Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 566.68 Million |

| Market Size (2031) | USD 739.39 Million |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Arab Emirates Chocolate Market Analysis by Mordor Intelligence

The United Arab Emirates chocolate market is expected to grow from USD 537.30 million in 2025 to USD 566.68 million in 2026 and is forecast to reach USD 739.39 million by 2031 at 5.47% CAGR over 2026-2031. This steady growth continues even as cocoa prices nearly doubled between 2024 and 2025, highlighting the sustained demand for premium and artisanal chocolate products, which appear to be less affected by fluctuations in raw material costs. Health-conscious expatriates are increasingly opting for dark, vegan, and sugar-free chocolate variants, aligning with global trends toward healthier consumption. Meanwhile, the rise of quick-commerce services, which significantly reduce delivery times, is fostering impulse purchases among consumers. Furthermore, the demand for luxury packaging, particularly for gifting during Ramadan and Eid, coupled with the influx of tourists in Dubai and Abu Dhabi malls, contributes to a balanced demand profile. This profile effectively combines everyday snacking preferences with high-margin seasonal sales peaks, showcasing the diverse consumer base and evolving market dynamics in the United Arab Emirates.

Key Report Takeaways

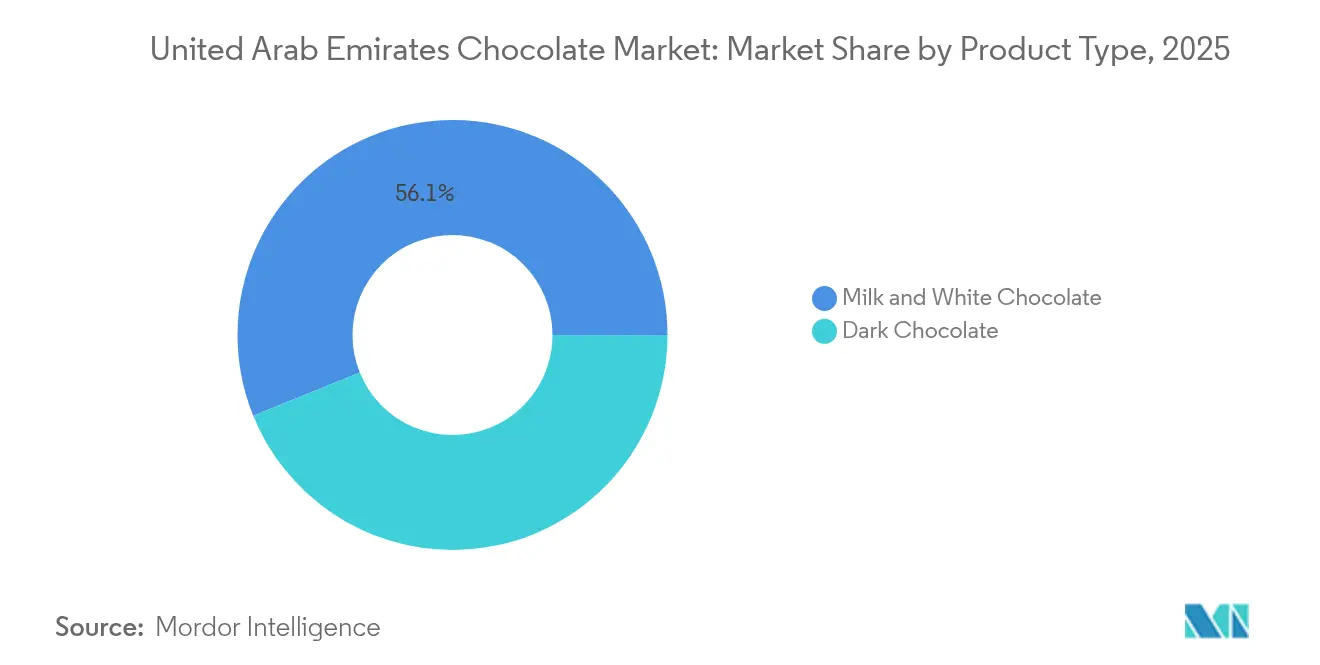

- By product type, milk and white chocolate held 56.12% of the United Arab Emirates chocolate market share in 2025, while dark chocolate is projected to grow at a 7.51% CAGR through 2031.

