Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

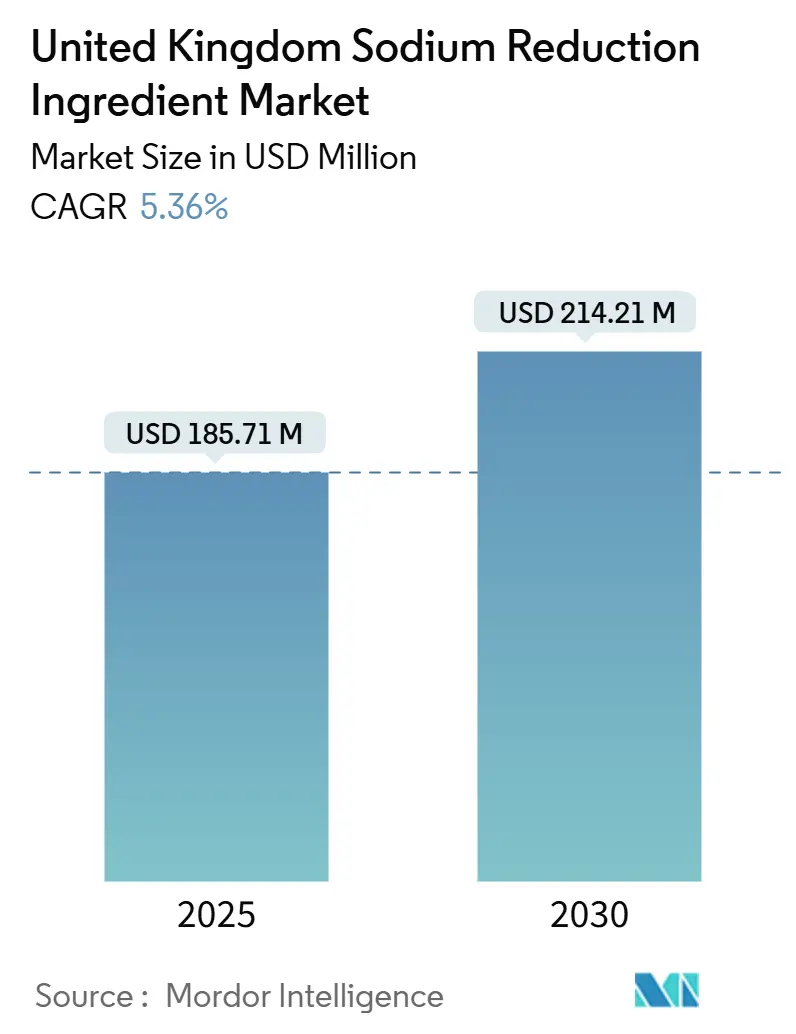

| Market Size (2025) | USD 185.71 Million |

| Market Size (2030) | USD 214.21 Million |

| Growth Rate (2025 - 2030) | 5.36% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Sodium Reduction Ingredient Market Analysis by Mordor Intelligence

The United Kingdom Sodium Reduction Ingredients market size stands at USD 185.71 million in 2025 and is projected to climb to USD 214.21 million by 2030, advancing at a 5.36% CAGR. Growth is anchored in public-health targets that seek to trim average salt intake to 6 grams a day, combined with technology that lets manufacturers offset the loss of sodium’s functional roles in flavor, preservation, and texture. Progress has accelerated as food makers react to an April 2025 Food Standards Agency review that warned of mandatory limits after more than half of ready meals missed voluntary targets. Reformulation now blends mineral salts and yeast extracts with flavor-masking peptides, while patent-protected delivery systems hold strategic value. Although inflation has widened the cost gap between mainstream and better-for-you products, consumers in premium channels continue to reward clean-label claims, giving natural sources extra momentum.

Key Report Takeaways

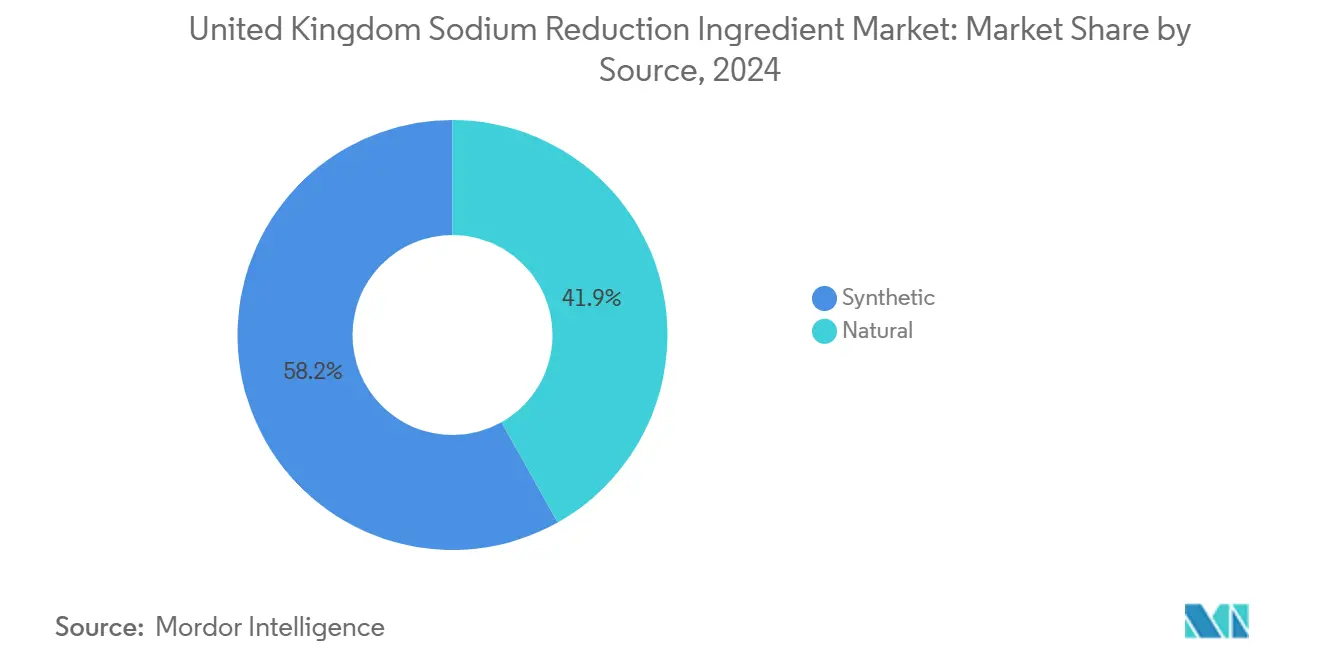

- By source, synthetic ingredients held 58.15% of the United Kingdom Sodium Reduction Ingredients market share in 2024, while natural alternatives are the fastest-growing segment at a 7.14% CAGR through 2030.

- By type, mineral salts accounted for 45.28% of the United Kingdom Sodium Reduction Ingredients market size in 2024, and yeast extracts are on track for a 6.15% CAGR to 2030.

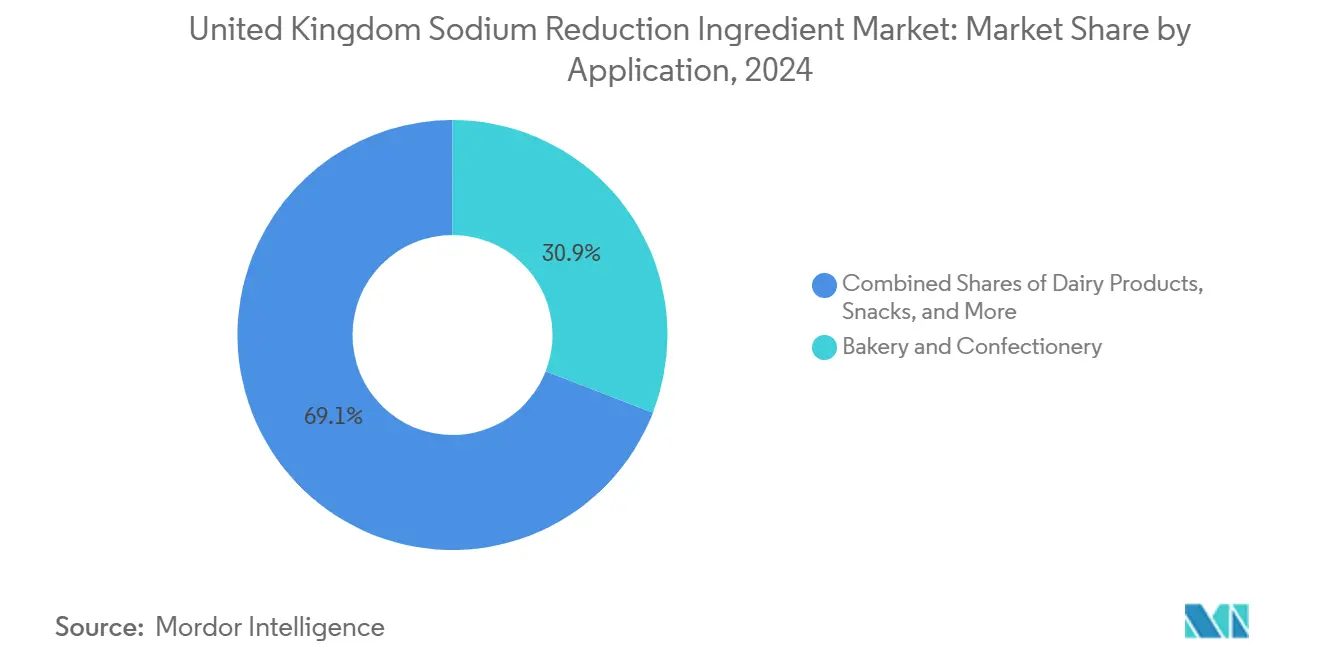

- By application, bakery and confectionery captured 30.89% of 2024 revenue, and meat products are advancing at a 6.82% CAGR over the forecast period.

United Kingdom Sodium Reduction Ingredient Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of Cardiovascular Diseases | +1.2% | National, with acute pressure in high-deprivation regions | Medium term (2-4 years) |

| Advancements in Salt Reduction Technologies and Ingredients | +1.0% | National, with early adoption in premium food segments | Short term (≤ 2 years) |

| Increasing Applications in Ready Meals and Convenience Foods | +0.8% | National, concentrated in urban retail channels | Medium term (2-4 years) |

| Rising Popularity of Functional and Better-For-You Snacks | +0.7% | National, skewed toward higher-income demographics | Medium term (2-4 years) |

| Food Reformulation in High-Consumption Food Categories | +0.9% | National, spanning bakery, meat, and dairy sectors | Long term (≥ 4 years) |

| Product Innovation in Multifunctional Ingredients | +0.6% | National, led by large-scale manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Cardiovascular Diseases

Cardiovascular disease remains the leading cause of death in the United Kingdom. As of 2024, the British Heart Foundation reports that excessive sodium intake contributes to hypertension in approximately 14 million adults[1]Source: British Heart Foundation, “UK Cardiovascular Disease Statistics 2024,” bhf.org.uk. This health issue imposes significant economic strain on the National Health Service, not only through direct healthcare costs but also due to productivity losses caused by CVD-related absenteeism and premature deaths. Public Health England introduced salt reduction targets in 2024 for 84 food categories, encouraging manufacturers to focus on ingredient innovation rather than simply diluting recipes. Recognizing the established link between dietary sodium and blood pressure, the Food Standards Agency now prioritizes reformulation efforts over consumer education, as voluntary behavior changes have reached a plateau. A 2024 study published in the Institute for Fiscal Studies journal found that between 2005 and 2011, the salt content in processed foods decreased by only 5.1%, with progress stagnating afterward, emphasizing the need for technological advancements instead of incremental changes.

Advancements in Salt Reduction Technologies and Ingredients

In 2025, peer-reviewed research highlighted yeast extracts as the preferred solution for sodium reduction. The study identified compounds such as glutamic acid, aspartic acid, and citric acid, which, at specific concentrations, enhance saltiness perception. This enables a sodium reduction of 10% to 40% without noticeable changes for consumers (source: frontiersin.org). The mechanism works by activating umami receptors through glutamate and nucleotides (5'-inosinate and 5'-guanylate), which amplify saltiness even at reduced sodium chloride levels. This approach differs significantly from potassium chloride substitution, which, at replacement ratios exceeding 30%, introduces metallic off-notes. These off-notes require flavor-masking agents, adding complexity to formulations. In 2024, Kerry Group introduced its TasteSense Savoury Solutions, combining yeast-extract platforms with mineral-salt blends. This innovation targets bakery and snack markets, where formulation changes can affect texture and browning. Yeast extracts offer a competitive advantage through their multifunctionality. In addition to sodium reduction, they provide natural preservation. Peptide fractions in yeast extracts inhibit Listeria and Salmonella, reducing the need for synthetic antimicrobials, which often raise clean-label concerns.

Increasing Applications in Ready Meals and Convenience Foods

In April 2025, Action on Salt's survey underscored the reformulation challenges in the ready meals category. The survey revealed that over 50% of the products analyzed exceeded the Food Standards Agency's voluntary salt targets, with some containing more than 3 grams of salt per serving. Sodium is essential in convenience foods for preservation during chilled transport, masking the flavors of reheated ingredients, and retaining moisture in microwave-reheated formats. This dependency creates a significant challenge for manufacturers: reducing sodium levels below 1.5 grams per 100 grams (the threshold for "high salt" front-of-pack labeling) often necessitates higher water activity. This increase can accelerate microbial growth, cutting shelf life from 7 days to 4 days unless additional preservatives are used. Potassium lactate has emerged as a popular alternative due to its dual functionality. It provides antimicrobial properties and moisture retention while replacing up to 25% of sodium chloride. However, this substitution comes at a cost, adding GBP 2 to GBP 4 (USD 2.50 to USD 5) per kilogram compared to conventional salt, as noted by the Food Standards Agency[2]Source: Food Standards Agency, “Voluntary Salt Reduction Programme,” food.gov.uk.

Rising Popularity of Functional and Better-For-You Snacks

In 2024, the UK snacks market, valued at GBP 3.8 billion (USD 4.8 billion), is undergoing a division between value-focused mainstream products and premium "better-for-you" options, which carry a 15% to 20% price premium. From 2018 to 2023, Walkers, a PepsiCo subsidiary, reduced salt content by 25% across its product range through gradual reformulation, effectively avoiding noticeable changes in taste (pepsico.com). A March 2025 survey by Action on Salt found that 85% of crisps, nuts, and popcorn meet voluntary salt targets. However, savoury popcorn lags behind, with only 60% compliance, indicating technical challenges specific to the category. The primary insight is that consumers are willing to pay more for health-oriented products, which helps offset the higher cost of yeast extracts compared to table salt. This premium positioning succeeds in segments where health claims influence purchasing decisions, while mainstream value products continue to rely on cost-effective mineral-salt substitutes.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevanca | Impact Timeline |

|---|---|---|---|

| Potential Off-taste and Texture Changes | -0.8% | National, acute in bakery and meat applications | Short term (≤ 2 years) |

| Food Affordability and Socioeconomic Equity Barriers | -0.6% | National, disproportionate in lower-income regions | Medium term (2-4 years) |

| Regulatory Compliance Burdens on Labeling and Additive Approvals | -0.4% | National, concentrated among SME manufacturers | Long term (≥ 4 years) |

| Limited Shelf-life and Stability Issues | -0.5% | National, critical in chilled ready meals and processed meat | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Potential Off-taste and Texture Changes

Potassium chloride, the primary mineral salt substitute, produces bitter and metallic off-notes when it replaces more than 30% to 40% of total sodium chloride. This sensory limitation restricts formulation flexibility. For instance, in bread reformulation, sodium chloride is essential for gluten development, yeast fermentation rates, and Maillard browning reactions. Reducing sodium chloride levels below 1.2% (based on flour weight) abruptly leads to a denser crumb structure and a lighter crust. In the UK, bakers have adopted a phased reduction strategy—cutting sodium by 10% to 20% over 18 to 24 months—to allow consumers to adjust their taste preferences. However, this extended timeline conflicts with regulatory pressures. Reformulating cheese presents even tougher challenges. Sodium is critical for curd formation, moisture removal, and flavor development during aging. Reduced-sodium cheese often results in a rubbery texture and bland flavor, limiting its appeal to a niche, health-conscious audience. The key takeaway is that effective reformulation requires a combination of ingredient systems—such as yeast extracts, herb extracts, and fermented components—rather than a single substitute. This method, while effective, increases formulation costs and adds technical challenges.

Food Affordability and Socioeconomic Equity Barriers

In 2024, the cost of sodium reduction ingredients was 2 to 5 times higher than that of conventional salt. For example, yeast extracts were priced between USD 6.30 and USD 18.90 per kilogram, compared to table salt's range of USD 0.25 to USD 0.63. This price gap resulted in a 5% to 10% increase in finished-product prices. These increases disproportionately impacted lower-income households, who were already dealing with a 25% rise in food prices between 2021 and 2023. The issue is particularly severe in high-deprivation regions, where cardiovascular disease (CVD) prevalence is higher, and price sensitivity is greater. This creates a challenging paradox: the populations most in need of sodium reduction are the least able to afford reformulated products. A 2024 study by the Institute for Fiscal Studies further revealed that the lowest-income households spend 15% of their budgets on food, compared to just 8% for the highest-income households. Policymakers face a critical decision: either mandate product reformulations, spreading the costs across all consumers, or subsidize healthier options, which would require significant fiscal resources. A government review in January 2025 indicates a preference for the former approach.

Segment Analysis

By Source: Natural Gains Ground Despite Cost Premium

Natural sources, priced 2 to 3 times higher than synthetic alternatives, are projected to grow at 7.14% annually through 2030, driven by clean-label preferences in premium food categories. In 2024, synthetic ingredients held 58.15% of the market share due to their cost-efficiency and technical performance in less scrutinized applications like industrial bakery and processed meat. Monosodium glutamate (MSG), labeled as E621 under UK/EU regulations, provides umami flavor with one-third the sodium content of table salt but faces consumer perception challenges despite approval by the Food Standards Agency under "quantum satis" principles food.gov.uk. Manufacturers increasingly prefer "yeast extract" labels over synthetic nucleotides like disodium inosinate (IMP) and disodium guanylate (GMP) to convey naturalness.

Consumers are willing to pay premiums for recognizable ingredients, supported by front-of-pack labels highlighting "no artificial additives." Natural yeast extracts, derived from Saccharomyces cerevisiae fermentation, deliver glutamic acid and nucleotides similar to synthetic versions while meeting clean-label standards. Lallemand Inc. and ABF Ingredients Group (Ohly GmbH) lead the natural yeast-extract market, using proprietary fermentation strains and autolysis techniques to maximize glutamate yields lallemand.com. Herb and spice extracts like rosemary, sage, and mushroom offer natural alternatives but are limited to savory applications. The natural segment’s 7.14% growth is driven by premiumization in snacks, ready meals, and artisan bakery, while synthetic ingredients dominate cost-sensitive mainstream markets.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Type: Yeast Extracts Outpace Mineral Salts

In 2024, mineral salts held a 45.28% market share, driven by potassium chloride's cost-effective substitution of 25% to 50% of sodium chloride at GBP 1 to GBP 3 (USD 1.26 to USD 3.78) per kilogram. However, its bitterness above 30% replacement ratios requires flavor-masking agents like yeast extracts, trehalose, or amino acids, adding formulation complexity. Calcium chloride supports curd firmness in cheese-making, and magnesium sulfate conditions dough in baking, but their astringent taste limits broader use. The UK Food Standards Agency imposes no restrictions on potassium chloride, unlike jurisdictions concerned about hyperkalemia risks in renal patients, offering formulation flexibility.

Yeast extracts, with a smaller 2024 share, are projected to grow at 6.15% through 2030 as manufacturers focus on multifunctionality. A 2025 study in Frontiers in Nutrition noted yeast extracts enable 10% to 40% sodium reduction, enhance umami, provide natural preservation, and restore browning in reduced-sodium bakery products (source: frontiersin.org). In 2024, Angel Yeast Co., Ltd. expanded production for Europe, while Synergy Flavours introduced encapsulated formats for ready meals, addressing reheating-related taste loss. Amino acids and glutamates, such as MSG, lysine, and glycine, offer moderate-cost technical performance but face consumer perception challenges. Emerging platforms like fermented vegetable extracts and seaweed-derived compounds remain in early commercialization stages.

By Application: Meat Products Accelerate Past Bakery

In 2024, the bakery and confectionery sector accounted for 30.89% of the application share, underscoring bread's prominence as the UK's primary dietary sodium source. With the average person consuming about two slices daily, this translates to roughly 0.8 grams of salt intake. Sodium chloride in bread plays several pivotal roles: it regulates yeast fermentation (with excess sodium hindering yeast activity), bolsters gluten networks for enhanced dough elasticity, and amplifies Maillard reactions, which are crucial for crust color and flavor. UK bakers, as highlighted in a 2024 study from the Journal of Food Science, have successfully reduced sodium content by 20% to 30% through a gradual reformulation approach—cutting salt by 5% annually over 4 to 6 years—ensuring no noticeable change in taste for consumers. On the other hand, while confectionery applications use less sodium, they encounter unique hurdles: sodium bicarbonate, vital for leavening in biscuits and cakes, when substituted with potassium bicarbonate, can impart undesirable soapy flavors if used in excess of 50%.

Forecasted to expand at 6.82% until 2030, meat and meat products face the steepest technical challenges, driving a heightened demand for sophisticated sodium-reduction ingredients. In processed meats, sodium chloride is crucial for curing, binding water, and providing antimicrobial benefits. A 2024 survey by Action on Salt revealed that chilled sliced meats contained an average of 2.09 grams of salt per 100 grams, with just 56% of products hitting voluntary salt targets[3]Source: British Heart Foundation. "UK Cardiovascular Disease Statistics 2024." bhf.org.uk. Potassium lactate has surfaced as a favored alternative, offering antimicrobial benefits and moisture retention, and can replace up to 25% of sodium chloride. However, this comes at an added cost of USD 2.50 to USD 5 per kilogram. Meanwhile, non-thermal preservation methods like high-pressure processing (HPP) and pulsed electric fields (PEF) can diminish sodium dependence, but their hefty capital investment—ranging from USD 625,000 to USD 2.5 million per processing line—restricts their use to larger processors.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

England dominates demand given its larger population and the concentration of ready-meal manufacturers around the Midlands and the South East. Regional bakery hubs in London and the South West contribute a sizable share of mineral-salt consumption, while craft bakeries in urban centers lean toward natural yeast extracts. Northern England shows higher cardiovascular disease rates and thus garners priority in public-health sodium targets, elevating long-term ingredient uptake in chilled savory pies and bread.

Scotland represents a smaller but strategic slice, where meat processors rely on sodium for traditional cured hams and sausages. Early trials with potassium lactate and acetate blends received government grant support, catalyzing adoption among export-oriented producers that supply English retailers. Wales and Northern Ireland have fewer processing plants yet share a high average salt intake, guiding local public-health campaigns that mirror national goals. Smaller manufacturers in these regions tap technical centers opened by ingredient suppliers to bridge R&D gaps.

Across the devolved administrations, differing timelines for adopting mandatory targets create staggered demand curves. England’s move toward binding limits will likely pull Scotland and Wales forward, shortening market adoption lags. The total addressable base grows as convenience-food factories cluster near population centers, driving the United Kingdom Sodium Reduction Ingredients market even in areas where data on regional split is limited. Ingredient suppliers tailor formulations to local recipes, such as oat-based morning goods in Scotland or pork pies in the Midlands, reinforcing regional relevance while still operating within a cohesive national framework.

Competitive Landscape

In the UK sodium reduction ingredients market, global ingredient giants capitalize on economies of scale in R&D, regulatory navigation, and supply-chain integration to lead premium segments. At the same time, regional specialists are tapping into niche opportunities, particularly in fermentation-derived and botanical-extract platforms. For example, Kerry Group's USD 1 billion acquisition of Niacet in December 2024 highlights these trends. This acquisition not only demonstrates vertical integration but also incorporates acetate-based preservation technologies into Kerry's portfolio. These technologies strengthen Kerry's sodium-reduction offerings, enabling meat processors to achieve both extended shelf life and reduced salt content. Meanwhile, the May 2023 merger of DSM and Firmenich has created a powerhouse that combines nutritional-ingredient expertise with flavor-house capabilities. This strategic merger allows them to provide comprehensive reformulation support—from sensory evaluations to regulatory dossier preparations—outperforming smaller competitors.

Patent filings emphasize the industry's focus on flavor-masking innovations. Givaudan SA has secured multiple patents for encapsulation techniques that reduce potassium chloride's bitterness until chewing. Similarly, Tate & Lyle PLC is looking ahead with 2024 patent applications for trehalose-yeast extract combinations, which enhance saltiness at 20% reduced sodium levels. Emerging opportunities lie in cost-effective natural substitutes that can bridge the price gap between synthetic ingredients and premium yeast extracts. While fermented vegetable extracts and mushroom-based compounds show potential in this area, they are still in early commercialization stages. Smaller companies like NuTek Food Science and S Black Ltd. are carving out a niche by serving SME food manufacturers. These manufacturers often face challenges due to the minimum-order requirements of global giants. By offering tailored formulations and technical support, these smaller players provide solutions that larger suppliers cannot economically deliver.

Technology is becoming a critical factor in market positioning. Cargill's strategic USD 75 million investment in 2024, which included fermentation capabilities for yeast-extract production in Indonesian facilities, highlights their ambition to enter natural segments, challenging the European specialists' long-standing dominance. Navigating the regulatory landscape—whether through Food Standards Agency assessments, preparing technical dossiers for E-number applications, or addressing front-of-pack labeling concerns—poses significant challenges. However, for established players with dedicated regulatory teams, these obstacles further reinforce their market position.

United Kingdom Sodium Reduction Ingredient Industry Leaders

-

Tate & Lyle PLC

-

DSM-Firmenich

-

Kerry Group plc

-

ABF Ingredients Group

-

Lallemand Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2024: Brenntag Specialties was appointed by K+S Minerals & Agriculture GmbH as global strategic distributor for three high-purity pharmaceutical salts: APISAL Sodium Chloride (GMP, pharmacopoeia quality, API), Potassium Chloride 99.9% KCl Ph. Eur., USP (API), and HD-NaCl (excipient grade).

- April 2024: Kerry launched Tastesense Salt, designed to deliver salt and savory taste without increasing sodium content. It retains essential flavor properties while replicating the salty impact, body, and linger. This innovation aims to address consumer demand for healthier food options by reducing sodium intake without compromising taste.

United Kingdom Sodium Reduction Ingredient Market Report Scope

Sodium reduction ingredients are products that help lower the sodium levels of food products, while maintaining savory taste in the products.

The United Kingdom sodium reduction ingredients market is segmented by source into natural and synthetic. By type, the market is segmented into mineral salts, amino acids and glutamates, yeast-based ingredients, and others. The market is segmented by application into bakery and confectionery, condiments, seasonings, and sauces, dairy products, meat and meat products, snacks, and others. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Source

| Synthetic |

| Natural |

By Type

| Mineral Salts |

| Amino Acids and Glutamates |

| Yeast-Based Ingredients |

| Others |

By Application

| Bakery and Confectionery |

| Condiments, Seasonings and Sauces |

| Dairy Products |

| Meat and Meat Products |

| Snacks |

| Others |

| By Source | Synthetic |

| Natural | |

| By Type | Mineral Salts |

| Amino Acids and Glutamates | |

| Yeast-Based Ingredients | |

| Others | |

| By Application | Bakery and Confectionery |

| Condiments, Seasonings and Sauces | |

| Dairy Products | |

| Meat and Meat Products | |

| Snacks | |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the United Kingdom Sodium Reduction Ingredients market in 2025?

United Kingdom Sodium Reduction Ingredients market is valued at USD 185.71 million in 2025.

What is the projected CAGR for sodium reduction ingredients sold in the United Kingdom?

The compound annual growth rate is expected at 5.36% between 2025 and 2030.

Which application is growing fastest for sodium reduction ingredients in the United Kingdom?

Meat and meat products lead with a forecast 6.82% CAGR through 2030.

Why are yeast extracts gaining popularity over mineral salts?

Yeast extracts deliver umami, antimicrobial action, and browning precursors together, while avoiding the metallic notes that limit potassium chloride.

Page last updated on: