United Kingdom Data Center Construction Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

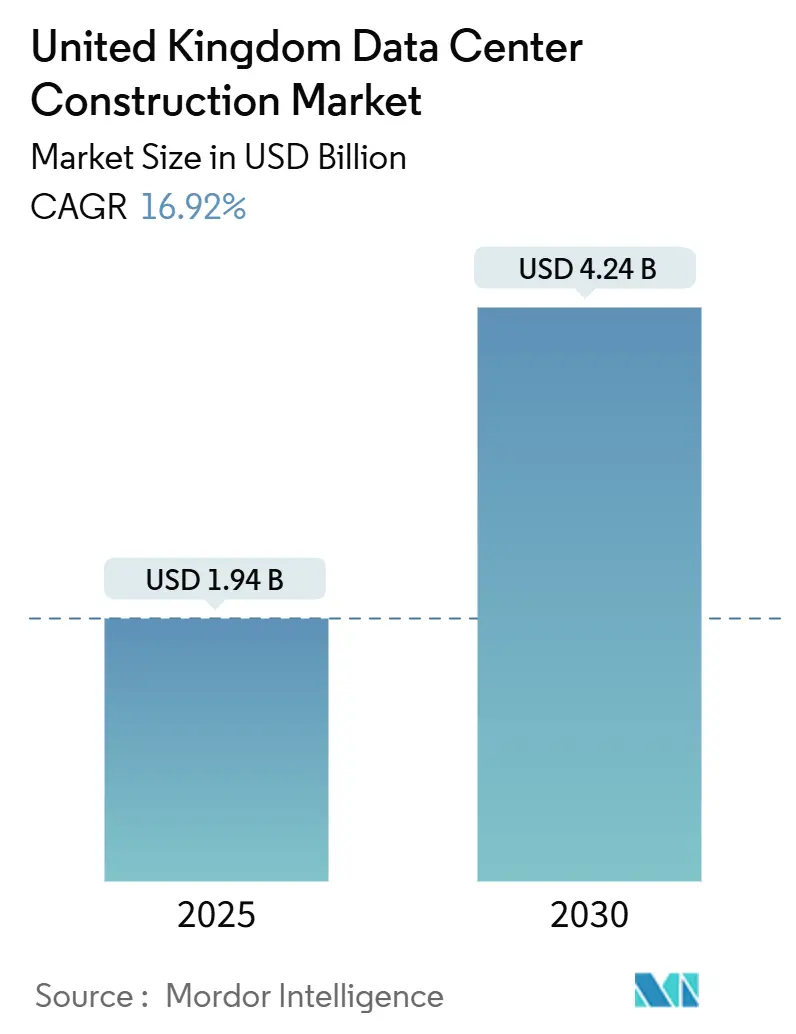

| Market Size (2025) | USD 1.94 Billion |

| Market Size (2030) | USD 4.24 Billion |

| Growth Rate (2025 - 2030) | 16.92% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Data Center Construction Market Analysis by Mordor Intelligence

The United Kingdom data center construction market reached USD 1.94 billion in 2025 and is forecast to expand to USD 4.24 billion by 2030, reflecting a 16.92% CAGR during the forecast period. Intensified government backing, hyperscaler capital commitments, and the official designation of data centers as Critical National Infrastructure are the primary growth engines. Demand for AI-ready capacity, rising 5G and planned 6G rollouts, and a national focus on digital sovereignty continue to shift design standards toward higher-tier, high-density facilities that demand advanced power and cooling solutions. Grid congestion around London is redirecting construction toward regions such as the Midlands and Northern England where capacity is still available. Meanwhile, on-site generation pilots and small modular reactor (SMR) concepts promise future resilience in power-hungry builds. Construction contractors with deep mechanical, electrical, and plumbing expertise and the ability to deliver in compressed timelines are best positioned to capture the largest projects.

Key Report Takeaways

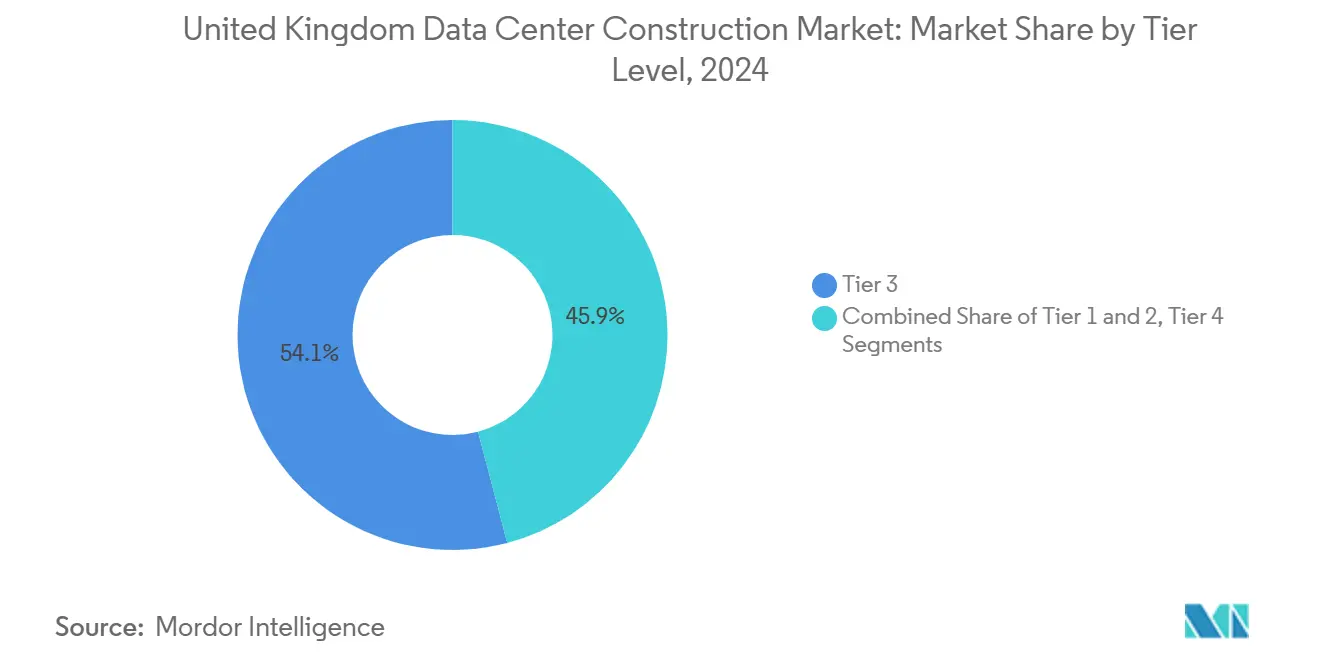

- By tier type, Tier 3 facilities held 54.1% of the United Kingdom data center construction market share in 2024, while Tier 4 is advancing at a 15.4% CAGR through 2030.

- By data center type, colocation captured 56.3% of the United Kingdom data center construction market in 2024; self-build hyperscaler sites are set to grow at a 16.2% CAGR to 2030.

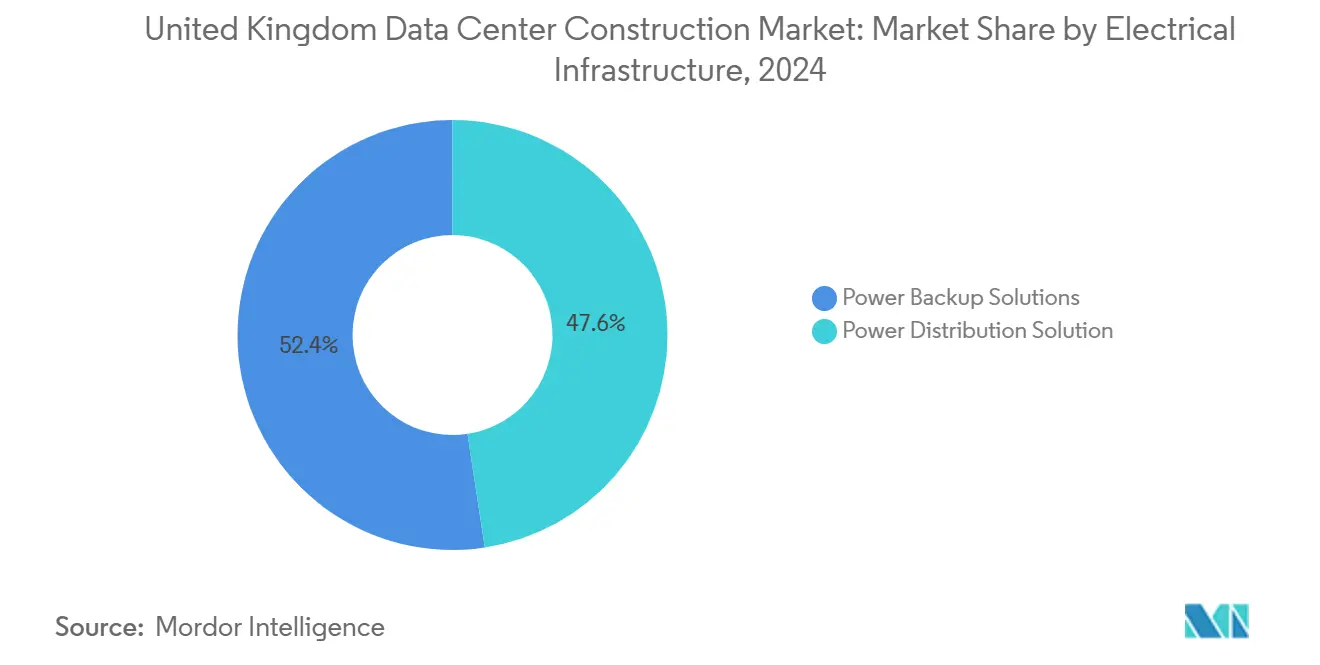

- By electrical infrastructure, power backup solutions accounted for 52.4% share of the United Kingdom data center construction market size in 2024, with power distribution systems expanding at a 15.7% CAGR through 2030.

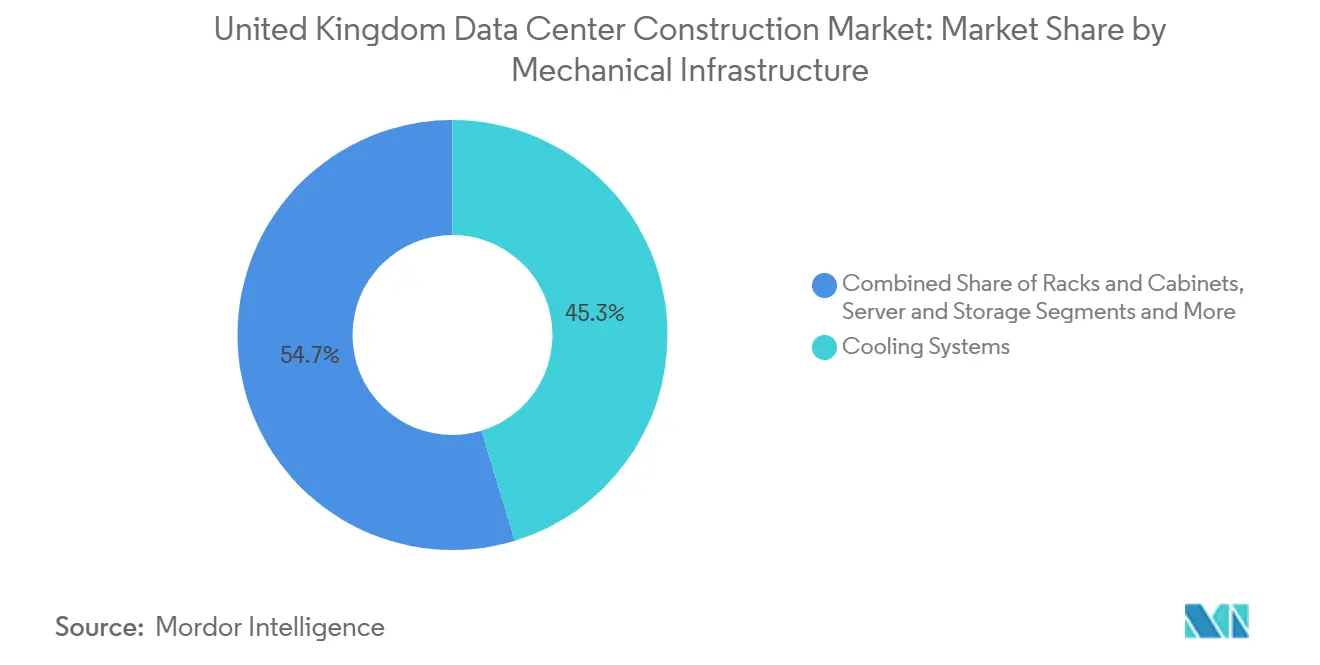

- By mechanical infrastructure, cooling systems secured 45.3% revenue share in 2024, while servers and storage post 14.9% CAGR, the fastest in the segment.

United Kingdom Data Center Construction Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G/6G rollout accelerates edge and core build-outs | +2.1% | National, concentrated in urban centers | Medium term (2-4 years) |

| Hyperscaler pre-leasing and AI-GPU demand wave | +3.2% | South East England, emerging in Midlands | Short term (≤ 2 years) |

| Government “AI Growth Zones” and GBP 14 billion (USD 18.80 billion) CNI program | +2.8% | Culham, Oxfordshire with national expansion | Medium term (2-4 years) |

| Data-center-as-critical-infrastructure tax incentives | +1.4% | National, enhanced in deindustrialized regions | Long term (≥ 4 years) |

| Nationally Significant Infrastructure fast-track permits | +1.7% | National, priority areas with grid capacity | Short term (≤ 2 years) |

| On-site small modular reactor pilots for green power | +0.9% | Culham, Tees Valley, future national rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G/6G rollout accelerates edge and core build-outs

Outdoor 5G coverage reached 90-95% in 2024, triggering demand for micro-data centers positioned within 20 km of radio sites to achieve sub-10 ms latency. Network operators map edge nodes across nearly 2,000 prospective locations, creating a multi-billion-pound construction pipeline that requires rapid modular builds. Trials for 6G starting in 2026 will intensify the need for regionally distributed processing power for augmented-reality and autonomous-vehicle workloads. Contractors respond with prefabricated steel modules that cut delivery schedules from 24 months to six, enabling operators to match the rollout pace of advanced mobile networks. The new edge form factor blends telecommunications and data center disciplines, demanding hybrid engineering teams and new safety standards.

Hyperscaler pre-leasing and AI-GPU demand wave

Microsoft’s 2024 procurement of 485,000 Nvidia AI accelerators, twice the order volume of its nearest peer, underpins forward-leasing deals that fund projects years before completion.[1]Financial Times, “Microsoft Orders 485,000 Nvidia Chips to Power AI,” ft.comSimilar commitments from Google and Amazon stretch contractor backlogs to 2027. AI racks now run at 80 kW instead of the historical 12 kW, raising capital outlay per megawatt by 40%. Contractors that can integrate liquid cooling, two-stage power distribution, and rapid commissioning capture margin expansion. Banks accept pre-lease contracts as collateral, lowering financing costs. The model shifts risk from developers to tenants and signals a structural change from speculative to demand-secured building.

Government “AI Growth Zones” and GBP 14 billion (USD 18.80 billion) CNI program

The first AI Growth Zone in Culham offers simplified permits and priority grid access, shaving at least 18 months from traditional planning cycles.[2]techUK, “Policy Brief: Fast-Track Permits for Digital Infrastructure,” techuk.org Government guarantees underpin large allocations for grid upgrades, land remediation, and site security. Funding flows to deindustrialized regions where redundant heavy-industry layouts shorten enablement phases. The policy directs investment into areas hosting 100 MW power feeds, spawning mega-projects that require consortium contracting. The resulting pipeline anchors thousands of skilled jobs and spreads digital-economy benefits nationwide.

Data-center-as-critical-infrastructure tax incentives

The 2024 Critical National Infrastructure designation grants enhanced capital allowances and business-rate relief for sustainable builds. Regional incentives trim total installed cost by up to 20% in Wales, Scotland, and Northern England relative to London. Developers reroute pipelines to take advantage of these savings, influencing labor deployment and supply-chain staging. The regime rewards high-efficiency cooling systems and on-site renewables, accelerating the adoption of direct-to-chip cooling and solar-plus-battery hybrids.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion in South-East; 132 kV connection moratoriums | -2.4% | South East England, West London priority | Short term (≤ 2 years) |

| Construction-grade labour and MEP cost inflation | -1.8% | National, acute in London and South East | Medium term (2-4 years) |

| Local opposition over water and visual footprint | -1.1% | Green belt areas, residential proximity zones | Medium term (2-4 years) |

| Tight EU/UK Scope-3 carbon-reporting compliance costs | -0.7% | National, enhanced scrutiny for large facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid congestion in South-East; 132 kV connection moratoriums

Connection wait times stretch to 15 years for large projects in West London because National Grid’s queue tops 700 GW The 132 kV moratoriums in boroughs such as Ealing and Hillingdon freeze new builds, pushing developers northward. National Grid’s GBP 35 billion substation program will bring relief, yet commissioning timelines extend well beyond immediate project needs. Contractors pivot to on-site gas peakers, battery farms, and district energy loops, although these approaches raise project cost by 25-30% and complicate planning consents.

Construction-grade labour and MEP cost inflation

The sector needs at least 543,000 skilled workers each year, yet pipelines deliver far fewer qualified trades. MEP wages have climbed 38% since 2020, and price jumps for prefabricated components reach 65%. [3] Cladco“Building Material Prices: 0.4% Rise in March 2024,” cladco.coTalent shortages add three to six months to build schedules, pressuring contractors to establish apprenticeship routes. Certified commissioning engineers remain scarce, and their absence can stall handovers even after civil works finish.

Segment Analysis

By Tier Type: mission-critical drives premium builds

Tier 3 facilities captured 54.1% of the United Kingdom data center construction market share in 2024, underscoring demand for 99.982% uptime among financial and public-sector tenants. The United Kingdom data center construction market size for Tier 3 builds stood at USD 1.05 billion in 2024 and is moving at a 12.1% CAGR to 2030. Tier 4, although smaller today, is on pace to swell by 15.4% annually, propelled by hyperscaler AI workloads that cannot tolerate downtime. Construction specifications call for fully redundant power paths and dual-loop cooling, which lift capex per megawatt by almost 60%. Contractors that can certify concurrent-maintenance standards find profitable niches.

Tier 1 and Tier 2 footprints are retreating as enterprises migrate legacy loads into more resilient clouds. For example, the Legal and General hyperscale campus in Newham is designed to Tier 4 to support latency-sensitive trading platforms. Such projects spread best-practice designs across the supply base, raising the baseline standard for future bids in the United Kingdom data center construction market.

Note: Segment shares of all individual segments available upon report purchase

By Data Center Type: hyperscalers reshape construction patterns

Colocation providers kept a 56.3% hold on the United Kingdom data center construction market in 2024, yet self-built hyperscaler campuses will generate the fastest growth at 16.2% CAGR. The United Kingdom data center construction market size for hyperscaler self-builds reached USD 0.82 billion in 2025 and is projected to more than double by 2030. Direct contracting lets Microsoft, Google, and Amazon align power densities, cooling, and security with their internal roadmaps. Developers face longer tenures but higher certainty as pre-leases underwrite finance.

Edge and enterprise categories stay relevant for latency-sensitive workloads tied to 5G. Micro-facilities of 1-3 MW often deploy in repurposed telecom exchanges, demanding compact layouts and modular electrical skids that suit smaller contractors. The bifurcation pushes general contracting groups to establish dedicated hyperscale divisions while spinning up local networks for edge rollouts.

By Electrical Infrastructure: power backup dominates amid grid constraints

Power backup captured 52.4% revenue within the United Kingdom data center construction market in 2024 as operators sought to buffer unreliable grid access. The United Kingdom data center construction market size for power backup installations reached USD 1.02 billion in 2024. High-density racks elevate battery and generator ratings, driving adoption of lithium-ion UPS systems and rotating flywheels. Power distribution equipment grows at 15.7% CAGR through 2030 as AI loads command dynamic allocation across busways that must support 80 kW racks.

On-site generation appears in new megacampus designs such as the North Lincolnshire proposal that integrates 49.9 MW of gas-fired capacity. These embedded plants embed resiliency yet add complexity to environmental permitting and increase capex per megawatt.

By Mechanical Infrastructure: cooling revolution drives innovation

Cooling systems retained 45.3% revenue in 2024 amid widespread retrofits that swap hot-aisle containment for liquid coolers. Servers and storage, though counted in mechanical outlays, register the quickest climb at 14.9% CAGR as GPU clusters gain traction. Liquid immersion, direct-to-chip cold plates, and rear-door heat exchangers now headline bids in AI campuses. Contractors must master leak-proof piping, dielectric fluids, and advanced leak detection to pass commissioning. The United Kingdom data center construction market size for advanced cooling surpassed USD 0.88 billion in 2025.

Waste-heat recovery systems emerge as a differentiator in planning applications for urban sites. District heating networks in London look to reclaim thermal output, aligning with Scope-3 carbon reporting rules. These add-ons earn business-rate relief under critical-infrastructure incentives.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

England hosts 263 operating facilities totaling 1,753 MW, maintaining leadership in the United Kingdom data center construction market. London and the South East together contribute 63% of 2025 project value yet face the stiffest grid constraints. Grid bottlenecks push fresh allocations to the Midlands, where land costs are lower and power is still accessible. Manchester gains prominence, with new capacity aligned to media and fintech tenants requiring regional redundancy.

The government’s AI Growth Zones policy begins in Culham, Oxfordshire, unlocking fast-track permits and grid upgrades to entice developers. Similar zones are under evaluation in Tees Valley and North Lincolnshire, both regions with heavy-industry heritage and surplus brownfield plots. These areas attract mega-projects such as the GBP 10 billion (USD 13.46 billion) QTS campus that repurposes the former Britishvolt battery site, supporting Northern economic regeneration.

Scotland and Wales benefit from renewable-energy abundance. Vantage Data Centers opted for Cardiff because the grid mixes wind and hydro at competitive tariffs, and devolved authorities provide extra capital allowances. Northern Ireland remains the smallest regional cluster but plays a niche role for cross-border latency-sensitive workloads that serve Irish and UK customers simultaneously.

Competitive Landscape

The contractor pool displays moderate fragmentation. Global infrastructure majors such as SKANSKA, Mace, AECOM, and Balfour Beatty leverage balance-sheet muscle and BIM toolchains to capture turnkey contracts. Specialists like ISG and Mercury Engineering concentrate on data center mechanical and electrical delivery, winning projects where rapid commissioning and technical nuance trump civil scale

Hyperscalers increasingly award design-build-operate mandates directly, bypassing colocation intermediaries. This model demands that contractors assume greater interface risk and maintain on-call upgrade teams once facilities go live. Technology adoption differentiates leaders: prefabrication of electrical and cooling skids compresses schedule by up to 40%, while integrated digital twins support predictive-maintenance handovers.

Consolidation accelerates as large builders acquire niche mechanical specialists to secure labor capacity and proprietary cooling intellectual property. Partnerships such as the Segro–Pure DC GBP 1 billion (USD 1.35 billion) joint venture exemplify real-estate capital combining with technical execution to chase hyperscale wallets. Edge projects open doors for regional firms with telecom pedigree, although ticket sizes remain modest compared with flagship 100 MW campuses.

United Kingdom Data Center Construction Industry Leaders

-

SKANSKA UK plc

-

ISG Ltd

-

AECOM

-

Rider Levett Bucknall

-

Mercury Engineering

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: National Grid began a substation build in Buckinghamshire to unlock 1.8 GW for future West London data centers, part of a GBP 35 billion grid expansion.

- May 2025: QTS confirmed the timeline for Blackstone’s GBP 10 billion (USD 13.46 billion) Northumberland AI campus, with works starting late 2025 and the final phase by 2035.

- March 2025: Segro and Pure DC formed a GBP 1 billion (USD 1.35 billion)venture to target hyperscale builds.

- February 2025: Vantage Data Centers committed EUR 1.4 billion (USD 1.61 billion) for EMEA expansion, including multiple UK sites.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom data center construction market as the value of design, civil works, mechanical-electrical-plumbing fit-outs, and commissioning for new build or capacity-expansion facilities that host mission-critical IT equipment across the UK.

Projects covering only interior refurbishments of server rooms below 250 kW are outside scope.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

- Tier 1 and 2

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed construction managers, colocation design leads, and permitting consultants active in London, Manchester, and the "energy-rich" North East. Discussions clarified average megawatt build costs, liquid-cooling adoption curves, and realistic grid-connection lead times, validating secondary signals and refining timeline assumptions.

Desk Research

We started with construction output series from the Office for National Statistics, Ofgem grid-connection records, Department for Science Innovation & Technology planning notes, and the UK Green Building Council's embodied-carbon guidelines to anchor investment intensity. Tender notices, Environmental Impact Statements, and Uptime Institute certification logs provided project-level timing and tier mix clues. Financials drawn from D&B Hoovers and press archives via Dow Jones Factiva helped benchmark leading contractors' UK revenue splits. These sources illustrate the evidence base; numerous additional publications, filings, and newsfeeds were reviewed to complete the picture.

Market-Sizing & Forecasting

A top-down approach converts national data-center megawatt additions, calculated from grid queue entries and planning approvals, into spend using our blended CAPEX per-MW curve, which varies by tier and cooling density. Select bottom-up checks, such as contractor revenue roll-ups and sampled project bills of quantities, are then overlaid to tighten totals. Key variables feeding the model include: (1) announced hyperscale capacity pipeline, (2) colocation pre-leasing ratios, (3) average build-time elongation driven by power-allocation delays, (4) construction-steel inflation, and (5) renewable-energy share mandates. A multivariate regression against these drivers guides the 2025-2030 forecast, and gaps in bottom-up evidence are bridged by expert-agreed ranges.

Data Validation & Update Cycle

Our outputs pass two rounds of anomaly screening, peer review, and leadership sign-off. We update the model each year, triggering interim revisions when major policy moves, hyperscale land acquisitions, or material cost shocks occur.

Why Mordor's United Kingdom Data Center Construction Baseline Is Dependable

Published estimates often differ because firms choose distinct scopes, input series, and refresh cadences. In data-center construction, totals swing when refurbishment work, land costs, or contingency buffers are treated inconsistently.

Key gap drivers we observed are: some publishers bundle electrical equipment resale, others assume constant $/MW despite liquid-cooling premiums, while a few roll forward 2021 build-to-supply ratios without rechecking the 132 kV connection moratorium in South-East England.

Mordor's model aligns scope strictly to on-site construction spend, applies dynamic cost curves, and is refreshed annually with verified grid and planning data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.94 B (2025) | Mordor Intelligence | - |

| USD 7.30 B (2024) | Global Consultancy A | Includes retrofit interiors and fixture renewals; uses static $/MW |

| USD 11.28 B (2024) | Regional Consultancy B | Adds land purchase and developer fees; no tier-specific cost uplift |

| USD 13.53 B (2024) | Trade Journal C | Applies Europe-wide cost factors, omits power-delay project deferrals |

In sum, our disciplined scope definition, variable-driven cost curve, and yearly source refresh give decision-makers a balanced, transparent baseline they can trace to concrete drivers and replicate with ease.

Key Questions Answered in the Report

What is the current size of the United Kingdom data center construction market?

The market reached USD 1.94 billion in 2025 and is forecast to climb to USD 4.24 billion by 2030

How fast is the market growing?

It is advancing at a 16.92% compound annual growth rate through 2030, supported by hyperscaler investments and government incentives

Which factors are driving the sharp rise in new builds?

Pre-leasing by hyperscalers, the national AI Growth Zones policy, and 5G–6G rollouts top the list, together adding more than seven percentage points to forecast CAGR

Why are Tier 4 facilities gaining traction?

AI training workloads and financial-services applications require 99.995% uptime, making Tier 4 designs—with fully redundant power and cooling—grow at 15.4% CAGR through 2030

Page last updated on: