Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

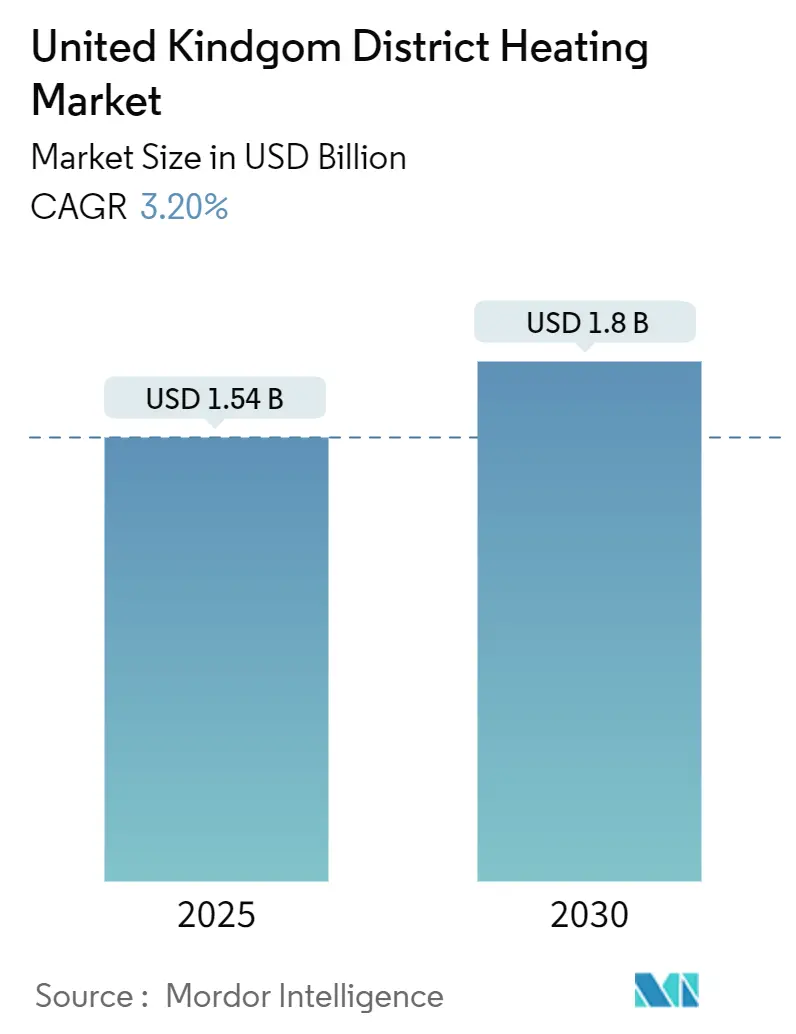

| Market Size (2025) | USD 1.54 Billion |

| Market Size (2030) | USD 1.8 Billion |

| Growth Rate (2025 - 2030) | 3.20% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom District Heating Market Analysis by Mordor Intelligence

The UK district heating market size stood at USD 1.54 billion in 2025 and is forecast to expand at a 3.20% CAGR to reach USD 1.8 billion by 2030.[1]Department for Energy Security and Net Zero, “Heat network zone opportunity reports,” GOV.UK, gov.uk This measured trajectory reflects the systemwide pivot from gas-dominant assets toward low-carbon heat pumps, waste-heat recovery, and large-scale thermal storage. Mandatory heat-network zoning is creating legally enforceable connection areas that de-risk customer acquisition, while the Green Heat Network Fund reduces capital outlay for projects integrating energy-from-waste heat or renewable electricity. Government grants now prioritize schemes delivering verifiable carbon cuts, prompting operators to blend river, mine-water, and wastewater heat with networked ground-source heat pumps. Investors are responding to these policy signals: institutional capital has intensified asset roll-ups that pool fragmented networks under professional management, accelerating technology upgrades such as 12-hour storage pits. Supply-chain constraints in skilled labour and metal commodities remain headwinds, yet Ofgem’s incoming consumer-protection regime is expected to strengthen end-user confidence and encourage higher connection rates.

Key Report Takeaways

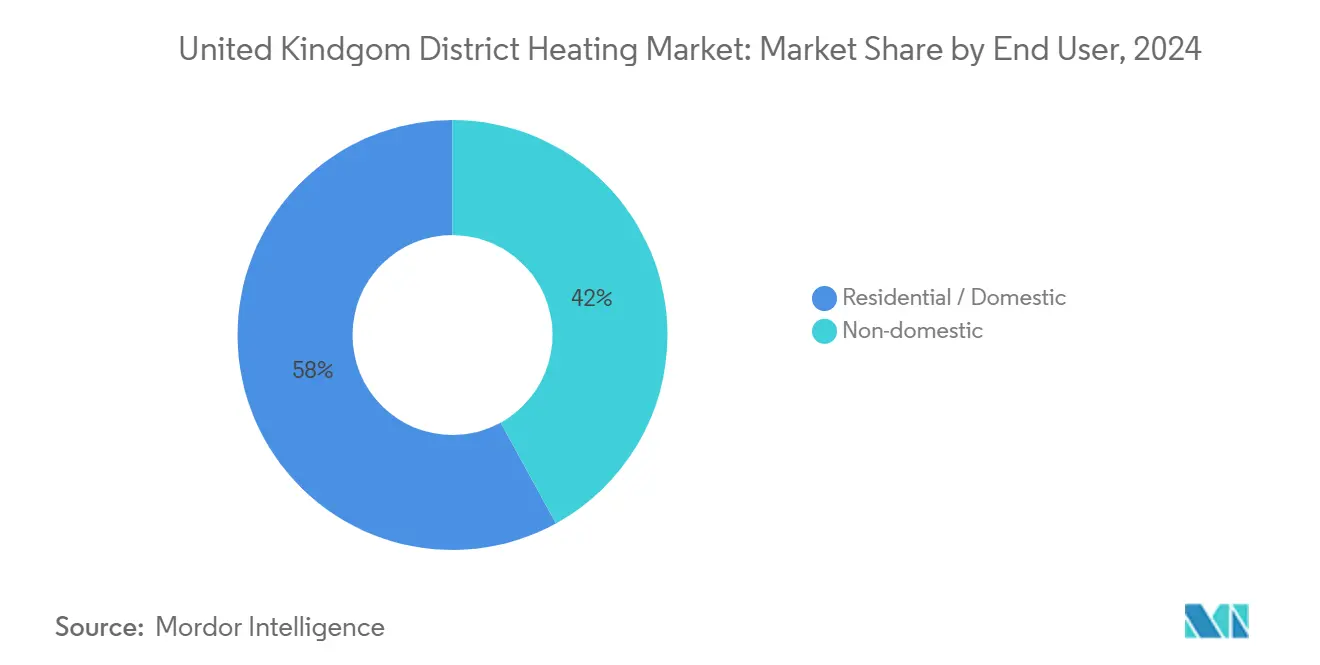

- By end user, residential consumers led with 58.0% of UK district heating market share in 2024, whereas non-domestic applications are projected to register a 4.53% CAGR through 2030.[2]Association for Decentralised Energy, “£34m awarded brings total GHNF investment to over £380m, boosting low carbon heat networks across England,” THEADE.CO.UK, theade.co.uk

- By primary heat source, gas-CHP systems commanded 71.5% of UK district heating market size in 2024, yet low-carbon heat pumps and waste-heat recovery are advancing at a 5.22% CAGR.

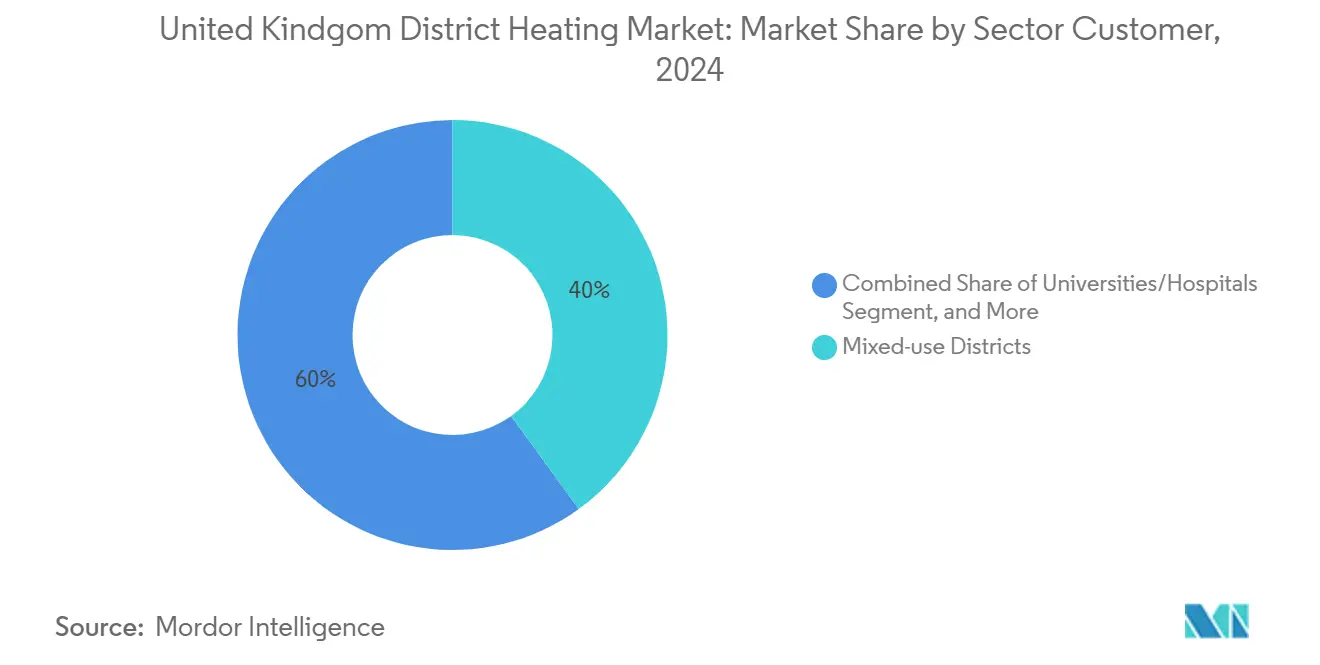

- By sector, mixed-use regeneration districts captured 40.0% of UK district heating market share in 2024, while universities and hospitals represent the fastest-growing customer group at 5.06% CAGR.

- By thermal-storage usage, networks equipped with ≥12 h storage are expanding at a 5.84% CAGR, highlighting the revenue potential from grid-balancing services.

United Kingdom District Heating Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Statutory heat-network zoning from 2025-26 | +1.20% | England, with pilot coverage across 28 local authorities | Medium term (2-4 years) |

| Green Heat Network Fund and HNES grants | +0.80% | England and Scotland | Short term (≤ 2 years) |

| Waste-heat capture mandate (EfW and sewage) | +0.60% | National, concentrated in urban centers | Medium term (2-4 years) |

| Falling cost of river/mine-water heat pumps | +0.40% | Scotland and Northern England mining regions | Long term (≥ 4 years) |

| Mandatory landlord tariff disclosure | +0.20% | National | Short term (≤ 2 years) |

| Aggregation of thermal storage into ESO flexibility | +0.30% | National grid balancing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Statutory heat-network zoning from 2025-26

Heat-network zoning gives local authorities legal power to mandate customer connections within defined boundaries, securing the heat density essential for commercial viability. The Department for Energy Security and Net Zero released opportunity reports for 16 areas, guiding Birmingham, Leeds, and Newcastle to map mandatory zones that cover new builds and many retrofit sites. Zoning transforms district heating from an optional technology into a compliance obligation, lowering demand risk for operators and offering predictable revenue streams attractive to long-term investors. Developers gain clarity on network sizing and phased expansion, while existing building owners face clear deadlines to decarbonize. The policy, therefore, shifts market power toward network owners capable of rapid capital deployment and proven operational competence.

Green Heat Network Fund and HNES grants

The Green Heat Network Fund has disbursed more than GBP 380 million (USD 475 million) since launch, including GBP 19.5 million for Leeds’s Aire Valley Heat and Power Network and GBP 7.2 million for the University of London’s Bloomsbury Energy Network. Grants reduce the weighted average cost of capital, unlock large energy-from-waste heat sources, and improve internal rates of return by up to 2 percentage points. Award criteria reward projects that combine waste-heat capture with heat pumps, pushing market design toward hybrid configurations that can meet sub-50 gCO2/kWh targets. Funding certainty has also catalysed private lenders; several commercial banks now accept GHNF awards as de-risking instruments when structuring senior debt.

Waste-heat capture mandate (EfW and sewage)

National planning policy now requires large energy-from-waste plants and wastewater facilities to make residual heat available to third-party networks. Cardiff’s GBP 15.5 million scheme captures steam from Viridor’s Energy Recovery Facility, delivering heat to the Senedd and Millennium Centre with forecast savings of 10,000 tCO2 annually.[3]Cardiff Council, “Low-carbon district heat network in Cardiff nears completion,” CARDIFFNEWSROOM.CO.UK, cardiffnewsroom.co.uk Similar mandates have encouraged SSE Energy Solutions and Scottish Water Horizons to target heat-from-wastewater projects, beginning with Inverness. These policies monetize previously wasted thermal energy, diversify operator income, and amplify carbon reductions beyond electricity generation.

Falling cost of river and mine-water heat pumps

University of Strathclyde research confirms that abandoned mines offer stable 12-15 °C water ideal for inter-seasonal storage, while river-source systems benefit from lower drilling costs.[4]Scottish Enterprise, “Unlocking the Economic Potential of Minewater Geothermal in Scotland,” SCOTTISH-ENTERPRISE.COM, scottish-enterprise.com The Gateshead Mine Water Heat Network uses a 6 MW heat pump producing heat at roughly 45 GBP/MWh, highly competitive against gas-fired systems. Capital costs continue to decline through modular skid packages and standardized heat-exchanger arrays, making subsurface resources increasingly attractive for networks seeking renewable baseload.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High front-end capex | -0.90% | National | Medium term (2-4 years) |

| Gas-power price-spread volatility | -0.40% | National | Short term (≤ 2 years) |

| Skilled-labour shortage (pipe-welders/HIU) | -0.60% | National, acute in London and Southeast | Medium term (2-4 years) |

| Consumer "monopoly billing" perception | -0.30% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High front-end capex

Material inflation lifted insulation prices by 2-11.7% during 2024-2025, while copper and steel volatility added further strain to balance sheets. Arup estimates geothermal networks cost GBP 2–4 million per MWth, with drilling alone accounting for up to 45% of expenditure. The capital intensity lengthens payback horizons and limits bankability for smaller developers. GHNF grants soften but do not eliminate the risk of sunk costs during feasibility and permitting. Equity investors, therefore, demand higher internal returns, slowing financial close for projects without anchor loads or long-term heat-offtake agreements.

Gas-power price-spread volatility

District heating margins rely on predictable spark-spread relationships between retail gas and electricity. Sudden wholesale swings increase the cost of electrically driven heat pumps relative to gas-CHP, complicating dispatch optimization. Although long-term power-purchase agreements can hedge exposure, few smaller schemes have the credit profile to secure fixed-price electricity beyond three years, preserving uncertainty that dampens investment appetite.

Segment Analysis

By End User: Residential Dominance Faces Non-Domestic Acceleration

Residential connections delivered 58.0% of UK district heating market share in 2024, benefiting from higher heat density in urban housing estates and mixed-use regeneration schemes. Social housing pilots underline the value proposition: the SHIELD trial indicates potential bill cuts of 40% for low-income tenants while meeting landlord retrofit obligations. Non-domestic demand is gaining momentum at 4.53% CAGR, driven by ESG imperatives and public-sector net-zero targets. Universities and hospitals, armed with capital grants and long asset-life planning horizons, now underwrite multi-megawatt expansions that lock in baseload demand.

Commercial property owners increasingly view heat networks as a hedge against future building-emissions taxes. Mandatory disclosure of operational carbon in leasing contracts pushes landlords toward networks that guarantee low-carbon coefficients. Meanwhile, local authorities bundle residential and municipal loads to unlock economies of scale, further widening the addressable base. The resulting blended customer mix stabilizes cash flows, positioning schemes for refinancing in private debt markets, and supporting the UK district heating market growth trajectory.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Primary Heat Source: Gas-CHP Transition Toward Heat Pumps

Gas-fired CHP retained 71.5% of UK district heating market size in 2024, though its dominance is eroding as carbon pricing and biomass-sustainability rules tighten. Low-carbon heat pumps and waste-heat systems expand at 5.22% CAGR, reflecting their eligibility for higher GHNF scoring and lower lifecycle emissions. The MEL Heat Network captures waste heat from the Millerhill Energy-from-Waste facility and boosts it with large heat pumps to serve Shawfair Town; Vattenfall calculates the hybrid system will avoid up to 90% of baseline emissions.

Ground-source configurations gain scale through networked arrays that share vertical boreholes across housing clusters, cutting per-dwelling drill costs by one-third. Air-source units increasingly act as summer top-up rather than sole supply, optimizing seasonal performance. Biomass remains niche in urban areas due to particulate limits, though rural estates still exploit local feedstock. Backup gas boilers persist for resilience, yet their runtime falls as storage and demand response improve.

By Sector and Customer: Mixed-Use Districts Lead University Growth

Mixed-use regeneration districts accounted for 40.0% of the UK district heating market share in 2024, reflecting planning frameworks that embed heat-network corridors at the concept stage. These schemes benefit from shared trenches, unified metering, and integrated electrical substations, lowering capex per connection. Universities and hospitals, forecast to grow at a 5.06% CAGR, use district heating to attain Scope 1 decarbonization targets while securing a reliable baseload for high-temperature sterilization or research labs.

Public and social housing projects leverage the Social Housing Decarbonisation Fund to subsidize connection fees, accelerating uptake among fuel-poor tenants. Commercial and retail parks still face tougher economics given lower load factor, but value propositions improve when thermal storage enables participation in demand-side flexibility markets. Forward-thinking councils now bundle retail parks into larger concessions that mix premium and subsidized customers, smoothing revenue and enhancing creditworthiness for private-finance initiatives. These strategic combinations underpin the resilience of the UK district heating market against macro-economic shocks.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Thermal-Storage Usage: Storage Integration Drives Flexibility Value

Networks without integrated storage represented 82.0% of installed capacity in 2024, a legacy of historically narrow focus on heat provision alone. However, systems equipped with ≥12 h pit or tank storage are scaling at 5.84% CAGR, monetizing electricity-market arbitrage and ESO flexibility payments. Storage allows operators to decouple heat generation from immediate demand, enabling off-peak electricity for heat-pump operation and thereby cutting marginal energy cost.

Short-duration (2 h) buffer tanks still dominate retrofit projects where space constraints forbid large pits, yet their market share will wane as urban planning allocates subterranean or brownfield plots for seasonal storage installations. Digital twins now optimize charge-discharge profiles at five-minute granularity, raising round-trip efficiency above 80% and maximizing income stacking. Aggregators bundle multiple storage-enabled networks into virtual power plants, signalling a long-term shift toward heat-electricity sector coupling that strengthens the value proposition of the UK district heating market.

Geography Analysis

England remains the epicentre of development thanks to GHNF funding and statutory zoning, with Leeds, Birmingham, and London leading rollouts that integrate waste-heat from EfW plants into urban grids. Scotland follows closely under the Heat Networks (Scotland) Act 2021, which targets 6 TWh of heat by 2030 and finances innovative use of mine-water and geothermal resources. Wales enters a formative growth phase: Cardiff’s newly commissioned network validates the cost-benefit of EfW heat capture, prompting other Welsh councils to consider similar models. Northern Ireland is still atthe pilot stage, using GeoenergyNI research to map subsurface heat potential and assess regulatory pathways.

Urban cores offer the highest connection density, with London’s Bloomsbury Energy Network retrofitting 80-year-old boilers in academic buildings. Industrial cities such as Leeds deploy the Aire Valley Heat and Power Network to serve manufacturing clusters and adjacent residential blocks. Coastal hubs eye seawater source heat pumps, though salinity corrosion control and planning permissions require further study. Local zoning decisions begin to cluster rollouts, creating contiguous heat-network corridors that attract private capital seeking scale.

Scotland’s geology provides unique opportunities. The Gateshead Mine Water scheme, although located in England, proves the concept for Scottish projects examining similar abandoned workings. Scottish Water and SSE plan to harvest wastewater heat across the Highlands and Lowlands, starting with Inverness, while the Dumfries Basin Aquifer underpins a campus-scale project at Crichton. These examples demonstrate how localized resource advantages can shape network architecture, diversify the supply mix and support the broader UK district heating market trajectory.

Competitive Landscape

Top Companies in UK District Heating Market

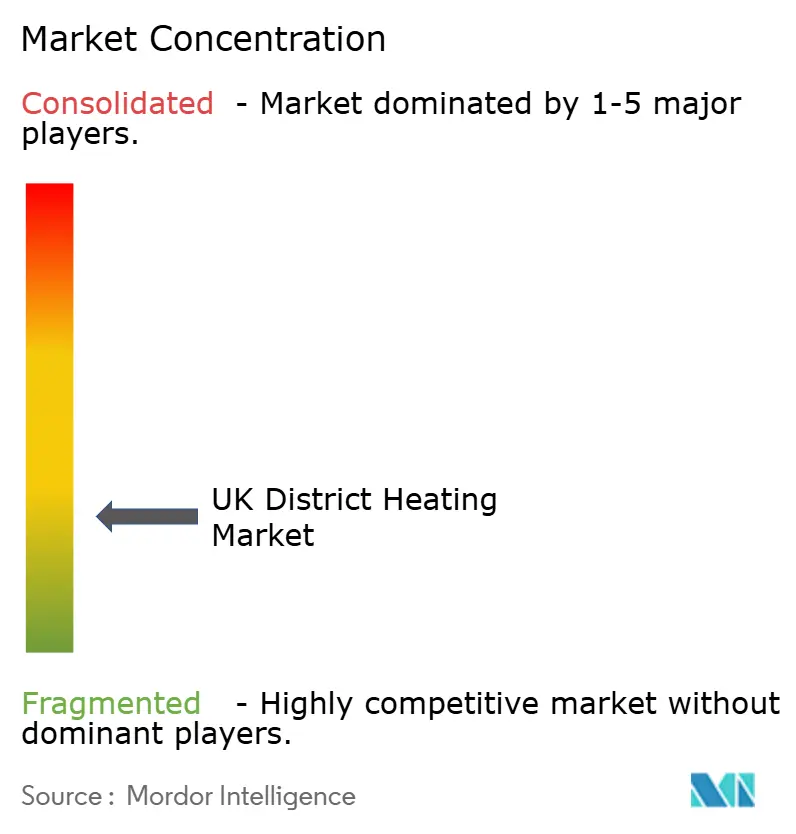

The competitive arena features a blend of multinational utilities, infrastructure funds, and specialized technology providers. Vital Energi, E.ON UK, and Vattenfall Heat UK collectively handled roughly 24% of connected load in 2024, illustrating moderate concentration. Institutional investors, exemplified by Swiss Life Asset Managers and Schroders Greencoat, have accelerated consolidation by purchasing Equans Urban Energy UK for GBP 260 million. The deal signals confidence in long-run regulated returns and hints at rising barriers to entry as Ofgem licensing becomes mandatory.

Strategic differentiation pivots on thermal storage integration, advanced digital control, and the ability to unlock new revenue streams from flexibility markets. Larger players leverage balance-sheet strength to pre-finance multi-year buildouts, capturing anchor loads before zoning expands. Mid-tier specialists such as Kensa Utilities focus on networked ground-source heat pumps for new-build dwellings, while ThamesWey Energy capitalizes on municipal concessions that bundle housing and civic buildings.

Competitive intensity is likely to escalate as smaller private equity-backed operators seek exits before full Ofgem regulation takes hold. Companies with proven consumer-protection systems will enjoy a regulatory premium, while laggards may face acquisition or attrition. Overall, the UK district heating market will increasingly resemble other regulated utilities, with scale, compliance competence and technology integration dictating competitive advantage.

United Kingdom District Heating Industry Leaders

-

Vital Energi Utilities Ltd

-

1 Energy Group Limited

-

Baxi Heating UK

-

Ramboll UK Limited

-

Veolia Environnement SA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Cardiff Council completed commissioning of its GBP 15.5 million district heat network, capturing waste heat from Viridor’s Energy Recovery Facility.

- March 2025: SSE Energy Solutions and Scottish Water Horizons formed a strategic partnership to develop low-carbon networks starting in Inverness.

- February 2025: The Department for Energy Security and Net Zero issued Heat Network Zone Opportunity Reports covering 28 local authorities.

- January 2025: SSE Energy Solutions signed an exclusive agreement with Stoke-on-Trent City Council for city-wide heat-network development.

United Kingdom District Heating Market Report Scope

District heating is the process of distributing heat in the form of hot water or steam through a network of insulated pipes from a centralized location to end users such as residential, commercial, or industrial.

The UK district heating Market is Segmented by end-user (residential/domestic and non-domestic).

The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By End User

| Residential / Domestic |

| Non-domestic |

By Primary Heat Source

| Gas-CHP |

| Low-carbon HP and Waste-heat |

| Biomass / Biogas |

| Other back-up (gas, electric) |

By Sector and Customer

| Mixed-use regeneration districts |

| Public and Social Housing |

| Universities and Hospitals |

| Commercial / Retail Parks |

By Thermal-Storage Usage

| No integrated storage |

| ≥2 h hot-water tanks |

| ≥12 h pit / tank storage |

| By End User | Residential / Domestic |

| Non-domestic | |

| By Primary Heat Source | Gas-CHP |

| Low-carbon HP and Waste-heat | |

| Biomass / Biogas | |

| Other back-up (gas, electric) | |

| By Sector and Customer | Mixed-use regeneration districts |

| Public and Social Housing | |

| Universities and Hospitals | |

| Commercial / Retail Parks | |

| By Thermal-Storage Usage | No integrated storage |

| ≥2 h hot-water tanks | |

| ≥12 h pit / tank storage |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the UK district heating market?

The market was valued at USD 1.54 billion in 2025 and is projected to reach USD 1.8 billion by 2030 at a 3.20% CAGR.

Which end-user segment leads demand for UK district heating?

Residential connections held 58.0% share in 2024, though non-domestic customers are growing faster due to ESG mandates.

How significant are heat pumps within UK district heating?

Low-carbon heat pumps and waste-heat systems are expanding at a 5.22% CAGR, gradually eroding gas-CHPs 71.5% share.

What role does thermal storage play in UK schemes?

Networks with ?12 h storage are increasing at 5.84% CAGR, earning extra revenue from electricity-system flexibility services.

How are government grants influencing project economics?

The Green Heat Network Fund has awarded over GBP 380 million, cutting capital costs and accelerating hybrid heat-network adoption.

Which regions are seeing the fastest growth in district heating?

England leads due to zoning and funding, while Scotland's mine-water and geothermal resources drive innovative deployments.

Page last updated on: