Market Overview

| Study Period | 2017 - 2028 |

|---|---|

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2028 |

| Market Size (2024) | USD 269.43 Million |

| Market Size (2028) | USD 336.21 Million |

| Growth Rate (2024 - 2028) | 5.69% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Sealants Market Analysis by Mordor Intelligence

The United Kingdom Sealants Market size is estimated at 269.43 million USD in 2024, and is expected to reach 336.21 million USD by 2028, growing at a CAGR of 5.69% during the forecast period (2024-2028).

The United Kingdom sealants industry is experiencing significant transformation driven by evolving technological advancements and sustainability initiatives. The electronics and electrical equipment manufacturing sector has emerged as a crucial end-user segment, with the UK electronics market projected to grow at an annual rate of 7.26% in the coming years. This growth is primarily attributed to the increasing adoption of advanced electronic components in various applications, from consumer electronics to industrial equipment. The rapid digitalization across industries and the growing emphasis on energy-efficient electronic systems have created new opportunities for specialized electronic sealants applications in electronic component protection and insulation.

The healthcare sector has become an increasingly important market for medical sealants, driven by technological innovations in medical device manufacturing and growing healthcare infrastructure investments. The medical technology market is expected to register a CAGR of approximately 5% through 2027, reflecting the increasing demand for advanced medical equipment and devices. The integration of medical sealants in medical device assembly, sterilization processes, and specialized medical equipment manufacturing has created new growth avenues for market participants. The focus on developing biocompatible and sterile sealant solutions has led to significant innovations in product formulations.

The do-it-yourself (DIY) and consumer retail segment has witnessed substantial growth, with the DIY and hardware industry projected to grow at a CAGR of 3.32% through 2027. This growth is driven by changing consumer preferences, increased home improvement activities, and the availability of user-friendly sealant products. The expansion of e-commerce platforms has revolutionized product distribution, making specialized sealant solutions more accessible to individual consumers. Manufacturers are responding by developing innovative packaging solutions and easy-to-use application systems targeted at the consumer market.

Environmental sustainability has emerged as a critical factor shaping the sealant industry landscape, with manufacturers increasingly focusing on developing eco-friendly sealant solutions. The industry has witnessed a significant shift towards low-VOC (volatile organic compounds) formulations and sustainable raw materials. This transformation is driven by stringent environmental regulations and growing consumer awareness about environmental impact. Manufacturers are investing in research and development to create bio-based alternatives and recyclable packaging solutions, while also implementing sustainable production practices to reduce their carbon footprint. The emphasis on sustainable solutions has led to innovations in product formulations and manufacturing processes, creating new opportunities for market differentiation.

United Kingdom Sealants Market Trends and Insights

Rising investments in housing and infrastructure by the government to boost the construction industry

- The United Kingdom is one of the largest construction markets in Europe. In 2020, the UK construction market contracted by 19.5% due to the COVID pandemic. The number of new homes registered to be built in the United Kingdom declined by 23.2% in 2020, falling to 123,151 homes. There were 115,455 new homes completed, 23% down from the previous year because of COVID-19 in the country. However, in 2021, the construction market recovered and registered a growth rate of 4.7% compared to the same period in 2020. The National House Building Council (NHBC) announced 153,339 new home registrations in 2021, a 25% increase compared to 2020.

- Private sector registrations are the key driver in the United Kingdom, and registrations rose from 80,475 in 2020 to 114,477 in 2021, an increase of more than 40%. In contrast, new home registrations in the rental sector decreased by 8% from 42,460 in 2020 to 38,862 in 2021 due to the deflection of Housing Association capital budgets toward building safety remediation on existing housing stock.

- The annual construction output increased by a record 12.7% in 2021 compared to 2020, mainly due to the pandemic contributing to a very weak 2020. The total new orders for construction increased by 9.2% (EUR1,121 million) in Q4 2021 compared to Q3 2021. The total construction output (seasonally adjusted) grew by 2.0% (EUR 281 million) in December 2021 compared to November 2021.

- To provide better infrastructure to the population across the country, the government has planned to invest 1-2% of its GDP in construction and infrastructure between 2020 and 2050 as part of the National Productivity Investment Fund (NPIF). Therefore, all the abovementioned factors are likely to impact the market studied.

Understand The Key Trends Shaping This Market

Download PDF

In addition to eco-friendly transportation by 2030, electric vehicle registrations growth is likely to propel the automotive production

- The UK automotive industry is a vital part of the UK economy, worth more than EUR 60.2 billion in turnover and adding EUR 11.9 billion value to the UK economy. However, in 2020, the automotive vehicle production in the country reduced by 29.5% compared to the same period in 2019, as the UK automotive sector faced some of the biggest challenges in its history while responding to the COVID-19 pandemic and repositioning for Brexit implications.

- After contracting by 29.5% in 2020, British automotive vehicle production further declined by 4.7% in 2021, as the semiconductor shortage severely affected production. New car registrations decreased 34% Y-o-Y in September 2021, which is excepted to affect the UK sealants market in the future.

- The United Kingdom is planning to phase out gasoline and diesel vehicles to promote the transition to more eco-friendly transportation by 2030. The country also planned an investment of over GBP 1.8 billion in infrastructure and grants to expand access to zero-emission vehicles and support a green economic recovery, thereby increasing the demand for the electric vehicles market in the country.

- The total number of BEV, PHEV, and HEV registrations in the United Kingdom accounted for 452,527 in 2021, registering a growth rate of 58.7% Y-o-Y, compared to 285,199 registrations in 2020. Out of total registrations in 2021 (with percentage Y-o-Y change), 190,727 (76.3%) were BEVs, 114,554 (70.6%) were PHEVs, and 147,246 (34.0%) were HEVs. In 2021, BEV, PHEV, and HEV captured around 27.5% share of total car registrations in the country.

Understand The Key Trends Shaping This Market

Download PDF

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Being the second largest aerospace sector in the world and with forecast of around 10% market share by 2030, United Kingdom aerospace sector is expected to increase

Segment Analysis: End User Industry

Building and Construction Segment in UK Sealants Market

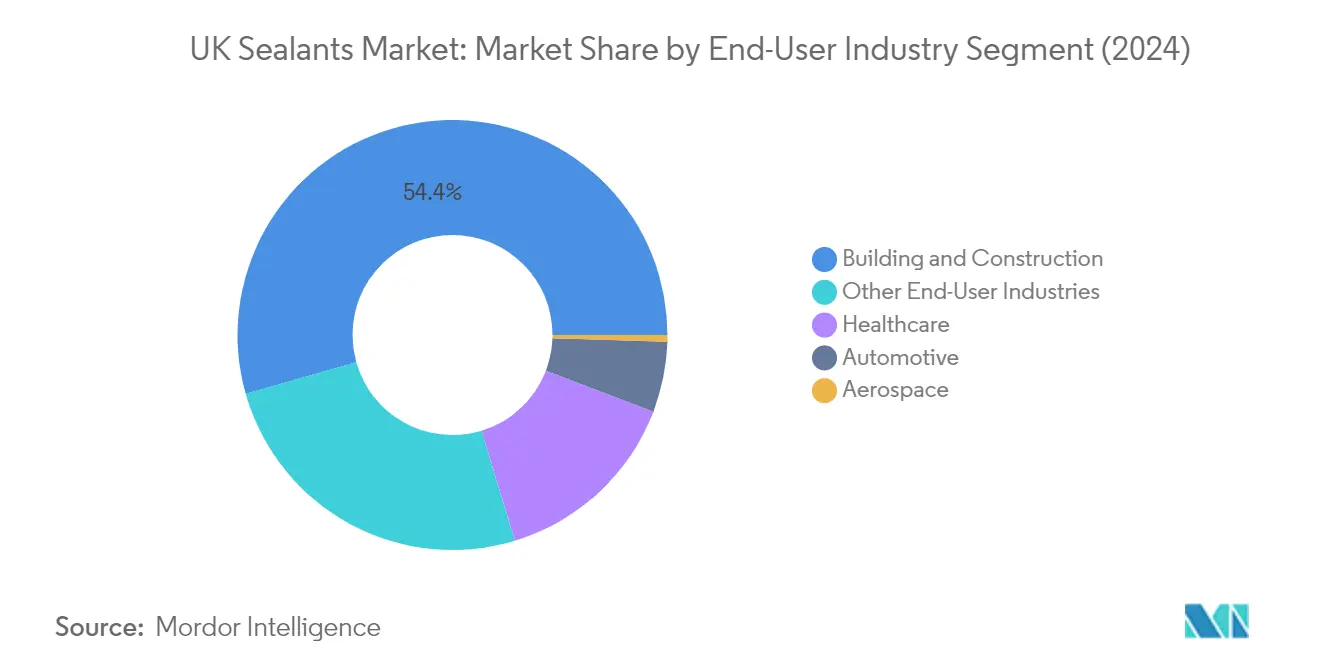

The building and construction segment dominates the UK sealants market, commanding approximately 54% of the total market share in 2024. This significant market position is primarily driven by the extensive application of construction sealants in various construction activities, including waterproofing, weather-sealing, crack-sealing, and joint-sealing applications. The segment's dominance is further strengthened by the European Union Commission's Next Generation EU Recovery Plan, which aims to rebuild infrastructure with a focus on energy efficiency and digital advancement. The plan's emphasis on constructing energy-efficient buildings and renovating existing structures has created substantial demand for construction sealants, particularly in applications such as flooring, roofing, windows, and door fixation frames.

Healthcare Segment in UK Sealants Market

The healthcare segment is emerging as the fastest-growing sector in the UK sealants market, with a projected growth rate of approximately 6% during 2024-2029. This robust growth is primarily driven by increasing investments in healthcare infrastructure and rising demand for medical device manufacturing. The segment's growth is further supported by the government's commitment to enhance healthcare system efficiency through significant funding allocations, including substantial investments in pharmaceutical and medical industry research and development. The expanding medical technology sector, coupled with growing applications in dentistry and medical equipment assembly, continues to drive innovation in healthcare-specific adhesive sealants solutions.

Remaining Segments in End User Industry

The automotive, aerospace, and other end-user industries collectively represent significant opportunities in the UK sealants market. The automotive sector is experiencing transformation through increased adoption of electric vehicles, driving demand for specialized adhesive sealants solutions. The aerospace segment, while smaller, maintains steady demand for high-performance industrial sealants in aircraft manufacturing and maintenance. Other end-user industries, including electronics manufacturing, HVAC systems, and consumer appliances, contribute to market diversity through varied applications ranging from electronic component protection to thermal insulation solutions.

Segment Analysis: Resin

Silicone Segment in UK Sealants Market

The silicone sealants segment dominates the UK sealants market, accounting for approximately 43% of the total market value in 2024. This significant market share can be attributed to silicone sealants' superior properties, including excellent durability, weather resistance, and versatility across multiple applications. Silicone sealants are particularly prevalent in the construction industry for weatherproofing applications and in the automotive sector for various bonding and sealing requirements. The segment's dominance is further strengthened by silicone sealants' unique ability to maintain flexibility across a wide temperature range and their excellent adhesion to both porous and non-porous surfaces, making them ideal for applications in the healthcare, electronics, and consumer goods industries. Additionally, the growing emphasis on energy-efficient buildings and sustainable construction practices has boosted the demand for silicone sealants due to their long-term durability and weather-sealing properties.

Polyurethane Segment in UK Sealants Market

The polyurethane sealants segment represents a significant growth opportunity in the UK sealants market, with a projected growth rate of approximately 6% from 2024 to 2029. This growth is primarily driven by increasing demand from the construction and automotive industries, where polyurethane sealants are valued for their excellent structural strength and flexibility. The segment's expansion is supported by ongoing technological advancements in polyurethane formulations, leading to improved performance characteristics and broader application possibilities. The rise in electric vehicle production and the growing focus on lightweight vehicle construction are creating new opportunities for polyurethane sealants. Furthermore, the segment is benefiting from increasing investments in infrastructure development and the renovation of existing buildings, where polyurethane sealants are preferred for their superior bonding properties and resistance to environmental factors.

Remaining Segments in Resin Segmentation

The remaining segments in the UK sealants market include epoxy sealants, acrylic sealants, and other specialty resin-based sealants, each serving specific applications and market niches. Acrylic sealants are particularly valued in the construction industry for their cost-effectiveness and ease of application, while epoxy sealants are preferred in industrial applications requiring high strength and chemical resistance. Other specialty resin-based sealants, including hybrid and modified polymers, are gaining traction due to their unique performance characteristics and environmental sustainability profiles. These segments collectively contribute to market diversity by offering specialized solutions for specific application requirements, ranging from general-purpose sealing to high-performance industrial applications. The continuous development of new formulations and technologies in these segments is driving innovation in the overall sealants market.

Competitive Landscape

Top Companies in United Kingdom Sealants Market

The UK sealants market is characterized by continuous product innovation and strategic expansion initiatives from leading players. Companies are heavily focused on developing eco-friendly and sustainable sealant solutions, particularly targeting low VOC emissions and enhanced performance characteristics. Operational agility has become paramount, with manufacturers establishing robust local manufacturing facilities and distribution networks across the United Kingdom to ensure reliable supply chains. Strategic moves in the market primarily revolve around strengthening technical capabilities, expanding production capacities, and developing application-specific solutions. Companies are increasingly investing in research and development to create innovative products for emerging applications in electric vehicles, healthcare, and energy-efficient construction. The expansion strategies include both organic growth through new product launches and inorganic growth through strategic partnerships with local distributors and manufacturers.

Market Structure Shows Mixed Competition Dynamics

The UK sealants market exhibits a partially fragmented structure with a mix of global conglomerates and specialized manufacturers. Global players like Sika AG, Henkel AG & Co. KGaA, and Arkema Group maintain significant market presence through their established brands and comprehensive product portfolios, while local players like Hodgson Sealants and Adshead Ratcliffe & Co Ltd. compete through specialized offerings and strong regional distribution networks. The market demonstrates a balanced competitive landscape where multinational companies leverage their technological expertise and research capabilities, while local players capitalize on their market understanding and customer relationships.

The competitive dynamics are shaped by the presence of both diversified chemical companies and specialized sealant manufacturers. Market consolidation activities are primarily driven by larger companies acquiring local manufacturers to expand their product portfolio and geographic reach. The industry witnesses strategic collaborations between manufacturers and end-users, particularly in the construction and automotive sectors, to develop customized solutions. Companies with integrated operations from manufacturing to distribution hold competitive advantages in terms of cost efficiency and market responsiveness.

Innovation and Sustainability Drive Future Success

For incumbent players to maintain and expand their market share, focus on sustainable product development and application-specific solutions is crucial. Companies need to invest in developing environmentally friendly formulations while maintaining high performance standards to meet evolving regulatory requirements and customer preferences. Building strong relationships with key end-user industries, particularly in the construction and automotive sectors, through technical support and customized solutions remains vital. Establishing efficient supply chains and local manufacturing capabilities helps in reducing operational costs and improving market responsiveness.

New entrants and challenger companies can gain ground by focusing on niche applications and underserved market segments. Success factors include developing specialized products for emerging applications in healthcare and electronics, while maintaining competitive pricing strategies. Companies need to consider the high concentration of end-users in the construction and automotive sectors while formulating their market entry strategies. The risk of substitution from alternative bonding technologies necessitates continuous innovation in product development. Future regulatory changes, particularly regarding environmental standards and safety requirements, will significantly influence market dynamics and competitive strategies. The sealant industry is poised for growth as companies innovate to meet these challenges.

United Kingdom Sealants Industry Leaders

-

Arkema Group

-

Dow

-

Henkel AG & Co. KGaA

-

Sika AG

-

Soudal Holding N.V.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2020: Hodgson Sealants launched a new product, HYSPEC 25 in Action, under its umbrella of hybrid sealants. The product has numerous applications in the construction industry.

- April 2019: Dow completed the separation of its Material Science division through a spin-off of Dow Inc.

United Kingdom Sealants Market Report Scope

Aerospace, Automotive, Building and Construction, Healthcare are covered as segments by End User Industry. Acrylic, Epoxy, Polyurethane, Silicone are covered as segments by Resin.

End User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

Resin

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

| End User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries | |

| Resin | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins |

Need A Different Region or Segment?

Customize Now

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF