| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Volume (2025) | 2.35 Million tonnes |

| Market Volume (2030) | 2.71 Million tonnes |

| CAGR | 2.94 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Glass Bottles and Containers Market Size")

United Kingdom (UK) Glass Bottles and Containers Market Analysis

The United Kingdom Glass Bottles and Containers Market size is estimated at 2.35 million tonnes in 2025, and is expected to reach 2.71 million tonnes by 2030, at a CAGR of 2.94% during the forecast period (2025-2030).

The UK glass packaging industry is experiencing significant transformation driven by evolving consumer preferences and macroeconomic challenges. According to trade data from April 2023, the UK's glass bottle imports totaled £40.7 million while exports stood at £15.8 million, resulting in a trade deficit of £24.9 million. This trade imbalance reflects the growing domestic demand and the need for increased local production capacity. The industry has witnessed substantial investments in glass bottle manufacturing capabilities, with several companies expanding their facilities to meet the rising demand. The sector's evolution is further shaped by changing consumer behavior, as evidenced by the increase in consumer spending on food and beverages, which reached £126.74 billion in 2022.

Energy costs and sustainability considerations are reshaping the industry's operational landscape. In 2022, industry surveys revealed that 72% of manufacturers were very concerned about rising energy prices, compared to just 33% in 2021. This has prompted significant investments in energy-efficient technologies and alternative energy sources. In July 2023, Encirc announced plans to develop a hydrogen-powered furnace at its Elton plant, demonstrating the industry's commitment to reducing energy consumption while maintaining production capacity. These initiatives are transforming the manufacturing processes while addressing both economic and environmental concerns.

Technological advancements are driving innovation in glass packaging solutions and manufacturing. Companies are increasingly focusing on lightweight glass solutions and enhanced decoration capabilities to meet evolving market demands. In July 2023, Croxsons manufactured innovative primary packaging for Necessary Good, featuring sophisticated design elements and sustainable characteristics. The industry is witnessing a shift toward more specialized and premium packaging solutions, particularly in the spirits and cosmetics sectors, where brand differentiation through packaging design has become crucial.

The industry is experiencing a significant shift toward circular economy principles and sustainable practices. British Glass reports that the UK's glass sector has achieved a recycling rate of 68.8%, one of the highest compared to other packaging materials. In 2023, several manufacturers have implemented closed-loop recycling systems, with companies like Beatson Clark incorporating up to 45% recycled content in their amber glass production. The industry's commitment to sustainability is further evidenced by initiatives such as the Glass Futures project, which aims to develop innovative, low-carbon manufacturing technologies.

United Kingdom (UK) Glass Bottles and Containers Market Trends

Increased Demand for Glass Packaging in the Beverage Industry

The beverage industry's growing preference for glass packaging is driven by both consumer demands and product quality considerations. Glass bottles are increasingly favored for alcoholic beverages due to their ability to preserve aroma and flavor, particularly in the premium spirits and wine segments. According to the UN Comtrade report, the value of wine exports in the United Kingdom reached approximately £557 million in 2022, significantly up from £467 million in 2021, indicating a robust demand for glass packaging in the wine sector.

The beer segment continues to be a significant driver of glass packaging demand. According to the Office for National Statistics (UK), beer remains the most popular alcoholic drink in the country, with consumers spending more than £76.4 billion on the beverage in 2022. This trend is further supported by the growing craft beer movement, where glass packaging is preferred for its premium appearance and product preservation capabilities. Additionally, in 2023, on-premise drink sales showed significant growth, with beer and cider sales in managed venues increasing by 7% compared to 2022, while cider sales alone saw a remarkable 25% year-over-year increase.

Understand The Key Trends Shaping This Market

Download PDF

Recyclability Benefits Offered by Glass Packaging Drive Sustainability

Recyclable glass packaging's infinite recyclability without quality degradation has become a crucial driver in the market's growth. According to British Glass, making new glass from recycled glass reduces CO2 emissions and energy use, saving 580 kg of carbon dioxide emissions with every ton of glass re-melted. The industry has demonstrated strong commitment to sustainability, with manufacturers like Beatson Clark incorporating an average of 45% recycled material in amber glass containers and 30% in white flint production.

The push toward sustainability is further evidenced by significant industry initiatives and investments. In December 2022, Encirc announced its partnership with Diageo to produce net zero glass at scale by 2030, with plans to build a new furnace at its Elton plant that would reduce carbon emissions by 90% using a combination of green electricity, low-carbon hydroxide, and carbon capture technology. This commitment to sustainability is reinforced by consumer preferences, as demonstrated by recent surveys showing that 64% of UK consumers are more likely to purchase from retailers offering sustainable packaging, and approximately 50% are willing to pay extra for sustainable packaging and delivery.

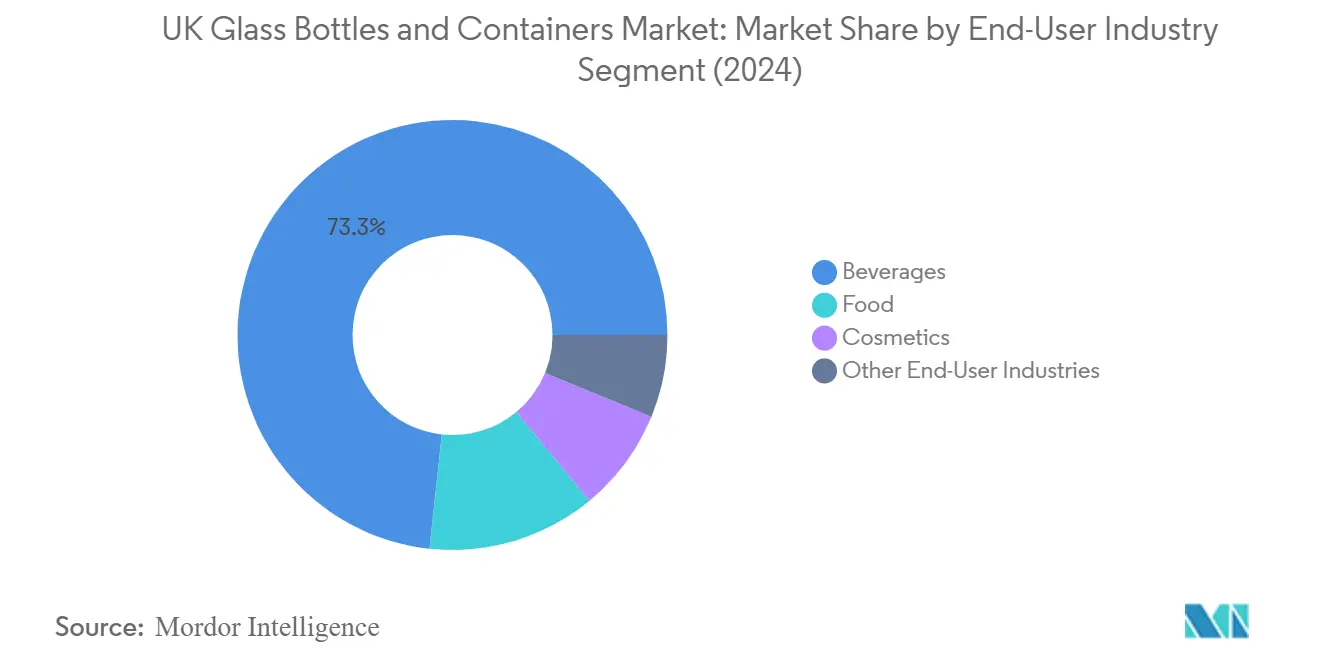

Segment Analysis: By End-User Industry

Beverages Segment in UK Glass Bottles and Containers Market

The beverages segment dominates the UK glass bottles and containers market, commanding approximately 73% market share in 2024. This substantial market presence is primarily driven by the extensive use of glass packaging containers in both alcoholic and non-alcoholic beverages. The segment's dominance is particularly evident in the alcoholic beverages category, where glass bottle packaging remains the preferred packaging material for premium spirits, wines, and craft beers due to its ability to preserve product quality and enhance brand perception. The non-alcoholic beverage sector, including carbonated soft drinks and premium water brands, also significantly contributes to this segment's leadership position. Glass packaging containers' inherent properties of chemical inertness, non-porosity, and impermeability make them particularly suitable for beverage applications, especially for premium food and beverage brands that prefer glass containers over other packaging options.

Food Segment in UK Glass Bottles and Containers Market

The food segment is emerging as the fastest-growing category in the UK glass bottles and containers market, with a projected growth rate of approximately 4% from 2024 to 2029. This robust growth is driven by increasing consumer demand for sustainable packaging solutions in food products, particularly in categories such as instant coffee, processed baby foods, dry mixes, spices, dairy products, sugar preserves, syrups, spreads, and processed fruits and vegetables. The segment's growth is further supported by the rising preference for food glass packaging in premium food products, as glass containers offer superior product preservation capabilities and align with the growing consumer emphasis on eco-friendly packaging solutions. The food industry's increasing focus on premium packaging and sustainable solutions continues to drive innovation in glass container designs and specifications, particularly for specialty food products and gourmet items.

Remaining Segments in End-User Industry

The cosmetics and other end-user industries segments complete the market landscape, each serving distinct applications and consumer needs. The cosmetics segment has established a strong presence in premium beauty and personal care products, where cosmetic glass packaging adds a luxurious appeal and maintains product integrity. Glass containers in this segment are particularly valued for their ability to preserve sensitive formulations and enhance brand positioning. The other end-user industries segment, which includes pharmaceuticals and specialty chemicals, relies on pharmaceutical glass packaging for its chemical stability and protective properties. These segments continue to evolve with increasing emphasis on sustainable packaging solutions and innovative design approaches to meet specific industry requirements and changing consumer preferences.

Segment Analysis: By Color

Flint Segment in UK Glass Bottles and Containers Market

The flint glass market segment dominates the UK glass bottles and containers market, commanding approximately 63% market share in 2024. The segment's prominence is driven by the increasing utilization of transparent packaging for food items such as wine, milk, beer, and juice, as consumers prefer to inspect products before purchase. Flint glass bottles are particularly favored in the wine industry, especially for rosé and white wines, where highlighting the product's color and improving overall aesthetics is crucial. The segment's growth is further supported by technological advancements in glass manufacturing, with companies like Beatson Clark incorporating up to 45% recycled material in their production processes. While there are stricter quality requirements for white or flint glass compared to other colors, with a maximum recycled glass content of 60% due to contamination risks, manufacturers are continuously innovating to maintain product quality while meeting sustainability goals.

Remaining Segments in Glass Bottles and Containers Market by Color

The amber and green segments play vital complementary roles in the UK glass bottles and containers market. Amber glass is particularly valued in the pharmaceutical and beer industries due to its superior UV protection properties, capable of absorbing the broadest range of light waves across the spectrum. This makes it ideal for protecting light-sensitive products and preventing beer from developing unpleasant tastes due to photooxidation. Green glass bottles, while offering less UV protection than amber, are widely used in the beer industry, especially by European breweries, for their aesthetic appeal and brand differentiation. Both colors support the industry's sustainability initiatives, with amber glass being infinitely recyclable without quality loss and green glass bottles capable of incorporating high percentages of recycled content, contributing to the circular economy goals of the packaging industry.

United Kingdom (UK) Glass Bottles and Containers Market Overview

Top Companies in UK Glass Bottles and Containers Market

The UK glass bottle manufacturers market features several prominent players, including Verallia Packaging, Ciner Glass, O-I Glass, Ardagh Group, and Beatson Clark, among others. These companies are driving market evolution through a sustained focus on product innovation, particularly in developing lightweight and sustainable glass packaging solutions. Strategic investments in new furnace technologies and manufacturing facilities demonstrate the industry's commitment to operational excellence and environmental sustainability. Companies are actively pursuing expansion through both organic growth and acquisitions, with a notable trend toward enhancing premium packaging capabilities, especially in the spirits segment. The market is characterized by continuous technological advancement in areas such as automated inspection systems, decorative techniques, and eco-friendly production methods, while companies are increasingly emphasizing circular economy principles through improved recycling infrastructure and processes.

Consolidated Market with Strong Local Presence

The UK glass container manufacturers market exhibits a relatively consolidated structure dominated by both global conglomerates and established local specialists. Global players like O-I Glass and Ardagh Group leverage their international expertise and extensive resource networks, while local manufacturers such as Beatson Clark maintain strong regional positions through specialized product offerings and deep customer relationships. The market has witnessed significant merger and acquisition activity, exemplified by strategic moves such as Verallia's acquisition of Allied Glass and TricorBraun's purchase of Continental Bottles, indicating a trend toward market consolidation.

The competitive dynamics are shaped by a mix of long-established manufacturers with historical presence and newer entrants bringing fresh perspectives and technologies. Companies are increasingly focusing on vertical integration and strategic partnerships across the value chain to strengthen their market positions. The industry structure promotes healthy competition while maintaining barriers to entry through high capital requirements and technical expertise needed for quality glass container production, leading to a stable competitive environment where successful players combine manufacturing excellence with customer-centric innovation.

Innovation and Sustainability Drive Future Success

Success in the UK glass packaging market increasingly depends on companies' ability to balance sustainability initiatives with operational efficiency and customer responsiveness. Incumbent players must focus on developing proprietary technologies for reduced carbon emissions, enhanced recycling capabilities, and improved production efficiency to maintain their market positions. The ability to offer customized glass packaging solutions while maintaining scale economies, combined with strong relationships across the beverage, food, and cosmetics sectors, has become crucial for market leadership.

New entrants and challenger brands can gain ground by focusing on niche segments and innovative packaging solutions, particularly in premium categories where brand differentiation is crucial. The industry faces moderate substitution pressure from alternative packaging materials, making it essential for companies to emphasize glass's unique benefits in terms of sustainability, product preservation, and premium positioning. Future success will increasingly depend on companies' ability to navigate evolving regulatory requirements, particularly regarding carbon emissions and recycling targets, while maintaining cost competitiveness and meeting changing customer preferences for sustainable packaging solutions.

United Kingdom (UK) Glass Bottles and Containers Market Leaders

-

Verallia Packaging (Verallia SA)

-

Ciner Glass Ltd

-

O-I Glass Inc.

-

Ardagh Group SA

-

Glassworks International

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

United Kingdom (UK) Glass Bottles and Containers Market News

- January 2023 - Absolut entered into a partnership agreement with Ardagh Group in Limmared to deploy a partially hydrogen-fired furnace beginning in the second half of 2023. This collaboration will accelerate a global shift towards a more sustainable glassmaking process. In Limmared, Ardagh will initiate a pilot project in which 20% of natural gas will be replaced by green hydrogen to produce all Absolut bottles across its portfolio.

- December 2022 - Encirc, an international player in the glass manufacturing industry, announced a partnership with Diageo to develop the world's first net-zero glass bottles on a large-scale basis by 2030. The partnership, which is part of the Vidrala group, will involve the construction of a hydrogen-powered furnace at the company's Elton plant in Cheshire. The furnace is expected to be operational in 2027 and will produce 200 million net-zero Smirnoff, Captain Morgans, Gordon's, and Tanqueray annually.

United Kingdom (UK) Glass Bottles and Containers Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Eco-system Analysis With an Emphasis on Circular Economy

- 4.4 Container Glass - Industry Landscape

- 4.5 Russia-Ukraine Conflict - Impact on the Market Eco-System

- 4.6 Import and Export Analysis

- 4.7 Cost Analysis With Key Drivers (Components and Energy Consumption)

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increased Demand for Glass Packaging in Beverage Industry

- 5.1.2 Recyclability Benefits Offered by Glass Packaging Drive Sustainability

-

5.2 Market Challenges

- 5.2.1 Alternative Packaging Options Challenging the Market Growth

- 5.3 Analysis of the Increasing Emphasis on Glass Recycling and the Current Recyclability Rate in the United Kingdom

- 5.4 Comparative Analysis of Collection and Recycling of Container Glass in the United Kingdom as Opposed to the European Market

- 5.5 Analysis of the Overall Glass Manufacturing Industry in the United Kingdom

- 5.6 Regulatory Framework

- 5.7 Demand for Glass Containers and Bottles - Retail and Foodservice Industries

- 5.8 Consumer Trends and Preference for Glass Packaging

- 5.9 Industry Standards - Bottle Sizes and Shapes

- 5.10 United Kingdom Glass Production Analysis

6. MARKET SEGMENTATION

-

6.1 By End-user Industry

- 6.1.1 Beverages

- 6.1.1.1 Alcoholic

- 6.1.1.1.1 Beer and Cider

- 6.1.1.1.2 Wine and Spirits

- 6.1.1.1.3 Other Alcoholic Beverages

- 6.1.1.2 Non-alcoholic

- 6.1.1.2.1 Carbonated Soft Drinks

- 6.1.1.2.2 Milk

- 6.1.1.2.3 Water and Other Non-alcoholic Beverages

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Other End-user Industries

-

6.2 By Color

- 6.2.1 Amber

- 6.2.2 Flint

- 6.2.3 Green

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Verallia Packaging (Verallia SA)

- 7.1.2 Ciner Glass Ltd

- 7.1.3 O-I Glass Inc.

- 7.1.4 Ardagh Group SA

- 7.1.5 Glassworks International

- 7.1.6 Gaasch Packaging

- 7.1.7 Berlin Packaging

- 7.1.8 Vidrala SA

- 7.1.9 Beatson Clark

- 7.1.10 Stoelzle Flaconnage

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

United Kingdom (UK) Glass Bottles and Containers Market Industry Segmentation

Glass has been one of the primary packaging materials used for multiple packaging drug and biological formulations. The unique combination of hermeticity, transparency, strength, and chemical durability makes glass the optimal material for such purposes.

The United Kingdom glass bottles and containers market is segmented by end-user industry (beverages (alcoholic (beer and cider, wine and spirits), non-alcoholic (carbonated soft drinks, milk, water)), food, cosmetics), color (amber, flint, green). The market sizes and forecasts are provided in terms of consumption volume (Tonnes) for all the above segments.

| By End-user Industry | Beverages | Alcoholic | Beer and Cider | |

| Wine and Spirits | ||||

| Other Alcoholic Beverages | ||||

| Non-alcoholic | Carbonated Soft Drinks | |||

| Milk | ||||

| Water and Other Non-alcoholic Beverages | ||||

| Food | ||||

| Cosmetics | ||||

| Other End-user Industries | ||||

| By Color | Amber | |||

| Flint | ||||

| Green | ||||

Need A Different Region or Segment?

Customize Now

United Kingdom (UK) Glass Bottles and Containers Market Research FAQs

How big is the UK Glass Bottles And Containers Market?

The UK Glass Bottles And Containers Market size is expected to reach 2.35 million tonnes in 2025 and grow at a CAGR of 2.94% to reach 2.71 million tonnes by 2030.

What is the current UK Glass Bottles And Containers Market size?

In 2025, the UK Glass Bottles And Containers Market size is expected to reach 2.35 million tonnes.

Who are the key players in UK Glass Bottles And Containers Market?

Verallia Packaging (Verallia SA), Ciner Glass Ltd, O-I Glass Inc., Ardagh Group SA and Glassworks International are the major companies operating in the UK Glass Bottles And Containers Market.

What years does this UK Glass Bottles And Containers Market cover, and what was the market size in 2024?

In 2024, the UK Glass Bottles And Containers Market size was estimated at 2.28 million tonnes. The report covers the UK Glass Bottles And Containers Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the UK Glass Bottles And Containers Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

United Kingdom (UK) Glass Bottles and Containers Market Research

Mordor Intelligence provides comprehensive industry analysis and market outlook for the glass bottles and containers market in the United Kingdom. Our research covers detailed market segmentation, industry statistics, and growth forecasts for various segments including glass packaging, glass container, and glass bottle manufacturing sectors. The report examines market leaders, emerging trends, and competitive dynamics across applications such as beverages, pharmaceuticals, and cosmetics. All these valuable insights are available in an easy-to-read report PDF format, enabling stakeholders to make informed decisions based on reliable market data and industry trends.

Our consulting expertise extends beyond traditional market research to provide strategic solutions for the glass container manufacturers UK and associated stakeholders. We offer comprehensive value chain analysis, regulatory assessment specific to glass packaging solutions, and technology scouting for innovative manufacturing processes. Our team conducts detailed B2B surveys with glass bottle suppliers UK and end-users, providing insights into customer needs and behavior analysis. We assist clients with product pricing and positioning assessment, particularly for specialized segments like pharmaceutical glass packaging and cosmetic glass packaging. Additionally, we support businesses in identifying and evaluating potential partners, suppliers, and distributors within the glass bottle industry, ensuring sustainable growth and market expansion.