Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

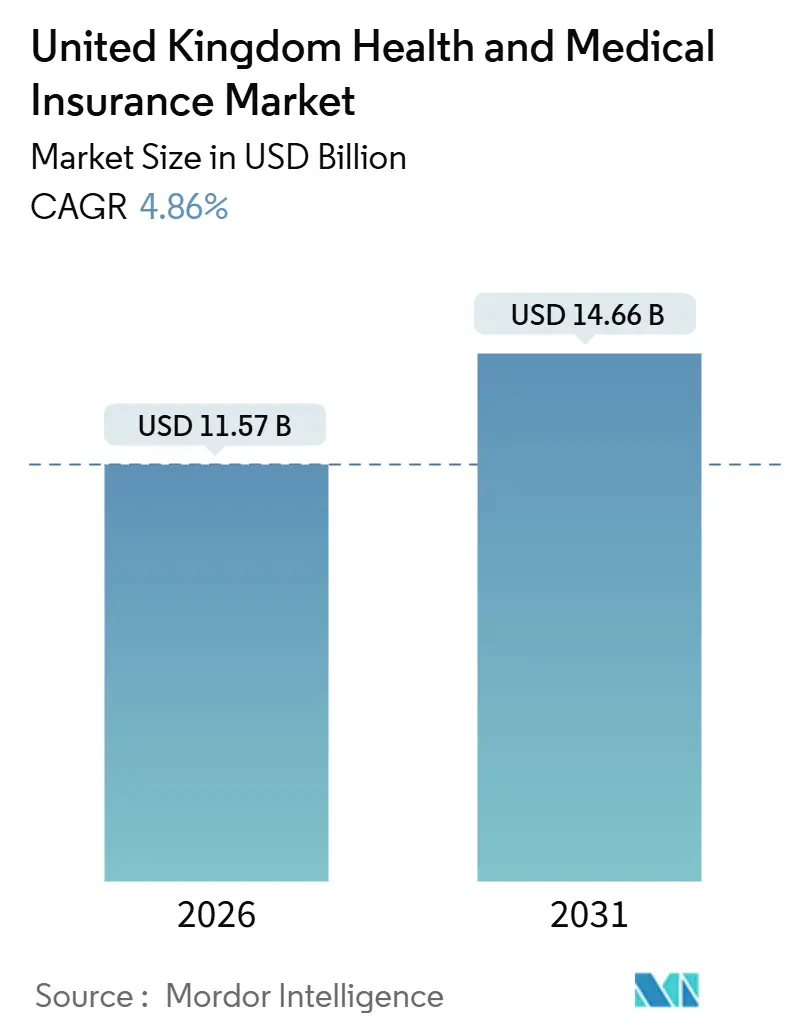

| Market Size (2026) | USD 11.57 Billion |

| Market Size (2031) | USD 14.66 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Health And Medical Insurance Market Analysis by Mordor Intelligence

The United Kingdom health and medical insurance market size is USD 11.57 billion in 2026 and is projected to reach USD 14.66 billion by 2031, reflecting a 4.86% CAGR. Elevated NHS waiting lists, digital access expectations, and broadening employer-sponsored coverage create a durable demand backdrop. Corporate schemes remain the anchor for distribution and enrollment, while digital-native channels gain traction with younger cohorts. Product strategies focus on comprehensive coverage for high-ticket care and on cash plans for affordable entry. England leads regional growth due to population concentration and provider infrastructure, with Northern Ireland recording the strongest growth outlook linked to cross-border dynamics and insurer expansion.

Key Report Takeaways

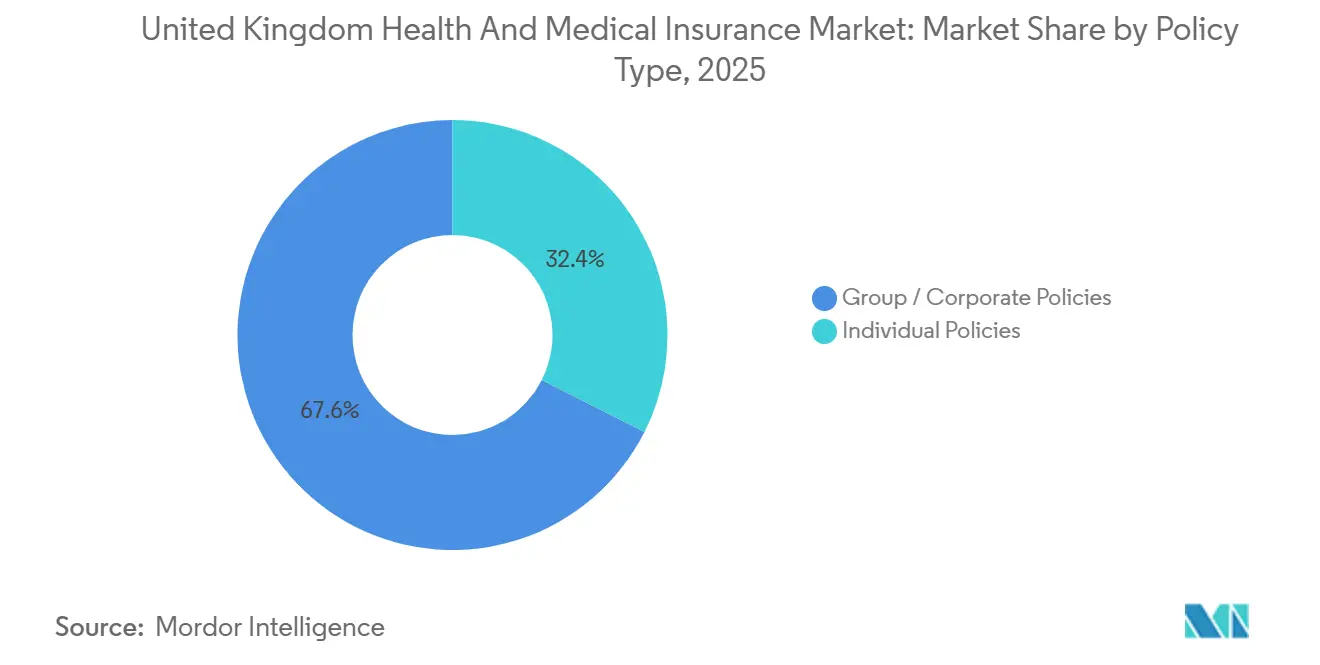

- By policy type, group and corporate policies led with 67.56% share of the United Kingdom health and medical Insurance market in 2025, while individual policies are forecasted to grow at a 6.48% CAGR through 2031.

- By coverage type, comprehensive in-patient and out-patient policies accounted for 61.86% share of the United Kingdom health and medical insurance market in 2025, and health cash plans are projected to expand at a 7.03% CAGR through 2031.

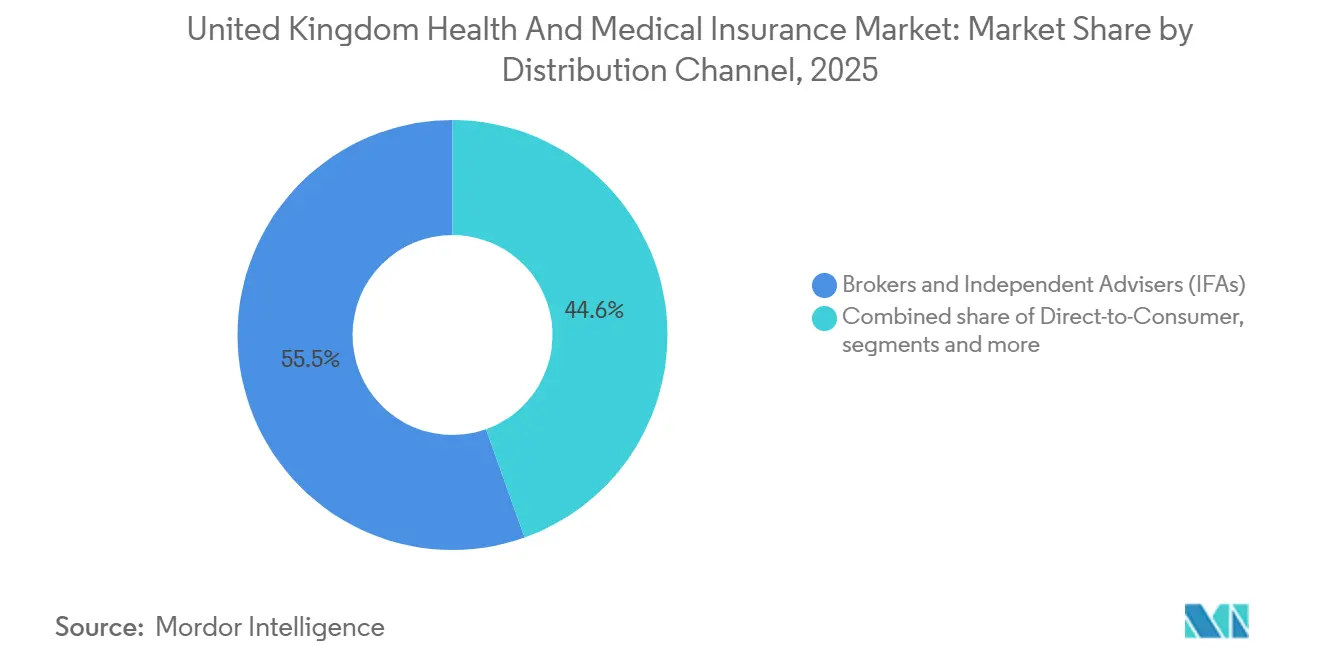

- By distribution channel, brokers and independent financial advisers held a 55.45% share of the United Kingdom health and medical insurance market in 2025, while online aggregators and insurtech platforms are projected to grow at a 7.84% CAGR through 2031.

- By end user, large corporates held 47.02% share of the United Kingdom health and medical insurance market in 2025, and individuals and families are projected to post the fastest 6.11% CAGR through 2031.

- By geography, England accounted for 82.29% share of the United Kingdom health and medical insurance market in 2025, and Northern Ireland is forecasted to record the fastest 5.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Health And Medical Insurance Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged NHS waiting lists | +1.8% | National, acute pressure in England with 7.39 million pathways as of April 2025 | Medium term (2-4 years) |

| Employer-sponsored benefits expansion | +1.2% | National, concentrated in London, Manchester, Birmingham | Short term (≤ 2 years) |

| Aging population and chronic disease | +0.9% | National, with older profiles in Scotland and Wales | Long term (≥ 4 years) |

| Digital-first, app-based administration | +0.6% | National, the highest penetration in urban England | Short term (≤ 2 years) |

| Salary-sacrifice PMI tax advantages | +0.5% | National, the strongest benefits for higher-rate taxpayers in Southeast England | Medium term (2-4 years) |

| Virtual GP networks as gatekeepers | +0.3% | National, addressing rural access gaps in Scotland, Wales, and Northern Ireland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Prolonged NHS Waiting Lists Fuelling Demand for Private Medical Insurance

NHS operational statistics show 7.39 million pathways awaiting treatment in April 2025, equivalent to an estimated 6.23 million individual patients, with only 59.7% of pathways treated within the 18-week constitutional standard, which remains well below the 92% target, keeping access constraints elevated in 2026[1]NHS England, “Monthly Operational Statistics, June 2025,” NHS England, england.nhs.uk. Pathways exceeding 52 weeks totaled 190,068, including 9,258 patients waiting over 65 weeks and 1,361 over 78 weeks, reinforcing the urgency households and employers feel about parallel private access solutions. Insurance-funded private hospital admissions reached 163,680 in Q2 2025, or 70% of total admissions, indicating that the United Kingdom health and medical insurance market is absorbing demand displaced by NHS wait times. Chemotherapy admissions rose 2% year over year in Q2 2025 to 18,540 treatments, a signal that oncology pathways are a specific pressure point driving insured utilization[2]Private Healthcare Information Network, “PHIN private market update: December 2025 UK,” Private Healthcare Information Network, phin.org.uk. Diagnostic waiting lists reached 1.7 million people in April 2025, with 21.2% waiting six weeks or more, which is pushing comprehensive policies that bundle imaging and endoscopy access to the forefront of product design in the United Kingdom health and medical insurance market.

Expansion of Employer-Sponsored Health Benefits Post-COVID-19

Employer-sponsored group policies covered 4.7 million people in 2023, the highest level in more than 30 years of ABI records, and the single largest driver of scale in the United Kingdom health and medical insurance market. Workplace claims rose 26% year over year to 1.3 million in 2023, with GBP 2.27 billion (USD 3.05 billion) paid, which underscores that employers are funding real use rather than offering symbolic benefits. Employers value reduced sickness absence, with ABI data suggesting prevention of 14 million lost working days annually, a productivity effect that supports continued premium budgets in 2026. Continuation of favorable tax treatment for salary sacrifice in the November 2025 Budget provides multi-year planning certainty for corporate benefits strategies and supports broader employee-funded participation, which widens the addressable base for the United Kingdom health and medical insurance market. As SMEs adopt streamlined group products through digital onboarding, distribution gains in the small employer segment complement large corporate renewals, sustaining a diverse demand pipeline in 2026.

Ageing Population & Chronic Disease Prevalence

The UK population reached 69.5 million in mid-2025, with populations aged 65 and over growing at 1.8–2.0% annually across the nation, an aging trend that expands utilization risk and reinforces supplemental coverage demand in the United Kingdom health and medical insurance market[3]Office for National Statistics, “UK Health Accounts: 2023 and 2024,” Office for National Statistics, ons.gov.uk. The Department of Health and Social Care cites 17 million adults with at least one long-term condition in England, generating GBP 23 billion (USD 30.94 billion) in acute care costs annually, a load that strains NHS capacity and points households toward private care for faster specialist access[4]HM Treasury, “Budget 2025 Policy Costings,” HM Treasury, assets.publishing.service.gov.uk. The United Kingdom health and medical insurance market aligns products to early intervention pathways and specialist diagnostics that help slow acute exacerbations in high-need cohorts, which fit demand patterns in older populations. Public budget pressures are expected to remain persistent, with policy papers reaffirming long-run growth in health and long-term care outlays as a share of GDP in the coming decades, which implies ongoing pressure for complementary private coverage in 2026 and beyond. These structural forces keep chronic disease and aging demographics central to growth discussions in the United Kingdom health and medical insurance market.

Rapid Uptake of Digital-First, App-Based Policy Administration

The 10 Year Health Plan commits to making the NHS App the full front door by 2028, and mandates that 70% of elective appointments are viewable digitally by March 2026, which sets baseline digital expectations that private insurers match through smooth mobile journeys in the United Kingdom health and medical insurance market. NHS operational guidance for 2025/26 requires universal rollout of core digital capabilities such as records access, online consultations, appointment management, and prescriptions through the NHS App, signaling a decisive shift in consumer behavior that private policies leverage with frictionless claims, preauthorization, and virtual GP access. Online appointment booking adoption rose from 6.8% in 2015 to 41% in 2024, which supports the pivot to app-based engagement and self-service across insurance lifecycles. FCA data confirms healthcare cash plans delivered 69% of premiums as claims in 2024, a result consistent with digitization benefits in claims processing and funds transfer, strengthening perceived value propositions. In 2026, these digital baselines anchor product differentiation in the United Kingdom health and medical insurance market through faster service, transparent coverage, and convenient care navigation.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium inflation outpacing wage growth | -0.7% | National, stronger effect on individual buyers and SMEs | Short term (≤ 2 years) |

| Market consolidation is reducing choice | -0.4% | National, with the top four carriers at an estimated 70% combined share | Long term (≥ 4 years) |

| Prospective NHS reforms are dampening PMI's need | -0.5% | Primarily England, with targets to lift 18‑week performance | Long term (≥ 4 years) |

| Data-privacy limits on wearable underwriting | -0.2% | National, bounded by UK GDPR and FCA consumer duty | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Inflation Outpacing Wage Growth

ONS Health Accounts show voluntary health insurance expenditure grew 2.4% in real terms in 2023, while real-terms claims costs rose 12.3%, implying insurers absorbed much of the medical inflation rather than fully repricing premiums in that period. ABI reported record claims payouts of GBP 3.57 billion (USD 4.80 billion) in 2023, up 21% from 2022, which increases the likelihood of premium rate corrections that can strain affordability for households and SMEs in 2026. Individual policyholders are most exposed because adverse selection effects concentrate risk when healthier members lapse, and older or sicker members retain coverage. Employers also face tougher renewal discussions if double-digit increases collide with budget limits, which can trigger design changes, higher excesses, or greater employee contributions. The United Kingdom health and medical insurance market therefore, balances strong demand with price sensitivity, and affordability remains a near-term friction point in 2026.

Prospective NHS Reforms Dampening Perceived Need for PMI

The 10 Year Health Plan for England targets restoration of the 18-week elective standard to 65% by March 2026 and ultimately aims for 92%, which, if achieved, could reduce perceived necessity for parallel private coverage over time. The Plan asks NHS organizations to deliver 4% productivity improvements in 2025/26, with sustained gains thereafter, alongside deepening the NHS App as the primary digital front door, which can improve access and convenience. Implementation extends through 2035 in stages, which gives the United Kingdom health and medical insurance market time to expand in the interim, yet steady progress could gradually compress the demand differential. Budget outlooks show health spending taking a rising share of day-to-day public expenditure across the Parliament, which underscores the scale of effort required to deliver sustained improvements. Behavioral persistence also matters because employers and families that adopt private insurance often retain it even if NHS service levels improve, limiting potential substitution in 2026.

Segment Analysis

By Policy Type: Corporate Schemes Propel Market Dominance

Group and corporate policies accounted for 67.56% of the 2025 share and covered 4.7 million people in 2023, giving this segment the largest enrollment base in the United Kingdom health and medical insurance market. Large employers with 250 or more staff treat private cover as a talent necessity in competitive sectors and anchor renewal stability in 2026. Workplace claims reached 1.3 million in 2023 with GBP 2.27 billion (USD 3.05 billion) in payouts, a scale that reflects real utilization rather than latent take-up. Risk pooling across employee populations supports richer benefits at competitive unit costs relative to individually underwritten policies. The United Kingdom health and medical insurance market also benefits from multi-year corporate planning cycles, which smooth demand across economic conditions.

Individual policies held 32.44% of the 2025 share and are projected to be the fastest-growing policy type at a 6.48% CAGR through 2031, supported by digitally enabled sales and salary sacrifice awareness. The individual buyer mix spans self-employed professionals, retirees supplementing NHS access, and employees without group benefits who are willing to self-fund through tax-efficient mechanisms. Digital aggregators compress search and acquisition costs, which improves price transparency and conversion. As inflation pressure eases for households, willingness to pay for faster diagnostics and consultant access is improving in 2026. These conditions expand the customer base for the United Kingdom health and medical insurance market as individual cover complements group growth.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Coverage Type: Comprehensive Plans Dominate, Cash Plans Accelerate

Comprehensive inpatient and outpatient policies held 61.86% of the 2025 share and serve members seeking wide diagnostic access, consultant choice, mental health pathways, and surgical coverage, which sustains high revenue per member in the United Kingdom health and medical insurance market. The Private Healthcare Information Network recorded insurance-funded admissions at 163,680 in Q2 2025 and cited a 2% year-over-year increase in chemotherapy admissions to 18,540, a trend that underscores the need for robust oncology benefits. These policies also feature enhanced imaging access and post-operative rehabilitation, which are valued as NHS waiting times persist in 2026. Providers and insurers align network strategies around location density and specialization to optimize member access. The United Kingdom health and medical insurance market continues to position comprehensive cover as the benchmark for full-service private pathways.

Health cash plans are projected to grow at a 7.03% CAGR through 2031, an outcome supported by FCA value measures showing 69% of premiums returned as claims in 2024 and by low monthly premiums in the GBP 10–30 (USD 13.45 - 40.36) range that appeal to budget-conscious consumers. Claims journeys are simple and fast, which builds positive word of mouth and retention. Inpatient-only core policies priced around GBP 600–1,200 (USD 807.31 - 1,614.6) annually offer catastrophic protection at a lower cost for households prioritizing financial security. Dental and specialist covers address constrained NHS access, while standalone virtual GP subscriptions at GBP 5–15 (USD6.72 - 20.18) per month create low-commitment entry points. The United Kingdom health and medical insurance market size for health cash plans is projected to expand at a 7.03% CAGR between 2026 and 2031, reinforcing their role as on-ramps to broader protection.

By Distribution Channel: Digital Platforms Disrupt Broker Dominance

Brokers and independent financial advisers held 55.45% of the 2025 share, reflecting entrenched corporate relationships and specialist expertise that remains essential to large-scheme procurement in the United Kingdom health and medical insurance market. Commission-based remuneration around group placements sustains broker economics at renewal, while some large buyers shift to fee-based engagements for advice separation. Complex benefit designs and multi-site employers continue to value human intermediation in 2026. Advisory relationships also steward scheme governance and ROI, which reinforces stickiness for the broker channel. This foundation supports the United Kingdom health and medical insurance industry while digital channels scale.

Online aggregators and insurtech platforms are the fastest-growing channel with a projected 7.84% CAGR, benefiting from digital-native buyer preferences and lower acquisition costs when quotes are standardized and instantly comparable across carriers. Young professionals accept self-service onboarding in exchange for transparent pricing and convenience. Direct-to-consumer channels account for around 23% of share complement aggregator growth and give insurers control of the customer journey, reducing commission loads and enabling sharper pricing. Bancassurance and affinity partnerships add access to bank and membership organizations with relevant profiles. The United Kingdom health and medical insurance market adapts to hybrid distribution, where brokers, direct channels, and aggregators each play distinct roles across segment needs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Large Corporations Lead, Individuals, and SMEs Accelerate

Large corporates held 47.02% of the 2025 end-user share and anchored installed coverage of 4.7 million people in 2023, reinforcing their status as the core demand pillar in the United Kingdom health and medical insurance market. Leading sectors include financial services, technology, pharmaceuticals, and professional services. Experience-rated pricing rewards employers with favorable claims histories and supports long-term benefit planning. ABI analysis indicates that health and protection insurance prevents 14 million sickness days annually, equivalent to 12,500 full-time workers, which informs benefit budget decisions. In 2026, employers continue to prioritize coverage as part of total reward narratives and business continuity plans.

Individuals and families are projected to grow the fastest at a 6.11% CAGR through 2031 as digital tools reduce acquisition friction and salary-sacrifice awareness lowers effective costs for higher-rate taxpayers. Cash plans at GBP 10–30 (USD 13.45 - 40.36) per month expand participation for cost-sensitive buyers who want value without underwriting hurdles. The SME segment, estimated at 24–26% of the 2025 end-user share, is a growth frontier as insurtech platforms automate enrollment, payroll integration, and mobile administration for businesses with 10–249 employees. Salary sacrifice models enable SMEs to facilitate access without bearing the full premium burden. The United Kingdom health and medical insurance market uses product tiers to serve each end user profile, aligning benefit depth with price points and digital preferences.

Geography Analysis

England held 82.29% of the 2025 regional share, reflecting population concentration and private hospital density as the main anchors of demand in the United Kingdom health and medical insurance market. Greater London accounted for 61,355 insurance-funded admissions in Q2 2025 and represented 37.5% of total United Kingdom insurance-funded activity, which far exceeds its 13% share of the national population and underlines London’s unique role in insured utilization. NHS England reported 7.39 million pathways awaiting treatment and 59.7% compliance with the 18-week standard in April 2025, which pressures households and employers to secure faster private pathways. PHIN noted 206,465 total private admissions in England in Q2 2025, with a modest year-over-year decline, yet insurance-funded volumes remained stable at scale. England accounted for 82.29% of the United Kingdom's health and medical insurance market size in 2025, which maps closely to its share of the United Kingdom's total population.

Scotland holds an estimated 6 - 7% of the 2025 share and recorded 13,455 total private admissions in Q2 2025, a rise of 3% year over year that contrasts with England’s decline and reflects localized demand resilience. Insurance-funded admissions in Scotland increased 3% to 7,290 in Q2 2025, signaling steady penetration gains from a lower base. The nation’s median age reached 42.8 years in mid-2024, tied with Wales as the oldest in the United Kingdom, which structurally supports the need for faster access to diagnostics and specialists. Infrastructure is concentrated in Glasgow and Edinburgh, so insurers balance networks with accessible cross-border care where necessary. Scotland’s share is expected to rise gradually as insurers target older professional cohorts and as digital pathways reduce access frictions.

Wales accounts for around 4 - 5% of the 2025 share, near its population share, and recorded 8,015 total private admissions in Q2 2025, a 2% decline year over year. Insurance-funded admissions held steady at 3,465, indicating stable insured demand even as self-pay softened. Wales shares with Scotland a median age of 42.8 years and limited private hospital distribution beyond Cardiff and Swansea, though proximity to Bristol and Birmingham supports network breadth for insured members. Northern Ireland holds around 3 - 4% of the 2025 share but is projected to grow the fastest at a 5.96% CAGR to 2031, assisted by cross-border care options and insurer expansion into Belfast’s growing professional services hub. Northern Ireland’s median age of 40.3 years, the youngest in the United Kingdom, provides a runway for future growth as care needs rise with age.

Competitive Landscape

The United Kingdom health and medical insurance market is moderately concentrated, with Bupa, AXA Health, Aviva, and VitalityHealth collectively estimated at around 70% share, while the broader United Kingdom insurance sector spans around 350 authorized firms supervised by the PRA for solvency and prudential standards. The Competition and Markets Authority continues to enforce the Private Healthcare Market Investigation Order 2014, securing compliance plans from three hospitals and transparency actions for 88 consultants in the 2024 - 25 period, which improves price and quality information for insured patients. The United Kingdom health and medical insurance market in 2026 emphasizes digital journeys, real-time authorizations, and integrated virtual GP services as mainstream differentiators.

VitalityHealth’s early move to integrate wearable incentives set a baseline for engagement programs that competitors matched with wellness initiatives tied to activity and prevention, which frame behavior-linked benefits as a common feature in 2026. Insurers deploy proprietary mobile apps to integrate policy management, telemedicine, and claims submission with photo uploads, which aligns with the NHS digital mandate and shapes expectations for fast, transparent service. Distribution strategies balance broker strength in corporate schemes with direct-to-consumer capabilities and aggregator partnerships to reach digital-native buyers efficiently. The United Kingdom health and medical insurance market continues to invest in automation to reduce operating expense ratios and to support sustainable pricing without sacrificing service quality, as indicated by the FCA’s value measures and complaint trends.

White-space opportunities cluster in SME group cover via digital onboarding, chronic condition navigation for the 17 million adults with long-term conditions, and targeted growth in Scotland, Wales, and Northern Ireland, where underpenetration offers room to expand. Health cash plans, projected to grow at a 7.03% CAGR, provide affordable entry points and function as acquisition channels for upgrades to comprehensive cover over time. The United Kingdom health and medical insurance market, therefore, aligns long-term strategy around multi-segment funnels, digital-first service, and employer partnerships that balance affordability and breadth of care.

United Kingdom Health And Medical Insurance Industry Leaders

Bupa

AXA Health

Aviva

VitalityHealth

WPA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: Nexus completed its acquisition of Sure Insurance Services, a specialist in medical tourism insurance. This expands Nexus’s underwriting capabilities and strengthens its niche product offerings across multiple markets, including the United Kingdom.

- October 2025: The Financial Conduct Authority published general insurance value measures data for 2024, reporting that healthcare cash plans delivered 69% of premiums as claims payouts compared to 72% in 2023. This data enhances market transparency by providing common indicators of value, including claims frequency, acceptance rates, average payouts, and claim complaint rates, enabling consumers to make more informed purchasing decisions and driving competitive discipline around value delivery. The FCA announced plans for a post-implementation review of value measures rules, with findings expected in summer 2026.

- September 2025: Berkshire Hathaway Specialty Insurance introduced new Group Personal Accident and Business Travel insurance products in the United Kingdom market, combining traditional coverage with digital health services like 24/7 virtual GP access and emergency support.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom health and medical insurance market as all private medical insurance policies, healthcare cash plans, and stand-alone dental covers sold to individuals, small groups, and large corporates, measured by gross earned premiums in USD terms.

Scope Exclusion: National Health Service expenditure, self-pay medical fees, critical-illness riders, and accident-only policies lie outside this market.

Segmentation Overview

- By Policy Type

- Individual Policies

- Group / Corporate Policies

- By Coverage Type

- In-patient Only (Core)

- Comprehensive (In- & Out-patient)

- Health Cash Plans

- Dental & Specialist Covers

- Other/Emerging (e.g., Virtual GP Access, Wellness Plans)

- By Distribution Channel

- Brokers & Independent Financial Advisers (IFAs)

- Direct-to-Consumer (Insurer)

- Bancassurance & Affinity Partnerships

- Online Aggregators / Insurtech Platforms

- By End User

- Individuals & Families

- Small & Medium Enterprises (SMEs)

- Large Corporates

- By Region (United Kingdom)

- England

- Scotland

- Wales

- Northern Ireland

Detailed Research Methodology and Data Validation

Primary Research

We spoke with brokers, human-resource benefit managers, actuaries at leading insurers, and independent financial advisers across England, Scotland, Wales, and Northern Ireland. Their insights on average group premium hikes, rising cash-plan penetration, and employer tender cycles bridged the information gaps left by desk research and guided final assumptions.

Desk Research

Mordor analysts started with reputable open sources such as the Office for National Statistics family-spending tables, the FCA Financial Lives Survey, Private Healthcare Information Network admission data, Association of British Insurers premium statistics, and OECD Health Accounts. Company filings and investor presentations added price and uptake details, while paid databases like D&B Hoovers and Dow Jones Factiva supplied insurer revenue splits.

Trade journals, parliamentary briefings, and patent activity on tele-health platforms helped us track emerging benefit designs and cost trends.

This list is illustrative; many additional public and proprietary references were tapped for validation and clarification.

Market-Sizing & Forecasting

A top-down reconstruction of earned premiums was built from HMRC tax data on employer-funded benefits, PHIN insured admission ratios, and per-capita PMI penetration. Select bottom-up checks, sampled average premiums multiplied by disclosed policy counts, served as guardrails before reconciliation. Key variables include: number of adults holding PMI, average corporate premium inflation, NHS waiting-list backlog, dental plan uptake, and cash-plan claim ratios. Multivariate regression anchors the forecast, with scenario analysis applied to NHS backlog clearance speeds. Any residual gaps in bottom-up estimates are prorated across product lines based on historic mix.

Data Validation & Update Cycle

Outputs pass multi-layer analyst review, variance checks against ABI and ONS trend series, and peer audits. Reports refresh annually, and material events such as regulatory tax changes trigger interim model updates. Before delivery, an analyst reruns the model to ensure clients receive our latest view.

Why Mordor's UK Health and Medical Insurance Baseline Commands Reliability

Published estimates often diverge because firms fold in different revenue streams, convert currencies at varied points, or update models on uneven cadences.

Key gap drivers stem from scope breadth, the handling of public spend, and premium inflation assumptions. Mordor's disciplined exclusion of NHS outlays, use of earned-not written premiums, and yearly refresh make our baseline the dependable choice for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.03 B (2025) | Mordor Intelligence | - |

| USD 266.4 B (2022) | Global Consultancy A | Includes NHS health spend and long-term care outlays, and applies average healthcare inflation rather than product-specific premiums. |

| USD 290.9 B (2024) | Industry Association B | Blends compulsory national insurance with private premiums and uses broad annual FX averages that overstate USD figures. |

| USD 64.3 B (2024) | Regional Consultancy C | Adds critical-illness and life-linked riders and assumes full policy uptake across reported memberships. |

In sum, while other publishers widen or compress definitions, our carefully bounded scope, transparent variables, and frequent refreshes provide a balanced, traceable baseline that clients can replicate and stress-test with confidence.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the United Kingdom health and medical insurance market growth outlook through 2031?

The market is USD 11.57 billion in 2026 and is projected to reach USD 14.66 billion by 2031 at a 4.86% CAGR.

Which policy type leads and which grows fastest in the United Kingdom health and medical insurance market?

Group and corporate policies lead with 67.56% share in 2025, while individual policies are projected to grow at a 6.48% CAGR through 2031.

How do NHS waiting lists influence the United Kingdom health and medical insurance market?

With 7.39 million pathways and only 59.7% treated within 18 weeks as of April 2025, prolonged waits push households and employers toward private cover for faster access.

Which coverage types are most attractive to buyers in 2026?

Comprehensive in patient and out patient policies hold 61.86% share for broad protection, while health cash plans are projected at a 7.03% CAGR as low cost, accessible options.

What regional trends define the United Kingdom health and medical insurance market?

England holds 82.29% share due to population and infrastructure scale, while Northern Ireland has the fastest projected CAGR at 5.96% through 2031.

How are digital tools changing customer expectations in this space?

The NHS App targets 70% of elective appointments visible digitally by March 2026, and insurers mirror that with mobile policy management, virtual GP access, and real time claims.