- By form, tablets and bars led with 39.05% revenue share in 2025; pralines and truffles are advancing at a 6.76% CAGR to 2031.

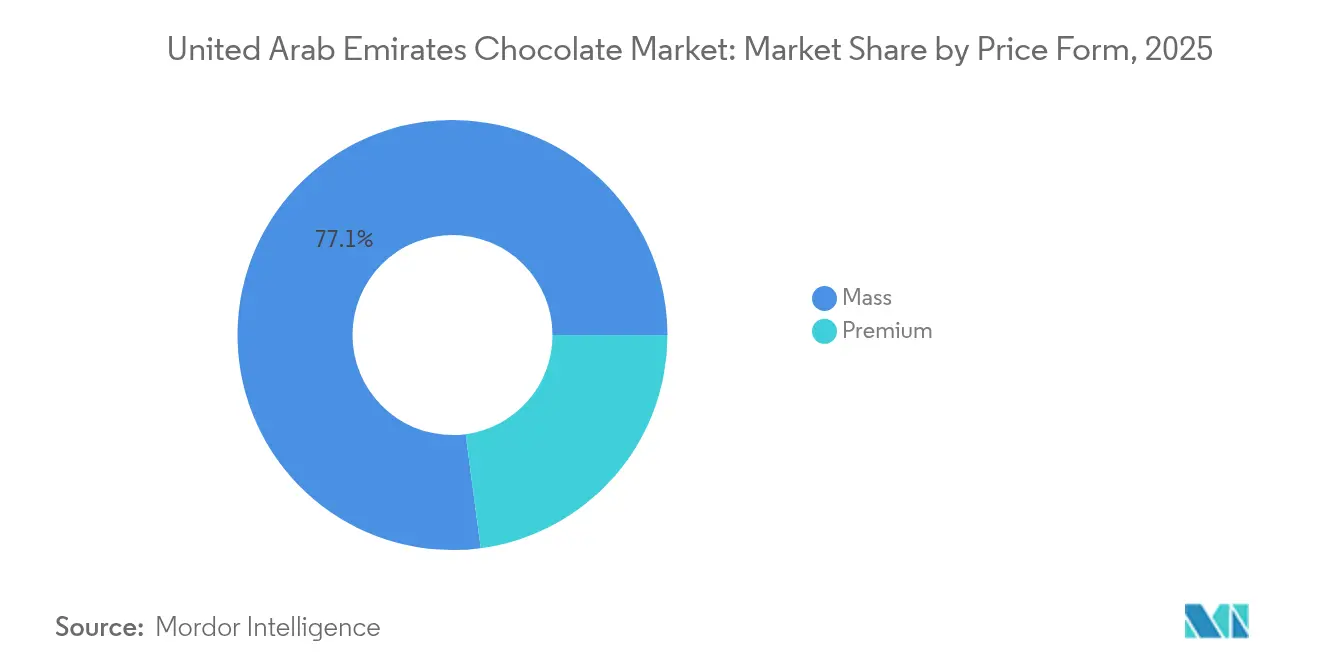

- By price form, the mass segment accounted for 77.10% of the United Arab Emirates chocolate market size in 2025, whereas premium products are forecast to expand at a 6.65% CAGR across the same horizon.

- By ingredient type, dairy-based items represented 75.70% of the United Arab Emirates chocolate market size in 2025, yet plant-based chocolate is climbing at a 6.92% CAGR

- By distribution channel, supermarkets and hypermarkets controlled 35.55% revenue in 2025, while online retail is set to accelerate at a 6.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Chocolate Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for premium and artisanal chocolates | +1.2% | Dubai, Abu Dhabi (core); Sharjah (emerging) | Medium term (2-4 years) |

| Rise of gift-giving and luxury packaging during festivals | +0.9% | National, with peak intensity in Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Strong tourism and hospitality sector supporting chocolate gifting/consumption | +0.7% | Dubai (primary); Abu Dhabi (secondary via cultural tourism) | Medium term (2-4 years) |

| Expansion of e-commerce and online retail channels | +0.8% | National, led by Dubai and Abu Dhabi metro areas | Short term (≤ 2 years) |

| Innovative flavors tailored to Middle Eastern tastes | +0.6% | National, with Dubai as innovation hub | Medium term (2-4 years) |

| Growing health consciousness boosting dark, vegan, and sugar-free chocolate | +1.0% | National, strongest in expatriate-heavy Dubai, Abu Dhabi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Increasing Demand for Premium and Artisanal Chocolates

Premium chocolate is projected to grow at a compound annual growth rate of nearly seven percent through 2030, significantly outpacing the mass segment's slower trajectory. This shift is not solely driven by rising disposable incomes—considering the United Arab Emirates' high GDP per capita in 2023—but rather reflects the growing consumer preference for experiential retail and the appeal of provenance storytelling. In a strategic move, Lindt introduced its limited-edition "Dubai Style Chocolate" bars in Europe during the first half of 2025. Priced at approximately sixteen dollars and with only a thousand bars produced, they sold out within hours, showcasing Lindt's ability to effectively leverage scarcity to drive demand. Meanwhile, Patchi, a key player in the market, has not only revamped its boutique at Mercato Mall but is also developing a massive GCC Experience Centre. This facility will feature personalization kiosks, foster business-to-business partnerships, and incorporate sustainability narratives, focusing on solar energy and recycling. The growth of the premium chocolate segment depends on retailers' ability to justify significant price premiums over mass brands. This can be achieved through transparent sourcing, exclusive product runs, and strong cultural connections—an edge that benefits established luxury brands and agile local artisans, rather than mid-tier multinational companies.

Rise of Gift-Giving and Luxury Packaging During Festivals

Seasonal gifting during Ramadan and Eid led to a significant 150% increase in sales and a remarkable 203.7% growth in gross merchandise value in 2025, with confectionery and pastries accounting for 20.4% of all gifting transactions on platforms such as Flowwow [1]Source: "Eid al-Fitr and Ramadan drive MENA e-commerce boom," samenacouncil.org. A consumer survey conducted in 2025 in Saudi Arabia—relevant to the United Arab Emirates due to shared cultural and demographic characteristics—revealed that 50% of respondents planned to increase their spending on chocolate, dates, and sweets during Ramadan, while 45% intended to purchase these items as gifts for Eid. However, this strong focus on seasonal demand introduces inventory challenges for retailers. Businesses must forecast demand 4 to 6 months in advance to secure essential packaging materials and imported chocolates. Any errors in these projections can result in excess inventory, leading to post-festival markdowns that erode annual profit margins. Furthermore, self-gifting witnessed a 15% year-on-year growth in the first half of 2024, reflecting a broader trend of premiumization extending beyond traditional occasions. Despite this, handmade chocolates ranked lower than flowers and balloons in self-gifting preferences, suggesting an opportunity to reposition these products as appealing options for personal indulgence.

Expansion of E-Commerce and Online Retail Channels

Online retail is expected to grow steadily over the coming years, gradually reducing the dominance of supermarkets and hypermarkets, which currently hold a significant share of the market. In the United Arab Emirates, e-commerce has become a major contributor to Visa's purchase volume. During this period, consumer interest in food and grocery searches has shown notable growth, while quick-commerce queries have experienced a remarkable increase in popularity during the first half of the year. To meet the rising demand for convenience, platforms such as Talabat, Noon, and Carrefour Now have incorporated chocolate into their rapid delivery services, promising delivery within a short timeframe. This trend provides an advantage to locally manufactured or warehoused stock-keeping units (SKUs) over European imports, which are often hindered by longer lead times. As a result, artisans based in the United Arab Emirates, including Mirzam, Zokolat, and The Goodness Company, are finding opportunities to bypass traditional retail channels and establish direct connections with consumers.

Growing Health Consciousness Boosting Dark, Vegan, and Sugar-Free Chocolate

Dark chocolate continues to gain popularity, while plant-based chocolate, including vegan, dairy-free, and date-sweetened options, is experiencing substantial growth. Both categories are outperforming the broader market by a significant margin, reflecting evolving consumer preferences for healthier and innovative alternatives. The Goodness Company's date-sweetened chocolate bars, which are sweetened using natural dates, frequently sell out on e-commerce platforms, showcasing consumers' growing willingness to invest in premium, clean-label products that align with their health-conscious lifestyles. Similarly, the United Arab Emirates-based brand Plaay has successfully carved out a niche by incorporating probiotic inulin, a dietary fiber that supports gut health, and refined-sugar-free recipes into its offerings. Plaay's products are widely accessible through prominent retailers such as Spinneys, Waitrose, Noon, and Talabat, further solidifying its presence in the market.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety regulations and sugar limitations | -0.5% | National, with Abu Dhabi Nutri-Mark as pilot | Short term (≤ 2 years) |

| Seasonal sales spikes leading to demand fluctuations | -0.3% | National, concentrated in Ramadan/Eid periods | Short term (≤ 2 years) |

| Fluctuations in ingredient quality due to global supply issues | -0.7% | National, affecting importers and local manufacturers | Medium term (2-4 years) |

| Pressure on packaging sustainability and waste reduction | -0.4% | Dubai, Abu Dhabi (regulatory focus); national (consumer expectation) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Food Safety Regulations and Sugar Limitations

Abu Dhabi's Nutri-Mark front-of-pack labeling, which will become mandatory from June 2025, assigns A-to-E grades based on the levels of sugar, sodium, and saturated fat in food products [2]Source: International Nut & Dried Fruit Council, “UAE: New Labeling Requirements Under Nutri-Mark Scheme,” inc.nutfruit.org. This initiative is particularly focused on the confectionery segment, where sugar content often exceeds 35 grams per 100 grams. As a result, mass-market milk chocolate bars are at risk of receiving D or E ratings, which could discourage health-conscious consumers from purchasing these products and lead retailers to reduce shelf space for items with lower ratings. Furthermore, Federal Law No. 10/2015 on Food Safety, along with heavy-metals regulations set to take effect in October 2024, establishes maximum residue limits for cadmium and lead in cocoa products. Importers will be required to provide batch-level certificates of analysis, which could increase compliance costs, particularly for smaller distributors. Additionally, Dubai Municipality's Montaji system mandates that imported chocolates must retain at least 50% of their shelf life upon entry into the United Arab Emirates, with a minimum of 6 months remaining. This regulation significantly compresses supply-chain timelines for European and Swiss imports, which typically require 8 to 12 weeks for sea freight.

Fluctuations in Ingredient Quality Due to Global Supply Issues

Cocoa prices experienced a significant surge of 93% between March 2024 and January 2025, exceeding USD 12,500 per metric ton. This sharp increase was driven by crop failures in West Africa and speculative trading activities. Nestlé, a major player in the food and beverage industry, highlighted the need for price hikes in the second half of 2025 due to escalating cocoa and coffee costs, noting that cocoa prices had tripled since early 2023. Similarly, Barry Callebaut, a leading manufacturer of high-quality chocolate and cocoa products, reported that cocoa prices were, on average, 131% higher year-on-year during the fiscal year 2023/24. This unprecedented rise compressed gross margins and forced the company to introduce surcharges for industrial customers to offset the impact. For importers and local manufacturers in the United Arab Emirates, this volatility poses dual challenges: the inflation of input costs, which cannot be fully transferred to price-sensitive mass-market consumers, and disruptions in supply chains when key sourcing regions, such as Ghana and Côte d'Ivoire, face adverse weather conditions or political instability. The United Arab Emirates' reliance on imports—80% of its food supply is sourced externally—further amplifies its exposure to fluctuations in freight rates and port congestion, as evidenced during the Red Sea shipping diversions in late 2023 and early 2024.

Segment Analysis

By Product Type: Dark Chocolate Gains on Wellness Wave

Milk and white chocolate accounted for a 56.12% market share in 2025, primarily driven by the popularity of mass-market brands such as Galaxy, Cadbury Dairy Milk, and Snickers. However, dark chocolate is emerging as a strong contender, with a projected compound annual growth rate (CAGR) of 7.51% through 2031, outpacing the segment's growth by 220 basis points. This growth reflects a shift in consumer preferences, particularly among health-conscious expatriates and affluent Emiratis in the United Arab Emirates, who are increasingly drawn to chocolate with 70% or higher cocoa content. These products are often marketed for their antioxidant benefits and low-sugar formulations, catering to a growing demand for healthier indulgence options. Despite this positive trend, regulatory clarity under Federal Law No. 10/2015, which governs food safety and standards, remains limited, posing challenges for manufacturers and marketers in the region.

Mirzam, a premium chocolate brand, has capitalized on this trend by offering single-origin dark chocolate bars sourced from Vietnam, Madagascar, and Papua New Guinea. These bars are priced between AED 34 and AED 634 (USD 9–173), reflecting their premium positioning in the market. Mirzam emphasizes a bean-to-bar production process and incorporates storytelling inspired by the historic Spice Route, which resonates with consumers seeking authenticity and quality. This approach has enabled the brand to justify price premiums of 5 to 10 times over mass-market chocolate brands, highlighting the growing willingness of consumers in the United Arab Emirates to pay for unique and high-quality chocolate experiences.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Tablets and Bars Lead, but Pralines Capture Premiumization

Tablets and bars accounted for a 39.05% market share in 2025, underscoring their widespread appeal in impulse purchases, supermarket checkouts, and vending machines. These formats have become a staple for consumers seeking convenience and accessibility. Meanwhile, pralines and truffles are projected to grow at a compound annual growth rate (CAGR) of 6.76% through 2031, reflecting a growing consumer preference for experiential products and gifting options that offer a sense of indulgence and personalization. This shift highlights the evolving dynamics of consumer behavior in the confectionery market.

The "Dubai chocolate" trend, featuring pistachio-filled and kunafa-infused bars, originated with local artisan FIX Dessert Chocolatier in the United Arab Emirates in 2021. This trend gained viral popularity in December 2023 and has since expanded globally, reaching renowned brands such as Lindt, Costco, Trader Joe's, and IHOP. Molded blocks, while occupying a niche position often associated with corporate gifting and hotel amenities, face growth challenges due to limited differentiation and competition from tablets. However, premium offerings in this segment, such as Bateel's date-filled chocolates and Patchi's personalized gift boxes, continue to cater to consumers seeking high-quality, luxurious options.

By Price Form: Mass Dominates, Premium Outpaces

In 2025, mass-market chocolate accounted for 77.10% of the market share. This dominance was primarily driven by the extensive product portfolios of major companies such as Mars, Ferrero, Mondelez International, and Nestlé. These brands leveraged widespread distribution channels, including supermarkets, hypermarkets, and convenience stores, to maintain their stronghold in the market. However, the premium chocolate segment is witnessing significant growth, with a compound annual growth rate (CAGR) of 6.65% projected through 2031. This growth is gradually narrowing the market share gap by 130 basis points annually, signaling a shift in consumer preferences toward higher-quality offerings.

The premium chocolate segment differentiates itself through its emphasis on provenance, craftsmanship, and exclusivity. Provenance highlights the origin of ingredients, such as single-origin cocoa or Aleppo pistachios, while craftsmanship focuses on meticulous production methods like bean-to-bar processing and hand-tempering. Limited availability further enhances the appeal of premium products, enabling price premiums of three to five times higher than mass-market alternatives. For example, in December 2024, Läderach launched a limited-edition "FrischSchoggi Dubai" bar, restricting purchases to one 100-gram slab per person per day across 23 global stores, including its outlet in Dubai Mall, United Arab Emirates. The product sold out within hours, showcasing the segment's ability to effectively monetize scarcity and cater to a growing demand for exclusive, high-quality chocolate products.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Ingredient Type: Dairy Leads, Plant-Based Surges

Dairy-based chocolate accounted for a 75.70% market share in 2025, highlighting its strong presence in popular categories such as milk chocolate, pralines, and truffles. This dominance reflects the enduring consumer preference for traditional dairy-based options. However, plant-based chocolate is emerging as a significant growth area, with a projected compound annual growth rate (CAGR) of 6.92% through 2031. This growth is primarily driven by increasing demand from health-conscious expatriates, vegan consumers, and individuals with lactose intolerance, who are seeking alternatives that align with their dietary preferences and health considerations.

Single-origin chocolate represents a specialized niche within the ingredient-type category, appealing to discerning consumers who value premium products with traceable origins. These chocolates are crafted using cocoa sourced from specific estates or cooperatives in regions such as Vietnam, Madagascar, Papua New Guinea, and Ecuador. For example, Mirzam, a chocolate maker based in the United Arab Emirates, sources cocoa beans directly from farmers. The company uses granite wheels to grind roasted beans over several days, ensuring a smooth texture without the use of additives. Additionally, Mirzam collaborates with local artists to create distinctive branding and packaging, further enhancing the appeal of its products.

By Distribution Channel: Supermarkets Lead, Online Gains

Supermarkets and hypermarkets accounted for a 35.55% market share in 2025, driven by key players such as Carrefour, Lulu, Spinneys, and Waitrose. These retailers attract consumers by offering extensive product assortments, competitive promotional pricing strategies, and strategically placed impulse-purchase items at checkouts and end-caps. Carrefour in the United Arab Emirates (UAE), for instance, provides a diverse range of premium chocolate brands, including Lindt, Godiva, Patchi, Toblerone, Hershey's, Nestlé, and Ferrero Rocher, catering to a wide variety of consumer preferences.

Online retail is expected to grow at a compound annual growth rate (CAGR) of 6.60% through 2031, gradually closing the gap with supermarkets. E-commerce platforms such as Talabat, Noon, and Carrefour Now are increasingly incorporating chocolate products into their offerings, capitalizing on their ability to meet 30-minute delivery commitments. This growth highlights shifting consumer preferences toward convenience and the increasing adoption of digital shopping channels in the United Arab Emirates. With nearly 100% internet and mobile phone penetration among the United Arab Emirates population, the Dubai Chamber of Commerce and Industry forecasts e-commerce sales to reach USD 8 billion by 2025 .

Geography Analysis

Dubai holds the largest share of the chocolate market in the United Arab Emirates, supported by an extensive network of grocery stores, a significant influx of tourists each year, and a robust retail infrastructure. Prominent retail destinations such as Dubai Mall, Mall of the Emirates, and City Walk play a pivotal role in driving chocolate sales. Additionally, Dubai is home to the majority of the country's food processing facilities and serves as the regional headquarters for globally recognized brands like Ferrero, Nestlé, and Godiva. In September 2024, Godiva further strengthened its presence in the region by opening another café at Dubai Mall, reflecting the emirate's importance as a hub for premium chocolate offerings.

Abu Dhabi holds the second-largest share of the chocolate market in the United Arab Emirates, driven by a considerable number of grocery stores, millions of annual tourists, and a wide array of hotels that act as key distribution channels for premium chocolate brands and gifting options. In June 2025, the emirate introduced the Nutri-Mark front-of-pack labeling system, which provides grades based on sugar, sodium, and saturated fat content. This initiative is anticipated to influence the formulation strategies of mass-market chocolate bars while also creating opportunities for the growth of low-sugar and dark chocolate variants, catering to evolving consumer preferences.Sharjah, Ajman, and the Northern Emirates collectively hold smaller shares of the chocolate market in the United Arab Emirates. These regions benefit from the presence of thousands of grocery stores in Sharjah but face challenges due to lower per-capita incomes compared to Dubai and Abu Dhabi. As a result, they primarily cater to price-sensitive consumers and families, with mass-market brands being distributed through hypermarkets like Lulu and convenience stores. Notably, Lee Chocolate, a company established in 1947, opened a new branch in Sharjah and received the "Best Chocolate Product Award" at ISM Middle East 2024. This achievement underscores the potential for local manufacturers to expand within the Northern Emirates. However, the limited tourism infrastructure and less affluent demographics in these areas restrict the growth of premium and artisanal chocolate consumption, thereby limiting their overall contribution to the market's expansion.

Competitive Landscape

Top Companies in UAE Chocolate Market

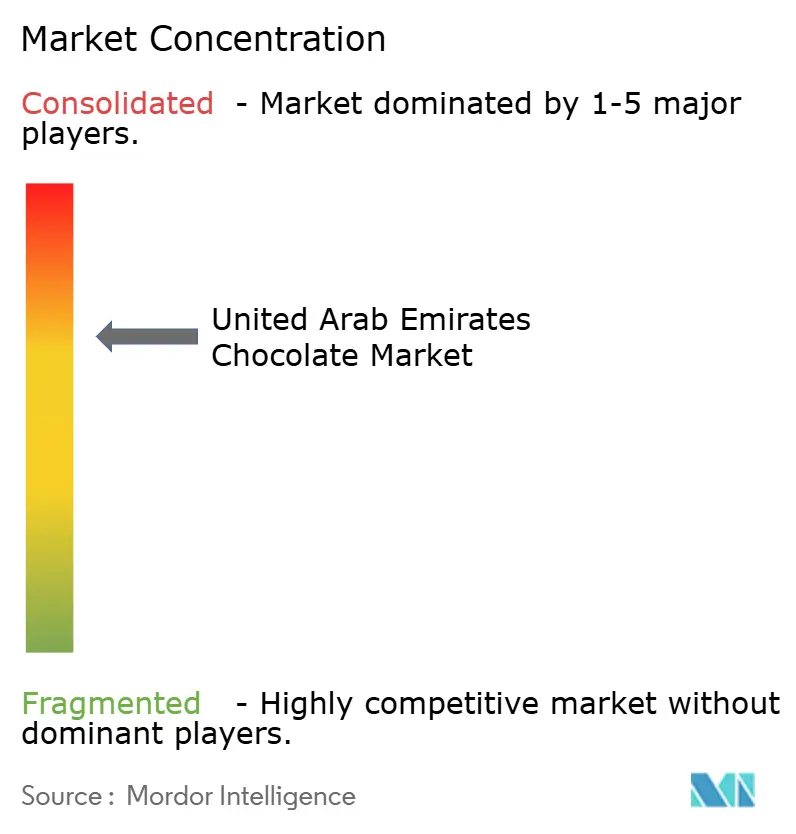

The UAE chocolate market demonstrates a moderately high level of concentration, with Mars, Ferrero, Mondelez, and Nestlé holding a significant share through mass-market brands distributed via supermarkets, hypermarkets, and convenience stores. Meanwhile, premium and gifting segments are dominated by brands such as Patchi, Al Nassma, Mirzam, and Bateel, which operate through boutiques, e-commerce platforms, and partnerships with hotels.

In February 2024, Ferrero established a new regional headquarters in Downtown Dubai, expanding its workforce from 12 to over 400 employees. The company aims to double its GCC business within five years, focusing on localized marketing, seasonal assortments, and B2B partnerships with hotels and airlines. Strategic trends in the market emphasize seasonal gifting occasions (Ramadan, Eid, Diwali), integration of e-commerce, and the introduction of Middle Eastern-inspired flavors such as pistachio, kunafa, dates, saffron, and camel milk. Multinational companies are increasingly licensing local flavors, while artisans are leveraging social commerce and travel retail to scale their operations.

Emerging opportunities in the market include functional chocolates infused with probiotics, collagen, or adaptogens, as well as heat-stable formulations designed for outdoor consumption in the UAE's extreme summer temperatures exceeding 40 degrees Celsius. Additionally, subscription models targeting expatriates seeking European or artisanal chocolate brands unavailable in local retail present a potential growth avenue.

United Arab Emirates Chocolate Industry Leaders

-

Mars, Incorporated

-

Ferrero International S.A.

-

Mondelez International, Inc.

-

Nestlé SA

-

Patchi Industrial Company S.A.L.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Fix Dessert Chocolatier launched a new chocolate flavor in Dubai, expanding its product offerings to appeal to evolving consumer tastes. This move enhances Fix’s regional brand presence and exemplifies innovation within the dynamic United Arab Emirates chocolate sector.

- June 2025: FIX Dessert Chocolatier launched its new “Time to Mango” chocolate bar and hosted a pop-up event at Mall of the Emirates, strengthening premium innovation and engagement in the United Arab Emirates chocolate market through experiential retail and exclusive flavors.

- November 2024: Careem partnered with Forever Rose’s Ebraheem El Samadi to launch luxury Belgian chocolate bars, delivering locally inspired flavors exclusively via Careem Groceries to Dubai and Abu Dhabi, strengthening premium chocolate offerings in the United Arab Emirates.

United Arab Emirates Chocolate Market Report Scope

Dark Chocolate, Milk and White Chocolate are covered as segments by Confectionery Variant. Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others are covered as segments by Distribution Channel.

By Product Type

| Dark Chocolate |

| Milk and White Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Form

| Mass |

| Premium |

By Ingredient Type

| Dairy-based |

| Plant-based |

| Single Origin |

By Distribution Channel

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Form | Mass |

| Premium | |

| By Ingredient Type | Dairy-based |

| Plant-based | |

| Single Origin | |

| By Distribution Channel | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels |

Need A Different Region or Segment?

Customize Now

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF