Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

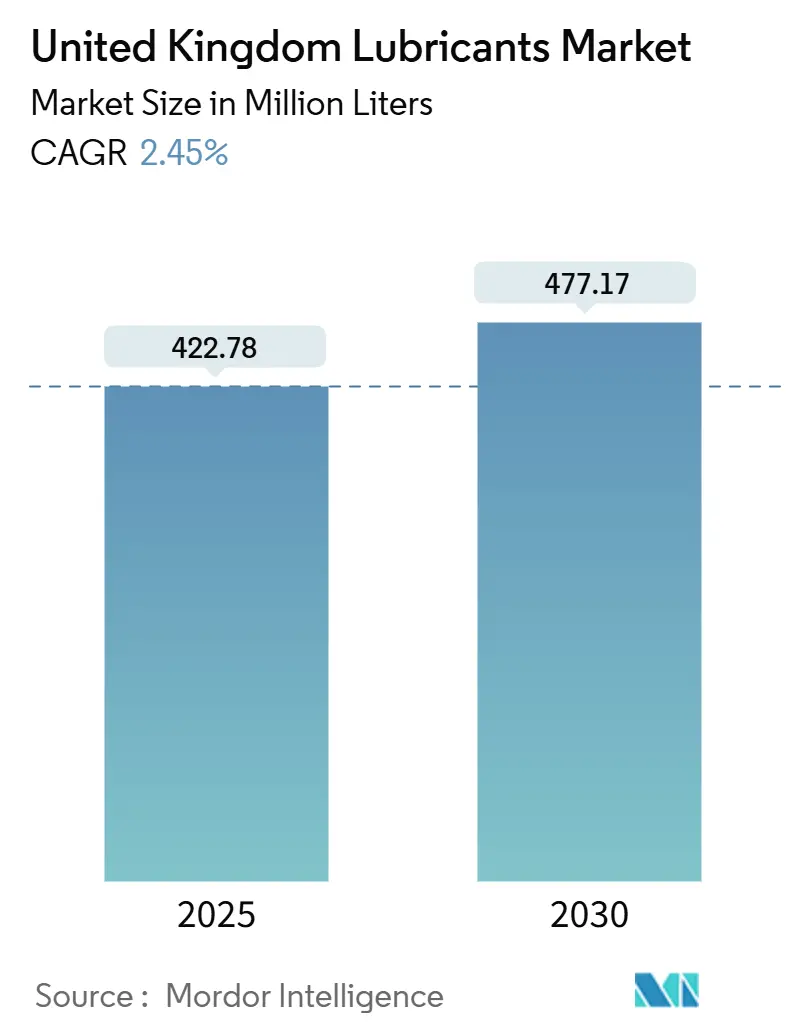

| Market Volume (2025) | 422.78 Million Liters |

| Market Volume (2030) | 477.17 Million Liters |

| Growth Rate (2025 - 2030) | 2.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Lubricants Market Analysis by Mordor Intelligence

The United Kingdom Lubricants Market size is estimated at 422.78 Million Liters in 2025, and is expected to reach 477.17 Million Liters by 2030, at a CAGR of 2.45% during the forecast period (2025-2030). Industrial demand linked to offshore wind, the reshoring of precision manufacturing, and the rollout of predictive-maintenance service models is accounting for a rising share of volume, even as conventional engine oil sales face a structural decline due to accelerating electric-vehicle (EV) uptake. Premium synthetic formulations continue to gain traction because Euro 7 emissions rules tighten performance requirements, fleet managers demand longer drain intervals, and plant operators seek to cut unplanned downtime. Suppliers with advanced additive chemistries, circular-economy base stocks, and IIoT-enabled fluid-monitoring platforms hold a competitive edge as industrial buyers prioritize reliability and compliance ahead of headline price. Meanwhile, shrinking domestic refining capacity is reshaping supply chain strategies, prompting blenders to adopt import hedging, specialty-grade localization, and re-refined feedstock integration to mitigate margin risk.

Key Report Takeaways

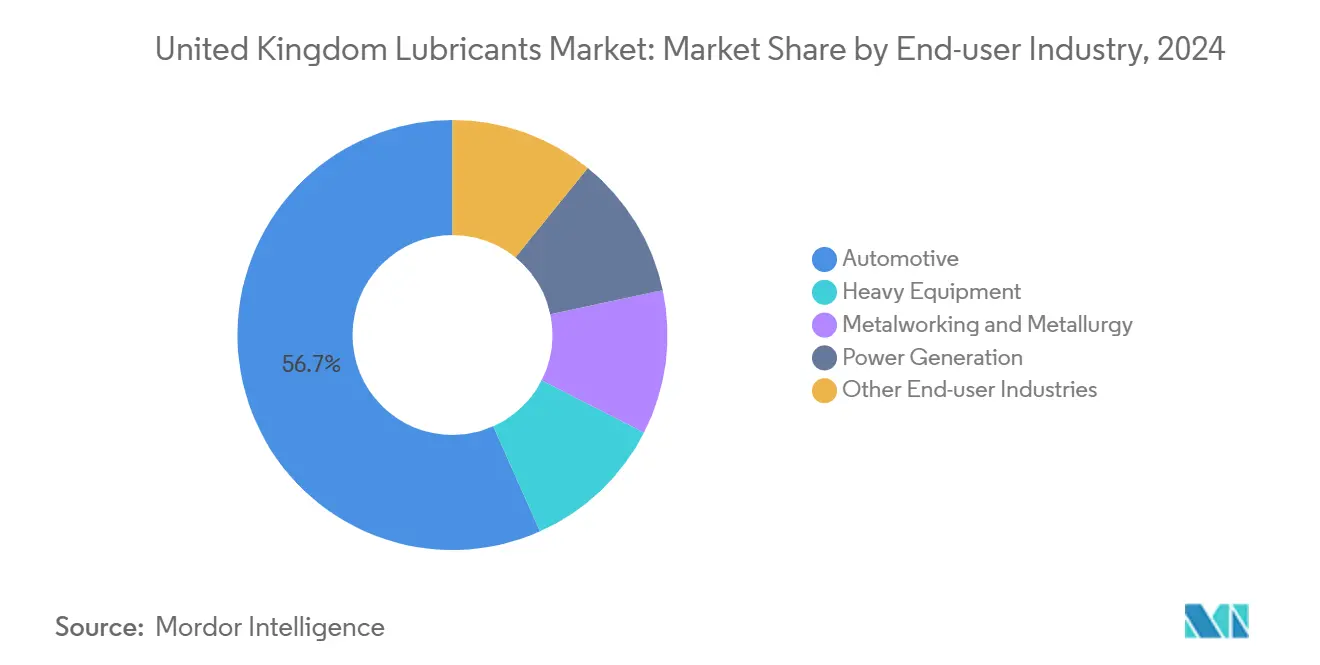

- By end-user industry, the automotive sector held 56.67% of the United Kingdom lubricants market share in 2024, whereas the power generation sector is projected to advance at a 2.89% CAGR through 2030.

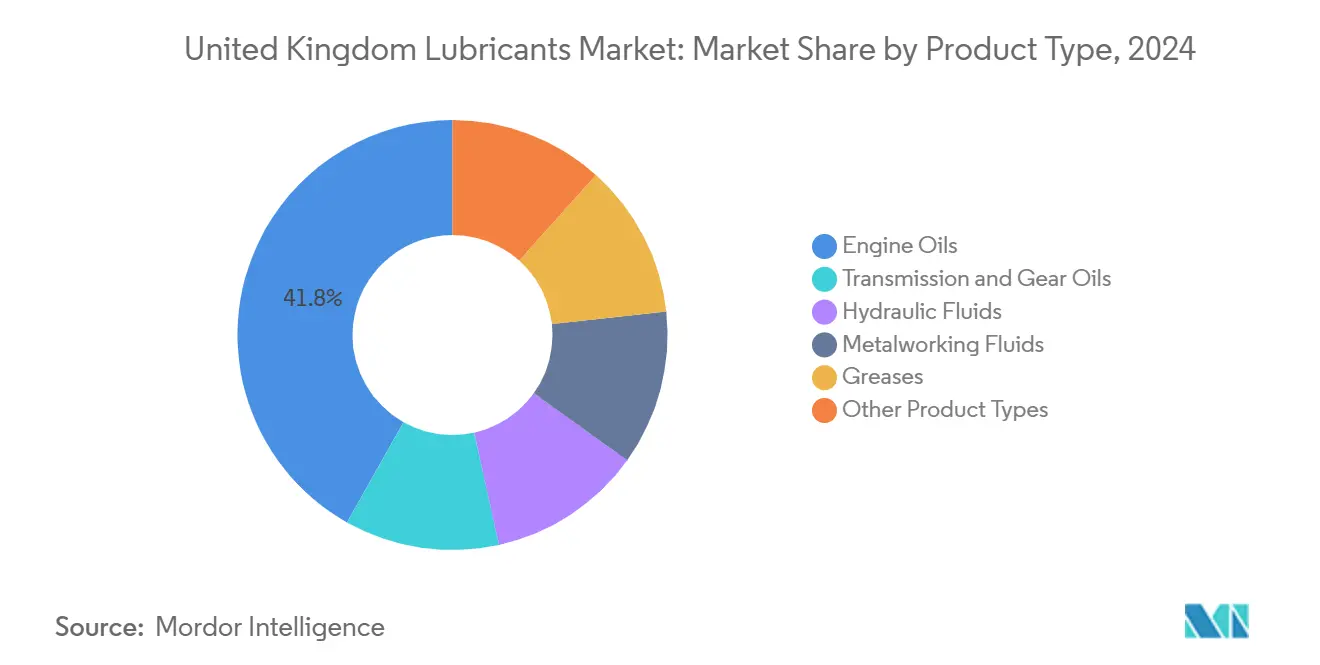

- By product type, engine oils commanded 41.84% of the United Kingdom lubricants market size in 2024, while greases are projected to grow at a 2.65% CAGR through 2030.

United Kingdom Lubricants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Euro 7 / UK CO₂-fleet rules spur premium synthetics | +0.8% | National, commercial-vehicle corridors | Medium term (2-4 years) |

| Manufacturing reshoring programmes | +0.6% | Midlands, North England, Central Belt Scotland | Medium term (2-4 years) |

| Offshore-wind build-out needs long-life greases | +0.4% | Scottish and North Sea coastlines | Long term (≥ 4 years) |

| IoT-enabled lube-as-a-service adoption | +0.3% | Manchester, Birmingham, Glasgow industrial hubs | Long term (≥ 4 years) |

| Circular-economy mandates boost re-refined oils | +0.2% | Early uptake in London and Edinburgh | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Euro 7 Emissions Standards Drive Premium Synthetic Adoption

Euro 7 rules, effective in 2025, impose tighter particulate and NOx thresholds that mineral oils struggle to meet, steering fleets toward synthetics with higher oxidation resistance and better low-viscosity film strength. Field data show that synthetics deliver 15–20% longer service life, reducing downtime and total ownership costs despite higher list prices[1]Lubrizol, “Synthetic Fluids for Euro 7 Compliance,” lubrizol.com. UK commercial-vehicle registrations climbed 8.2% in 2024, multiplying demand for Euro 7-grade lubricants in logistics, construction, and municipal fleets. Suppliers with proprietary additive packages enjoy margin upside, while legacy mineral producers retreat to price-sensitive legacy niches.

Manufacturing Reshoring Programmes Boost Industrial Lubricant Demand

Domestic output rose 3.1% in 2024 as firms relocated production from Asia, lifting consumption of metalworking fluids, hydraulic oils, and NSF-approved food-grade lubricants. Government incentives worth GBP 4.5 billion through 2026 target aerospace, electronics, and renewable-energy equipment, each rich in lubrication points. Midlands and Northern clusters report 25–30% spikes in industrial-fluid orders as greenfield plants ramp up, favoring suppliers with technical service teams and rapid-response warehouses.

Offshore Wind Expansion Creates Specialized Grease Market

Capacity is slated to reach 50 GW by 2030, with 70% of this concentrated in Scottish waters, where subarctic temperatures and salt spray accelerate component wear. Modern turbines contain 200–400 kg of grease across bearings, pitch systems, and yaw drives, requiring marine-grade chemistries that last five to seven years between relubrication visits[2]ExxonMobil, “Lubrication in Offshore Wind Turbines,” corporate.exxonmobil.com. Long-life formulas command price premiums of 40–60% and reward R&D investments from multinational blenders.

IoT Integration Transforms Lubrication Service Models

Factory managers adopt sensor-rich predictive-maintenance platforms that schedule fluid changes based on condition rather than calendar benchmarks. Shell’s LubeAnalyst cut unplanned downtime by 35% at United Kingdom sites through real-time alerts and auto-reorder APIs. Subscription analytics lock in repeat revenue and reposition lubricants as a managed service, tilting competitive advantage toward suppliers with digital diagnostics.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating EV parc lowers engine-oil volumes | -0.7% | Urban centers nationwide | Medium term (2-4 years) |

| Volatile crude and additive feedstock prices | -0.4% | Import-dependent supply chains | Short term (≤ 2 years) |

| Shrinking base-oil refining capacity | -0.3% | All UK distribution networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electric Vehicle Adoption Erodes Traditional Engine-Oil Demand

EV registrations surged 38% in 2024 to reach 315,000 units, accounting for 18.1% of new-car sales and reducing engine oil demand per vehicle. Fleet data indicate that electric vans reduce lubricant use by 60–70% compared to diesel models, as drivetrains shift to sealed bearings and coolant-damped power electronics. With a ban on new internal-combustion engine sales from 2030, engine oil volumes are expected to face permanent contraction despite the emergence of EV thermal-management fluids.

Volatile Feedstock Costs Pressure Margin Sustainability

Brent traded between USD 70 and USD 95 per barrel in 2024, while specialty additive prices spiked amid supply disruptions, resulting in 5–8% swings in finished-fluid costs. Currency volatility exacerbates input uncertainty for small blenders that lack long-term procurement leverage, leading to ad-hoc price adjustments that erode customer loyalty in price-sensitive segments.

Segment Analysis

By End-user Industry: Automotive Dominance Faces Electrification Pressure

The automotive segment accounted for 56.67% of the UK lubricants market in 2024, reflecting the nation’s 32 million-vehicle parc and dense commercial fleet activity. The UK lubricants market size tied to the automotive sector is forecast to decelerate as electrification advances; yet, premium synthetics for Euro 7 diesel vans and light trucks continue to support both volume and value. Large fleet operators now prioritize longer drain intervals and warranty-compliant low-SAP formulations to lower the total cost of ownership. Meanwhile, plant-based manufacturing reshoring reallocates lubricant demand toward heavy equipment in new gigafactories and food-processing lines, gradually trimming the automotive share.

Power generation currently holds only a single-digit percentage but is expected to register the fastest 2.89% CAGR as offshore wind capacity scales. Turbine OEMs mandate tailored ester-enhanced fluids and water-resistant greases that can run for seven-year intervals between servicing, driving high-unit-value sales. Construction equipment, marine, and aerospace collectively stabilize base-load volumes through mixed machinery parks that rely on hydraulic, gear, and compressor oils. Automotive suppliers reposition R&D budgets toward EV thermal-management fluids, while industrial specialists invest in field-service teams to support power-plant operators, indicating a gradual dilution of vehicle-centric revenue concentration.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Engine Oils Lead Despite EV Headwinds

Engine oils captured 41.84% of the 2024 volume, confirming their historical primacy in the UK lubricants market share. The share will decline but remain substantial through 2030 thanks to the legacy internal-combustion parc and Euro 7 demand for premium synthetics. The UK lubricants market size for engine oils is expected to shift from mineral to mid-SAPS and full-SAPS blends, characterized by lower volatility and improved low-ash profiles.

Greases top the growth leaderboard at a 2.65% CAGR, propelled by wind-turbine main-bearing requirements and factory automation that installs centralized grease-feeding systems. Transmission and gear oils post solid mid-single-digit volume, underpinned by heavy-duty truck activity and advanced manufacturing robotics. Metalworking fluids receive a boost from precision aerospace machining lines, although health and safety regulations are accelerating the adoption of boron-free and low-formaldehyde chemistries. Specialty compressor, transformer, and refrigeration oils fill high-margin niches shielded from commodity pricing battles due to stringent OEM technical approvals.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Regional consumption patterns align with industrial heritage, infrastructure development, and renewable energy investment. Scotland commands disproportionate volumes of marine-grade turbine greases, holding the lion’s share of the 70% capacity located in North Sea waters. Aberdeen service hubs anchor supply chains that ferry specialty fluids to offshore platforms via purpose-built vessels.

The Midlands corridor, stretching from Coventry to Birmingham, remains the single largest automotive lubricant pocket, absorbing roughly 35% of engine and gear oil demand, thanks to its dense OEM and Tier-1 supply chains. Heavy-equipment OEMs (original equipment manufacturers) operating in Stafford and the East Midlands are further deepening their hydraulic-fluid requirements. Northern England’s Manchester-Sheffield axis sustains robust metalworking-fluid consumption due to legacy steel and precision engineering clusters, while regional development funds lure battery and composite-material plants that bring fresh lubrication points.

London and the Southeast contribute sizable commercial-vehicle volumes through logistics, e-commerce fulfillment, and construction, despite passenger-car electrification lagging behind the national curve. Wales captures incremental growth from wind component manufacturing and port logistics tied to Celtic Sea offshore projects. Brexit-driven reshoring amplifies the strategic importance of local blending facilities near each consumption hub, reducing lead times and shielding buyers from cross-Channel freight exposure.

Competitive Landscape

The United Kingdom Lubricants Market is moderately consolidated. Shell adds digital analytics to bulk-fluid contracts, BP pilots bio-based ester chemistries, while ExxonMobil upgrades Fawley refinery to secure specialty base-oil supply. Strategic pillars focus on R&D for EV-specific fluids, localized blending to offset declining refinery output, and IoT service models that integrate condition monitoring into every liter sold. Market participants with balanced automotive-industrial portfolios and proprietary additive know-how are best positioned to withstand the twin headwinds of EV substitution and feedstock volatility.

United Kingdom Lubricants Industry Leaders

-

ExxonMobil Corporation

-

TotalEnergies

-

Shell plc

-

BP p.l.c.

-

Chevron Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: DriveTec unveiled its Bag-in-Box oil range for workshops nationwide. This new offering, which optimizes space for stocking engine oils, encompasses eight grades, collectively addressing more than 60% of the United Kingdom's car parc.

- February 2025: Metalube launched its next-generation, food-safe, NSF-registered high-performance chain oils. The new products are specifically designed to enhance overall equipment effectiveness through higher thermal stability.

United Kingdom Lubricants Market Report Scope

By End-user Industry

| Automotive |

| Heavy Equipment |

| Metalworking and Metallurgy |

| Power Generation |

| Other End-user Industries |

By Product Type

| Engine Oils |

| Transmission and Gear Oils |

| Hydraulic Fluids |

| Metalworking Fluids |

| Greases |

| Other Product Types |

| By End-user Industry | Automotive |

| Heavy Equipment | |

| Metalworking and Metallurgy | |

| Power Generation | |

| Other End-user Industries | |

| By Product Type | Engine Oils |

| Transmission and Gear Oils | |

| Hydraulic Fluids | |

| Metalworking Fluids | |

| Greases | |

| Other Product Types |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the UK lubricants market in 2025?

The market stands at 422.78 million liters in 2025. It is expected to grow to 477.17 million liters by 203.

Which end-user sector consumes the most lubricants?

Automotive accounts for 56.67% of 2024 volume, although its share will decline as EVs gain traction.

Which product category is expanding the fastest?

Greases lead with a 2.65% CAGR due to offshore wind-turbine demand.

How will electric vehicles affect lubricant demand?

EVs remove engine-oil requirements and can cut per-vehicle lubricant volumes by up to 70%.

What regional cluster shows the strongest growth?

Scotland is growing quickly as 70% of UK offshore wind capacity drives demand for marine-grade turbine greases.

Page last updated on: