact of COVID-19 on the United States' AMI market.

| Type | ||||||||

| Smart Metering Devices (Electricity, Water, and Gas) | ||||||||

| ||||||||

| Services (Professional - Program Management, Deployment and Consulting and Managed) |

| End-user | |

| Residential | |

| Commercial | |

| Industrial |

US AMI Market Size Summary

The United States Advanced Metering Infrastructure (AMI) market is poised for significant growth, driven by the increasing adoption of smart meters and the development of integrated, IT-enabled power grids. These smart meters are pivotal in transforming the utility industry by providing detailed insights into energy usage, enhancing energy efficiency, and improving the security and reliability of energy systems. The market's expansion is further supported by initiatives like the American Recovery and Reinvestment Act, which has facilitated funding for smart grid projects. The digitalization of the electrical grid, coupled with smart city initiatives, is creating lucrative opportunities for AMI deployment across the country. However, the high costs associated with smart meter installation and the challenges in project implementation pose potential barriers to market growth.

The market landscape is moderately fragmented, with key players like Itron Inc., IBM Corporation, and Cisco Systems Inc. actively contributing to the development and deployment of AMI solutions. Recent collaborations and projects, such as those in Texas and Minnesota, highlight the ongoing efforts to enhance metering infrastructure and integrate advanced technologies. The shift from traditional meters to smart meters is expected to streamline operations for utility companies, reduce labor costs, and provide accurate real-time data for better resource management. As more homes and businesses adopt smart meters, the demand for AMI solutions is anticipated to rise, supported by the growing emphasis on energy efficiency and sustainability in the United States.

US AMI Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Value Chain Analysis

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Threat of New Entrants

-

1.3.2 Bargaining Power of Buyers

-

1.3.3 Bargaining Power of Suppliers

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 Type

-

2.1.1 Smart Metering Devices (Electricity, Water, and Gas)

-

2.1.2 Solution

-

2.1.2.1 Meter Communication Infrastructure (Solution)

-

2.1.2.2 Software

-

2.1.2.2.1 Meter Data Management

-

2.1.2.2.2 Meter Data Analytics

-

2.1.2.2.3 Other Software Types

-

-

-

2.1.3 Services (Professional - Program Management, Deployment and Consulting and Managed)

-

-

2.2 End-user

-

2.2.1 Residential

-

2.2.2 Commercial

-

2.2.3 Industrial

-

-

US AMI Market Size FAQs

What is the current US AMI Market size?

The US AMI Market is projected to register a CAGR of 11.60% during the forecast period (2024-2029)

Who are the key players in US AMI Market?

Itron Inc., IBM Corporation, Cisco Systems Inc., Mueller Systems LLC and Oncor Electric Delivery Company LLC are the major companies operating in the US AMI Market.