Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

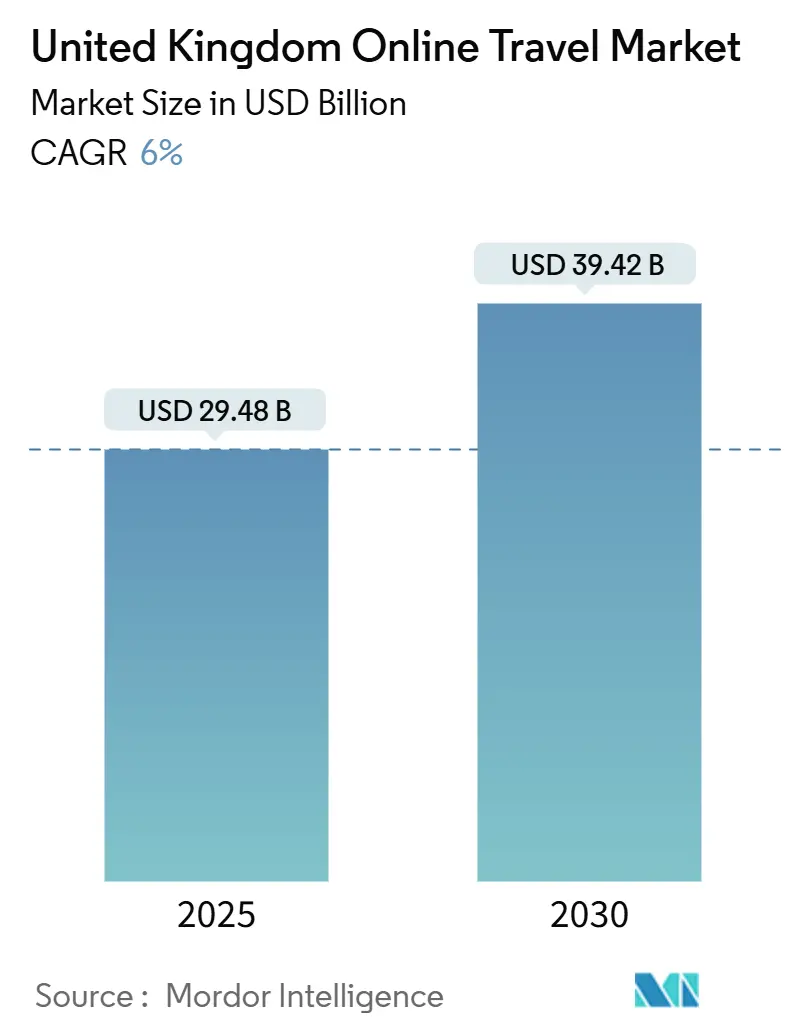

| Market Size (2025) | USD 29.48 Billion |

| Market Size (2030) | USD 39.42 Billion |

| Growth Rate (2025 - 2030) | 6.00% CAGR |

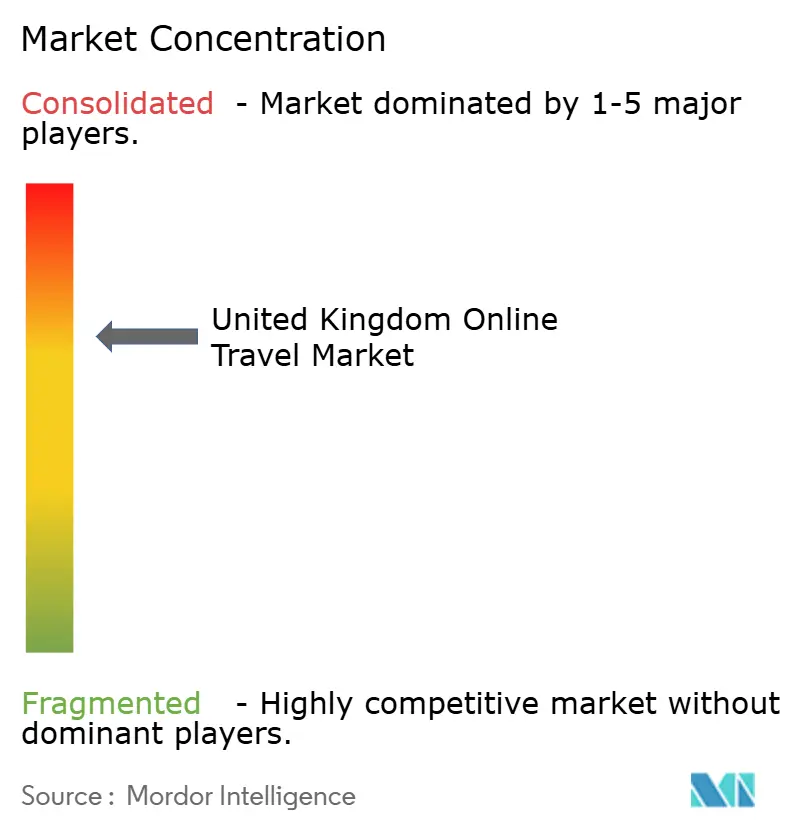

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Online Travel Market Analysis by Mordor Intelligence

The United Kingdom online travel market stood at USD 29.48 billion in 2025 and is forecast to reach USD 39.42 billion by 2030, expanding at a 6.00% CAGR. Platform innovation, mobile-first booking habits, and a decisive leisure rebound underpin this trajectory despite cost-of-living pressures and currency volatility. Heritage-site digital twins, open-banking refunds, and “work-from-anywhere” policies enlarge addressable demand, while commission-free dynamic packaging broadens product choice. Airline slot scarcity at Heathrow and rising merchant service fees temper near-term momentum, but mobile conversions, meta-search growth, and a Generation Z wave sustain a resilient outlook for the United Kingdom online travel market.

