Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

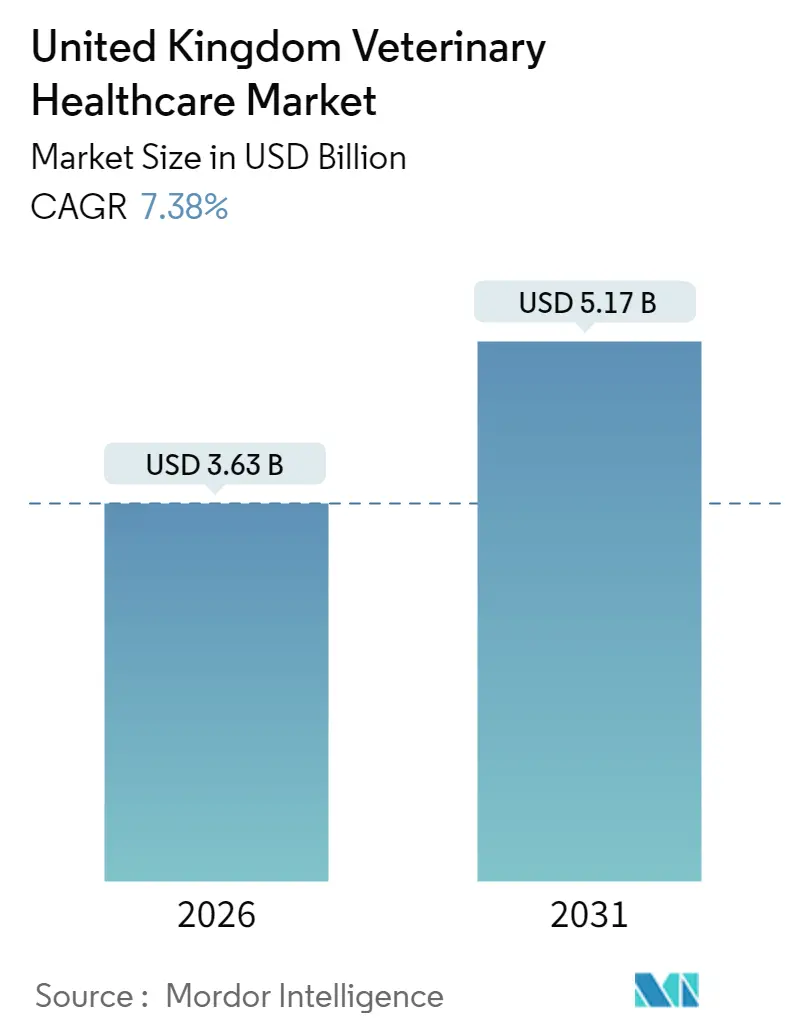

| Market Size (2026) | USD 3.63 Billion |

| Market Size (2031) | USD 5.17 Billion |

| Growth Rate (2026 - 2031) | 7.38% CAGR |

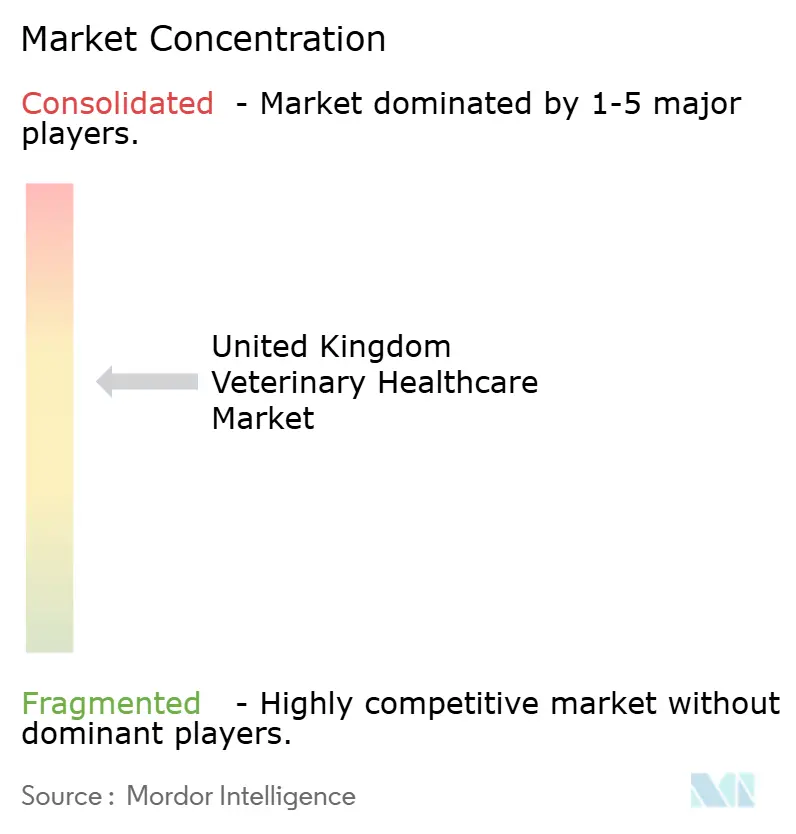

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Veterinary Healthcare Market Analysis by Mordor Intelligence

The United Kingdom veterinary healthcare market was valued at USD 3.38 billion in 2025 and estimated to grow from USD 3.63 billion in 2026 to reach USD 5.17 billion by 2031, at a CAGR of 7.38% during the forecast period (2026-2031). Companion animal ownership has risen to 60% of households, a structural demand driver that cushions the market against Brexit-related supply realignments. Consolidation among practice groups strengthens purchasing power and accelerates technology adoption, yet it intensifies regulatory scrutiny aimed at protecting consumer choice. Rapid upgrades in point-of-care testing, artificial intelligence (AI) diagnostics and long-acting parasiticides elevate clinical standards while widening revenue streams for practices. Meanwhile, livestock operators expand biosecurity programs in response to repeated H5N1 alerts, anchoring steady volumes for vaccines and surveillance services.

Key Report Takeaways

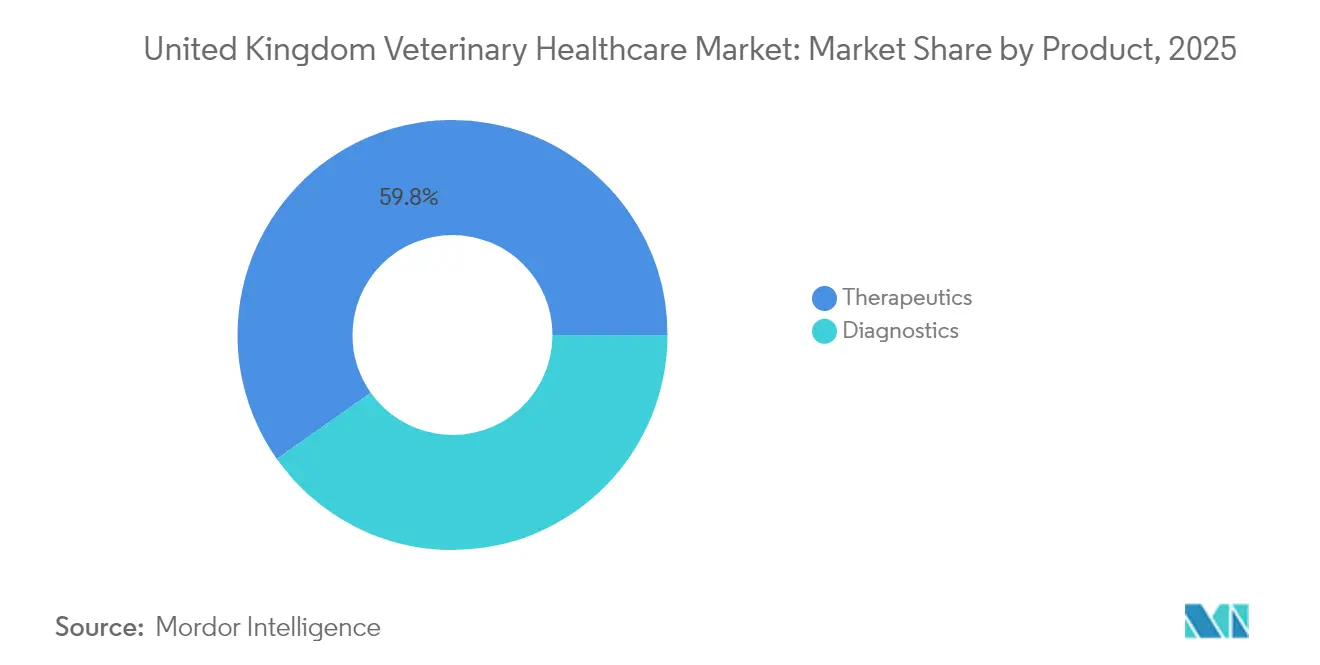

- By product, therapeutics led with 59.78% of the United Kingdom veterinary healthcare market share in 2025; diagnostics is forecast to register a 7.59% CAGR to 2031.

- By animal type, dogs and cats accounted for 44.86% of the United Kingdom veterinary