| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 102.69 Billion |

| Market Size (2030) | USD 120.27 Billion |

| CAGR (2025 - 2030) | 3.21 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

UK Contract Logistics Market Analysis

The United Kingdom Contract Logistics Market size is estimated at USD 102.69 billion in 2025, and is expected to reach USD 120.27 billion by 2030, at a CAGR of 3.21% during the forecast period (2025-2030).

The United Kingdom's contract logistics market landscape is experiencing significant transformation driven by evolving supply chain dynamics and technological advancements. Around 89% of all goods transported by land in Great Britain are moved directly by road, highlighting the critical importance of efficient road transportation infrastructure in the country's logistics industry. The integration of advanced technologies like autonomous vehicles, blockchain, and Internet of Things (IoT) devices is revolutionizing warehouse operations and transportation management. Smart warehouses are becoming increasingly prevalent, with industrial wireless solutions, sensors, and radiofrequency identification (RFID) tags enabling real-time tracking and enhanced operational efficiency.

The e-commerce sector continues to be a major catalyst for innovation in logistics services, with consumer e-commerce now accounting for over 36% of the total retail market in the United Kingdom. This shift has prompted logistics companies to expand their warehousing capacity significantly, with the sector acquiring approximately 13.6 million square feet of warehouse space, representing 22% of total commercial property acquisitions. The demand for advanced fulfillment centers has led to the development of sophisticated automation systems and artificial intelligence-driven solutions for inventory management and order processing.

Recent strategic partnerships and innovations are reshaping the industry landscape. In February 2022, BT Group partnered with GXO Logistics to transform part of BT Group's supply chain across the UK, demonstrating the industry's move toward consolidated and efficient operations. Additionally, Guy's and St Thomas' NHS Foundation Trust's pioneering initiative with CEVA Logistics to trial a daily riverboat delivery service showcases the industry's commitment to sustainable logistics solutions and alternative transportation methods.

The international trade landscape is evolving with new strategic agreements and technological implementations. In February 2022, Britain and South Korea signed an agreement to reinforce pandemic-damaged supply lines for key products like semiconductors, indicating a broader trend toward strengthening international supply chain resilience. The industry is witnessing increased adoption of big data analytics and advanced inventory management systems, with logistics providers investing in cloud computing and IoT devices for real-time remote monitoring and enhanced supply chain visibility. These technological advancements are enabling more precise tracking, better resource allocation, and improved operational efficiency across the logistics market.

UK Contract Logistics Market Trends

E-commerce Growth and Digital Transformation

The explosive growth of e-commerce in the United Kingdom has become a fundamental driver for the contract logistics market, with online retail now accounting for over 36% of the total retail market. This shift in consumer behavior has created unprecedented demands for sophisticated contract logistics services, particularly in areas such as reverse logistics operations and flexible tracking capabilities. Logistics companies in the UK are responding by expanding their infrastructure and capabilities, as evidenced by major investments in new fulfillment centers and distribution hubs across the country. For instance, GEODIS opened two new facilities in 2021: a 40,000 square meter warehouse in Doncaster and a 70,000 square meter logistics site in Lutterworth, specifically designed to handle increased e-commerce volumes.

The evolution of e-commerce has also necessitated the development of more complex and integrated logistics services. Companies are increasingly focusing on providing seamless omnichannel experiences, requiring logistics providers to develop sophisticated return management systems and flexible delivery options. This is exemplified by the growing adoption of services like click-and-collect, same-day delivery, and automated returns processing. The demand for these services has led to the implementation of advanced warehouse management systems and automated sorting facilities, enabling faster processing times and improved accuracy in order fulfillment. Furthermore, the rise of social commerce and mobile shopping has created new requirements for real-time inventory visibility and dynamic delivery scheduling, pushing logistics providers to enhance their technological capabilities.

Understand The Key Trends Shaping This Market

Download PDF

Technological Innovation and Digital Integration

The contract logistics market is being fundamentally transformed by the widespread adoption of advanced technologies, particularly in areas such as the Internet of Things (IoT), artificial intelligence, and automation. Smart warehouses have emerged as a cornerstone of modern logistics services operations, incorporating industrial wireless solutions, sensors, and radiofrequency identification (RFID) tags to enable real-time tracking and enhanced operational efficiency. These technological advancements are particularly evident in the implementation of autonomous intelligent vehicles (AIVs) in warehouse operations, which can halve picking times and significantly reduce the physical intensity of work while improving overall operational efficiency.

The integration of big data analytics and advanced inventory management systems has revolutionized how logistics operations are planned and executed. Companies are increasingly embedding IoT sensors on parts, packages, and equipment to track them throughout their journey, providing unprecedented visibility across the supply chain network. The adoption of blockchain technology is also gaining traction, offering enhanced security and transparency in logistics operations. Furthermore, the development of autonomous vehicles and drone delivery systems is opening new possibilities for last-mile delivery solutions, with several companies conducting trials of these innovative delivery methods. These technological innovations are complemented by the growing implementation of cloud computing and artificial intelligence, which enable real-time decision-making and predictive analytics for optimized logistics operations.

Sustainability and Environmental Considerations

Environmental sustainability has emerged as a crucial driver in the third-party logistics market, with companies increasingly prioritizing green logistics solutions in response to growing environmental awareness and regulatory pressures. This shift is evidenced by innovative initiatives such as the pilot program launched by Guy's and St Thomas' NHS Trust, which introduced daily riverboat delivery services on the River Thames in partnership with CEVA Logistics, marking a significant step toward reducing carbon emissions in urban logistics operations. The industry is witnessing a broader adoption of sustainable practices, including the implementation of electric vehicles for last-mile delivery and the development of eco-friendly packaging solutions.

The focus on sustainability extends beyond transportation to encompass warehouse operations and supply chain optimization. Third-party logistics providers are investing in energy-efficient facilities, implementing renewable energy solutions, and adopting circular economy principles in their operations. This includes the development of reverse logistics capabilities that support product recycling and refurbishment programs. Companies are also increasingly utilizing advanced analytics and route optimization technologies to reduce fuel consumption and minimize environmental impact. The integration of sustainable practices is further supported by the development of green building standards for warehouses and distribution centers, incorporating features such as solar panels, energy-efficient lighting systems, and water conservation measures.

Manufacturing Sector Specialization

The diverse manufacturing base in the United Kingdom, encompassing sectors such as automotive, aerospace, pharmaceuticals, and electronics, has created a strong demand for specialized contract logistics services. This specialization is particularly evident in the development of industry-specific expertise and customized solutions that address the unique requirements of different manufacturing sectors. For instance, in the automotive sector, logistics providers are implementing sophisticated just-in-time delivery systems and specialized handling procedures for sensitive components, as demonstrated by XPO Logistics' partnership with Mercedes-Benz Parts Logistics for managing UK parts distribution through an integrated, digitally-managed transportation network.

The manufacturing sector's demand for enhanced supply chain visibility and traceability has driven significant innovations in 3PL operations. 3PL providers are implementing advanced track-and-trace systems that enable real-time monitoring of goods throughout the supply chain, helping manufacturers identify bottlenecks, optimize inventory levels, and ensure timely delivery to customers. This is particularly crucial in industries such as pharmaceuticals and aerospace, where component traceability and quality control are paramount. The need for flexible logistics solutions has also led to the development of scalable operations that can adapt to demand fluctuations, enabling manufacturers to optimize resource utilization and maintain cost efficiency while meeting varying production requirements.

Segment Analysis: By Type

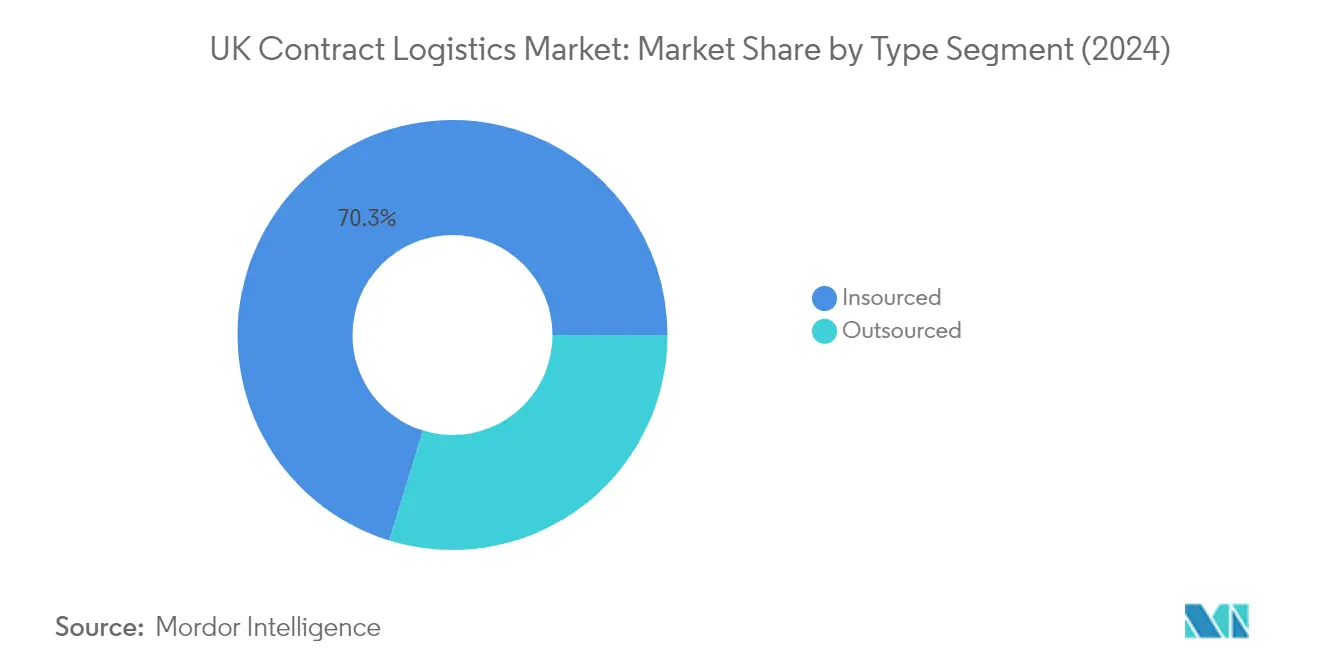

Insourced Segment in UK Contract Logistics Market

The insourced segment continues to dominate the UK contract logistics market, holding approximately 70% market share in 2024. This significant market position reflects the preference of large multinational companies across various industries to manage their supply chain and logistics services internally. These organizations have developed sophisticated, customized business models based on their specific requirements, allowing them to maintain direct control over their logistics operations. The segment's strength is particularly evident in sectors like manufacturing, retail, and automotive, where companies have invested heavily in developing their in-house logistics capabilities, including advanced warehousing facilities, transportation networks, and digital infrastructure. The adoption of robotic process automation and other technological innovations has further enhanced the efficiency of insourced logistics operations, enabling companies to optimize their supply chain performance while maintaining quality control and operational flexibility.

Outsourced Segment in UK Contract Logistics Market

The outsourced segment is experiencing the fastest growth in the UK contract logistics market, with a projected growth rate of approximately 5% during 2024-2029. This accelerated growth is driven by increasing demand from businesses looking to optimize their operations and reduce capital expenditure through third-party contract logistics services partnerships. The segment's expansion is supported by the rising complexity of supply chain operations, particularly in e-commerce fulfillment and last-mile delivery services. Third-party logistics providers are investing heavily in advanced technologies, automated warehousing solutions, and digital platforms to enhance their service offerings. The trend towards outsourcing is particularly strong among small and medium-sized enterprises that benefit from the expertise, infrastructure, and economies of scale offered by specialized logistics service providers, without the need for significant capital investment in their own logistics operations.

Segment Analysis: By End User

Manufacturing and Automotive Segment in UK Contract Logistics Market

The manufacturing and automotive segment dominates the UK logistics market, holding approximately 32% market share in 2024. This significant market position is supported by the UK's robust manufacturing sector and highly skilled workforce that maintains international competitiveness through efficient supply chains. The segment's strength is particularly evident in the automotive sector, where major logistics providers have established dedicated facilities and innovative solutions. The implementation of autonomous intelligent vehicles (AIVs) and digital warehouse management systems has enhanced operational efficiency in this segment. The manufacturing success is maintained through strategic sourcing of components, optimizing internal processes, and leveraging strong international relationships for material procurement.

Healthcare and Pharmaceutical Segment in UK Contract Logistics Market

The healthcare and pharmaceutical segment is projected to experience the highest growth rate of approximately 6% during 2024-2029. This accelerated growth is driven by increasing demand for temperature-controlled contract logistics solutions, particularly for biological medicines and personalized treatments. The segment's expansion is further supported by investments in advanced cold chain facilities and specialized warehousing solutions. The implementation of cutting-edge technologies such as IoT-enabled temperature monitoring systems and blockchain for supply chain transparency has become crucial for maintaining product integrity. The growing emphasis on pharmaceutical security and compliance with stringent regulatory requirements continues to drive innovation in specialized logistics solutions for this sector.

Remaining Segments in UK Contract Logistics Market

The consumer goods and retail, hi-tech, and other end-user segments collectively form a substantial portion of the UK logistics industry. The consumer goods and retail segment has been transformed by the surge in e-commerce activities and omnichannel distribution requirements. The hi-tech segment focuses on secure supply chain solutions and specialized handling of sensitive electronic components. The other end-users segment, encompassing energy, construction, and aerospace industries, contributes to market diversity through specialized logistics requirements and value-added services. Each of these segments continues to drive innovation in areas such as warehouse automation, last-mile delivery solutions, and sustainable logistics practices.

UK Contract Logistics Industry Overview

Top Companies in UK Contract Logistics Market

The UK contract logistics market features prominent UK logistics companies like DHL Supply Chain, Wincanton, Clipper Logistics, and UPS, leading the industry through continuous innovation and strategic expansion. These contract logistics companies are increasingly focusing on technological advancement through automation, robotics, and digital solutions to enhance operational efficiency and meet evolving customer demands. Market leaders are strengthening their positions through strategic acquisitions and partnerships, particularly in specialized sectors like e-commerce fulfillment, healthcare logistics, and temperature-controlled distribution. The industry is witnessing significant investments in sustainable practices, including electric vehicle fleets and eco-friendly warehousing solutions. Companies are also expanding their warehouse networks, especially near major urban centers, while developing specialized capabilities in areas like reverse logistics and value-added services to maintain a competitive advantage.

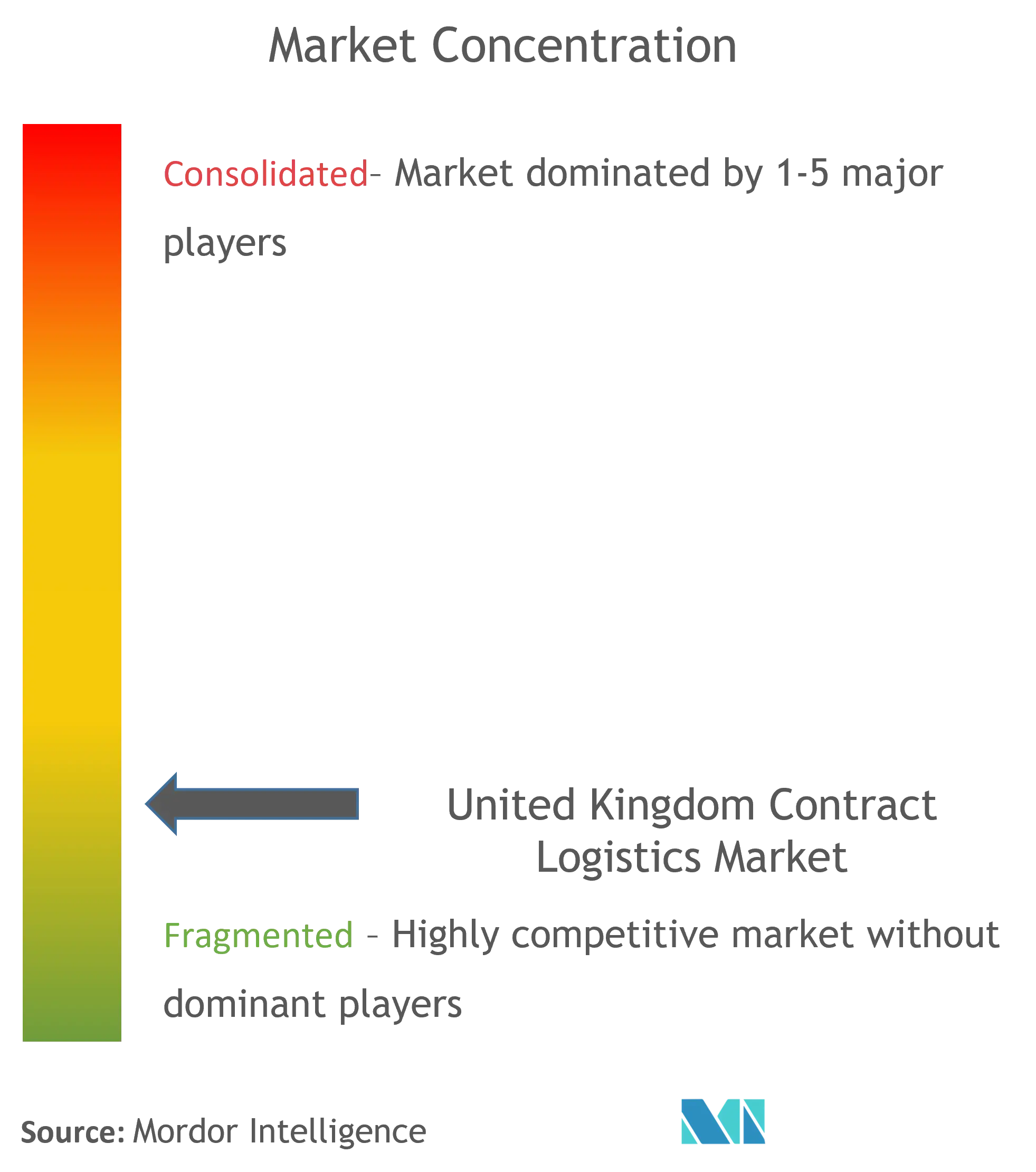

Fragmented Market with Strong Local Presence

The UK contract logistics market demonstrates characteristics of near-perfect competition, with numerous players operating at various service levels and geographical scales. While global logistics conglomerates maintain substantial market share through their extensive networks and comprehensive service offerings, local specialists have carved out strong positions in niche segments such as bulk chemicals, temperature-controlled foods, and specialized distribution. The market's fragmented nature has led to intense competition, driving companies to differentiate through service quality, technological capabilities, and customer relationships rather than purely price-based competition.

The industry is experiencing ongoing consolidation through mergers and acquisitions, as larger players seek to expand their service portfolios and geographical coverage. International companies are actively pursuing acquisitions of local players to strengthen their UK presence, particularly in response to post-Brexit market dynamics. However, the market continues to support both large-scale integrated service providers and smaller specialized operators, with successful companies in both categories focusing on building closer customer relationships and offering tailored solutions to specific industry verticals.

Innovation and Specialization Drive Market Success

Success in the UK contract logistics market increasingly depends on companies' ability to adapt to rapidly evolving customer requirements and technological advancements. Market leaders are investing heavily in digital transformation, including warehouse automation, artificial intelligence, and advanced analytics capabilities to optimize operations and enhance service delivery. Companies focusing on specialized industry solutions, particularly in high-growth sectors like e-commerce, healthcare, and technology, are better positioned to capture market share and maintain strong customer relationships. The development of sustainable logistics solutions and investment in green technologies has become a crucial differentiator in winning and retaining environmentally conscious customers.

For new entrants and smaller players, success lies in identifying and serving underserved market niches while building technological capabilities to compete effectively. The increasing complexity of supply chains and growing customer demands for specialized services create opportunities for companies that can offer innovative solutions in areas like urban logistics, reverse logistics, and value-added services. Regulatory changes, particularly around environmental standards and post-Brexit trade requirements, are reshaping competitive dynamics and creating new opportunities for companies that can effectively navigate these challenges while maintaining operational efficiency and service quality.

UK Contract Logistics Market Leaders

-

XPO Logistics

-

CEVA Logistics

-

DHL International GmbH.

-

Eddie Stobart Logistics

-

Kuehne Nagel

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

UK Contract Logistics Market News

- July 2023: By 2025, CEVA Logistics is expected to switch all of its contract logistics and freight warehouses to 100% low-carbon electricity. The commitment will be based on a mix of low-carbon electricity purchases (renewable & nuclear) from local utilities, as well as increasing its generation of electricity through rooftop solar panels (which CEVA will triple by 2025). CEVA also aimed to achieve 100% LED lighting in warehousing facilities by 2023.

- April 2023: Maersk’s UK warehousing network continues to grow with the signing of a new lease for 685,000 square feet (approximately 63,000 square meters) at SEGRO Logistics Park East Midlands Gateway. A.P. Møller – Mærsk A/S currently operates warehouses in the UK in Doncaster, Tamworth, and Kettering.

UK Contract Logistics Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

-

4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Increased Globalization boosting the market

- 4.2.1.2 Technological advancements bolstering the market

- 4.2.2 Market Restraints

- 4.2.2.1 Infrastructure limitation affecting the market

- 4.2.2.2 Shortage of Labour force affecting the market

- 4.2.3 Market Opportunities

- 4.2.3.1 International trade boosting the market

- 4.2.3.2 Specialized services boosting the market

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technological Trends in the Market

- 4.5 Industry Policies and Regulations

- 4.6 Industry Value Chain Analysis

- 4.7 Insights into the E-commerce Industry in the Country (both Domestic and Cross-border)

- 4.8 Insights into Contract Logistics in the Context of After-sales/Reverse Logistics

- 4.9 Brief on Different Services Provided by Contract Logistics Players

- 4.10 Spotlight on Freight Transportation Costs/Freight Rates

- 4.11 Insights into the Effect of Brexit in the UK Logistics Industry

- 4.12 Impact of COVID-19 on the Market

5. MARKET SEGMENTATION

-

5.1 By Type

- 5.1.1 Insourced

- 5.1.2 Outsourced

-

5.2 By End-User

- 5.2.1 Manufacturing and Automotive

- 5.2.2 Consumer Goods and Retail

- 5.2.3 Pharmaceuticals and Healthcare

- 5.2.4 Hi-tech

- 5.2.5 Other End-Users (Energy, Construction, Aerospace, etc.)

6. COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

-

6.2 Company Profiles

- 6.2.1 DHL Supply Chain

- 6.2.2 UPS

- 6.2.3 Wincanton

- 6.2.4 XP Supply Chain

- 6.2.5 Eddie Sobert

- 6.2.6 CEVA Logistics

- 6.2.7 Clipper Logistics

- 6.2.8 FedEx

- 6.2.9 Rhenus Logistics

- 6.2.10 EV Cargo*

- *List Not Exhaustive

- 6.3 Other Companies (Key Information/Overview)

7. FUTURE OF THE MARKET

8. APPENDIX

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

UK Contract Logistics Industry Segmentation

Contract logistics refers to a long-term collaboration for a wide plethora of services ranging from the conveyance of products or spare parts to the end customer delivery.

The UK contract logistics market is segmented by type (insourced and outsourced) and end-user (manufacturing and automotive, consumer goods and retail, pharmaceuticals and healthcare, hi-tech, and other end users).

The report offers the market size and forecasts in terms of value (USD) for all the above segments.

| By Type | Insourced |

| Outsourced | |

| By End-User | Manufacturing and Automotive |

| Consumer Goods and Retail | |

| Pharmaceuticals and Healthcare | |

| Hi-tech | |

| Other End-Users (Energy, Construction, Aerospace, etc.) |

Need A Different Region or Segment?

Customize Now

UK Contract Logistics Market Research FAQs

How big is the United Kingdom Contract Logistics Market?

The United Kingdom Contract Logistics Market size is expected to reach USD 102.69 billion in 2025 and grow at a CAGR of 3.21% to reach USD 120.27 billion by 2030.

What is the current United Kingdom Contract Logistics Market size?

In 2025, the United Kingdom Contract Logistics Market size is expected to reach USD 102.69 billion.

Who are the key players in United Kingdom Contract Logistics Market?

XPO Logistics, CEVA Logistics, DHL International GmbH., Eddie Stobart Logistics and Kuehne Nagel are the major companies operating in the United Kingdom Contract Logistics Market.

What years does this United Kingdom Contract Logistics Market cover, and what was the market size in 2024?

In 2024, the United Kingdom Contract Logistics Market size was estimated at USD 99.39 billion. The report covers the United Kingdom Contract Logistics Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United Kingdom Contract Logistics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

United Kingdom Contract Logistics Market Research

Mordor Intelligence provides a comprehensive analysis of the United Kingdom contract logistics market. We leverage our extensive expertise in the logistics industry to deliver detailed research. Our report examines the evolving landscape of 3PL and third-party logistics services. It offers crucial insights into the UK logistics market. The analysis covers major logistics companies UK operations and highlights emerging trends in contract logistics services. Additionally, it evaluates the dynamics of the logistics market across the region.

Stakeholders in the logistics industry can access our report PDF for download. It features an in-depth analysis of contract logistics companies and their service offerings. The report examines the size of the UK logistics market, providing detailed assessments of logistics services providers and their technological capabilities. Our comprehensive coverage includes contract logistics innovations and UK logistics services developments. We also offer future growth projections, delivering actionable insights for business leaders and investors in the logistics United Kingdom sector.