Key Report Takeaways

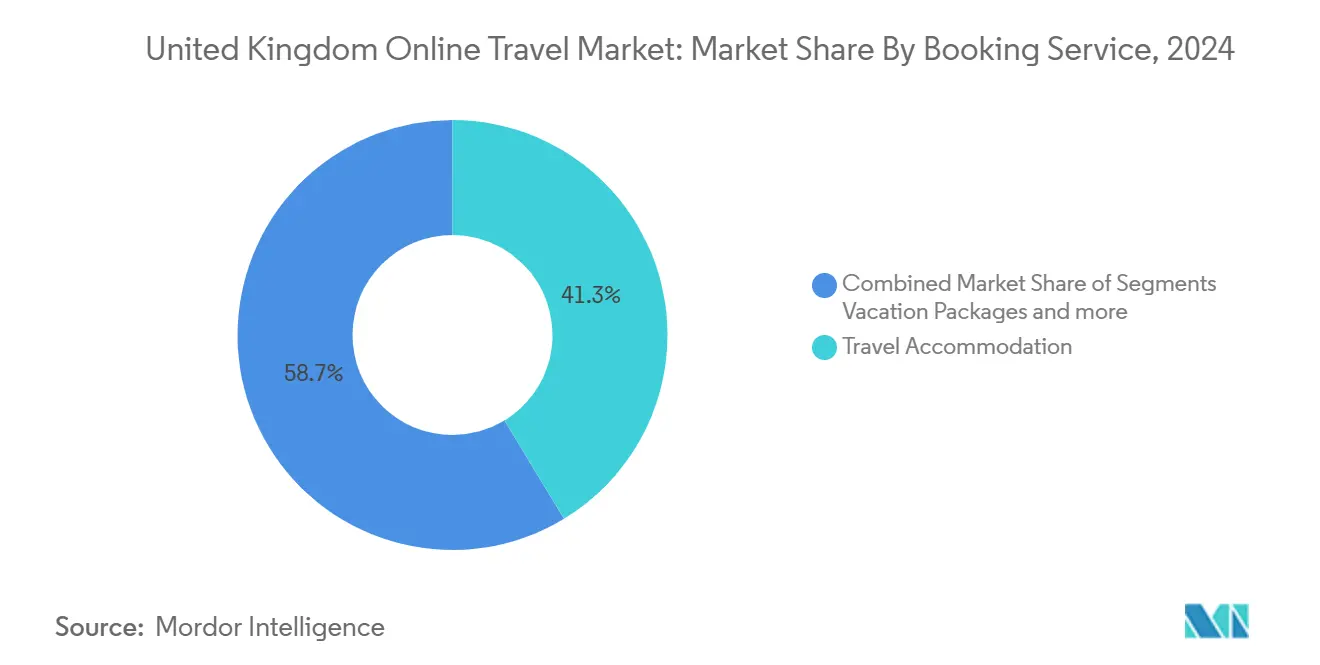

- • By booking service, Travel Accommodation held 41.30% of the United Kingdom online travel market share in 2024, whereas Vacation Packages are advancing at a 10.45% CAGR through 2030.

- • By device type, mobile booked 67.90% of the United Kingdom online travel market size in 2024 and are forecast to expand at a 9.89% CAGR to 2030.

- • By platform type, online travel agencies captured 65.90% revenue share of the United Kingdom online travel market in 2024, while meta-search engines are projected to grow at 11.33% CAGR.

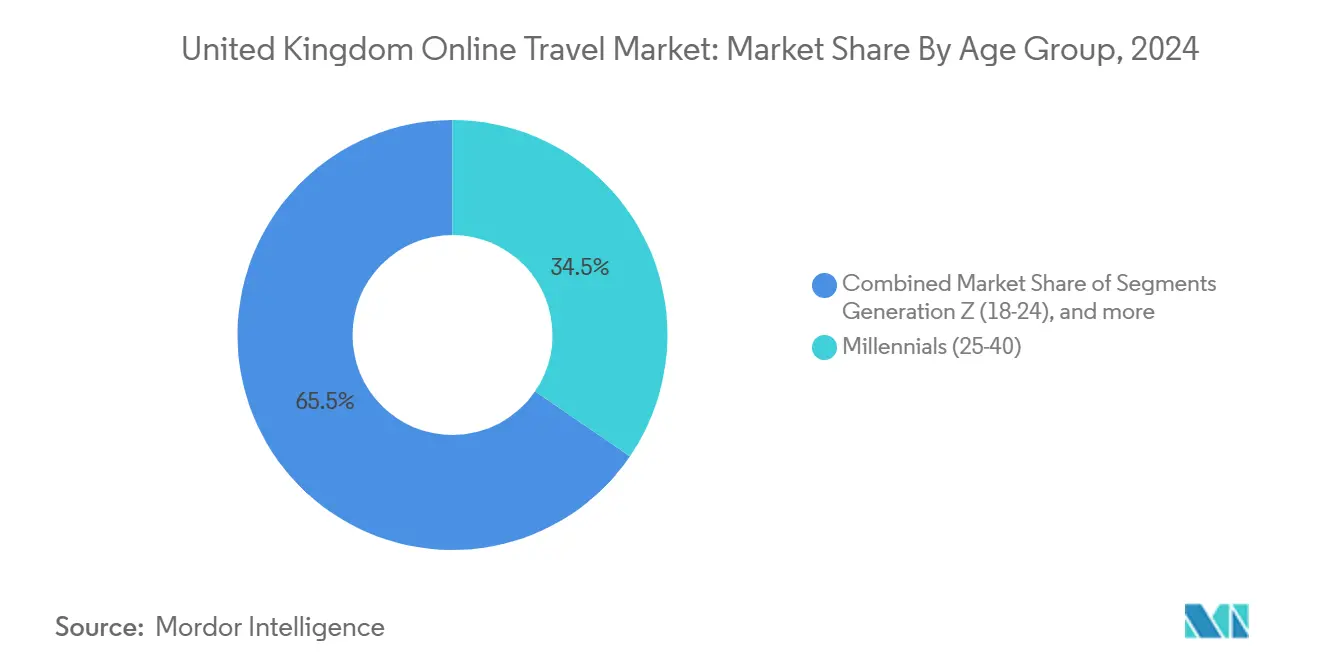

- • By age group, Millennials controlled 34.50% of the segment revenue of the United Kingdom online travel market in 2024, yet Generation Z usage is scaling at an 8.20% CAGR through 2030.

- • By traveller type, leisure trips represented 65.30% of bookings of the United Kingdom online travel market in 2024; the visiting-friends-and-relatives niche is growing fastest at 7.61% CAGR.

- • By geography, England accounted for 67.61% of the United Kingdom online travel market 2024 spend, with Scotland forecast to post the strongest 6.73% CAGR over the outlook period.

United Kingdom Online Travel Market Trends and Insights

Drivers Impact Analysis

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic leisure rebound & pent-up demand | +1.8% | England, Scotland, Wales | Short term (≤ 2 years) |

| Acceleration of mobile booking & in-app payments | +1.2% | National, urban centers | Medium term (2-4 years) |

| Dynamic packaging legislation lifting commission caps | +0.9% | England, Wales regulatory zones | Medium term (2-4 years) |

| Mainstreaming of work-from-anywhere travel policies | +0.7% | England, Scotland business hubs | Long term (≥ 4 years) |

| Heritage-site digital twins driving immersive trip planning | +0.5% | England, Scotland heritage corridors | Long term (≥ 4 years) |

| Open-banking-powered instant refunds boosting customer trust | +0.4% | National, early adoption in London | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic leisure rebound & pent-up demand

International arrivals are forecasted to reach 43.4 million by 2025, reflecting a 5% growth compared to 2024, with an anticipated visitor expenditure of GBP 33.7 billion [1]VisitBritain, “Inbound Tourism Forecast 2025,” visitbritain.org. Visits to friends and relatives primarily drive the recovery of the UK travel market, as residents increasingly prioritize reconnecting and planning domestic overnight trips. Corporate adoption of “super-commuting” policies is fostering the rise of blended business-leisure travel, contributing to longer stays. Despite inflationary challenges, travel remains the leading discretionary spending category, supporting the growth of the UK’s online travel market through 2026. Post-2026, the market is expected to stabilize and return to baseline growth levels.

Acceleration of mobile booking & in-app payments

In 2024, mobile devices contributed to 67.90% of total bookings, with a projected CAGR of 9.89%, surpassing desktop usage. The adoption of digital payment solutions such as Apple Pay, Google Pay, and biometric boarding processes has significantly enhanced conversion rates. British Airways is piloting facial recognition technology to streamline gate-to-seat passenger experiences. Generation Z, with over 50% favoring mobile platforms, is driving the shift toward a mobile-first approach. This trend highlights the critical need for operators to prioritize mobile-centric strategies to remain competitive.

Dynamic packaging legislation lifting commission caps

The Package Travel and Linked Travel Arrangements Regulations 2018 eliminated outdated commission caps, facilitating seamless integration of flights, accommodations, and activities into dynamic vacation packages. This regulatory change has driven a 10.45% CAGR in the vacation packages market, as key players like TUI incorporate lastminute.com's inventory across multiple channels. Enhanced buyer confidence, supported by mandatory insolvency protection and transparent pricing, has contributed to higher transaction values. The ability to offer real-time bundling has strengthened operators' competitive positioning in the market. These developments underscore the growing demand for flexible and comprehensive travel solutions.

Mainstreaming of work-from-anywhere travel policies

The adoption of hybrid work models has significantly increased the demand for "workcations," prompting businesses to allocate higher budgets toward adaptable and sustainable travel options. In 2024, corporate travel spending experienced growth, highlighted by TravelPerk’s strategic acquisition of AmTrav for USD 135 million to enhance its platform capabilities. This acquisition reflects the industry's focus on scaling operations to meet evolving travel demands. Suppliers are optimizing operational efficiency by encouraging extended stays and mid-week departures. These strategies aim to balance load factors and improve resource utilization across the travel supply chain.

Restraints Impact Analysis

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising merchant service fees from UK card issuers | -0.8% | National, all digital transactions | Short term (≤ 2 years) |

| Airline capacity crunch & slot constraints at Heathrow | -0.6% | London, Southeast England aviation corridors | Medium term (2-4 years) |

| Data-privacy clamp-downs on third-party cookie tracking | -0.4% | National, EU spill-over | Short term (≤ 2 years) |

| Volatile GBP-EUR exchange rates are squeezing OTA margins | -0.3% | National, European route exposure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising merchant service fees from UK card issuers

Mastercard and Visa collectively account for 95% of travel-related transactions in the UK, exerting significant control over the market. Their decision to increase processing fees beyond inflation has imposed an additional annual cost of over GBP 250 million on merchants [2]Payment Systems Regulator, “Interim Card Scheme Fees Review,” psr.org.uk . Smaller online travel agencies (OTAs), with limited bargaining power, are increasingly vulnerable to market exits or consolidation. Emerging pay-by-bank schemes present a potential alternative; however, their current cost structure remains less competitive compared to card payments. These dynamic underscores the growing financial strain on merchants and the need for cost-effective payment solutions in the travel industry.

Airline capacity crunch & slot constraints at Heathrow

In the first half of 2024, Heathrow Airport operated near its capacity, handling approximately 40 million passengers. The limited availability of slots has resulted in higher airfares and constrained the addition of new routes. With the approval of the proposed third runway still pending, airlines are reallocating operations to Gatwick Airport or forming strategic rail partnerships. To partially address these challenges, the Civil Aviation Authority has reduced airline charges to GBP 23.72 per passenger. These developments highlight the operational and strategic adjustments required to manage growing passenger volumes and infrastructure constraints [3]UK Civil Aviation Authority, “Price Control at Heathrow Airport,” caa.co.uk .

Segment Analysis

By Booking Service: Vacation Packages Lead Growth Acceleration

Vacation Packages are driving significant growth in the United Kingdom's online travel market, recording a strong CAGR of 10.45%. This growth highlights their increasing importance as a key revenue stream within the market. In 2024, Travel Accommodation accounted for a notable share of the market, emphasizing its critical role in shaping consumer expenditure. The rising demand for lodging solutions reflects evolving consumer preferences and spending priorities. These trends collectively underline the dynamic nature of the online travel market in the United Kingdom.

Regulation-driven dynamic packaging has enabled OTAs to integrate flights, accommodations, and tours into customizable offerings with flexible pricing models. TUI’s strategic alliance with lastminute.com has significantly expanded its Tours & Activities network to 100 countries, enhancing its global footprint [4]TUI Group, “Q2 2025 Results Presentation,” tuigroup.com . The Alternative Lodging segment continues to gain traction, as evidenced by Airbnb’s Q4-2024 revenue of USD 2.5 billion. This growth reflects the increasing consumer shift toward non-traditional lodging options. Such developments demonstrate the evolving competitive landscape and the diversification of offerings within the online travel market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Device Type: Mobile Dominance Accelerates

In 2024, mobile bookings represented 67.90% of total transactions, with projections indicating they will surpass half of all transactions by 2030, driven by a CAGR of 9.89%. This growth highlights the diminishing role of desktop bookings, which continue to decline. The adoption of frictionless wallet payments and biometric boarding processes is accelerating this transition. These advancements streamline the booking experience, making mobile platforms more appealing to consumers. The trend underscores a significant shift in consumer behavior toward convenience and technology-driven solutions.

Gen Z's strong preference for mobile platforms, coupled with app-exclusive rewards, is solidifying the dominance of smartphones in consumer interactions. TUI has reported substantial double-digit growth in app-based revenues, reflecting the increasing reliance on mobile channels. Additionally, Alipay+ is enhancing payment efficiency for Asian tourists, further driving mobile adoption. Despite this, desktops maintain a limited role in managing complex corporate travel itineraries. However, their relevance continues to erode as mobile solutions gain traction across broader use cases.

By Platform Type: Meta-search Engines Disrupt Traditional Models

In 2024, Online Travel Agencies accounted for 65.90% of total sales, maintaining their dominant position in the market. However, meta-search engines are expanding at a compound annual growth rate (CAGR) of 11.33%, driven by travelers' preference for transparent price comparisons. The implementation of the Digital Markets Act has introduced “gatekeeper” obligations for Booking.com, which is expected to improve market access for smaller suppliers. This regulatory shift is likely to foster a more competitive landscape by reducing barriers for emerging players. As a result, the dynamics of the online travel market are evolving, with increased opportunities for smaller entities to gain visibility.

Artificial intelligence (AI) is playing a transformative role in the travel industry, with companies like eDreams Odigeo and Google Cloud’s oneworld prototype leading advancements in personalized travel planning. These AI-driven solutions enable end-to-end customization, enhancing the customer experience and streamlining the booking process. Concurrently, airlines are focusing on rebuilding their direct booking portals to minimize dependency on third-party platforms and reduce commission costs. This strategic shift is intensifying competition as airlines aim to strengthen their direct customer relationships. The ongoing developments underscore the growing importance of technology and direct engagement in reshaping the competitive dynamics of the travel market.

By Traveler Type: VFR Segment Drives Recovery

In 2024, the Leisure sector contributed 65.30% to total revenue, maintaining its dominant position in the market. The Visiting Friends & Relatives (VFR) segment is projected to grow at a 7.61% CAGR, driven by evolving travel patterns. Extended stays and mid-week departures are becoming more common as travelers prioritize reconnection trips. This shift highlights changing consumer preferences and their impact on travel dynamics. The VFR segment's growth underscores its increasing significance within the broader travel market.

The rise of hybrid work has introduced the "workcation" trend, blending work and leisure travel. To address this demand, TravelPerk is scaling its flexible inventory to accommodate these hybrid travel needs. Business travel demand remains below pre-pandemic levels, reflecting a slower recovery trajectory. However, there is a growing emphasis on premium fare options and sustainability-focused travel. These trends indicate a shift in corporate travel priorities, aligning with broader market changes.

By Age Group: Generation Z Reshapes Market Dynamics

In 2024, Millennials accounted for 34.50% of the United Kingdom's online travel market, reflecting their significant influence on the industry. However, Generation Z is emerging as a key demographic, with a robust CAGR of 8.20%, and is projected to reshape the market by 2030. This cohort demonstrates a strong preference for mobile-based bookings and meta-search platforms, aligning with their tech-savvy nature. Sustainability and peer reviews are critical factors influencing their travel decisions, highlighting their focus on ethical and informed choices. As a result, businesses must adapt their strategies to cater to the evolving preferences of Generation Z to remain competitive.

Baby Boomers continue to prioritize longer stays, often selecting premium accommodations that align with their preference for comfort and luxury. In contrast, Generation X is driving the trend of multi-generational travel, showcasing their role as planners for family-oriented experiences. These generational behaviours underline the diverse demands within the market, requiring tailored approaches to meet varying customer needs. Understanding these distinct preferences is essential for businesses aiming to capture market share across different age groups. Companies must leverage these insights to develop targeted offerings and enhance customer satisfaction.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

England commanded more than half of the United Kingdom's online travel market size in 2024, driven by London’s financial hub status, Heathrow’s connectivity, and dense heritage assets. Leisure, business, and MICE demands bolster a regional CAGR outlook. While capacity constraints at Heathrow and escalating city center costs temper potential growth, initiatives like Crossrail and HS2 enhance multimodal connectivity.

Scotland, while contributing a smaller market base, demonstrates the highest CAGR within the UK travel market. Key drivers include heritage corridors, whisky trails, and digital tourism grants, which effectively attract long-haul visitors. Domestic holiday participation among Scots declined to 18% in 2024; however, increased inbound tourism mitigated this downturn. The National Trust for Scotland's integration of augmented reality has strategically extended visitor activity into the shoulder season. These initiatives collectively position Scotland as a dynamic growth area within the UK travel market.

Wales and Northern Ireland collectively maintain a notable market share within the UK travel industry. Wales leverages its geographical proximity to major English population centers and its focus on coastal eco-tourism to attract visitors. Northern Ireland benefits from expanded air connectivity through Belfast and the popularity of Game of Thrones-themed tours, which enhance its tourism appeal. Both regions are actively investing in EU-funded rural connectivity projects, which are expected to improve online booking conversions. These strategic efforts underline the regions' commitment to strengthening their positions in the UK's online travel market.

Competitive Landscape

The United Kingdom's online travel market exhibits a moderately concentrated structure. Booking Holdings holds the leading position, with Expedia Group ranking as the second-largest player. Airbnb, TUI, and Trainline complete the list of the top five competitors in the market. Collectively, these companies dominate the market, showcasing significant influence over its dynamics. However, increasing regulatory scrutiny is compelling these firms to adopt measures such as data sharing and reducing self-preferencing to ensure compliance.

TUI has strengthened its vertical integration strategy, achieving EUR 23.2 billion in revenue for 2025 by integrating hotels, flights, and in-destination services. Expedia is leveraging artificial intelligence to deliver tailored travel packages, enhancing customer engagement and satisfaction. Booking.com is piloting a fintech escrow solution aimed at accelerating payment processes for suppliers, improving operational efficiency. These strategic moves highlight the growing importance of technology-driven solutions in the travel market. The focus on innovation underscores the shift towards creating seamless and personalized customer experiences.

HBX is preparing for a EUR 725 million IPO to support the expansion of its B2B marketplace, signaling its growth ambitions. The corporate travel market has seen significant consolidation, with Good Travel Management merging with CT Travel Group to form a GBP 85 million entity. This merger reflects the trend of companies scaling operations to enhance competitiveness and market presence. Investments in technology, mobile user experience, and payment innovations increasingly define competitive advantage in the travel sector. The shift away from inventory scale emphasizes the importance of digital transformation in driving growth and differentiation.

United Kingdom Online Travel Industry Leaders

Booking Holdings Inc.

Expedia Group Inc.

Airbnb Inc.

TUI Group

On the Beach Group plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Eurostar committed GBP 1.7 billion for 50 trains to launch London–Frankfurt and London–Geneva links in the early 2030s, promoting rail substitution for short-haul flights.

- March 2025: Amadeus selected Google Cloud to accelerate AI flight-search accuracy and offer management innovation.

- January 2025: HBX filed for a Spanish IPO seeking up to EUR 725 million to grow its travel technology marketplace.

- November 2024: Juniper bought Traveltek to scale cruise and dynamic packaging capabilities in key outbound markets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom online travel market as all consumer bookings for domestic or outbound transportation, lodging, vacation packages, and ancillary travel services that are transacted and paid for through internet-enabled interfaces on desktops, laptops, or mobile devices, whether via an online travel agency, metasearch site, or a supplier's own portal, and expressed in gross booking value before commissions.

Scope Exclusion: Purchases completed through bricks-and-mortar travel shops, call centers, or corporate self-booking tools fall outside this market.

Segmentation Overview

- By Booking Service

- Transportation

- Air Travel

- Bus & Coach Travel

- Rail Travel

- Car Rental

- Cruise

- Travel Accommodation

- Hotels & Resorts

- Alternative Lodging / Rentals

- Vacation Packages

- Others (Activities, Travel Insurance, Ancillary)

- Transportation

- By Device Type

- Desktop & Laptop

- Mobile (Smartphone & Tablet)

- By Platform Type

- Online Travel Agencies (OTAs)

- Direct Supplier Websites

- Meta-search Engines

- By Traveler Type

- Leisure

- Business

- Visiting Friends & Relatives (VFR)

- By Age Group

- Generation Z (18-24)

- Millennials (25-40)

- Generation X (41-56)

- Baby Boomers (57-75)

- By Region

- England

- Scotland

- Wales

- Northern Ireland

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed airline revenue-management executives, OTA category managers, hotel distribution heads, and payment-gateway providers across England, Scotland, and Wales. These conversations clarified ride-sharing bundling rates, mobile-only promo adoption, and seasonality inflections, letting us refine assumptions and close gaps spotted in desk work.

Desk Research

We began with publicly available macro data, monthly inbound and outbound traveler volumes from the UK Office for National Statistics, Civil Aviation Authority passenger counts, the Bank of England's card-spend series, and Ofcom's annual internet-penetration survey to anchor demand, spend, and digital reach. Trade bodies such as ABTA, WTTC, and the European Travel Commission supplied trend notes on booking channel shifts, while company 10-Ks and investor decks helped us benchmark average selling prices and take rates. Select paid repositories, notably D&B Hoovers for revenue splits and Dow Jones Factiva for press releases, rounded out firm-level inputs. The sources cited are illustrative rather than exhaustive; many additional references informed data checks.

Market-Sizing & Forecasting

A top-down build starts with traveler counts by purpose and trip length, multiplied by spend per trip adjusted for the share booked online. Results are cross-checked through sampled OTA gross bookings, supplier-direct digital sales, and channel take-rate disclosures. Key model variables include smartphone penetration, outbound holiday frequency, average airfares, accommodation ADR, and promotional discount depth. Multivariate regression, incorporating GDP per capita and real exchange-rate swings, projects these drivers to 2030. Where supplier roll-ups ran thin, calibration occurred once senior interviewees validated realistic conversion funnels.

Data Validation & Update Cycle

Outputs face two tiers of scrutiny. First, built-in variance tests flag outliers against historic ratios; second, a senior peer reviews every worksheet before sign-off. We refresh models annually and trigger interim revisions after material events such as a VAT change or major platform merger, ensuring clients always receive a current viewpoint.

Why Mordor's United Kingdom Online Travel Baseline Rings True

Published numbers often diverge because analysts choose different scopes, base years, or digital-spend definitions.

By aligning our scope tightly to gross online bookings and applying recent 2024 card-spend benchmarks, Mordor minimizes such drift.

Key gap drivers include whether peer reports fold in offline agency websites, how they treat peer-to-peer rentals, their currency-conversion date, and the cadence at which assumptions are refreshed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 29.48 B (2025) | Mordor Intelligence | |

| USD 42.60 B (2024) | Global Consultancy A | Includes offline agency web bookings and service-fee markups |

| USD 26.20 B (2021) | Industry Analysis B | Older base year; excludes peer-to-peer lodging yet applies global CAGR to UK |

The comparison shows that once outdated bases, wider scopes, or unverified markups are stripped away, our disciplined variable selection and yearly refresh provide a balanced, transparent baseline that decision-makers can rely on.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the United Kingdom online travel market?

The market is valued at USD 29.48 million in 2025 and is projected to hit USD 39.42 million by 2030 at a 6.00% CAGR.

Which booking service segment is growing fastest?

Vacation Packages lead with a 10.45% CAGR through 2030, supported by dynamic packaging regulations that removed commission caps.

Why are mobile devices so dominant in UK travel bookings?

Mobile accounts for 67.9% of 2024 transactions, propelled by digital-wallet ubiquity, biometric boarding, and app-exclusive loyalty features.

How do recent UK regulations affect online travel platforms?

The Digital Markets, Competition and Consumers Act bans hidden fees and fake reviews, while the Digital Markets Act forces gatekeepers to end self-preferencing, increasing transparency for travelers.

Which region inside the UK offers the strongest growth outlook?

Scotland is set to expand at a 6.73% CAGR to 2030, underpinned by heritage-tourism investment and upgraded digital infrastructure.

What level of market concentration exists among UK online travel players?

The top five operators control more than half of the revenue, giving the sector a moderate-to-high concentration.