healthcare market size in 2025, while poultry is advancing at an 7.93% CAGR through 2031.

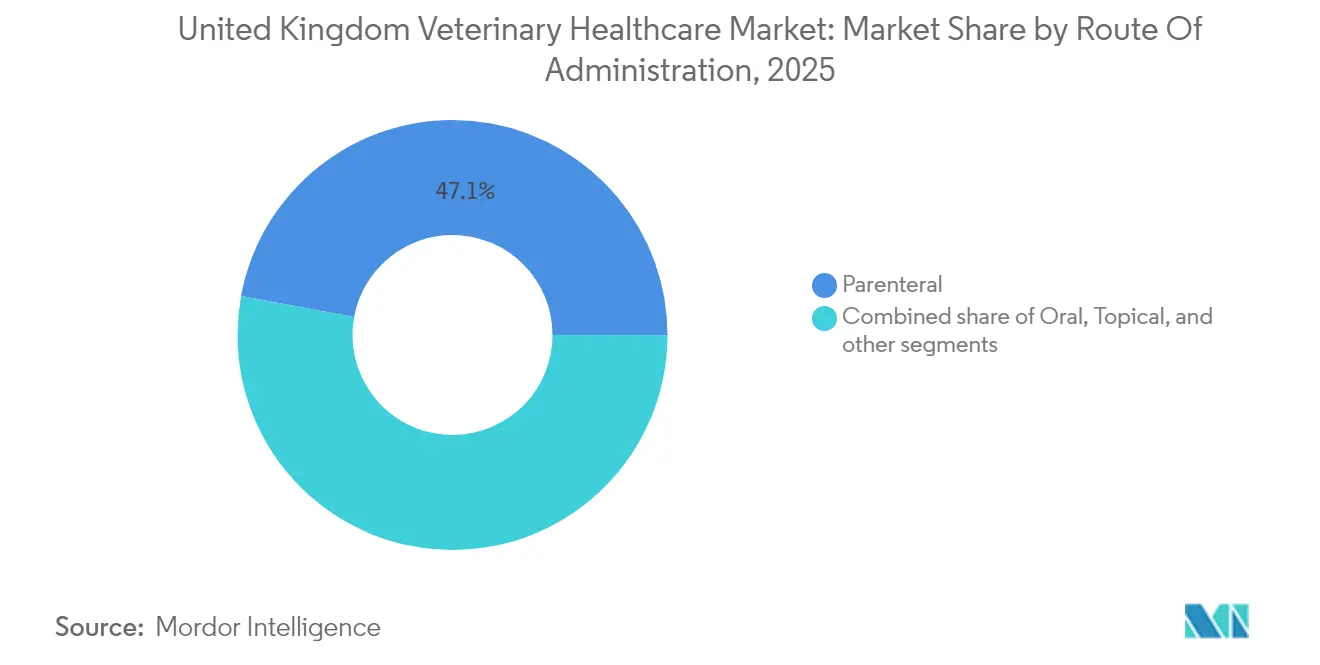

- By route of administration, parenteral delivery commanded 47.10% share of the United Kingdom veterinary healthcare market size in 2025; oral formulations are expanding at a 7.68% CAGR to 2031.

- By end user, veterinary hospitals and clinics held 55.88% revenue share in 2025, whereas point-of-care settings record the fastest projected CAGR at 8.43% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Veterinary Healthcare Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in veterinary therapeutics and diagnostics | +1.8% | UK-wide, strongest in urban hubs | Medium term (2-4 years) |

| Growing companion animal ownership and expenditure | +2.1% | UK-wide, highest in Southeast England | Long term (≥4 years) |

| Rising livestock health management needs amid zoonotic risks | +1.2% | Rural UK; Scotland, Wales focus | Short term (≤2 years) |

| Expansion of corporate veterinary practice networks | +1.5% | Major metropolitan areas nationwide | Medium term (2-4 years) |

| Increasing adoption of pet insurance and wellness plans | +1.3% | UK-wide, pronounced in London & Midlands | Medium–long term (3-5 years) |

| Government and regulatory support for One-Health initiatives | +1.0% | UK-wide, with public-sector concentration | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements In Veterinary Therapeutics and Diagnostics

AI-enabled platforms such as Zoetis’ Vetscan Imagyst now provide on-site cytology in minutes, freeing scarce clinicians for higher-value tasks and reducing diagnostic error rates. Portable infrared thermography and wearable sensors extend continuous monitoring for livestock, triggering early alerts that curb herd-level losses[1]UK Government, “Veterinary Medicines (Amendment etc.) Regulations 2024,” gov.uk. Integrated telemedicine portals tethered to in-clinic devices foster hybrid workflows that expand reach into rural communities. IDEXX’s inVue analyzer shows how modular chemistry, hematology and urinalysis stations compress full laboratory capability into countertop space, enabling same-visit treatment decisions. Long-acting parasiticides such as MSD’s BRAVECTO chewable extend dose intervals to 12 weeks, reinforcing owner compliance while moderating antimicrobial use.

Growing Companion Animal Ownership and Expenditure

Seventeen-point-two million UK households housed a pet in 2024, with the dog and cat population growing by 1.5 million annually. Owners treat animals as family members, elevating demand for oncology, orthopedic and behavioral services once confined to human medicine. Men now account for 27% of adult-cat adoptions versus 18% for women, shifting product and service preferences toward technology-driven convenience[2]UK Pet Food, “Pet Population Survey 2024,” ukpetfood.org. Aged pets require chronic disease management, extending lifetime spend per animal. Emotional capital forged during pandemic lockdowns sustains willingness to finance premium diagnostics, fueling revenue beyond pure volume growth.

Rising Livestock Health Management Needs Amid Zoonotic Risks

The government raised its H5N1 pandemic threat rating to Level 4 in 2024, reinforcing the strategic link between animal and public health. Farm health planning adoption jumped to 73% of holdings, and 85% of those plans were veterinarian-led, up from 65% in 2012. Tight movement controls under the Bluetongue Disease Framework require veterinary certification, increasing on-farm service frequency. Northern Ireland’s dependence on medicines registered in Great Britain compels localized supply solutions to maintain welfare standards amid Brexit-driven distribution frictions.

Expansion Of Corporate Veterinary Practice Networks

Corporate ownership grew from 10% of practices in 2013 to nearly 60% by 2024, catalyzing a Competition and Markets Authority (CMA) investigation into pricing transparency. Mars Petcare’s 2025 purchase of Linnaeus adds referral depth to its first-opinion network, illustrating multilevel integration strategies. CVS Group’s 458-site footprint delivers USD 647.3 million revenue, demonstrating the scale economies that support advanced imaging and specialized surgery investments. Centralized procurement and standard protocols boost clinical consistency, yet the CMA warns of potential consumer harm where local competition erodes.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cost of veterinary services and products | -1.4% | UK-wide, most acute in large cities | Short term (≤2 years) |

| Limited availability of skilled veterinary professionals | -1.1% | Rural UK; Northern England, Scotland | Medium term (2-4 years) |

| Prevalence of counterfeit and sub-standard medicines | -1.0% | Online and informal supply channels nationwide | Short term (≤2 years) |

| Market consolidation impacting supplier bargaining power | -0.8% | UK-wide, especially corporate practice clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Cost of Veterinary Services and Products

Average veterinary invoices have climbed 60% since 2014, amplifying affordability barriers that push some owners to postpone treatments. The Dogs Trust reports clients weighing elective care against budget constraints, signaling elastic demand that could temper overall growth. Forty percent of clinic employees say revenue targets sway clinical decisions, fueling CMA scrutiny. IDEXX noted a 2.1% dip in visit frequency in 2024 despite value gains, highlighting price sensitivity in preventive care segments.

Limited Availability of Skilled Veterinary Professionals

EU-sourced veterinarian registrations fell 68% between 2019 and 2021, tightening labor supply. The Food Standards Agency warns public safety inspections are understaffed, with only one UK national among 30 veterinarians in Food Standards Scotland[3]Food Safety Magazine, “Veterinary shortage threatens inspections,” foodsafetymagazine.com. A new school at Scotland’s Rural College will expand graduate output, yet near-term shortages force practices to cut hours or decline cases, especially in remote areas.

Segment Analysis

By Product: Diagnostics Drive Innovation Despite Therapeutic Dominance

Therapeutics generated 59.78% of United Kingdom veterinary healthcare market share in 2025, reflecting entrenched demand for vaccines, parasiticides and anti-infectives. Diagnostics is growing at a 7.59% CAGR as point-of-care devices and AI analytics shorten the path from sample to therapy. Immunodiagnostics dominate revenue today, while molecular assays scale rapidly for resistance profiling. Portable ultrasound and digital radiography embed in primary care, replacing referrals and unlocking ancillary fees. Within therapeutics, vaccine uptake accelerates on heightened biosecurity awareness, whereas antimicrobial-laden feed additives face regulatory headwinds, nudging manufacturers toward precision nutrition alternatives.

Investment in diagnostics aligns with evidence-based protocols that lower drug overuse and improve outcomes, further anchoring recurring consumables revenue. AI platforms classify cytology slides in under eight minutes, enabling same-day oncology interventions. As practice groups aggregate, bulk procurement of analyzers lowers per-test costs, widening access to advanced assays even in mid-tier clinics.

Note: Segment shares of all individual segments available upon report purchase

By Animal Type: Companion Animals Lead While Poultry Accelerates

Dogs and cats accounted for 44.86% of United Kingdom veterinary healthcare market size in 2025, supported by 13.5 million dogs and 12.5 million cats needing routine, emergency and specialty care. Poultry is projected to expand at an 7.93% CAGR as stringent avian influenza surveillance heightens veterinary oversight across commercial flocks. Equine demand remains stable, fueled by sports and leisure riding, while ruminant health programs gain traction under climate-adaptation pressures. Swine operators adopt modern traceability, yet African swine fever vigilance keeps veterinary certification volumes high.

Pet humanization drives uptake of chemotherapy, MRI scans and behavioral therapies, elevating average spend per visit. Poultry producers embed veterinarians in biosecurity governance, reducing downtime costs from disease outbreaks. Cross-species H5N1 transmission to sheep in 2024 underlines growing need for multi-species surveillance frameworks.

By Route Of Administration: Oral Delivery Gains Despite Parenteral Leadership

Parenteral formats held 47.10% of United Kingdom veterinary healthcare market share in 2025, favored for rapid response in emergencies and mass immunizations. Oral products are progressing at a 7.68% CAGR as chewables and palatable tablets boost owner compliance. Topical innovations extend flea and tick control durations, while inhalation and implantable devices represent niches for chronic therapies. Long-duration molecules slash dosing frequency, lessening stress for pets and farm animals alike. In livestock, injectables retain primacy because uniform dosing ensures herd-wide protection during outbreaks.

Convenience-oriented owners endorse once-quarterly oral parasiticides that pair efficacy with ease, a model likely to migrate into preventive antibiotics should antimicrobial stewardship allow. Meanwhile, injectable formulations anchor large-animal procedures where precise dosing and rapid kinetics outweigh administration discomfort.

Note: Segment shares of all individual segments available upon report purchase

By End User: Point-Of-Care Testing Transforms Traditional Practice Models

Veterinary hospitals and clinics generated 55.88% revenue in 2025, spanning general practice, referral and emergency settings. Point-of-care facilities are forecast to clock an 8.43% CAGR, enabled by compact analyzers that slash turnaround from days to minutes. Reference laboratories keep relevance for complex assays such as PCR panels and histopathology, while academia supports evidence generation and specialist training.

In-house testing ecosystems tie hardware, reagents and cloud analytics, creating high-margin, recurring consumables streams. Corporate owners exploit volume discounts to outfit each site with integrated hematology, chemistry and urinalysis modules, standardizing protocols network-wide. Teleconsultation overlays permit specialists to review live data, widening geographic reach without physical expansion.

Geography Analysis

England, especially the Southeast, anchors companion-animal revenues, reflecting density of pet owners and strong disposable income. Scotland emphasizes livestock services; its new veterinary school addresses chronic workforce gaps and fosters research into food-animal medicine. Wales concentrates on sheep programs funded under endemic disease follow-up schemes, while Northern Ireland grapples with Brexit-linked supply risks because 85% of its animal medicines are registered in Great Britain. Rural regions nationwide face clinician shortages that constrain large-animal services despite rising demand. Urban clusters benefit from corporate consolidation, enabling MRI suites and 24-hour emergency centers, although price disparities widen between city and countryside.

The island nation’s natural sea borders aid biosecurity yet complicate logistics when outbreaks arise, necessitating swift import controls, as evidenced after Hungarian foot-and-mouth detections in 2024. Climate stresses hit southern counties first, lengthening parasite seasons and driving earlier vaccination cycles, whereas northern areas tackle respiratory issues in colder, wetter conditions.

Competitive Landscape

The market is moderately consolidated. CVS Group, IVC Evidensia, Pets at Home and Mars Petcare’s Linnaeus dominate corporate practice ownership, giving them leverage in procurement and tech deployment. Mars deepened its referral network in July 2025 via Linnaeus, combining oncology, neurology and cardiology specialists under one umbrella.

CVS invested in AI triage software and a home-delivery pharmacy, reinforcing seamless client experience. IVC Evidensia pilots mobile clinics to reach underserved rural zones. Diagnostic giants Zoetis and IDEXX partner with corporate chains to embed proprietary analyzers, locking in reagent revenues and data subscriptions.

Regulators intervene to keep pricing in check. The CMA’s ongoing investigation could mandate transparent fee disclosures and generic prescription options, potentially reshaping revenue models. Meanwhile, pharmaceutical players extend into services: MSD’s BRAVECTO marketing couples product with practice education, and Elanco aligns with Medgene on H5N1 vaccines poised for UK launch.

United Kingdom Veterinary Healthcare Industry Leaders

Boehringer Ingelheim

MSD Animal Health

Virbac Corporation

Ceva Santé Animale

Elanco Animal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Mars Petcare completed its acquisition of Linnaeus Group, adding five referral centers and 82 first-opinion sites to its U.K. network and deepening vertical integration across the country’s veterinary services landscape.

- June 2025: Zoetis introduced the AI Masses cytology module for the Vetscan Imagyst analyzer nationwide, giving U.K. clinics real-time slide interpretation and accelerating the shift toward AI-enabled point-of-care diagnostics.

- April 2025: The Veterinary Medicines Directorate cleared MSD Animal Health’s latest BRAVECTO chewable for canine parasite control.

- April 2025: The Veterinary Medicines Directorate authorized MSD Animal Health’s latest BRAVECTO chewable, extending 12-week oral parasite protection for dogs and broadening treatment options for U.K. companion-animal practitioners.

- January 2025: The updated Veterinary Medicines (Amendment etc.) Regulations removed marketing-authorization renewals and strengthened pharmacovigilance rules, modernizing oversight of all animal-health products sold in the United Kingdom.

- January 2025: Merck Animal Health obtained global rights to the VECOXAN parasiticide brand, bolstering its ruminant-health line in the United Kingdom.

United Kingdom Veterinary Healthcare Market Report Scope

As per the report's scope, veterinary healthcare can be defined as the science associated with diagnosing, treating, and preventing animal diseases. The increasing importance of the production of livestock animals is generating growth in the veterinary healthcare market. The UK veterinary healthcare market is segmented by product and animal type. The product segment is further segmented into therapeutics and diagnostics. The therapeutics segment is further segmented into vaccines, parasiticides, anti-infectives, medical feed additives, and other therapeutics, while the diagnostic segment is divided into immunodiagnostic tests, molecular diagnostics, diagnostic imaging, clinical chemistry, and other diagnostics. The animal type segment is further divided into dogs and cats, horses, ruminants, swine, poultry, and other animals. The report offers the value (USD) for the above segments.

By Product

| Therapeutics | Vaccines |

| Parasiticides | |

| Anti-Infectives | |

| Medical Feed Additives | |

| Other Therapeutics | |

| Diagnostics | Immunodiagnostic Tests |

| Molecular Diagnostics | |

| Diagnostic Imaging | |

| Clinical Chemistry | |

| Other Diagnostics |

By Animal Type

| Dogs & Cats |

| Horses |

| Ruminants |

| Swine |

| Poultry |

| Other Animal Types |

By Route Of Administration

| Oral |

| Parenteral |

| Topical |

| Other Route of Administrations |

By End User

| Veterinary Hospitals & Clinics |

| Reference Laboratories |

| Point-Of-Care / In-House Testing Settings |

| Academic & Research Institutes |

| By Product | Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-Infectives | ||

| Medical Feed Additives | ||

| Other Therapeutics | ||

| Diagnostics | Immunodiagnostic Tests | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Clinical Chemistry | ||

| Other Diagnostics | ||

| By Animal Type | Dogs & Cats | |

| Horses | ||

| Ruminants | ||

| Swine | ||

| Poultry | ||

| Other Animal Types | ||

| By Route Of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| Other Route of Administrations | ||

| By End User | Veterinary Hospitals & Clinics | |

| Reference Laboratories | ||

| Point-Of-Care / In-House Testing Settings | ||

| Academic & Research Institutes | ||

Key Questions Answered in the Report

How large is the United Kingdom veterinary healthcare market in 2026?

It is valued at USD 3.63 billion, with a 7.38% CAGR projected through 2031.

Which product category is expanding fastest?

Diagnostics registers the highest growth at a 7.59% CAGR, outpacing therapeutics.

Why is poultry health spending rising quickly?

Sustained avian influenza surveillance and tighter biosecurity rules push poultry segment growth at an 7.93% CAGR.

What is driving the shift toward point-of-care testing in clinics?

Compact analyzers deliver lab-quality results in minutes, improving treatment speed and client satisfaction while generating recurring consumables revenue.

How is consolidation affecting vet service pricing?

Corporate practice ownership near 60% draws CMA scrutiny as fees rise, creating calls for greater transparency.

Page last updated on: