United Kingdom Retail Banking Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

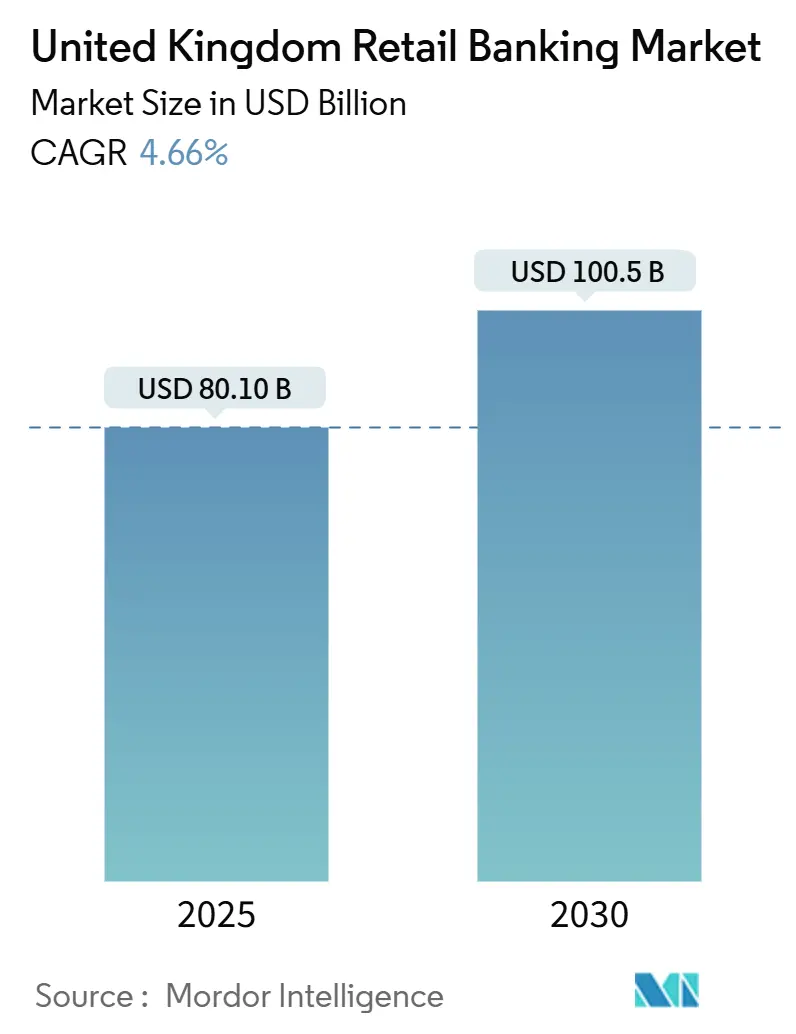

| Market Size (2025) | USD 80.10 Billion |

| Market Size (2030) | USD 100.5 Billion |

| Growth Rate (2025 - 2030) | 4.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Retail Banking Market Analysis by Mordor Intelligence

The United Kingdom retail banking market stands at a current value of USD 80.1 billion and is forecasted to reach a market size of USD 100.5 billion by 2030, reflecting a 4.66% CAGR. Rising digital engagement, pro-innovation regulation, and rapid product diversification are allowing banks to unlock fresh revenue despite continuing macroeconomic pressures such as inflation and interest-rate volatility. Rate cuts delivered by the Bank of England in February and May 2025 are reshaping pricing power across mortgage and savings portfolios, while mandatory open-banking APIs continue to intensify customer mobility. Consolidation moves by large incumbents, paired with swift growth among neobanks, are accelerating a technology arms race that centres on mobile experience, data analytics, and ESG-linked products. Competitive emphasis is therefore shifting toward cost-to-serve efficiency, speed of product rollout, and balance-sheet agility, all of which underpin the medium-term expansion forecast for the United Kingdom retail banking market.

Key Report Takeaways

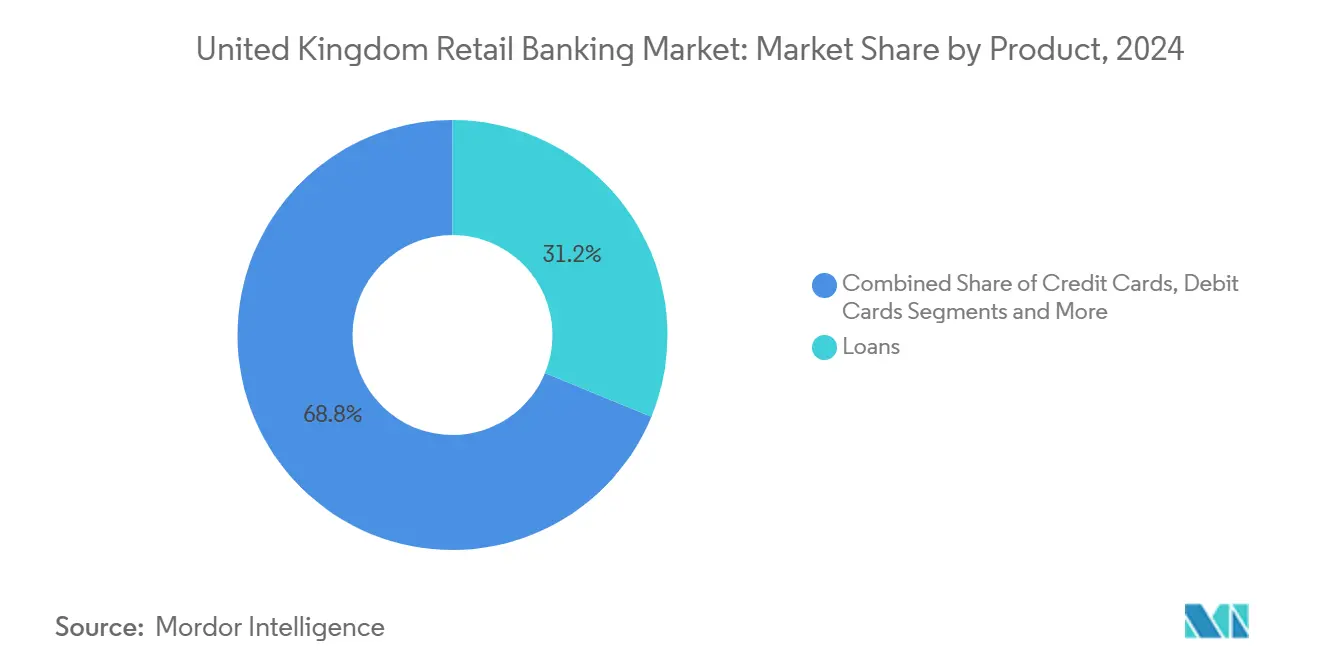

- By product category, loans led with 31.2% of the United Kingdom retail banking market share in 2024; Other Products are projected to expand at a 6.8% CAGR to 2030.

- By channel, online banking held 52.4% share of the United Kingdom retail banking market size in 2024; Online banking is projected to rise at a CAGR of 7.2% through 2030.

- By customer age group, the 29-44 years cohort accounted for a 35.7% share of the United Kingdom retail banking market size in 2024; the 18-28 years segment is projected to advance at a 6.3% CAGR through 2030.

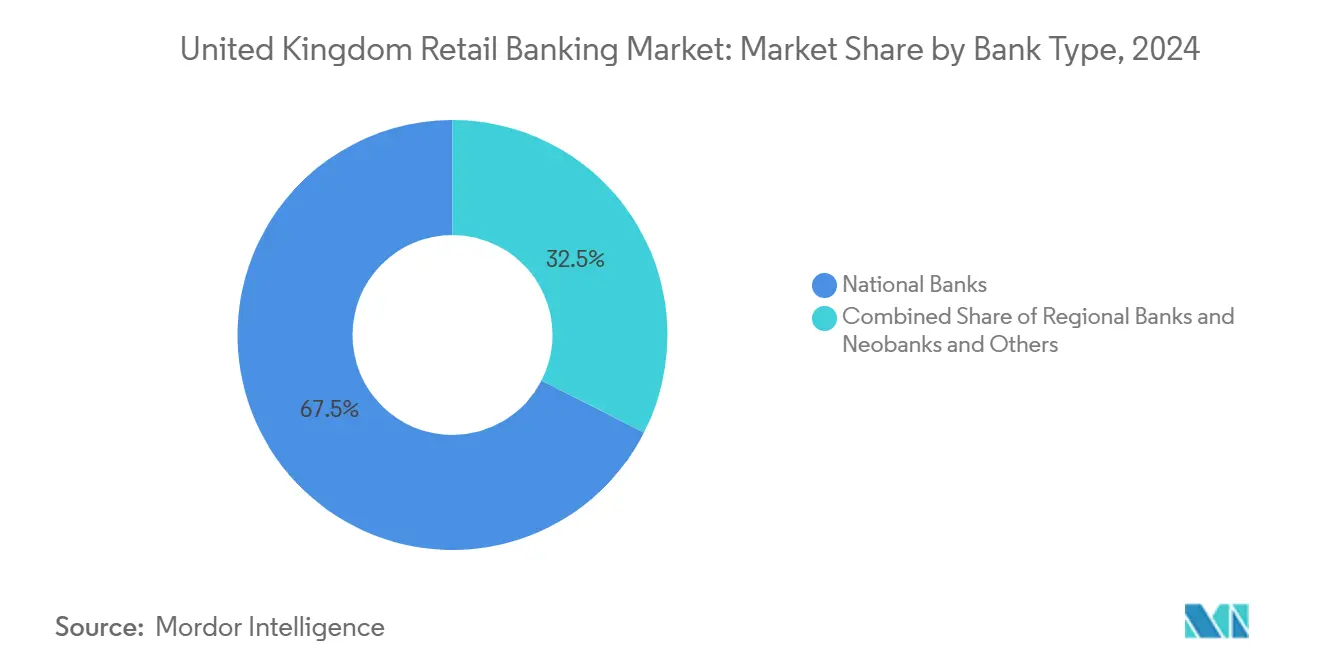

- By bank type, national banks controlled 67.5% of the United Kingdom retail banking market share in 2024, whereas neobanks & others are forecasted to post a 9.1% growth rate during 2025-2030.

United Kingdom Retail Banking Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bank Rate–Induced Expansion of Net-Interest Margins | +1.2% | UK-wide, higher in high-mortgage regions | Medium term (2-4 years) |

| Mandatory Open-Banking APIs Accelerating Account-Switching & Aggregation | +0.8% | UK-wide, urban concentration | Long term (≥ 4 years) |

| Rapid Adoption of Mobile Banking in the UK | +1.0% | UK-wide, metropolitan focus | Short term (≤ 2 years) |

| Fixed-Rate Mortgage Maturity Wave Driving Re-Mortgage Volumes | +0.9% | UK-wide, South East & London | Short term (≤ 2 years) |

| Regulated “Buy-Now-Pay-Later” Boosting Unsecured Lending Penetration | +0.5% | UK-wide, younger users | Medium term (2-4 years) |

| Rise of ESG-Linked Deposit Products under UK Green Finance Strategy | +0.4% | UK-wide, affluent urban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bank Rate–Induced Expansion of Net-Interest Margins

The February and May 2025 Bank of England base-rate cuts to 4.5% and 4.25% have widened the spread between lending and funding costs for many institutions[1]Bank of England, “Monetary Policy Report May 2025,” bankofengland.co.uk. Traditional lenders swiftly repriced new fixed-rate mortgages but moved more slowly on deposit rates, crystallizing a favorable lag that flowed directly into net-interest income. Early-2025 data show mortgage completions climbing 50%, confirming that borrowers still view fixed-rate products as attractive before further rate moves. Banks with large, low-cost retail deposit bases capture the greatest benefit, yet the FCA’s Consumer Duty rules obligate clearer disclosure that could compress this advantage over time. As competition for refinances heats up, margin sustainability will hinge on disciplined product pricing and funding-cost optimization.

Mandatory Open-Banking APIs Accelerating Account-Switching & Aggregation

Standardized APIs let fintech platforms move current-account data between providers in minutes rather than weeks, cutting long-standing frictions that once anchored customers. Switch-rate acceleration is steering loyalty toward perceived service quality, pushing 42% of banks to place digital-experience upgrades at the top of their investment agendas. Third-party aggregators simultaneously harvest richer customer data, enabling highly personalized offers that deepen engagement. Institutions with advanced analytics turn this aggregated insight into cross-sell uplift, while laggards risk churn as users gravitate to interface-centric brands. Over a four-year horizon, continued ecosystem build-out is expected to keep customers switching above historic norms, sustaining upward pressure on product innovation across the United Kingdom retail banking market.

Rapid Adoption of Mobile Banking in the United Kingdom

Mobile banking volumes have climbed 64% since 2024 as apps displace browser and branch interactions. Operating-cost leverage is immediately visible: digital transactions cost pennies compared with pounds for branch servicing. Banks offering friction-free mobile journeys report higher cross-sales than peers with basic functionality, reinforcing the revenue upside that accompanies channel migration. Yet only one quarter of institutions have replaced legacy cores to fully exploit cloud scalability, creating a widening capability gap that favors technology leaders. The short-term momentum of mobile adoption, therefore, remains one of the most potent growth accelerants for the United Kingdom retail banking market.

Fixed-Rate Mortgage Maturity Wave Driving Re-Mortgage Volumes

Half of all United Kingdom mortgagors face higher monthly payments as 2021-era fixed deals expire and require refinancing. Early-2025 data indicate monthly payment increases topping GBP 500 for many households, especially in London and the South East. Lenders are easing affordability rules to capture refinancing flows, yet the “mortgage lock-in” effect still suppresses housing-transaction volumes. Product teams are responding with longer terms, offset features, and flexible overpayment structures designed to preserve borrower retention without eroding margins. Over the next two years, remortgage volumes will stay elevated, underpinning loan growth within the United Kingdom retail banking market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange-Fee Caps Compressing Card-Fee Income | -0.6% | United Kingdom-wide, card-heavy models | Short term (≤ 2 years) |

| Branch Closures Creating Rural Financial Exclusion Risk | -0.3% | Rural Scotland, Wales, Northern England | Medium term (2-4 years) |

| FCA Consumer Duty Escalating Compliance & Product-Design Costs | -0.7% | United Kingdom-wide, small firms are most affected | Medium term (2-4 years) |

| Loan-Impairment Spike from Cost-of-Living Squeeze | -0.5% | Low-income regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Interchange-Fee Caps Compressing Card-Fee Income

Regulation limits debit-card interchange to 0.2% and credit-card interchange to 0.3%, stripping an estimated GBP 480 million of annual income from banking book P&Ls[2]HM Treasury, “Interchange Fees: UK Regulation Update 2024,” gov.uk. Larger banks spread the loss across diversified revenue, yet specialist card issuers must tilt toward interest-earning balances and subscription-style fees. Brexit-linked rises on United Kingdom-to-EEA transactions lifted fees as high as 1.5%, but impending PSR caps threaten to reverse those gains[3]Payment Systems Regulator, “Card Scheme Cross-Border Fees Final Report,” psr.org.uk. In the near term, pressure on interchange economics complicates digital-wallet monetization strategies and slows credit-card innovation.

Branch Closures Creating Rural Financial Exclusion Risk

Roughly 6,000 branches have shut since 2015, with rural communities suffering the heaviest reduction. Physical access deficits elevate cash-handling costs for small businesses and widen the digital divide among older residents. Government-backed banking hubs are rolling out, yet concerns persist that network coverage lags real community needs. Areas experiencing heavy closure concentrations also report higher uptake of alternative, often higher-cost, financial-service providers. Over the medium term, reputational and regulatory scrutiny will weigh on banks that downsize networks without robust mitigation plans.

Segment Analysis

By Product: Loans Drive Revenue While Innovation Accelerates

Loans contributed 31.2% to the United Kingdom retail banking market share in 2024, underscoring their central role in interest-income generation. The remortgage surge described earlier supports continued volume expansion, while competitive repricing and diversified mortgage features aim to maintain borrower stickiness. Buy-to-let lending grew 47% in Q4 2024, signaling investor confidence despite higher base-rate volatility. Transactional current accounts remain core relationship anchors but produce limited standalone revenue, motivating cross-sell strategies into higher-yielding credit lines.

The Other Products category is forecast to compound at 6.8% annually through 2030, outpacing core lending growth. ESG-linked deposits, mass-affluent wealth solutions, and embedded payments reinforce revenue resilience as margins narrow on traditional products. Debit-card volumes climbed to 2.2 billion transactions worth GBP 66.5 billion in March 2024[4]UK Finance, “UK Card Payments 2024,” ukfinance.org.uk. Savings instruments such as Bank of Scotland’s 5.50% Monthly Saver attract funds that can be recycled into lending, lowering wholesale funding reliance. Collectively, product-line diversification is broadening the revenue base of the United Kingdom retail banking market.

Note: Segment shares of all individual segments available upon report purchase

By Channel: Digital Transformation Reshapes Service Delivery

Online channels held 52.4% of the United Kingdom retail banking market size in 2024, with digital transactions growing 7.2% annually. Every major institution now positions mobile as the default service gateway, blending payments, budgeting tools, and marketplace offers into a single interface. The 18% of adults who still visit branches monthly value face-to-face advisory for complex needs, illustrating that bricks-and-clicks integration remains essential.

Traditional networks are rationalizing footprints, yet post-office partnerships and video-banking kiosks sustain physical reach. Investment priorities skew toward cloud migration, API microservices, and cyber-resilience to safeguard the expanding digital perimeter. Over the forecast horizon, omnichannel fluency will be a defining competitive lever within the United Kingdom retail banking market.

By Customer Age Group: Demographic Preferences Drive Strategy

Consumers aged 29-44 commanded 35.7% of the United Kingdom retail banking market share in 2024, reflecting their peak borrowing years for mortgages and family-related spending. Banks target this cohort with bundled home-purchase services, insurance add-ons, and long-term investment products. Their hybrid channel behaviors demand seamless toggling between app and branch, pushing interface consistency to the top of design briefs.

The 18-28 group is set to grow fastest at 6.3% CAGR as financial-entry products like BNPL and student accounts migrate to mobile-first formats. Neobanks resonate strongly with this demographic through transparent pricing and real-time budgeting notifications. Institutions that cement early relationships gain lifetime cross-sell potential as these customers accumulate wealth, illustrating the demographic’s strategic relevance for the United Kingdom retail banking market.

By Bank Type: Competitive Dynamics Reshape Market Structure

National banks held 67.5% of the United Kingdom retail banking market size in 2024, leveraging product breadth and strong funding franchises. Their scale enables heavy technology investment, but legacy IT and branch costs temper agility compared with digital-native rivals.

Neobanks forecast 9.1% growth between 2025 and 2030 on the strength of lean cost bases and app-centric branding. Early-stage customer acquisition relied on fee-free accounts, yet sustained profitability depends on expanding into credit, wealth, and SME services. Incumbents counter by launching sub-brand apps and, in some cases, acquiring challengers outright, a trend likely to continue as the United Kingdom retail banking market evolves.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Regional variation remains pronounced, even within the compact United Kingdom footprint. London and the South East command outsized volumes in mortgages and wealth management thanks to higher incomes and property values. The fixed-rate maturity wave is especially intense here, adding refinance urgency that lifts short-term lending activity. Fintech density in the capital also speeds up the adoption of every new feature unveiled across the United Kingdom retail banking market.

Northern England, Scotland, Wales, and Northern Ireland display distinct demand characteristics shaped by disparate economic growth rates and population density. Rural zones observe the steepest branch-closure ratios, which threaten service exclusion for less-digital customers. The government’s 350-hub rollout is intended to offset access gaps, yet critics argue hub coverage lags the pace of closures. Community-rooted building societies often defend shares by emphasizing personal service and local underwriting autonomy that big banks sometimes lack.

Digital usage now exerts more influence on geographic opportunity than physical infrastructure. Almost 98% of United Kingdom adults hold a current account, shrinking the unbanked population to 1.6%. Nonetheless, 26% still struggle to obtain cash conveniently, fueling policy pressure for multi-provider cash-back facilities and ATM subsidies. Banks that devise sustainable hybrid models capable of serving both hyper-digital urbanites and cash-reliant rural customers will cement durable regional franchises in the United Kingdom retail banking market.

Competitive Landscape

The United Kingdom retail banking market remains concentrated around the “Big Four” of Lloyds Banking Group, Barclays, HSBC, and NatWest, all of which wield extensive customer bases and capital strength. Open-banking-driven switching, however, is chipping away at incumbent stickiness, compelling back-office modernization and aggressive cost-management programmes. HSBC aims for USD 3 billion in cost savings through 2027 by consolidating duplicated operations and increasing automation.

Strategic consolidation is accelerating. Nationwide’s USD 3.7 billion acquisition of Virgin Money strengthens its mortgage and savings franchise, while NatWest’s USD 2.5 billion purchase of Sainsbury’s Bank assets adds customer scale and data to fuel cross-selling. Deal flow reflects a belief that fixed-cost digital infrastructure favors larger balance sheets, even as regulators maintain a cautious stance on market-power concentration.

Neobanks such as Monzo, Starling, and Revolut continue to steal share in day-to-day banking by emphasizing user interface, instant notifications, and fee transparency. Yet they, too, face profitability headwinds as customer acquisition costs rise and interchange ceilings bite. Competitive priorities therefore converge on data monetization, AI-driven personalization, and embedded-finance partnerships that place banking into non-bank customer journeys, sustaining innovation velocity across the UK retail banking market.

United Kingdom Retail Banking Industry Leaders

Lloyds Banking Group PLC

Barclays Bank UK PLC

HSBC UK Bank plc

NatWest Group PLC

Santander UK PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Bank of England lowered its policy rate to 4.25%, trimming mortgage costs and prompting fresh fixed-rate offers below 4%.

- April 2025: Barclays intensified private-bank client acquisition using digital wealth tools for high-net-worth individuals.

- April 2025: Revolut highlighted strong Irish growth and flagged new cross-border product launches.

- February 2025: The United Kingdom Finance projected a modest mortgage-lending recovery following base-rate cuts and stable arrears.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom retail banking market as all fee and interest income generated from current and savings accounts, unsecured personal lending, mortgages, payment cards, and related digital-banking services offered to individuals and very small enterprises. Products aimed at corporates, investment banking desks, and capital-markets activities stay outside this scope.

Scope exclusion: corporate and wholesale banking revenues are not counted.

Segmentation Overview

- By Product

- Transactional Accounts

- Savings Accounts

- Debit Cards

- Credit Cards

- Loans

- Other Products

- By Channel

- Online Banking

- Offline Banking

- By Customer Age Group

- 18-28 Years

- 29-44 Years

- 45-59 Years

- 60 Years and Above

- By Bank Type

- National Banks

- Regional Banks

- Neobanks & Others

Detailed Research Methodology and Data Validation

Primary Research

To validate desk findings, we interviewed branch managers, digital-only executives, consumer finance academics, and fintech associations across London, Birmingham, Manchester, and Edinburgh. Conversations clarified pricing spreads, neobank account churn, and channel cost curves, enabling our team to reconcile modeled margins with on-ground realities.

Desk Research

Mordor analysts began with publicly available tier-1 datasets such as Bank of England monetary statistics, FCA strategic reviews, UK Finance mortgage and card volumes, the Office for National Statistics household income series, and IMF macro indicators. Regulatory filings, investor presentations, and reputable trade journals helped sharpen product split ratios, while paid tools, D&B Hoovers for bank financials and Dow Jones Factiva for press flow, supplied timely corporate moves. These sources, together with other government releases and association papers consulted but not listed here, built the factual base.

Market-Sizing & Forecasting

A top-down construct starts with Bank of England deposit and loan stock, reconstructs fee pools from payment-volume estimates, and then aligns with FCA household penetration data. Select bottom-up checks, sampled bank financials and typical APR×volume tests, re-anchor totals. Key model drivers include personal deposit growth, mortgage originations, average net interest margin, digital-bank adoption, real GDP, and policy rate trajectories. Multivariate regression projects each driver, after which scenario analysis adjusts for regulatory or rate shocks; gaps in bottom-up inputs are bridged with regional peer benchmarks or prudent elasticity ranges.

Data Validation & Update Cycle

Outputs pass variance scans against historical trends and peer ratios before a senior analyst reviews anomalies. Reports refresh once a year, with interim patches if material events, rate resets or major M&A, shift the baseline. A final pre-release sweep ensures clients receive the latest vetted view.

Why Mordor's UK Retail Banking Baseline Inspires Confidence

Published figures often diverge because firms mix corporate banking, apply divergent rate paths, or lock forecasts to outdated exchange rates. By ring-fencing strictly retail income streams and refreshing assumptions each quarter, Mordor presents a decision-ready midpoint, whereas others may overstate growth by folding in investment services or understate it through conservative digital-adoption curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 80.1 B (2025) | Mordor Intelligence | - |

| USD 91.0 B (2024) | Global Consultancy A | Includes wealth-management and SME cash-management fees |

| USD 71.1 B (2024) | Industry Association B | Uses narrower product list, omits credit-card interchange |

| USD 71.0 B (2024) | Regional Consultancy C | Applies constant 2023 FX rate and excludes digital-only banks |

Taken together, the comparison shows that when scope, FX, and product granularity are harmonized, Mordor's disciplined bottom-up checks atop a transparent top-down spine deliver the balanced, reproducible baseline that stakeholders can trust.

Key Questions Answered in the Report

What is the projected size of the United Kingdom retail banking market by 2030?

The UK retail banking market size is forecast to reach USD 100.5 billion by 2030, supported by a 4.66% CAGR.

Which product line currently leads revenue generation?

Loans dominate, holding 31.2% of United Kingdom retail banking market share in 2024, with mortgages providing the largest individual contribution.

How fast are neobanks growing in the United Kingdom?

Neobanks and other digital challengers are expected to expand at about 9.1% per year between 2025 and 2030, outpacing traditional banks.

Why are open-banking APIs important for market competition?

Mandatory APIs reduce account-switching time from weeks to minutes, increasing customer mobility and forcing providers to compete on service quality.

What impact do interchange-fee caps have on banks?

Caps lower card-fee income, removing roughly GBP 480 million annually and pressuring banks to focus on interest-bearing balances and subscription fees.

How are ESG considerations shaping new banking products?

Under the UK Green Finance Strategy, ESG-linked deposits and loans tie pricing to sustainability metrics, attracting savers who prioritize environmental impact while reinforcing brand trust.