UK Residential Vacuum Cleaner Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

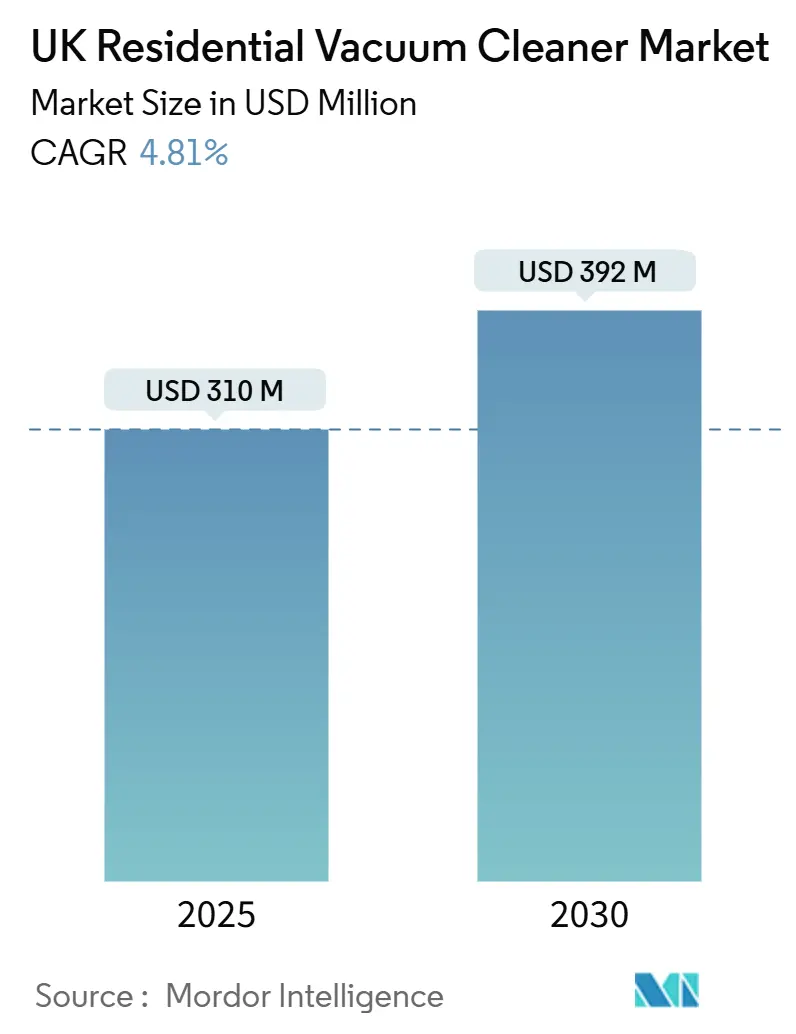

| Market Size (2025) | USD 310 Million |

| Market Size (2030) | USD 392 Million |

| Growth Rate (2025 - 2030) | 4.81% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UK Residential Vacuum Cleaner Market Analysis by Mordor Intelligence

The UK residential vacuum cleaners market is valued at USD 310 million in 2025 and is forecast to reach USD 392 million by 2030, advancing at a 4.81% CAGR. Demand continues to pivot toward cordless stick and robotic units as urban households prioritize convenience, run-time, and smart-home integration. Energy-efficiency labelling, rising electricity costs, and sustained post-pandemic hygiene concerns reinforce replacement cycles, while regulatory clarity on CE-mark recognition reduces time-to-market for new launches.[1]Department for Business and Trade, “UK Government Extends CE Marking Recognition,” gov.uk Established players such as Dyson and SharkNinja lead a rapid innovation race, yet both contend with component cost inflation and Brexit-linked supply-chain friction. Online retail is scaling fastest, reshaping shopper journeys and giving brands direct data feedback loops, although multi-brand stores still dominate high-involvement purchases. Competitive intensity is therefore high, but incremental value growth flows from premium features, retailer-exclusive editions, and eco-design credentials.

Key Report Takeaways

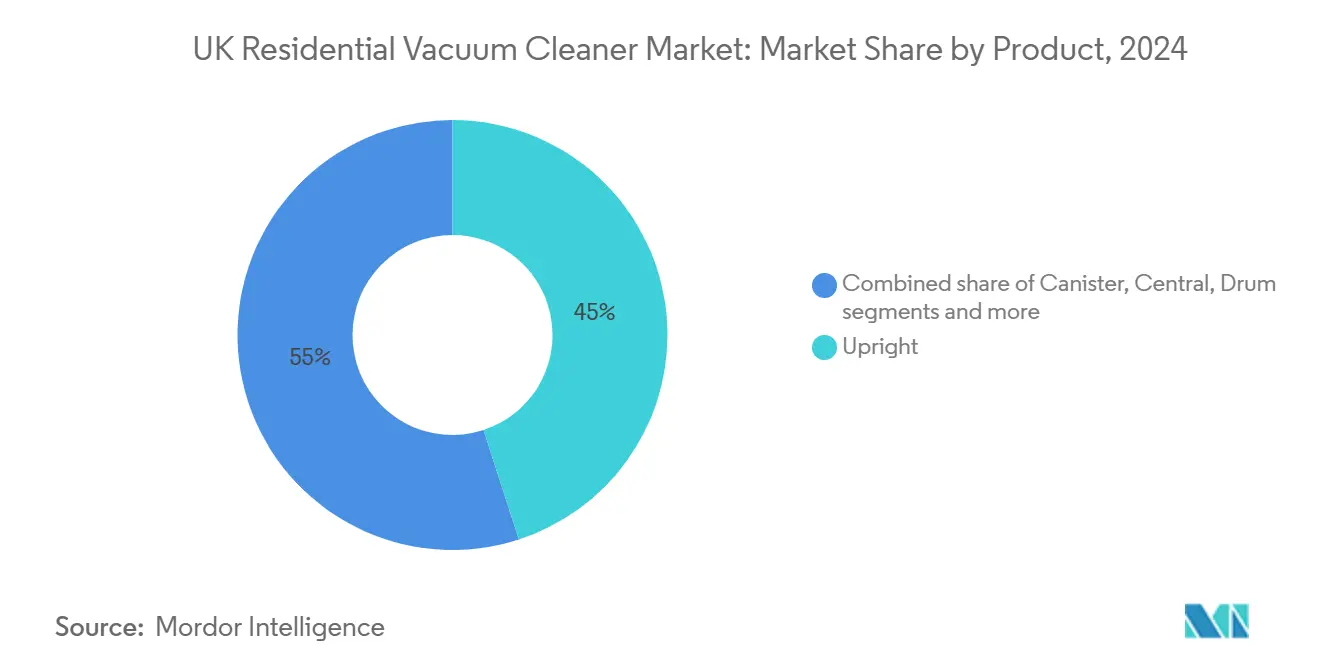

- By product type, upright models led with 45% of the UK residential vacuum cleaners market share in 2024, while robotic units are projected to grow at a 6.3% CAGR through 2030.

- By cord type, corded vacuums accounted for 58% share of the UK residential vacuum cleaners market size in 2024; the cordless segment is expanding at 5.8% CAGR between 2025-2030.

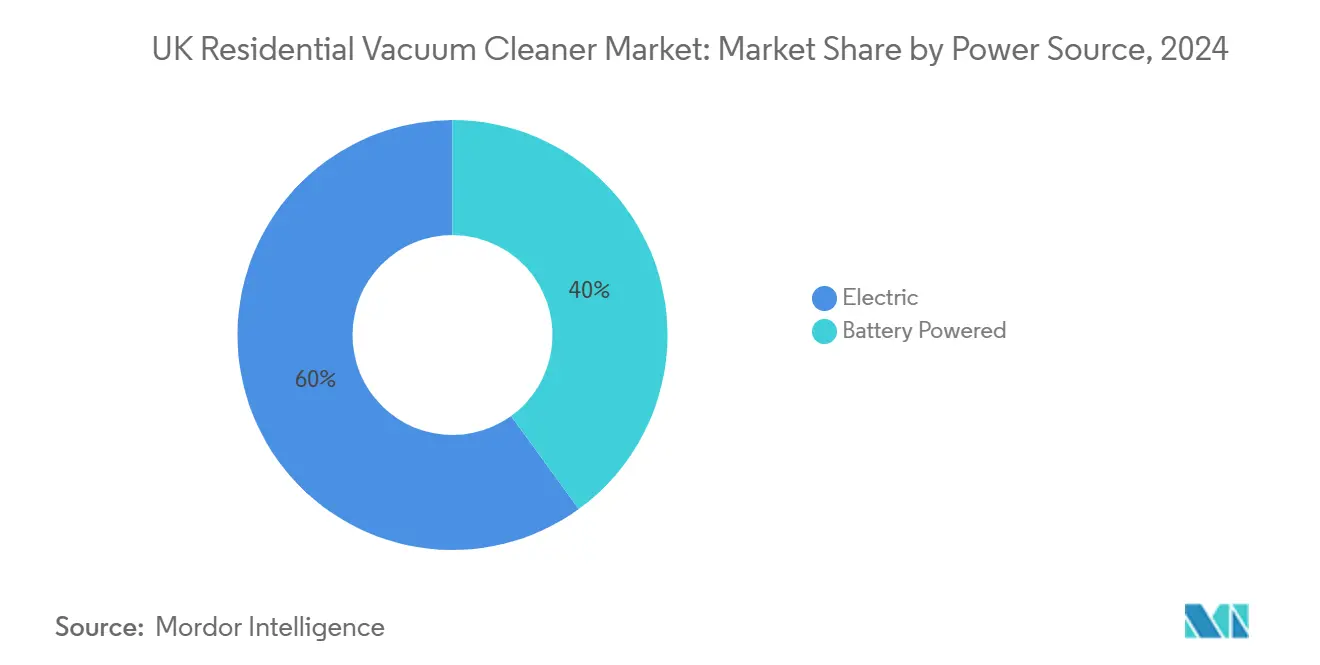

- By power source, electric-powered units held 60% share of the UK residential vacuum cleaners market size in 2024; battery-powered models are set to grow at 5.6% CAGR to 2030.

- By distribution, multi-brand stores controlled 40% revenue share in 2024, while online channels recorded the highest forecast CAGR at 6.0% through 2030.

- By geography, England commanded 80% of the UK residential vacuum cleaners market size in 2024; Northern Ireland is the fastest-growing region at 5.2% CAGR to 2030.

UK Residential Vacuum Cleaner Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of cordless vacuums | +2.4% | Urban centers across England | Medium term (2–4 years) |

| Energy-efficiency labelling | +1.9% | UK-wide | Short term (≤2 years) |

| Heightened hygiene focus post-COVID | +1.4% | Densely populated cities | Short term (≤2 years) |

| Smart-home penetration | +1.8% | London and other tech hubs | Medium term (2–4 years) |

| Retailer-exclusive premium launches | +0.9% | High-income areas | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cordless Stick & Upright Vacuums across UK Households

Cord-free technology is reshaping household cleaning, evidenced by a 5.8% CAGR projection for cordless units through 2030. Longer runtimes, lighter chassis, and one-click emptying have unlocked genuine room-to-room mobility, pushing premium price points higher and supporting margin growth. SharkNinja’s PowerDetect line exemplifies the appeal, offering up to 70 minutes of operation and self-empty docks that satisfy larger homes without mid-session charging. Brands are therefore monetizing convenience even as real wages face pressure, signalling consumers’ readiness to pay for tangible daily time savings and ergonomic gains.

Energy-Efficiency Labelling (Ecodesign) Fueling Replacement Demand

Energy-efficiency rules have accelerated the UK vacuum cleaner replacement cycle, sustaining sales momentum even after Brexit. EU Ecodesign standards lifted average vacuum performance while cutting wattage, and their legacy continues to shape buyer expectations despite the country’s regulatory independence.[2]European Union, “Ecodesign Directive: Energy Labeling for Vacuum Cleaners,” europa.eu Shoppers now scan energy labels as closely as price tags, a habit reinforced by steep electricity bills. Manufacturers are responding with adaptive-suction models that trim power draw without sacrificing pickup. Electrolux’s 800 Series illustrates the shift: its smart modes cut consumption by up to 52% on corded units and 47% on cordless versions, showing how efficiency can coexist with premium features.[3]Electrolux Group, “Electrolux Launches 800 Series with Recycled Plastics,” electroluxgroup.com Rising utility costs mean operating expense has become a headline spec, making high-rated models more compelling than ever for UK households.

Heightened Hygiene Focus Post-COVID Lifting Multi-Surface Sales

British households now equate vacuuming with health protection. HEPA-sealed systems capable of trapping allergens and viruses have become a baseline expectation, elevating formerly niche filtration upgrades into mainstream SKUs. Multi-surface heads that transition between carpet and hard flooring without manual swapping satisfy varied post-renovation floor plans. Brands that quantify particle removal efficacy and partner with allergy foundations achieve persuasive differentiation.

Smart-Home Penetration Accelerating App-Connected Robots

Smart-phone scheduling, room mapping, and voice-assistant links are redefining robotic vacuums, giving the segment an industry-leading 6.3% CAGR outlook. Consumers pay a clear premium because hands-free upkeep delivers measurable lifestyle convenience. Wi-Fi diagnostics also allow brands to push firmware updates and subscription consumables, tilting revenue toward recurring streams.

Retailer-Exclusive Premium Launches Boosting Value Growth

Co-developed colourways, accessory bundles, and limited editions create scarcity and discourage direct price comparison, keeping promotional discounting in check. Retailers gain margin-accretive traffic drivers, while manufacturers secure controlled merchandising and rapid sell-through data. These tactical collaborations, therefore, anchor premium ASPs even in a price-sensitive retail climate.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity amid cost-of-living squeeze | -2.4% | Low-income regions nationwide | Medium term (2–4 years) |

| Brexit-linked component duties | -1.9% | Manufacturers sourcing from the EU | Short term (≤2 years) |

| Substitution by steam-mops & hard-floor appliances | -1.4% | Urban areas with hard flooring | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity Amid Cost-of-Living Squeeze Dampening Premium Uptake

Household budgets are under strain, prompting value-driven shoppers to delay purchases above GBP 300 (USD 377) or trade down to mid-tier lines. Brands respond with “good-better-best” ladders that re-package core innovations—digital motors or self-clean brushes—at reduced specifications to defend volume. Budget SKUs from private labels further intensify price comparisons, testing the resilience of established premium segments.

Brexit-Linked Component Duties Disrupting Inventory Flow

Divergent customs checks and rules-of-origin paperwork have raised inbound costs for motors, plastics, and PCB assemblies. Some producers have shifted partial assembly to the UK to avoid repeated border crossings, yet short-term stock buffering ties up working capital and compresses margins. While the government’s indefinite CE-mark recognition simplifies regulatory filings, logistics friction persists until supply chains fully reroute.

Segment Analysis

By Product: Uprights Hold Leadership as Robots Surge

Upright units captured 45% UK residential vacuum cleaners market share in 2024, aided by strong brand recognition and perceived deep-cleaning power. Their dominance is slowly eroding, however, as robots blitz marketing channels with 6.3% CAGR momentum and demonstrably hands-free operation. The UK residential vacuum cleaners market for robotic models is buoyed by dual vacuum-mop hybrids and self-empty bases that extend user disengagement intervals. Canister designs retain a loyal niche among multi-surface households seeking maneuverability under furniture, while wet-and-dry machines cater to garage and renovation clean-ups, underscoring the breadth of cleaning scenarios manufacturers must address.

Sustained R&D around LiDAR mapping, AI obstacle avoidance, and edge-to-edge suction widens functional gaps between robotic generations. Premium robots now promise dirt storage for up to 60 days, positioning themselves as semi-autonomous home maintenance appliances rather than traditional vacuums. Meanwhile, uprights evolve through ergonomic articulating joints and allergen-sealed dust bins to preserve their relevance, often bundling extra stair tools and anti-hair-wrap rollers for pet owners.

Note: Segment shares of all individual segments are available upon report purchase

By Cord Type: Cordless Freedom Commands Premium

Corded models retained 58% of UK residential vacuum cleaners market share in 2024 because they cost less up front and run continuously without battery worries. Yet the cordless segment is racing ahead at a 5.8% CAGR through 2030, signaling a broad consumer shift toward grab-and-go cleaning. The pattern is strongest in urban flats and among younger buyers, who favor lighter bodies and instant start-up over peak motor wattage. Premium cordless units now post run-times near 70 minutes and feature self-empty bases, as seen in SharkNinja’s PowerDetect line. Even so, average cordless prices still sit two to three times higher than equivalent corded SKUs, underlining the value growth they deliver to brands.

This premium gap, while lucrative, also heightens exposure to inflation-linked belt-tightening as shoppers evaluate convenience versus cost. Manufacturers respond by offering modular battery packs, quick-charge cradles, and tiered feature sets that let price-sensitive households step into cordless ownership. Marketing messages now emphasize “total clean time per charge” and “auto power optimization” rather than raw wattage, aligning with evolving purchase criteria. As a result, the UK residential vacuum cleaners market size for cordless models is on track to capture a larger slice of future revenues, even if corded units keep a foothold among budget-driven families seeking uninterrupted runtime.

By Power Source: Battery Innovation Redefines Performance Metrics

Electric mains units dominate in sheer unit volume, yet battery-powered designs rewrite performance perceptions through high-torque digital motors synchronized with smart load-sensing algorithms. The UK residential vacuum cleaners market size for battery-powered formats is on track to expand at 5.6% CAGR, capturing incremental share as run-times climb and watt-hour price declines accelerate. Research teams allocate substantial resources to thermal management, cell chemistry, and rapid-charge circuitry, knowing that runtime ratings headline marketing copy and heavily influence conversion.

Environmental regulations that promote energy conservation compound pressure on corded watts, nudging consumers toward variable-speed, energy-aware battery models that self-throttle suction when debris sensors read low dust levels. This shift creates a virtuous cycle: greater demand for funds further battery R&D, which in turn unlocks lighter designs and longer autonomy.

By Distribution Channel: Online Acceleration Reshaping Retail Landscape

Multi-brand chains still shepherd 40% of 2024 sales, providing hands-on demonstrations, impulse accessory bundling, and immediate take-home gratification. Nevertheless, pure-play e-commerce and direct-to-consumer storefronts grow at 6.0% CAGR, fostering price transparency and doorstep return policies that de-risk high-ticket online purchasing. The pandemic-driven boom in click-and-collect entrenched omnichannel buyer journeys, where shoppers research rankings and unboxing videos online before validating suction feel in store.

Premium brands leverage flagship concept stores to deliver theatrical product demos and explain subscription filter programs, but scale distribution nationwide via marketplace storefronts. Online share, therefore, expands fastest in rural Scotland, Wales, and parts of Northern Ireland, where physical range is sparse, underscoring the importance of last-mile logistics partnerships and responsive chat support.

Geography Analysis

England underpins 80% of the UK residential vacuum cleaners market, reflecting both population weight and higher disposable incomes. London and the broader Southeast set style cues: early adoption of robotic and app-linked units cascades outward through social media and retailer adjacency. Retail clusters in Manchester, Birmingham, and Leeds also function as showcase hubs, giving manufacturers critical floor space to demonstrate filtration performance and self-cleaning docks.

Northern Ireland represents the highest growth trajectory at a 5.2% CAGR through 2030. Robust housing completions, cross-border value shopping, and a younger demographic amplify demand for mid-priced cordless sticks that double as car vacuums. Compact geography enhances last-mile delivery economics, allowing online pure-plays to offer next-day service even in semi-rural postcodes.

Scotland’s market leans toward models with hospital-grade HEPA filtration, a response to long indoor winters and associated air-quality awareness. Central Belt cities such as Glasgow embrace cordless convenience, whereas Highlands consumers favor durability and large debris paths suited to mixed flooring in detached homes. Wales shows a tilt toward robust wet-and-dry and all-surface machines that contend with mud tracked in from outdoor lifestyles. Both territories increasingly rely on e-commerce to overcome limited store density, prodding brands to refine region-specific search advertising and flexible delivery slots.

Competitive Landscape

The UK residential vacuum cleaners market sits at a moderate concentration point where two leaders—Dyson and SharkNinja—absorb significant mindshare yet leave room for challengers. Dyson’s direct-sales strategy spotlights aerodynamic engineering and digital motor IP, sustaining premium status and high brand loyalty. SharkNinja counters with rapid SKU refreshes, aggressive media spend, and wide multi-channel availability, achieving double-digit volume gains over the last two fiscal years.

Legacy players Hoover Candy and Vax leverage heritage cues and value-for-money positioning, while Miele capitalizes on German engineering credibility and extended product lifespans. Component inflation and Brexit-induced customs complexity spur near-shoring evaluations; Gtech has already repatriated selected assembly lines to the West Midlands to shorten lead times and safeguard quality.

Strategic plays span cross-category expansions into air purifiers and floor-care consumables, bundling HEPA filters and scent pods into subscription replenishment models that smooth revenue. Co-marketing with smart-home platforms enables vacuum brands to ride broader home-automation adoption waves. The competitive picture remains fluid, yet players that balance product novelty with price segmentation and sustainable material commitments are best placed to secure share.

UK Residential Vacuum Cleaner Industry Leaders

-

Dyson Ltd.

-

SharkNinja

-

Operating LLC Vax Ltd. (Techtronic Industries)

-

Hoover Candy Group S.r.l.

-

Miele & Cie. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Aviva research shows UK homes are experiencing a gadget boom with robot vacuums leading smart cleaning adoption

- March 2025: Kärcher unveiled a sustainable dry-vacuum range using up to 60% recycled plastic and HEPA-14 filtration, available UK-wide from summer 2025

- March 2025: Electrolux launched 800 Bagged and 800 Cordless cleaners made with up to 75% recycled plastic and energy-saving smart modes

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the United Kingdom residential vacuum cleaner market as the annual value of new, electrically powered devices bought by households to remove dust and debris from indoor floors, carpets, upholstery, and similar surfaces. The study covers upright, canister, drum, central, wet-and-dry, stick, cordless, and robotic variants sold through all retail and direct-to-consumer channels.

Scope exclusion: appliances designed for commercial, industrial, or professional janitorial use are not counted.

Segmentation Overview

- By Product

- Upright

- Canister

- Central

- Drum

- Wet and Dry

- Robotic

- By Cord Type

- Corded

- Cordless

- By Power Source

- Battery Powered

- Electric

- By Distribution Channel

- Multi-brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- England

- Scotland

- Wales

- Northern Ireland

Detailed Research Methodology and Data Validation

Primary Research

Several semi-structured interviews with product managers at appliance brands, large electrical retailers, and e-commerce category buyers across England, Scotland, Wales, and Northern Ireland allowed us to validate household replacement cycles, promotional ASP swings, and the true share of cordless stock keeping units. Surveys of recent buyers clarified usage frequency and willingness to pay for robotic models, sharpening elasticity assumptions.

Desk Research

We began by mapping product flow with open datasets such as the U.K. Office for National Statistics retail sales index, HMRC import-export tariff code 8508 shipment values, Eurostat PRODCOM 275121 data, and energy-label registrations held by the U.K. Office for Product Safety. Company 10-K filings and investor decks, trade bodies like the British Home Enhancement Trade Association, and consumer-electronics press releases helped us benchmark average selling prices and technology shifts (for example, rapid gains for cordless stick units). Subscription tools that Mordor analysts access, D&B Hoovers for company revenue splits and Dow Jones Factiva for deal/launch news, filled additional gaps. The secondary list here is illustrative; many more sources fed the evidence base.

Market-Sizing & Forecasting

A top-down model starts with household count, mapped to penetration of working vacuum units and annual replacement ratios; import-production-stock balances from customs and ONS reconcile physical volume. Resulting unit totals are multiplied by weighted ASP ladders that reflect mix shifts toward cordless and robotic devices. Supplier roll-ups and sampled online price tracking supply a bottom-up reasonableness check before totals are locked. Key variables modeled include new dwelling completions, disposable income per capita, e-commerce share of durable goods, robotic unit price deflation, and lithium-ion battery cost curves. Forecasts to 2030 use multivariate regression with scenario analysis layered for macro-economic swings; coefficients are fine-tuned with expert consensus gathered in our interviews. Gaps where retailer stocking data are thin are bridged with three-year moving averages.

Data Validation & Update Cycle

Outputs undergo variance checks against historic ONS retail volumes and HMRC trade flows. Any anomaly above a 5% threshold triggers analyst re-work and a second-level review. Reports refresh every twelve months, with mid-cycle updates when major regulatory or supply-chain events occur; a final pre-publication pass ensures users receive the latest view.

Why Mordor's UK Residential Vacuum Cleaner Baseline Commands Reliability

Published values differ because publishers pick different scopes, pricing bases, and refresh rhythms.

Key gap drivers here are: several studies bundle commercial units, some quote sell-in factory revenue rather than household spend, and many uplift historic data with uniform growth factors without rechecking ASP erosion from promotional pricing. Mordor anchors numbers to household-only demand, current retail prices, and an annually rebuilt model.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 310 M (2025) | Mordor Intelligence | - |

| USD 1,003 M (2024) | Regional Consultancy A | Includes commercial sales and service robots; factory-gate pricing |

| USD 862 M (2024) | Trade Journal B | Uses customs values only; omits domestic production and retail mark-ups |

The comparison shows how widening scope and differing price bases inflate totals. By aligning strictly to household demand, triangulating both volume and value, and refreshing inputs yearly, our baseline offers decision-makers a balanced, traceable figure they can plan against with confidence.

Key Questions Answered in the Report

What is the current size of the UK residential vacuum cleaners market?

The market is valued at USD 310 million in 2025 and is projected to reach USD 392 million by 2030.

Which product segment is growing fastest?

Robotic vacuum cleaners are expanding at a 6.3% CAGR through 2030, outpacing all other product formats.

How important is the cordless segment?

Cordless models are forecast to grow at 5.8% CAGR, steadily eroding corded share as battery technology improves.

Which region in the UK is seeing the quickest market growth?

Northern Ireland leads with a projected 5.2% CAGR between 2025 and 2030.

How are rising living costs affecting vacuum cleaner sales?

Budget pressures are driving some consumers to trade down, but premium brands are countering through tiered product lines and exclusive retailer collaborations.

What role do energy-efficiency labels play in purchase decisions?

High visibility of A-class labels continues to spur replacement demand as households seek to lower electricity bills, supporting a positive sales cycle.

Page last updated on: