Market Size of UK Facility Management Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Market Size (2024) | USD 69.28 Billion |

| Market Size (2029) | USD 75.19 Billion |

| CAGR (2024 - 2029) | 1.65 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

UK Facility Management Market Analysis

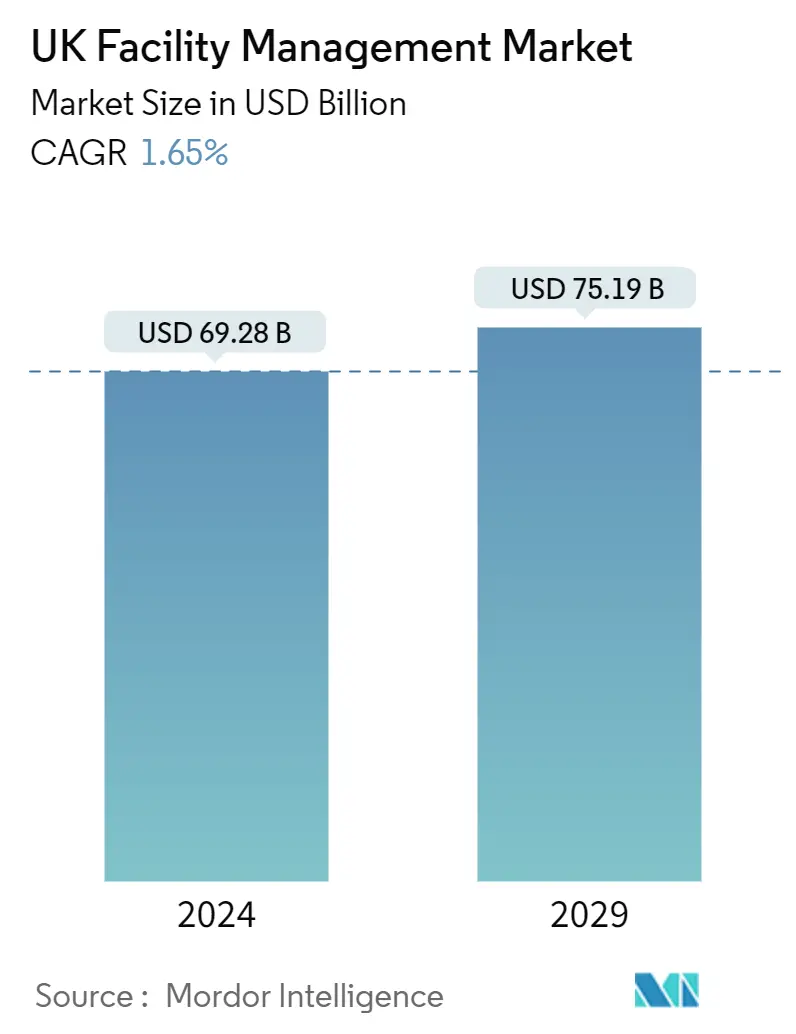

The UK Facility Management Market size is estimated at USD 69.28 billion in 2024, and is expected to reach USD 75.19 billion by 2029, growing at a CAGR of 1.65% during the forecast period (2024-2029).

- In terms of maturity and sophistication, the United Kingdom is one of Europe's most mature and sophisticated markets for facility management services. Given the increasing penetration of facility management services, providers are actively focusing on specialized services to obtain a foothold in the industry, which also saw many changes due to the region's macroeconomic and social changes.

- Various service providers operating in the country have emphasized growing their presence over the last decade to benefit from the increasing demand for facility management, especially with the current trend favoring outsourcing non-core functions. Given the dynamics across the country, the country is witnessing increased opportunities to leverage facility management and corporate real estate in innovative ways. According to BNP Paribas Real Estate, in 2023, the United Kingdom headed the ranking as the country with the most significant value of commercial real estate investments, amounting to about EUR 43.5 billion.

- The government is also focusing on closing the country's productivity gap for small to medium enterprises. For instance, in the recent past, the British government pledged EUR 56 million to enhance leadership and management skills. The funding also forms part of the Business Productivity Review announced by the Department for Business, Energy, and Industrial Strategy (BEIS) and Strategy, which sets out a 10-point action plan to help UK companies harness technology and boost productivity, thereby driving the market growth.

- Also, the facility management industry is expected to expand due to consumers' shifting preferences toward outsourced facility management services to cut costs. Businesses may save significantly by outsourcing building operations and maintenance while concentrating on their core competencies. Research by the Building Owners & Managers Association (BOMA) found that, on average, private commercial properties spend USD 2.15 on maintenance and repairs per square foot. Expenditures associated with maintaining the facility, such as labor costs for cleaning and upkeep, are not included in this amount. Businesses can save expenses and leverage the time saved by outsourcing to better use their workers in their core operations.

- Moreover, various market vendors are expanding their business operations through multiple contracts. For instance, in January 2023, Sodexo announced that it won a five-year contract to offer integrated facilities management (IFM) for a global bank's London offices. As part of the GBP 2 million-a-year contract, Sodexo would deliver services that connect with employees and make their working environment as engaging as possible. The services include catering, hospitality, cleaning, technical services, reception and guest services, and the management of the in-house gym.

- In September 2023, Apleona, a significant European integrated facilities management company based in Neu-Isenburg near Frankfurt (Main), acquired JCW Group Limited (JCW). The two companies will form a robust platform for integrated facilities management. Their complementary enterprise models, regional footprints, and client portfolios will secure strong organic growth with existing and recent Apleona clients in the United Kingdom and Europe.

- The growing competition in the market impacts the profit margins and growth of existing vendors. The competition level between suppliers is so high that FM services are transitioning to commoditized in the country. However, the country's recovering economic stability is anticipated to improve the market demand gradually and, subsequently, the profit margins of the market players. As suggested by the UK Facilities Management Market Survey by RICS, the profit margins, workloads, and employment opportunities are anticipated to grow over the next couple of years.

- Increasing inflation can affect the growth of the United Kingdom facility management market in several ways. If inflation leads to higher costs for inputs such as labor, materials, and equipment, facility management companies may face increased operating expenses, potentially squeezing profit margins unless they can pass these costs onto clients through higher prices. According to the Office for National Statistics (UK), the UK inflation rate was 3.2% in March 2024, compared with 3.4% in the previous month. Between September 2022 and March 2023, the United Kingdom experienced seven months of double-digit inflation, which peaked at 11.1% in October 2022.

UK Facility Management Indsutry Segmentation

Facility management is an organizational function that integrates people, places, and processes within the built environment to improve people's quality of life and the productivity of the core business.

The UK facility management market is segmented by facility management type (in-house FM service, outsourced FM service (single FM, bundled FM, and integrated FM)), offering type (hard FM (building O&M and property services, mechanical, electrical, and plumbing services, other hard FM services (including energy services)), and soft FM (safety and security services, office support services, janitorial services, catering services, other soft FM services)), and end users (commercial, institutional, public/infrastructure, industrial, and other end users), and region (London and South East England, South West England, Midlands & East England, North of England, and Rest of the United Kingdom). The market sizes and forecasts are in terms of value USD for all the above segments.

| By Facility Management Type | |||||

| In-House Facility Management | |||||

|

| By Offering Type | |||||||

| |||||||

|

| By End-user Industry | |

| Commercial | |

| Institutional | |

| Public/Infrastructure | |

| Industrial | |

| Other End-user Industries |

| By Region | |

| London and South East England | |

| South West England | |

| Midlands and East England | |

| North of England | |

| Rest of the United Kingdom |

UK Facility Management Market Size Summary

The UK facility management market is characterized by its maturity and sophistication, positioning it as one of the leading markets in Europe. The sector is experiencing a shift towards specialized services as providers seek to capitalize on the growing demand for outsourced non-core functions. This trend is driven by macroeconomic and social changes, as well as the increasing emphasis on leveraging facility management and corporate real estate in innovative ways. The government's initiatives to enhance productivity, particularly among small to medium enterprises, further support the market's expansion. The focus on sustainable building practices and lifecycle management in the construction sector also contributes to the rising demand for facility management services, which are essential for managing complex building systems and ensuring operational efficiency.

The market is highly competitive and fragmented, with numerous players engaging in strategic partnerships, acquisitions, and mergers to strengthen their positions. The commercial segment, in particular, is witnessing significant growth as businesses prioritize operational efficiency, occupant satisfaction, and risk management. Facility management services are crucial for maintaining the complex infrastructure of commercial buildings, thereby minimizing downtime and enhancing business operations. The increasing interest in smart buildings and IoT technologies presents additional opportunities for market vendors to innovate and expand their service offerings. Despite challenges such as inflation and rising operational costs, the market is poised for gradual growth, driven by the recovery of economic stability and the ongoing demand for integrated facility management solutions.

UK Facility Management Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Assessment of the Impact of Macroeconomic Factors on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Facility Management Type

-

2.1.1 In-House Facility Management

-

2.1.2 Outsourced Facility Management

-

2.1.2.1 Single FM

-

2.1.2.2 Bundled FM

-

2.1.2.3 Integrated FM

-

-

-

2.2 By Offering Type

-

2.2.1 Hard FM

-

2.2.1.1 Building O&M and Property Services

-

2.2.1.2 Mechanical, Electrical, and Plumbing Services

-

2.2.1.3 Other Hard FM Services (includes Energy Services)

-

-

2.2.2 Soft FM

-

2.2.2.1 Safety and Security Services

-

2.2.2.2 Office Support Services

-

2.2.2.3 Janitorial Services

-

2.2.2.4 Catering Services

-

2.2.2.5 Other Soft FM Services

-

-

-

2.3 By End-user Industry

-

2.3.1 Commercial

-

2.3.2 Institutional

-

2.3.3 Public/Infrastructure

-

2.3.4 Industrial

-

2.3.5 Other End-user Industries

-

-

2.4 By Region

-

2.4.1 London and South East England

-

2.4.2 South West England

-

2.4.3 Midlands and East England

-

2.4.4 North of England

-

2.4.5 Rest of the United Kingdom

-

-

UK Facility Management Market Size FAQs

How big is the UK Facility Management Market?

The UK Facility Management Market size is expected to reach USD 69.28 billion in 2024 and grow at a CAGR of 1.65% to reach USD 75.19 billion by 2029.

What is the current UK Facility Management Market size?

In 2024, the UK Facility Management Market size is expected to reach USD 69.28 billion.