Market Size of United Kingdom Plastic Packaging Films Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

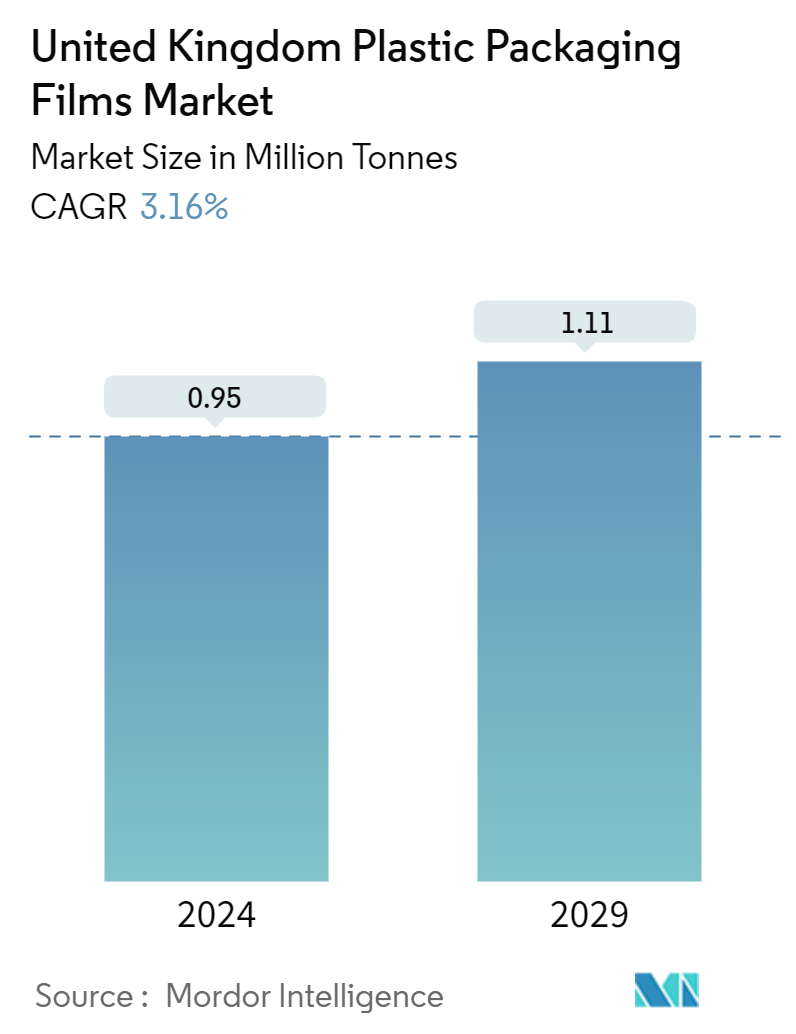

| Market Volume (2024) | 0.95 Million tonnes |

| Market Volume (2029) | 1.11 Million tonnes |

| CAGR (2024 - 2029) | 3.16 % |

| Market Concentration | Low |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order |

United Kingdom Plastic Packaging Films Market Analysis

The United Kingdom Plastic Packaging Films Market size is estimated at 0.95 Million tonnes in 2024, and is expected to reach 1.11 Million tonnes by 2029, growing at a CAGR of 3.16% during the forecast period (2024-2029).

- The rising need for high-performance films is propelling the growth of the plastic packaging film market in the United Kingdom. This market growth is also driven by heightened barrier requirements across various end-user industries, including food packaging, pharmaceuticals, and consumer goods. Advancements in processing technologies facilitate the use of plastic films, ensuring their suitability and cost efficiency in production. These technological improvements enable manufacturers to meet stringent industry standards and cater to the evolving demands of consumers.

- Consumers in the region gravitate toward products with extended shelf lives, driven by convenience and a growing concern for reducing food waste. With its superior barrier properties, plastic film packaging shields items from moisture, oxygen, light, and other elements that can compromise their quality and freshness. As a result, it is proving instrumental in prolonging the shelf life of a wide array of perishable items, spanning from food and beverages to pharmaceuticals and personal care products. Additionally, the lightweight nature of plastic film packaging reduces transportation costs and carbon emissions, making it an environmentally friendly option. The versatility of plastic film also allows innovative packaging designs that cater to various consumer preferences and market demands.

- On-the-go consumption, smaller households, and rising demand for convenience increasingly define modern lifestyles. Plastic film packaging is a solution, offering lightweight, portable, and resealable features that align with these lifestyles. Single-serve and portion-controlled formats are gaining traction, catering to consumers' convenience and portion-control preferences. Additionally, the versatility of plastic film packaging allows innovative designs and functionalities, such as easy-open features and extended shelf life, further enhancing its appeal to consumers and manufacturers alike.

- The UK government introduced the plastic packaging tax (PPT) to curb plastic waste, effective 2022. This tax targets plastic packaging with less than 30% recycled content. This levy compels companies that produce plastic packaging to adopt more recycled materials, aiming to slash plastic waste destined for landfills or incineration. In April 2024, the tax increased to GBP 217.85 per tonne. The tax's proceeds are earmarked to bolster the UK's recycling infrastructure and combat plastic waste. These regulations are poised to reshape the market, presenting challenges and opportunities.

- Recycling is pivotal in establishing a closed loop for sustainable plastics. Advancements in collection, sorting techniques, and innovative recycling methods ensure that plastic retains its value throughout its lifecycle. As the region has established mandated targets for recycled content, it underscores the importance of innovation and investment in reducing waste and enhancing recycling efficiency.

United Kingdom Plastic Packaging Films Industry Segmentation

Plastic films are versatile, serving to wrap products, overwrap various packaging types (from individual packs to palletized loads), and create sachets, bags, and pouches. They are often part of laminates, which are combined with other plastics and materials for packaging. The report delves into the demand for these converted packaging films, analyzing them across essential resin and application categories. This broad scope mirrors the diverse needs of the market and the shifting preferences of consumers and businesses.

The UK plastic packaging film market is segmented by type (polypropylene (biaxially oriented polypropylene (BOPP) and cast polypropylene (CPP)), polyethylene (low-density polyethylene (LDPE) and linear low-density polyethylene (LLDPE)), polyethylene terephthalate (biaxially oriented polyethylene terephthalate (BOPET)), polystyrene, bio-based, and PVC, EVOH, PETG, and other film types) and end user (food [candy & confectionery, frozen foods, fresh produce, dairy products, dry foods, meat, poultry, and seafood, pet food, and other food products (seasonings & spices, spreadables, sauces, condiments, etc.)], healthcare, consumer products packaging (cosmetics, household, and personal care), industrial packaging, and other end users (agricultural, chemical, and others)). The market sizes and forecasts are provided in terms of volume (units) for all the above segments.

| By Type | |

| Polypropylene(PP) (Biaxially Oriented Polypropylene (BOPP),Cast polypropylene (CPP)) | |

| Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE)) | |

| Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET)) | |

| Polystyrene | |

| Bio-Based | |

| PVC, EVOH, PETG, and Other Film Types |

| By End-User Industry | ||||||||||

| ||||||||||

| Healthcare | ||||||||||

| Personal Care & Home Care | ||||||||||

| Industrial Packaging | ||||||||||

| Other End-use Industry Applications (Agricultural, Chemical, Etc.) |

United Kingdom Plastic Packaging Films Market Size Summary

The United Kingdom plastic packaging films market is experiencing a notable expansion, driven by the increasing demand for high-performance films across various sectors such as food packaging, pharmaceuticals, and consumer goods. This growth is supported by advancements in processing technologies that enhance the suitability and cost efficiency of plastic films, allowing manufacturers to meet stringent industry standards. The market is further bolstered by consumer preferences for products with extended shelf lives, which are facilitated by the superior barrier properties of plastic films. These films protect products from environmental factors like moisture and light, thereby prolonging the freshness and quality of perishable items. The lightweight nature of plastic film packaging also contributes to reduced transportation costs and carbon emissions, aligning with environmental sustainability goals. Additionally, the versatility of plastic films enables innovative packaging designs that cater to modern consumer lifestyles, characterized by on-the-go consumption and a preference for convenience.

The market landscape is shaped by regulatory developments such as the UK's plastic packaging tax, which encourages the use of recycled materials and aims to reduce plastic waste. This regulatory environment presents both challenges and opportunities for market players, prompting investments in recycling infrastructure and sustainable packaging solutions. Polyethylene remains a dominant material due to its flexibility, moisture barrier properties, and recyclability, making it a preferred choice for packaging films. The demand for transparent packaging, particularly in the food and beverage sector, is on the rise, driven by consumer preferences for product visibility and quality assurance. The market is characterized by high competition and low product differentiation, with key players like Elite Plastics Limited, Innovia Films, and Berry Global Inc. actively investing in innovative and sustainable packaging solutions. These developments underscore the market's dynamic nature, as companies strive to meet evolving consumer demands and regulatory requirements while promoting sustainability and efficiency in packaging.

United Kingdom Plastic Packaging Films Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

-

2. MARKET SEGMENTATION

-

2.1 By Type

-

2.1.1 Polypropylene(PP) (Biaxially Oriented Polypropylene (BOPP),Cast polypropylene (CPP))

-

2.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

-

2.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

-

2.1.4 Polystyrene

-

2.1.5 Bio-Based

-

2.1.6 PVC, EVOH, PETG, and Other Film Types

-

-

2.2 By End-User Industry

-

2.2.1 Food

-

2.2.1.1 Candy & Confectionery

-

2.2.1.2 Frozen Foods

-

2.2.1.3 Fresh Produce

-

2.2.1.4 Dairy Products

-

2.2.1.5 Dry Foods

-

2.2.1.6 Meat, Poultry, And Seafood

-

2.2.1.7 Pet Food

-

2.2.1.8 Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)

-

-

2.2.2 Healthcare

-

2.2.3 Personal Care & Home Care

-

2.2.4 Industrial Packaging

-

2.2.5 Other End-use Industry Applications (Agricultural, Chemical, Etc.)

-

-

United Kingdom Plastic Packaging Films Market Size FAQs

How big is the United Kingdom Plastic Packaging Films Market?

The United Kingdom Plastic Packaging Films Market size is expected to reach 0.95 million tonnes in 2024 and grow at a CAGR of 3.16% to reach 1.11 million tonnes by 2029.

What is the current United Kingdom Plastic Packaging Films Market size?

In 2024, the United Kingdom Plastic Packaging Films Market size is expected to reach 0.95 million tonnes.