| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 78.62 Million |

| Market Size (2030) | USD 105.86 Million |

| CAGR (2025 - 2030) | 6.13 % |

Major Players*Disclaimer: Major Players sorted in no particular order |

Market Major Players")

Market Size")

UK Combined Heat and Power (CHP) Market Analysis

The UK Combined Heat And Power Market size is estimated at USD 78.62 million in 2025, and is expected to reach USD 105.86 million by 2030, at a CAGR of 6.13% during the forecast period (2025-2030).

The UK Combined Heat and Power (CHP) market is experiencing significant transformation driven by evolving energy infrastructure needs and sustainability goals. The sector has seen substantial investments in new projects, exemplified by VH Global's £78 million funding announcement in September 2021 for innovative power generation equipment projects in Nottinghamshire and County Durham. These projects, featuring gas-fired engine technology with carbon capture and reuse systems, demonstrate the industry's commitment to clean, net-zero, flexible, and dependable electricity solutions. The construction activity around CHP installations has shown remarkable resilience, with the Office of National Statistics reporting that new orders for construction in the private commercial sector increased to 114 in 2021, representing a 32% growth compared to pre-pandemic levels.

Technological advancements in CHP systems have led to improved efficiency and environmental performance across various applications. The industry has witnessed a notable shift towards more sophisticated systems, particularly in the commercial and industrial sectors, where combined cycle gas turbine CHP systems have demonstrated superior efficiency levels. These systems have shown the capability to convert fuel to 40% electricity or more, marking a significant improvement in energy conversion efficiency. The integration of advanced control systems and smart technologies has further enhanced the operational capabilities of CHP installations, enabling better load management and optimization of energy production.

The market has seen a growing emphasis on renewable and low-carbon CHP solutions, particularly in the industrial and commercial sectors. In March 2022, MPC Energy Solutions completed the acquisition of the Neol CHP plant in Caguas, with an energy production capacity of approximately 26,000 MWh per year. This trend is further supported by the government's Heat Networks Investment Project (HNIP), which has provided significant funding for district heating projects. For instance, Cory received £12.1 million in funding through HNIP in May 2021 for a major district heating project, demonstrating the government's commitment to supporting sustainable energy solutions.

The industry landscape is being reshaped by strategic partnerships and innovative business models. Gas distribution company SGN and UK renewable energy solutions provider Vital Energi announced a 50:50 joint venture in July 2021, creating an Energy Services Company (ESCO) aimed at providing affordable and low-carbon infrastructure. This trend towards collaboration is enabling more comprehensive energy solutions, with companies combining their expertise to deliver more efficient and sustainable cogeneration systems. The sector has also witnessed increased activity in the biogas CHP segment, with several projects focusing on utilizing organic waste for energy generation, particularly in agricultural and industrial applications.

UK Combined Heat and Power (CHP) Market Trends

Growing Commercial and Industrial Applications

The expanding commercial and industrial infrastructure in the United Kingdom has emerged as a significant driver for the Combined Heat and Power (CHP) market. According to the Office of National Statistics, the construction sector witnessed remarkable growth, with new orders for construction in the private commercial sector reaching USD 17,960 million in 2022, representing a 35% increase compared to 2020. This surge in construction activity has created substantial opportunities for CHP system installations across various commercial establishments, including hotels, supermarkets, office buildings, sports centers, hospitals, and data centers. The versatility of CHP systems in meeting diverse energy requirements has made them particularly attractive for commercial applications, where they provide both energy independence and security.

The commercial sector's energy consumption patterns have significantly influenced CHP system adoption, particularly in supermarkets where refrigeration, lighting, and HVAC systems account for the majority of energy usage, with refrigeration alone responsible for approximately one-third of total consumption. These facilities require specialized CHP configurations to address varying load demands during operational and non-operational hours, leading to the development of more sophisticated internal combustion engine CHPs with higher electrical efficiency. Additionally, the emergence of fuel cell-based CHP systems, driven by falling costs and improved efficiency, has further expanded the technology's commercial applications, particularly in facilities requiring consistent power supply like hospitals and data centers. The integration of heat recovery systems within these facilities enhances power plant efficiency and contributes to overall energy conservation systems.

Understand The Key Trends Shaping This Market

Download PDF

Government Support and Policy Framework

The United Kingdom's robust policy framework and financial incentive programs have significantly propelled the CHP market forward. The Contract for Difference (CFD) Scheme, a government mechanism supporting low-carbon electricity generation, has been instrumental in incentivizing investments in high upfront cost installations of renewable power systems, including renewable CHP systems. This scheme provides crucial protection to project developers from volatile market prices, thereby reducing investment risks and encouraging broader adoption of CHP technology. Furthermore, the Enhanced Capital Allowances (ECA) program allows businesses to write off 100% of their investment in energy-saving technologies, including CHP systems, against taxable profits during the investment period, making the technology financially more attractive to commercial and industrial users.

The government's commitment to supporting CHP adoption is further evidenced by specialized initiatives targeting specific sectors. For instance, the Heat Networks Investment Project (HNIP) has provided substantial funding for district heating projects incorporating CHP systems. A notable example is the GBP 12.1 million funding received by Cory in 2023 for a major district heating project, comprising a GBP 1.6 million commercialization grant and GBP 10.5 million construction loan. Additionally, the introduction of super deduction and special rate first-year allowances for companies subject to corporation tax has created additional financial incentives for CHP installations, particularly benefiting industrial users investing in new plant and machinery. The role of distributed generation and distributed energy resources is increasingly recognized in these policy frameworks, promoting a decentralized approach to energy production.

Environmental Regulations and Emission Reduction Targets

The United Kingdom's stringent environmental regulations and ambitious emission reduction targets have become a crucial driver for the CHP market. Natural gas-based CHP systems have gained particular prominence as they produce the lowest carbon dioxide emissions among all fossil fuel-based technologies, aligning perfectly with the nation's greenhouse gas reduction objectives. According to the Department for Business, Energy, and Industrial Strategy, CHP units utilizing natural gas not only achieve significant reductions in nitrogen oxide emissions but also operate with virtually no sulfur or contaminant emissions, making them an environmentally superior choice for power generation.

The transition toward more sustainable energy solutions has been further accelerated by the development of advanced CHP technologies. The emergence of hydrogen-based fuel cell CHP systems represents a significant advancement in ultra-low emission technology, producing only water vapor as a byproduct. This technological evolution has particularly impacted the transportation sector, where hydrogen-powered fuel cell electric vehicles (FCEVs) are classified as ultra-low emission vehicles (ULEVs). The government's commitment to environmental sustainability is reflected in its announcement of more than GBP 200 million in funding for a three-year comparative demonstration program to evaluate zero-emission solutions for heavy goods vehicles (HGVs), with a clear mandate to ban the sale of fossil-fuel-powered trucks weighing 26 tonnes or less from 2035. Additionally, the focus on waste heat recovery in CHP systems contributes to reducing overall emissions and enhancing system efficiency.

Segment Analysis: End User

Industrial Segment in UK CHP Market

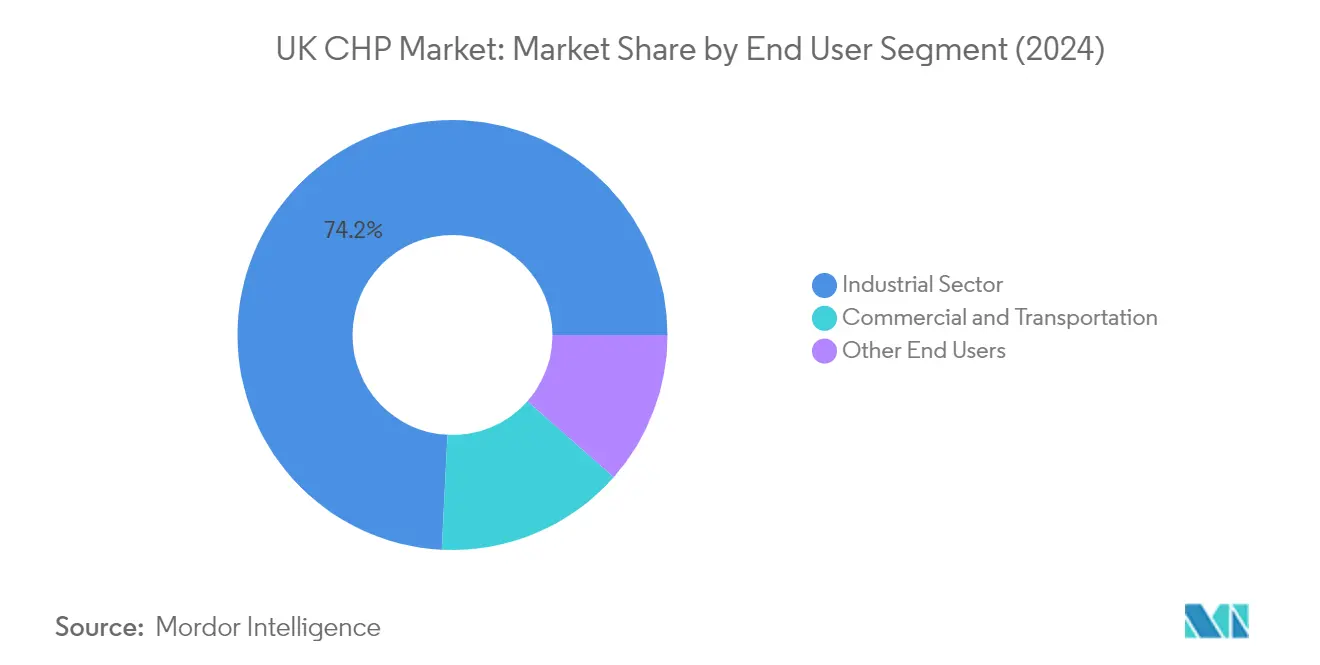

The industrial sector dominates the UK Combined Heat and Power (CHP) market, holding approximately 74% market share in 2024. This significant market position is driven by extensive industrial cogeneration adoption across oil and gas terminals, refineries, chemical industries, food and beverage manufacturing, paper publishing, printing, sewage treatments, and iron and steel industries. The sector's dominance is further reinforced by government initiatives like Enhanced Capital Allowances (ECA) that allow businesses to write off 100% of their investment in energy-saving technologies against taxable profits. Additionally, the introduction of super deduction and special rate first-year allowances for companies subject to corporation tax has strengthened the industrial sector's position in the CHP market. The integration of industrial energy systems is pivotal in maintaining this growth trajectory.

Commercial and Transportation Segment in UK CHP Market

The commercial and transportation sector represents the fastest-growing segment in the UK CHP market for the period 2024-2029. This growth is primarily driven by increasing adoption in hotels, supermarkets, office buildings, sports centers, hospitals, data centers, and shopping centers. The sector's expansion is supported by the development of fuel cell-based CHP systems, which are becoming increasingly popular due to falling costs and rising efficiency. The growth is further accelerated by significant construction projects in the pipeline worth about GBP 2.5 billion in various parts of the United Kingdom, particularly in the hotel sector. The healthcare sector is also contributing to this growth, with the government's New Hospital Programme announcing the development of 40 new hospitals by 2030, creating substantial opportunities for commercial cogeneration system installations.

Remaining Segments in End User Segmentation

The other end-user segments, including agriculture, community heating, and leisure facilities, play a vital role in the UK CHP market despite having a smaller market share. The agricultural sector utilizes CHP technologies for crop processing, dairy and animal farms, horticulture, and water heating applications, particularly through biogas plants that convert organic materials into energy. Community heating projects are gaining traction through government initiatives and funding programs, while leisure facilities are increasingly adopting CHP systems to support amenities such as swimming pools, gyms, and indoor sports courts. These segments collectively contribute to the market's diversity and demonstrate the versatility of CHP applications across different sectors, including residential cogeneration.

Segment Analysis: Type

Gas Turbine Segment in UK CHP Market

The gas turbine segment holds approximately 5% market share in the UK Combined Heat and Power (CHP) market in 2024, making it a significant technology choice among the primary turbine types. Gas turbine CHP systems are particularly well-suited for large-scale and industrial CHP applications with greater than 1 MW capacity, offering advantages like low maintenance requirements and high-quality waste heat generation. The segment's strength is further reinforced by its economic benefits, as gas turbines represent one of the lowest costs per MW capacity in large-scale CHP systems. Major companies like General Electric Energy, Siemens Energy AG, and Caterpillar Inc. are actively providing gas turbine CHP systems in the United Kingdom, contributing to the segment's market position. The use of combined cooling heat and power systems enhances the efficiency of these applications.

Steam Turbine Segment in UK CHP Market

The steam turbine segment is projected to experience notable growth during the forecast period 2024-2029, driven by its versatility in fuel usage and widespread adoption in industrial applications. Steam turbines offer unique advantages as they can operate with various fuels, from clean natural gas to solid waste, including all types of wood, coal, wood waste, and agricultural byproducts. This segment's growth is particularly supported by its increasing adoption in medium and large-scale industrial and institutional applications where inexpensive fuels such as coal, biomass, solid waste, refinery residual oil, and refinery gases are available. The segment's expansion is further bolstered by its primary focus on heat generation, making it especially attractive for industrial plants and commercial buildings with high thermal loads, such as hospitals and district heating systems. The integration of trigeneration systems further enhances the segment's appeal.

Remaining Segments in Type Segmentation

The other types segment, which includes reciprocating engines and organic Rankine cycle CHP systems, plays a crucial role in the UK CHP market. Reciprocating engine CHP systems are particularly valued for their high electrical efficiencies and reliability, making them suitable for distributed generation applications across industrial, commercial, and institutional facilities. Meanwhile, organic Rankine cycle CHP systems are gaining traction due to their ability to efficiently convert medium-grade waste heat into useful energy, particularly beneficial in renewable energy applications. These technologies complement the traditional turbine-based systems by offering solutions for specific applications and contributing to the market's technological diversity, forming part of the total energy systems approach.

UK Combined Heat and Power (CHP) Industry Overview

Top Companies in UK Combined Heat and Power Market

The UK combined heat and power market features prominent players, including Caterpillar Inc., Centrica PLC, General Electric Company, Mitsubishi Power, Siemens Energy AG, Ramboll Ltd, and HELEC Ltd. These companies are increasingly focusing on product innovations, particularly in areas of energy efficiency systems and enhanced efficiency systems. Strategic partnerships and collaborations, especially in renewable energy integration and smart grid solutions, have become crucial for market expansion. Companies are demonstrating operational agility through modular CHP solutions and rapid deployment capabilities, while also investing in digitalization and remote monitoring capabilities. Geographic expansion strategies are primarily centered around strengthening presence in industrial clusters and urban development zones, with companies also emphasizing after-sales service networks and technical support infrastructure.

Market Structure Shows Mixed Global-Local Dynamic

The UK CHP market exhibits a unique structure where global conglomerates operate alongside specialized local players, creating a dynamic competitive environment. Global players like GE and Siemens leverage their extensive technological capabilities and international experience to serve large-scale industrial power generation applications, while local specialists such as HELEC Ltd focus on customized solutions for specific market segments. The market demonstrates moderate consolidation, with larger players maintaining their positions through established relationships with industrial clients and utilities, while smaller players carve out niches in specific applications or regional markets.

Recent market activities indicate an increasing trend toward strategic acquisitions and partnerships, particularly in the renewable energy and sustainable solutions segment. Companies are forming joint ventures to combine complementary capabilities, as evidenced by collaborations between gas distribution companies and renewable energy solution providers. The acquisition landscape shows particular interest in biomass cogeneration facilities and renewable energy developments, indicating a strategic shift toward sustainable energy solutions and decarbonization efforts.

Innovation and Sustainability Drive Future Success

For established players to maintain and expand their market share, developing integrated solutions that combine traditional cogeneration capabilities with renewable energy sources has become crucial. Companies need to focus on enhancing their digital capabilities, particularly in areas of predictive maintenance and smart grid integration. The ability to offer flexible financing options and turnkey solutions, combined with strong local service networks, will be essential for maintaining competitive advantage. Additionally, developing expertise in sector-specific applications, particularly in emerging areas like data centers and sustainable urban development, will be crucial for market leadership.

New entrants and challenger companies can gain ground by focusing on specialized market segments and developing innovative business models that address specific customer pain points. Success factors include the ability to offer modular, scalable solutions that can be easily integrated with existing infrastructure, and developing strong partnerships with local utilities and energy service companies. The regulatory environment, particularly regarding carbon emissions and renewable energy integration, will continue to shape market opportunities, while the increasing focus on energy security and grid resilience creates new opportunities for innovative solutions. Companies must also address the growing end-user demand for sustainable solutions while managing technology obsolescence risks.

UK Combined Heat and Power (CHP) Market Leaders

-

General Electric Company

-

Caterpillar Inc.

-

Siemens Energy AG

-

Ramboll Group

-

Centrica PLC

- *Disclaimer: Major Players sorted in no particular order

_Market.webp)

Need More Details on Market Players and Competitors?

Download PDF

UK Combined Heat and Power (CHP) Market News

- In May 2023, DS Smith officially unveiled the new Kemsley CHP plant with E.ON. The company has joined hands with energy provider E.ON to launch a combined heat and power (CHP) plant at DS Smith's paper mill in Kent.

- In May 2023, Centrica partner 2G Energy decided to introduce its 100% hydrogen-powered combined heat and power (CHP) engine at the UK's first 'Road to Net Zero Tour.' This is one of several promising projects the UK's energy firm thinks will pave the way for low-carbon hydrogen to replace fossil fuels in a large portion of the energy mix.

- In March 2022, MPC Energy Solutions announced that it had completed the acquisition of the Neol CHP plant in Caguas, Puerto Rico, and the United Kingdom. The plant has a capacity of 3.4 MW, and the energy production is expected to be around 26,000 MWh per year. Furthermore, the company has a long-term power purchase agreement to supply electricity from the plant to Neolpharma Inc., a pharmaceutical company.

UK Combined Heat and Power (CHP) Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Investments in the CHP-Based Power Projects

- 4.5.1.2 Supportive Government Policies And Incentives To Develop And Operate CHP Plants

- 4.5.2 Restraints

- 4.5.2.1 Increasing Natural Gas Prices in the United Kingdom

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 CHP Power Plant Statistics, 2014-2022 (by Number and Capacity)

- 4.9 CHP Power Plant Fuel Used Statistics (by Fuel Type and Sector)

5. MARKET SEGMENTATION

-

5.1 End User

- 5.1.1 Industrial Sector

- 5.1.2 Commercial and Transportation Sector

- 5.1.3 Other End Users (Agriculture, Community Heating, Leisure, etc.)

-

5.2 Type

- 5.2.1 Gas Turbine

- 5.2.2 Steam Turbine

- 5.2.3 Other Types (Reciprocating Engine and Organic Rankine Cycle CHP)

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Caterpillar Inc.

- 6.3.2 Centrica PLC

- 6.3.3 General Electric Company

- 6.3.4 Mitsubishi Power Ltd

- 6.3.5 Siemens Energy AG

- 6.3.6 Ramboll Group

- 6.3.7 Helec Limited

- 6.3.8 Tedom AS

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Combined Heat And Power (CHP) Systems

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

UK Combined Heat and Power (CHP) Industry Segmentation

Combined heat and power is a technology that generates heat and electricity simultaneously, from the same energy source, in individual homes or buildings.

The United Kingdom combined heat and power market is segmented by type and end-user. By type, the market is segmented into gas turbine, steam turbine, and other types (reciprocating engine and organic rankine cycle CHP). By end-User, the market is segmented into the industrial sector, commercial and transportation sector, and other end users (agriculture, community heating, leisure, etc). For each segment, the market sizing and forecasts have been done based on revenue (USD).

| End User | Industrial Sector |

| Commercial and Transportation Sector | |

| Other End Users (Agriculture, Community Heating, Leisure, etc.) | |

| Type | Gas Turbine |

| Steam Turbine | |

| Other Types (Reciprocating Engine and Organic Rankine Cycle CHP) |

Need A Different Region or Segment?

Customize Now

UK Combined Heat and Power (CHP) Market Research FAQs

How big is the UK Combined Heat And Power (CHP) Market?

The UK Combined Heat And Power (CHP) Market size is expected to reach USD 78.62 million in 2025 and grow at a CAGR of 6.13% to reach USD 105.86 million by 2030.

What is the current UK Combined Heat And Power (CHP) Market size?

In 2025, the UK Combined Heat And Power (CHP) Market size is expected to reach USD 78.62 million.

Who are the key players in UK Combined Heat And Power (CHP) Market?

General Electric Company, Caterpillar Inc., Siemens Energy AG, Ramboll Group and Centrica PLC are the major companies operating in the UK Combined Heat And Power (CHP) Market.

What years does this UK Combined Heat And Power (CHP) Market cover, and what was the market size in 2024?

In 2024, the UK Combined Heat And Power (CHP) Market size was estimated at USD 73.80 million. The report covers the UK Combined Heat And Power (CHP) Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the UK Combined Heat And Power (CHP) Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

UK Combined Heat And Power (CHP) Market Research

Mordor Intelligence provides a thorough analysis of the UK CHP market. We leverage our extensive expertise in industrial power generation and energy efficiency systems. Our research delves into combined heat and power technologies, including distributed energy resources, district heating, and advanced heat recovery systems. The report offers detailed insights into industrial cogeneration, commercial cogeneration, and residential cogeneration applications. It focuses particularly on power plant efficiency and waste heat recovery technologies.

Stakeholders can download our report PDF, which covers emerging trends in distributed generation and total energy systems. The analysis includes industrial energy systems, power generation equipment, and innovative energy conservation systems. Our research also explores advanced applications such as trigeneration and combined cooling heat and power. This offers valuable insights for decision-makers in the cogeneration sector. The report's comprehensive coverage assists businesses in optimizing their operations while advancing sustainable energy solutions through improved system integration and efficiency.