United Arab Emirates Container Glass Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

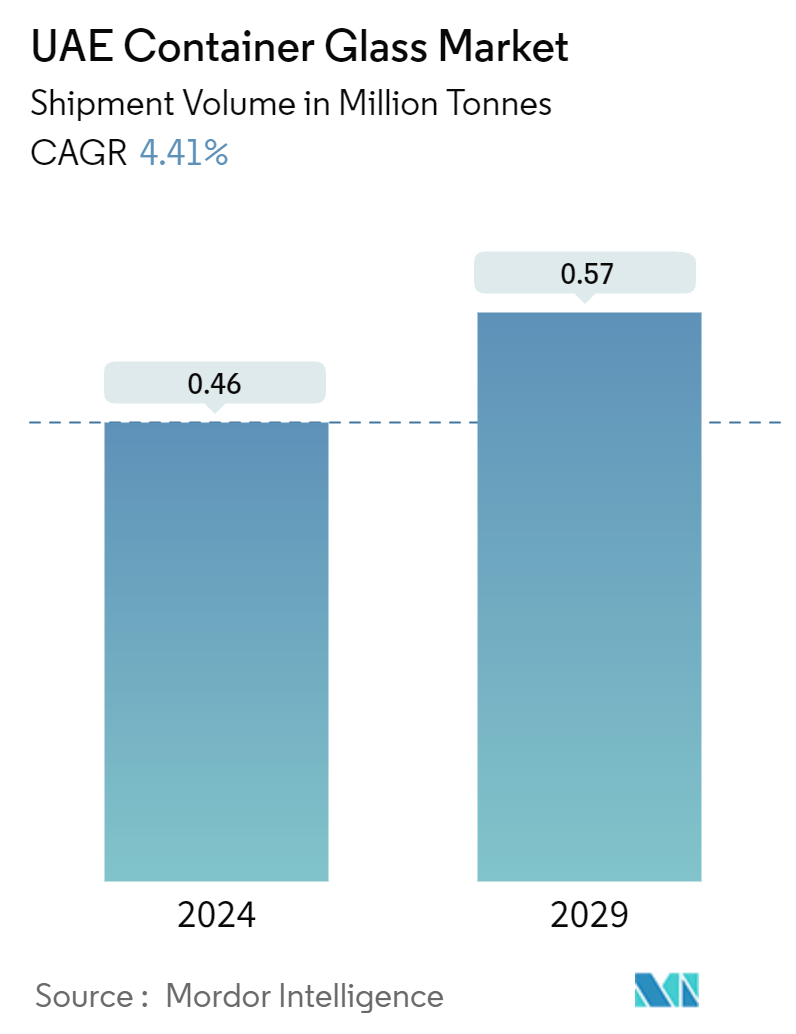

| Market Volume (2024) | 0.46 Million tonnes |

| Market Volume (2029) | 0.57 Million tonnes |

| CAGR (2024 - 2029) | 4.38 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

United Arab Emirates Container Glass Market Analysis

The UAE Container Glass Market size in terms of shipment volume is expected to grow from 0.46 Million tonnes in 2024 to 0.57 Million tonnes by 2029, at a CAGR of 4.41% during the forecast period (2024-2029).

- In the United Arab Emirates, consumers are increasingly opting for glass containers, such as bottles, due to their sustainability, durability, and aesthetic appeal. Glass distinguishes itself from other packaging materials by not absorbing stains or odors. This characteristic ensures that jars remain clean and residue-free, subsequently boosting product demand.

- Data from the United States Department of Agriculture (USDA) underscores the UAE's position as the second-largest economy in the region. Thanks to its strategic location, robust infrastructure, and business-friendly policies, the UAE has cemented its role as a pivotal food trade hub. In 2023, a surge in tourism significantly bolstered the country's food and beverage industry.

- The rising popularity of non-alcoholic beverages in the UAE is attributed to its flourishing tourism sector, the rapid expansion of cafes and restaurants, and a notable shift in consumer preferences towards flavored drinks. These trends are propelling the increased adoption of glass containers in the nation.

- For years, the UAE has positioned itself as a significant player in pharmaceutical manufacturing, diminishing its dependence on imported medicines. Data from the Dubai World Trade Center (DWTC) indicates that the country boasts 23 manufacturing centers, producing approximately 2,500 locally made medicines through advanced manufacturing processes. This burgeoning pharmaceutical landscape is driving the demand for container glass.

- Despite the benefits of container glass being non-toxic, all-natural, and adept at protecting products from harmful chemicals over extended durations, the market encounters challenges. The lightweight and durable nature of plastic, which makes it a favored choice for packaging in the beverage, food, and cosmetic sectors, poses a significant threat to the growth of the glass container market.

United Arab Emirates Container Glass Market Trends

Beverages Segment to Hold Significant Market Share

- According to the USDA, the United Arab Emirates (UAE), strategically positioned at the heart of the Arabian Peninsula, boasts a sophisticated infrastructure that facilitates the seamless import, export, and transit of goods on both regional and global scales. Capitalizing on its advantageous location, cutting-edge infrastructure, and business-friendly policies, the UAE has firmly established itself as a pivotal hub for the food and beverage trade, leading to a heightened demand for glass packaging.

- The UAE's thriving beverage industry is largely fueled by an influx of tourists and expatriates. A report from the UAE Food & Beverage Business Group (F&B Group) reveals that the food and beverage sector accounts for 25% of the nation's total manufacturing GDP, highlighting its significance in driving market growth. Additionally, local manufacturers focus on producing container glass specifically for the food and beverage sectors, further propelling the market's growth.

- With strict regulations governing alcohol production and sales, the UAE has seen a notable rise in non-alcoholic beverage enterprises. The growing popularity of non-alcoholic beers like Corona Cero, Moussy, and Fayrouz has intensified the demand for glass bottle packaging. Moreover, a nationwide shift towards healthier choices, combined with a broadening range of product offerings and regulatory influences, is driving the increased consumption of non-alcoholic beverages. This trend not only signifies long-term lifestyle changes but also amplifies the demand for these products.

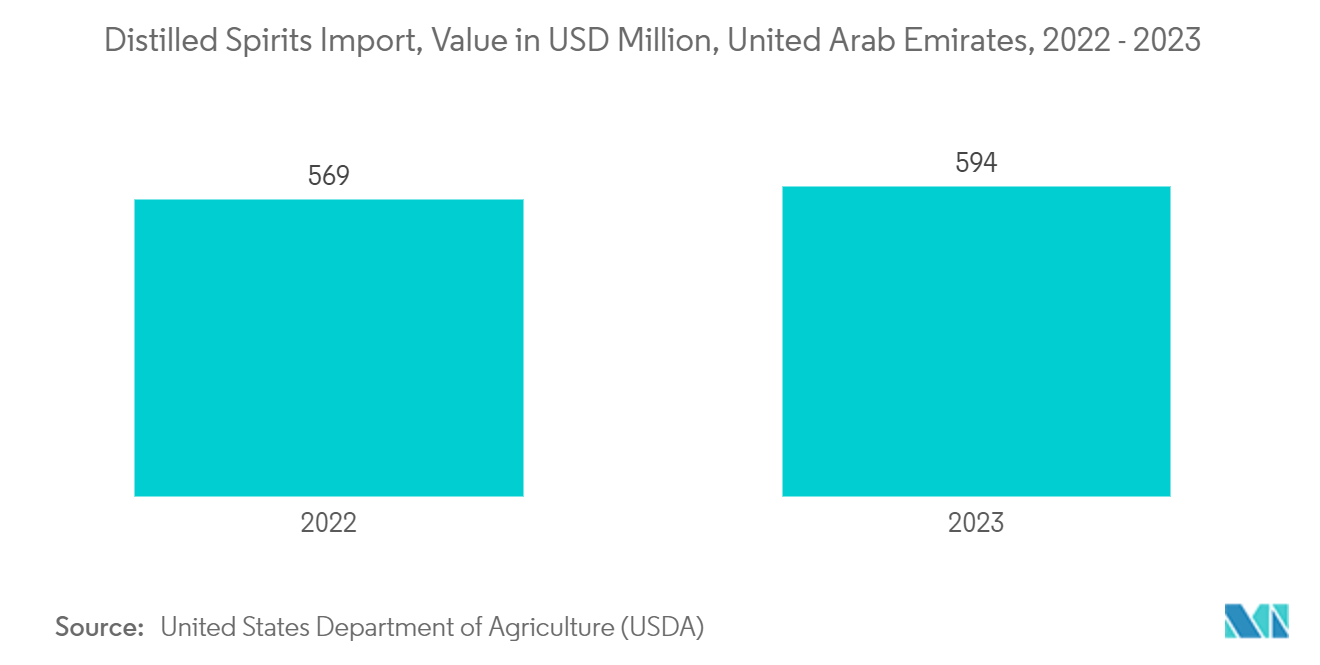

- The UAE's expanding palate for a variety of premium alcoholic drinks is reflected in its escalating imports of distilled spirits. USDA data indicates a jump in distilled spirit imports, climbing from USD 569 Million in 2022 to USD 594 Million in 2023, highlighting the surging demand.

Pharmaceutical Segment is Expected to Grow Significantly

- The Middle East is rapidly emerging as a key player in the pharmaceutical industry. Through ambitious initiatives, strategic partnerships, and substantial investments, the region is poised to spearhead healthcare innovation. The UAE's pharmaceutical sector is evolving swiftly, influenced by economic strategies like the Dubai Industrial Strategy 2030 and the Abu Dhabi Vision 2030, all aimed at addressing the needs of its growing population. This upward trajectory is significantly driving the demand for glass packaging in the pharmaceutical sector.

- In the UAE, a bustling center for pharmaceuticals, medicine manufacturers are boosting production to satisfy rising consumer demands. For instance, in August 2024, OZON Pharmaceuticals secured a deal to establish a vast 150,700 sq. ft. manufacturing facility in Dubai Industrial City. The initial phase of this plant, with an investment of AED 110 million (USD 29.95 Million), aims to produce over 300 million tablets each year, further intensifying the country's demand for glass containers.

- RAK Ghani Glass LLC, a leading manufacturer in the UAE, provides pharmaceutical glass containers to clients spanning the GCC, Middle East, Asia, and Europe. Additionally, major players in the UAE are placing a stronger focus on sustainable manufacturing and emission-free production, further enhancing the appeal of glass packaging in the region.

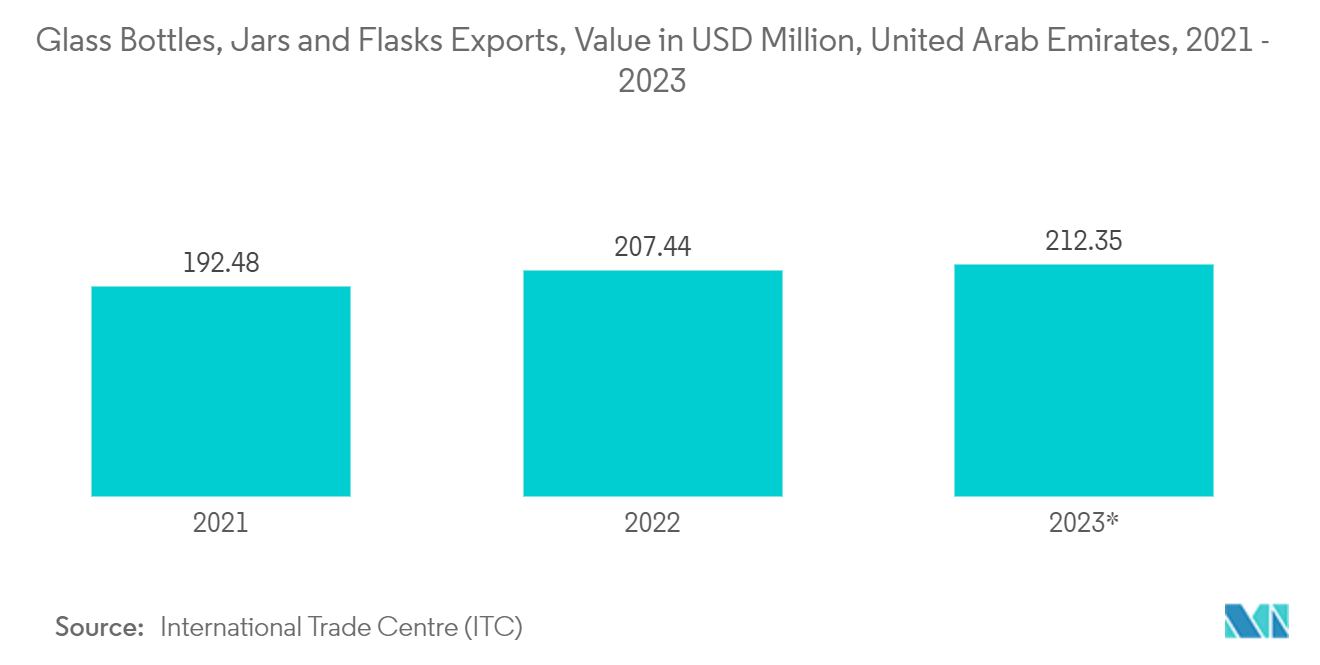

- The UAE stands out not only as a producer but also as a global exporter of glass bottles, jars, and flasks designed for pharmaceutical applications. According to the International Trade Center (ITC), the UAE's glass product exports were valued at an impressive USD 192.48 Million in 2021, with expectations to climb to USD 212.35 Million by 2023. France, Brazil, and South Africa emerge as the primary markets for these exports.

United Arab Emirates Container Glass Industry Overview

The United Arab Emirates Container Glass Market is consolidated, with major players such as RAK Ghani Glass LLC, Al Tajir Glass Industries, Saverglass LLC, and Global Packaging operating in the market and vying for higher market share. These players aim to develop new products, merge and acquire, and expand to cater to the growing consumer demand in the United Arab Emirates market.

United Arab Emirates Container Glass Market Leaders

-

RAK Ghani Glass LLC

-

Saverglass LLC

-

Al Tajir Glass Industries

-

Global Packaging

-

Alwarabottles.com

*Disclaimer: Major Players sorted in no particular order

United Arab Emirates Container Glass Market News

- September 2024: Gulf Capital, an investment firm based in the United Arab Emirates, has divested its strategic stake in Egypt's Middle East Glass S.A.E. (MEG). The stake was sold to MENA Glass Holdings Limited, MEG's majority shareholder. Gulf Capital's growth investment resulted in MEG rising to prominence as the largest glass packaging manufacturer in the Middle East and the second largest across Africa.

- December 2023: Orora Ltd., an Australian packaging company, acquired Saverglass LLC, a glass packaging firm located in the United Arab Emirates, by purchasing Olympe. This acquisition is poised to enhance Orora's strategic advantage, scale, and diversification, paving the way for future growth opportunities.

UAE Container Glass Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Import Export Data of Container Glass

4.3 PESTLE Analysis

4.4 Industry Value Chain Analysis

4.5 Sustainability Trends for Packaging

4.6 Container Glass Furnace Capacity and Location in UAE

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rising Food and Beverage Product Consumption in the Country

5.1.2 Growing Demand of Glass Containers in Pharmaceutical Industry

5.2 Market Challenge

5.2.1 Demand of Plastic Material Over Glass can Hamper the Market Growth

5.3 Trade Scenerio: Analysis of the Historical and Current Export Import Paradigm for Container Glass Industry in United Arab Emirates

6. MARKET SEGMENTATION

6.1 By End-User Industry

6.1.1 Beverage

6.1.1.1 Alcoholic Beverages

6.1.1.2 Non-Alcoholic Beverages

6.1.2 Food

6.1.3 Cosmetics

6.1.4 Pharmaceutical (Excluding Vials and Ampoules)

6.1.5 Other End-User Industries

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 RAK Ghani Glass LLC

7.1.2 Alwarabottles.com

7.1.3 Saverglass LLC

7.1.4 Al Tajir Glass Industries

7.1.5 Global Packaging

- *List Not Exhaustive

8. SUPPLEMENTARY COVERAGE - ANALYSIS OF MAJOR FURNACE SUPPLIERS TO MAJOR CONTAINER GLASS PLANTS IN THE REGION**

9. FUTURE OUTLOOK OF THE MARKET

United Arab Emirates Container Glass Industry Segmentation

Container glass is designed for crafting glass containers, including bottles, jars, drinkware, and bowls. Its key attributes include chemical inertness, sterility, and non-permeability, rendering it especially sought after in the beverage, food, pharmaceutical, and cosmetic sectors. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The United Arab Emirates Container Glass Market is segmented by end-user industry ((beverages (alcoholic beverages and non-alcoholic beverages), food, cosmetics, pharmaceutical and other end-user industries). The market sizes and forecasts are provided in terms of volume (tonnes) for all the above segments.

| By End-User Industry | ||||

| ||||

| Food | ||||

| Cosmetics | ||||

| Pharmaceutical (Excluding Vials and Ampoules) | ||||

| Other End-User Industries |

UAE Container Glass Market Research FAQs

How big is the UAE Container Glass Market?

The UAE Container Glass Market size is expected to reach 0.46 million tonnes in 2024 and grow at a CAGR of 4.38% to reach 0.57 million tonnes by 2029.

What is the current UAE Container Glass Market size?

In 2024, the UAE Container Glass Market size is expected to reach 0.46 million tonnes.

Who are the key players in UAE Container Glass Market?

RAK Ghani Glass LLC, Saverglass LLC, Al Tajir Glass Industries, Global Packaging and Alwarabottles.com are the major companies operating in the UAE Container Glass Market.

What years does this UAE Container Glass Market cover, and what was the market size in 2023?

In 2023, the UAE Container Glass Market size was estimated at 0.44 million tonnes. The report covers the UAE Container Glass Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the UAE Container Glass Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

UAE Container Glass Industry Report

Statistics for the 2024 UAE Container Glass market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. UAE Container Glass analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

UAE Container Glass Market Report Snapshots