| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 5.00 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Ultra-Thin Glass Market Analysis

The Ultra-thin Glass Market is expected to register a CAGR of greater than 5% during the forecast period.

The ultra-thin glass industry is experiencing significant technological advancement and innovation across multiple sectors. According to the Japan Electronics and Information Technology Industries Association (JEITA), the global electronics and IT industry production was valued at USD 3,436.8 billion in 2022, highlighting the robust foundation for ultra-thin glass applications. The industry's evolution is particularly evident in display technologies, where manufacturers are pushing boundaries in developing thinner, more durable, and flexible glass solutions. This transformation is reshaping product design possibilities across various electronic devices, from smartphones to large-format displays.

The semiconductor industry is witnessing revolutionary developments in ultra-thin glass applications, particularly in advanced packaging solutions. In September 2023, Intel announced groundbreaking progress in generating the first ultra-thin glass substrates for next-generation advanced packaging, scheduled for implementation post-2027. This development represents a significant shift in semiconductor manufacturing technology, as companies seek to enhance performance while reducing form factors. The integration of ultra-thin glass in semiconductor applications is creating new possibilities for device miniaturization and improved functionality.

The medical and biotechnology sectors are emerging as significant adopters of ultra-thin glass technology, driven by increasing demands for sophisticated diagnostic and monitoring devices. As of 2022, Malaysia alone hosted over 700 medical device manufacturers, indicating the growing industrial base for specialized glass applications in healthcare. The adoption of ultra-thin glass in medical devices is particularly notable in microscopy, biosensors, and diagnostic equipment, where precision and reliability are paramount.

The television and display manufacturing landscape continues to evolve with ultra-thin glass technologies playing a crucial role. According to industry reports, Samsung maintained its leadership in the global television set market with a 19.6% share in 2022, followed by LG and TCL at 11.7%. This competitive landscape is driving innovation in display technologies, with manufacturers focusing on developing advanced ultra-thin glass solutions for improved picture quality and reduced form factors. The industry is witnessing a shift towards more sophisticated display technologies that require increasingly specialized ultra-thin glass compositions and manufacturing processes.

Ultra-Thin Glass Market Trends

Growing Demand from Consumer Electronics

The extensive adoption of ultra-thin glass in consumer electronics has been driven by its unique combination of properties, including lightweight characteristics, perfect flatness, flexibility, and superior surface quality. These properties make ultra-thin glass ideal for various applications, from touchscreen displays and fingerprint sensors to semiconductor substrates. In 2022, Samsung introduced an innovative ultra-thin glass solution for foldable smartphones, measuring only one-third the thickness of a human hair, which was incorporated into the Galaxy Z Fold4 and Galaxy Z Flip4 devices, demonstrating the advancing capabilities of ultra-thin glass technology in consumer devices.

The electronics manufacturing industry continues to expand its utilization of ultra-thin glass, particularly in display technologies and device protection. According to the Japan Electronics and Information Technology Industries Association (JEITA), the global electronics and IT industry production was estimated at USD 3,436.8 billion in 2022, registering a growth rate of 1% year-over-year. The German electrical and electronic industry further exemplified this growth, with turnover reaching EUR 224.5 billion (~USD 236.57 billion) in 2022, showcasing a robust growth rate of 12.02% compared to the previous year. These significant investments in electronics manufacturing, coupled with the increasing demand for more sophisticated display technologies and device protection solutions, continue to drive the demand for ultra-thin glass in the consumer electronics sector.

Understand The Key Trends Shaping This Market

Download PDF

Emerging Utilization from the Automotive Industries

The automotive industry's growing adoption of ultra-thin glass has been primarily driven by the need for lightweight components and advanced glazing solutions that contribute to improved vehicle efficiency and enhanced user experience. Ultra-thin glass is increasingly being utilized in automotive applications such as heads-up displays, instrument clusters, infotainment screens, and panoramic roofs, offering significant weight reduction of 25-30% without compromising safety requirements. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), global vehicle production reached 85.01 million units in 2022, registering a growth rate of 5.99% compared to the previous year, indicating an increased demand for advanced materials including ultra-thin glass.

The electric vehicle (EV) segment has emerged as a particularly strong driver for ultra-thin glass adoption, with manufacturers seeking innovative solutions to optimize vehicle weight and enhance display technologies. In 2022, global electric vehicle sales reached 10.522 million units, registering a remarkable growth rate of 55% compared to the previous year. The World Economic Forum (WEF) reported that approximately 4.3 million new battery-powered EVs (BEVs) and plug-in hybrid electric vehicles (PHEVs) were sold globally in just the first half of 2022, with BEV sales growing by around 75% yearly and PHEVs by 37%. This rapid expansion of the EV market, combined with the increasing integration of advanced display technologies and smart glazing solutions in vehicles, continues to drive the demand for ultra-thin glass in the automotive sector.

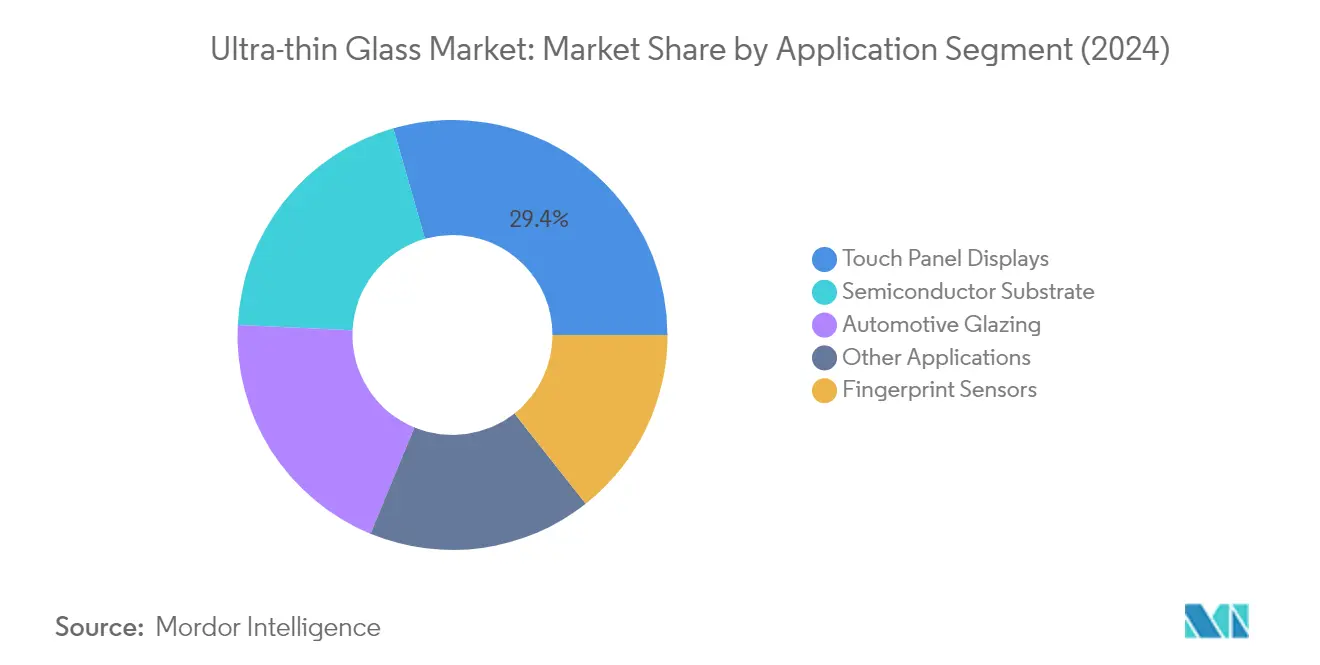

Segment Analysis: By Application

Touch Panel Displays Segment in Ultra-thin Glass Market

The touch panel displays segment continues to dominate the global ultra-thin glass market, commanding approximately 29% market share in 2024. This significant market position is driven by the widespread adoption of touch-enabled devices across various consumer electronics, including smartphones, tablets, and smart wearables. The segment's dominance is further reinforced by technological advancements in display technologies, particularly in OLED and AMOLED displays, which require ultra-thin glass for optimal performance. Major electronics manufacturers are increasingly incorporating advanced touch panel displays in their products, with companies like Samsung leading innovations in foldable display technology using ultra-thin glass solutions. The segment's strong performance is also supported by the growing demand for larger display sizes and improved touch sensitivity in both consumer and commercial applications.

Semiconductor Substrate Segment in Ultra-thin Glass Market

The semiconductor substrate segment is emerging as the fastest-growing application area in the ultra-thin glass market, with a projected growth rate of approximately 12% during 2024-2029. This remarkable growth is primarily driven by the increasing demand for advanced semiconductor packaging solutions and the rapid expansion of the semiconductor industry globally. The segment's growth is further accelerated by significant investments in semiconductor manufacturing capabilities, particularly in regions like Asia-Pacific and North America. The United States' CHIPS and Science Act, with its $52 billion investment in chip manufacturing, and the European Union Chips Act, mobilizing over EUR 43 billion in investments, are creating substantial opportunities for ultra-thin glass in semiconductor applications. The segment is also benefiting from the growing adoption of advanced packaging technologies and the increasing need for high-performance electronic devices.

Remaining Segments in Ultra-thin Glass Market by Application

The other significant segments in the ultra-thin glass market include fingerprint sensors, automotive glazing, and other applications, each serving unique market needs. The fingerprint sensors segment is gaining prominence due to the increasing integration of biometric security features in smartphones and other electronic devices. Automotive glazing applications are expanding with the growing adoption of advanced display technologies in vehicles and the trend toward lighter, more energy-efficient automotive components. The other applications segment encompasses diverse uses such as solar energy applications and medical devices, contributing to the market's overall diversity. These segments collectively demonstrate the versatility of ultra-thin glass and its critical role in enabling various technological advancements across different industries.

Segment Analysis: By End-User Industry

Consumer Electronics Segment in Ultra-thin Glass Market

The consumer electronics segment continues to dominate the global ultra-thin glass market, commanding approximately 60% of the total market share in 2024. This significant market position is primarily driven by the extensive use of ultra-thin glass in smartphones, wearable devices, tablets, and other electronic displays. The segment's dominance is further reinforced by the increasing adoption of OLED and AMOLED displays, which require ultra-thin glass to achieve their full potential. Major electronics manufacturers are continuously pushing for thinner and lighter displays, with companies like Samsung introducing innovative ultra-thin glass solutions for foldable smartphones. The segment's strong performance is also supported by the growing consumer electronics manufacturing base in Asia-Pacific, particularly in countries like China, South Korea, and Japan, where over 70% of global electronics production takes place.

Automotive Segment in Ultra-thin Glass Market

The automotive segment is emerging as the fastest-growing sector in the ultra-thin glass market, with a projected growth rate of approximately 12% during 2024-2029. This remarkable growth is primarily driven by the increasing integration of advanced display technologies in modern vehicles, including heads-up displays, instrument clusters, and infotainment screens. The segment's growth is further accelerated by the rising production of electric vehicles, which typically incorporate more electronic displays and sensors requiring ultra-thin glass components. The automotive industry's shift towards lightweight materials to improve fuel efficiency and reduce emissions is also contributing to the increased adoption of ultra-thin glass solutions. Additionally, the development of smart glass applications and panoramic roofs in premium vehicles is creating new opportunities for ultra-thin glass manufacturers in the automotive sector.

Remaining Segments in End-User Industry

The biotechnology and other end-user industries segments complete the ultra-thin glass market landscape, each serving unique applications and requirements. The biotechnology segment utilizes ultra-thin glass primarily in microscopy applications, biotech samples, and prep slide surfaces, while also finding applications in biosensors due to its chemical compatibility and durability. Other end-user industries encompass diverse applications including solar energy projects, where ultra-thin glass is used in photovoltaic modules, and various industrial applications requiring precise optical and mechanical properties. These segments continue to evolve with technological advancements and increasing demand for specialized applications, contributing to the overall market diversity and growth potential.

Ultra-thin Glass Market Geography Segment Analysis

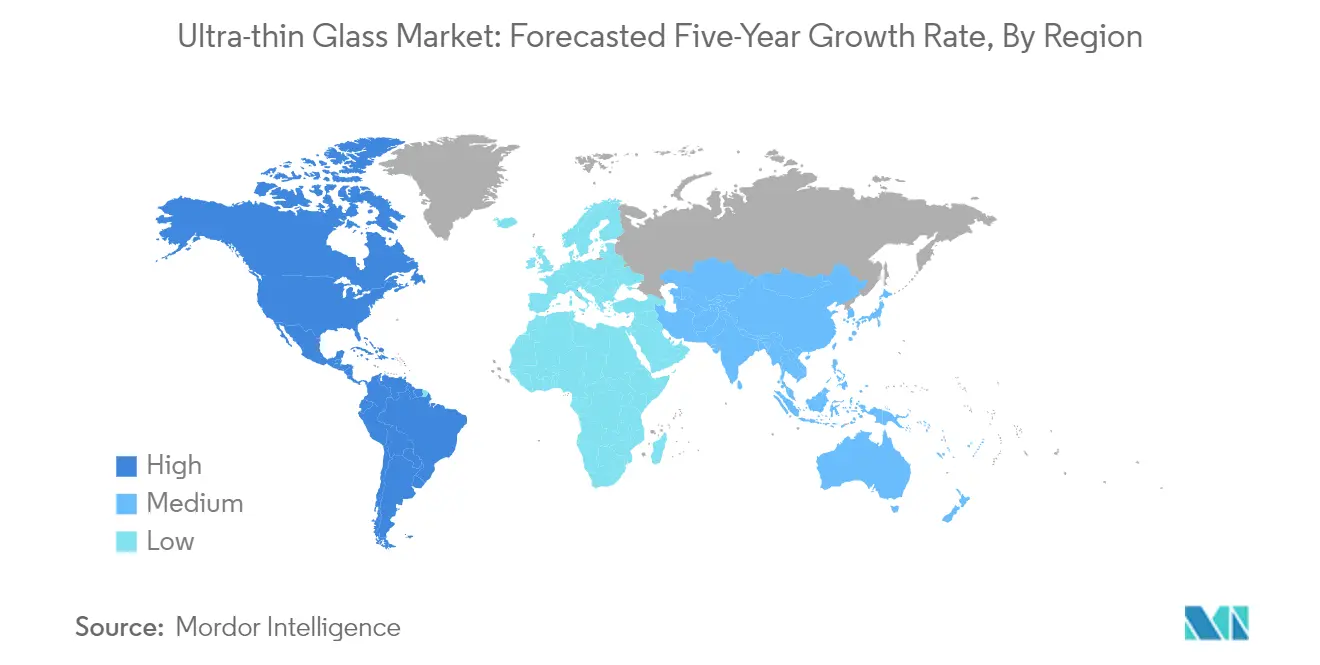

Ultra-thin Glass Market in Asia-Pacific

The Asia-Pacific region represents the largest market for ultra-thin glass globally, driven by its robust electronics manufacturing base and growing automotive sector. China, Japan, India, and South Korea are the key contributors to the regional ultra-thin glass market growth. The region's dominance is attributed to the presence of major consumer electronics manufacturers, particularly in countries like China and South Korea. The increasing adoption of advanced display technologies, rising demand for smartphones, and growing electric vehicle production are fueling market expansion across the region.

Ultra-thin Glass Market in China

China dominates the Asia-Pacific ultra-thin glass market, holding approximately 48% share of the regional market. The country's leadership position is supported by its massive electronics manufacturing infrastructure and growing automotive sector. China's strong market presence is reinforced by its position as the world's largest base for electronics production. The country serves both domestic demand and exports, with a particular focus on smartphones, TVs, and other electronic devices. The government's supportive policies and increasing investments in semiconductor manufacturing further strengthen China's position in the ultra-thin glass market.

Ultra-thin Glass Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 12% during 2024-2029. The country's market expansion is driven by increasing investments in electronics manufacturing and the government's push towards domestic production through initiatives like 'Make in India' and the National Policy of Electronics. India's growing consumer electronics sector, coupled with rising demand for smartphones and other digital devices, is creating substantial opportunities for ultra-thin glass manufacturers. The country's evolving automotive sector and increasing focus on electric vehicles are further contributing to market growth.

Ultra-thin Glass Market in North America

North America represents a significant market for ultra-thin glass, characterized by advanced technological adoption and a strong presence in semiconductor manufacturing. The United States, Canada, and Mexico form the key markets in this region, with each country contributing uniquely to the market dynamics. The region's growth is primarily driven by increasing demand from consumer electronics, automotive applications, and emerging technologies in display systems.

Ultra-thin Glass Market in United States

The United States leads the North American market, accounting for approximately 69% of the regional ultra-thin glass market share. The country's dominant position is supported by its advanced semiconductor industry and strong presence of research and development facilities. The US market benefits from the presence of major technology companies and continuous innovations in display technologies. The implementation of the CHIPS Act and increasing investments in domestic semiconductor manufacturing further strengthen the country's position in the ultra-thin glass market.

Ultra-thin Glass Market in Canada

Canada demonstrates the highest growth potential in North America, with an expected growth rate of approximately 12% during 2024-2029. The country's market is driven by increasing investments in advanced manufacturing technologies and growing demand from the automotive sector. Canada's focus on electric vehicle production and expanding electronics manufacturing base creates significant opportunities for ultra-thin glass applications. The country's strong emphasis on technological innovation and sustainable manufacturing practices further supports market growth.

Ultra-thin Glass Market in Europe

Europe maintains a strong position in the ultra-thin glass market, with Germany, France, the United Kingdom, and Italy as key contributing countries. The region's market is characterized by high technological adoption and significant investments in research and development. Germany emerges as the largest market in the region, while France shows the highest growth potential. The European market benefits from a strong automotive manufacturing base and increasing focus on renewable energy applications.

Ultra-thin Glass Market in Germany

Germany stands as the cornerstone of the European ultra-thin glass market, driven by its robust automotive industry and strong electronics manufacturing sector. The country's leadership in automotive innovation, particularly in electric vehicles, creates substantial demand for ultra-thin glass applications. Germany's advanced manufacturing capabilities and strong focus on technological innovation make it a key market for ultra-thin glass products.

Ultra-thin Glass Market in France

France demonstrates the strongest growth trajectory in the European market, supported by increasing investments in electronics manufacturing and automotive applications. The country's focus on developing advanced display technologies and growing adoption of electric vehicles drives market expansion. France's commitment to technological innovation and sustainable manufacturing practices creates favorable conditions for ultra-thin glass market growth.

Ultra-thin Glass Market in South America

The South American ultra-thin glass market shows promising growth potential, with Brazil and Argentina as the key markets. Brazil emerges as both the largest and fastest-growing market in the region, driven by its expanding electronics manufacturing sector and growing automotive industry. The region's market growth is supported by increasing investments in consumer electronics and rising demand for advanced display technologies.

Ultra-thin Glass Market in Middle East and Africa

The Middle East and Africa region presents emerging opportunities in the ultra-thin glass market, with Saudi Arabia and South Africa as key contributing countries. South Africa leads the regional market in terms of size, while Saudi Arabia shows the highest growth potential. The region's market development is driven by increasing investments in electronics manufacturing and growing adoption of advanced display technologies in consumer electronics and automotive applications.

Get Analysis on Important Geographic Markets

Download PDF

Ultra-Thin Glass Industry Overview

Top Companies in Ultra-thin Glass Market

The ultra-thin glass market is characterized by continuous product innovation, with leading companies focusing on developing advanced manufacturing technologies and specialized glass solutions. Companies are investing heavily in research and development to create thinner, more durable, and versatile glass products, particularly for emerging applications in the electronics and automotive sectors. Strategic partnerships with end-users, especially in the consumer electronics industry, have become crucial for maintaining market position and ensuring steady demand. Operational agility is demonstrated through the establishment of regional manufacturing facilities and distribution networks, allowing companies to better serve local markets and reduce supply chain vulnerabilities. Market leaders are expanding their geographical presence through strategic acquisitions and joint ventures, particularly in high-growth regions like Asia-Pacific, while simultaneously investing in sustainable manufacturing practices and energy-efficient production methods.

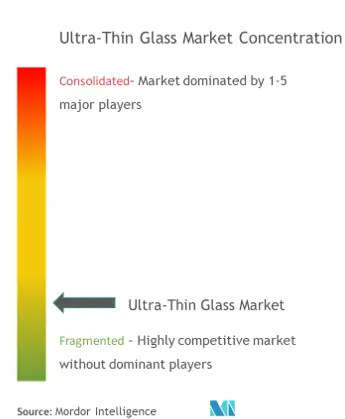

Consolidated Market Led By Global Players

The ultra-thin glass industry exhibits a consolidated structure dominated by established global manufacturers with extensive manufacturing capabilities and technological expertise. Major players like AGC Inc., Corning Incorporated, and Nippon Electric Glass Co. Ltd maintain their leadership through vertically integrated operations, strong research capabilities, and long-standing relationships with key customers. These companies leverage their diverse product portfolios and global presence to serve multiple end-user industries, while regional players focus on specific applications or geographical markets. The market's high entry barriers, including substantial capital requirements and technical expertise, contribute to its consolidated nature.

The competitive landscape is characterized by strategic collaborations and partnerships, particularly in emerging markets and new application areas. Companies are increasingly focusing on developing specialized products for specific applications, such as foldable displays and automotive glazing, to differentiate themselves in the market. The industry has witnessed selective mergers and acquisitions aimed at expanding technological capabilities and geographical reach, though major consolidation moves are limited due to the already concentrated nature of the market. Regional players, particularly in Asia, are gradually expanding their presence through investments in advanced manufacturing facilities and technology partnerships.

Innovation and Customization Drive Future Success

Success in the ultra-thin glass market increasingly depends on companies' ability to innovate and adapt to rapidly evolving end-user requirements, particularly in the consumer electronics and automotive sectors. Market leaders are strengthening their positions through continuous investment in research and development, focusing on developing proprietary technologies and manufacturing processes. Companies are also expanding their product portfolios to include specialized solutions for emerging applications, while maintaining strong relationships with key customers through collaborative development projects and long-term supply agreements. The ability to provide customized solutions while maintaining cost competitiveness has become a crucial differentiator in the market.

For new entrants and smaller players, success lies in identifying and focusing on specific market niches or regional opportunities where they can build competitive advantages. Companies need to develop strong technical capabilities and establish reliable supply chains to compete effectively. The market's future will be shaped by factors such as increasing demand for flexible displays, growing adoption of electric vehicles, and stricter environmental regulations regarding manufacturing processes. Players must also consider the concentrated nature of key end-user industries, particularly consumer electronics, where strong relationships with major manufacturers are essential for success. The relatively low threat of substitution for ultra-thin glass in many applications provides stability, but companies must continue to innovate to maintain their competitive edge.

Ultra-Thin Glass Market Leaders

-

Nippon Electric Glass Co.,Ltd

-

SCHOTT AG

-

AGC Glass Europe

-

Corning Incorporated

-

Fraunhofer FEP

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Ultra-Thin Glass Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Demand from Consumer Electronics

- 4.1.2 Other Drivers

-

4.2 Restraints

- 4.2.1 High Cost of Raw Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porters Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION

-

5.1 Application

- 5.1.1 Semiconductor Substrate

- 5.1.2 Touch Panel Displays

- 5.1.3 Fingerprint Sensors

- 5.1.4 Automotive Glazing

- 5.1.5 Other Applications

-

5.2 End-user Industry

- 5.2.1 Consumer Electronics

- 5.2.2 Automotive

- 5.2.3 Biotechnology

- 5.2.4 Other End-user Industries

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 AGC Glass Europe

- 6.4.2 Central Glass Co. Ltd

- 6.4.3 Changzhou Almaden Co. Ltd

- 6.4.4 Corning Incorporated

- 6.4.5 CSG Holding Co. Ltd

- 6.4.6 Emerge Glass

- 6.4.7 Fraunhofer FEP

- 6.4.8 Nippon Electric Glass Co. Ltd

- 6.4.9 Nitto Boseki Co., Ltd

- 6.4.10 Novalglass

- 6.4.11 Schott AG

- 6.4.12 Taiwan Glass Industry Corporation

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Advanced Glass for Solar Energy Projects

- 7.2 Other Opportunities

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Ultra-Thin Glass Industry Segmentation

The report on ultra-thin glass market includes:

| Application | Semiconductor Substrate | ||

| Touch Panel Displays | |||

| Fingerprint Sensors | |||

| Automotive Glazing | |||

| Other Applications | |||

| End-user Industry | Consumer Electronics | ||

| Automotive | |||

| Biotechnology | |||

| Other End-user Industries | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Ultra-Thin Glass Market Research FAQs

What is the current Ultra-thin Glass Market size?

The Ultra-thin Glass Market is projected to register a CAGR of greater than 5% during the forecast period (2025-2030)

Who are the key players in Ultra-thin Glass Market?

Nippon Electric Glass Co.,Ltd, SCHOTT AG, AGC Glass Europe, Corning Incorporated and Fraunhofer FEP are the major companies operating in the Ultra-thin Glass Market.

Which is the fastest growing region in Ultra-thin Glass Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Ultra-thin Glass Market?

In 2025, the Asia Pacific accounts for the largest market share in Ultra-thin Glass Market.

What years does this Ultra-thin Glass Market cover?

The report covers the Ultra-thin Glass Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Ultra-thin Glass Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Ultra-thin Glass Market Research

Mordor Intelligence provides comprehensive insights into the rapidly evolving ultra-thin glass market. We leverage our extensive research expertise and global industry connections to deliver thorough analysis. Our study examines the ultra thin glass industry dynamics, including manufacturing technologies, supply chain complexities, and emerging applications. The report offers detailed coverage of various segments, from super thin glass technologies to specialized ultra thin glass substrates used in advanced electronics.

Stakeholders across the value chain can access crucial data about the ultra thin glass market size and growth projections. Our report is available in an easy-to-download PDF format. It includes detailed segments covering the expanding market for ultra thin glass in smartphones, displays, and semiconductor applications. The report delivers actionable insights for manufacturers, suppliers, and end-users. These insights are supported by rigorous primary research and data-driven forecasting methodologies. We examine both established and emerging applications of ultra-thin glass technologies.