UK Dog Food Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 3.68 Billion |

| Market Size (2030) | USD 4.81 Billion |

| Growth Rate (2025 - 2030) | 5.48% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UK Dog Food Market Analysis by Mordor Intelligence

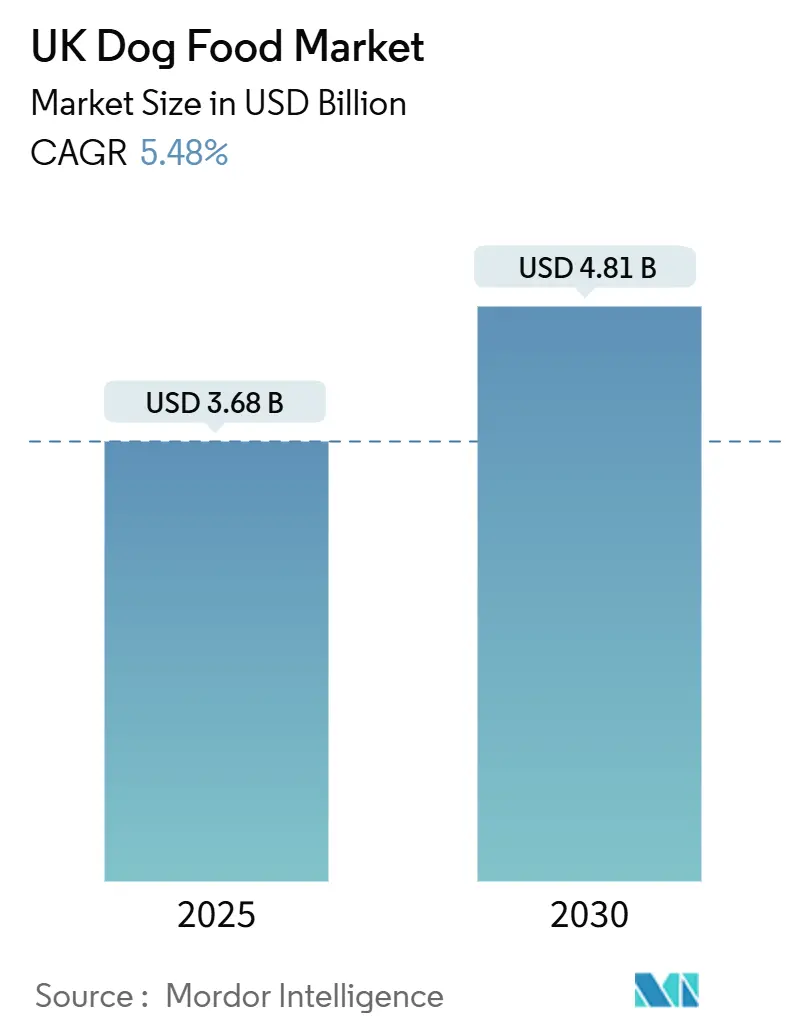

The UK dog food market size stood at USD 3.68 billion in 2025 and is forecast to reach USD 4.81 billion by 2030, advancing at a 5.48% CAGR over 2025-2030. Robust demand, continued premiumization, and rising e-commerce penetration sustain growth despite inflation-led trading-down behavior. Supply-chain adjustments after Brexit elevate input costs, yet regulatory clarity around four approved insect species and novel packaging innovations offset some cost pressure. Leading manufacturers deploy artificial-intelligence tools, subscription models, and functional-ingredient R&D to capture share, while retailer own-label offerings intensify price competition. Premium wet formulas, sustainable proteins, and portion-controlled SKUs aimed at small breeds represent the most dynamic innovation pockets.

Key Report Takeaways

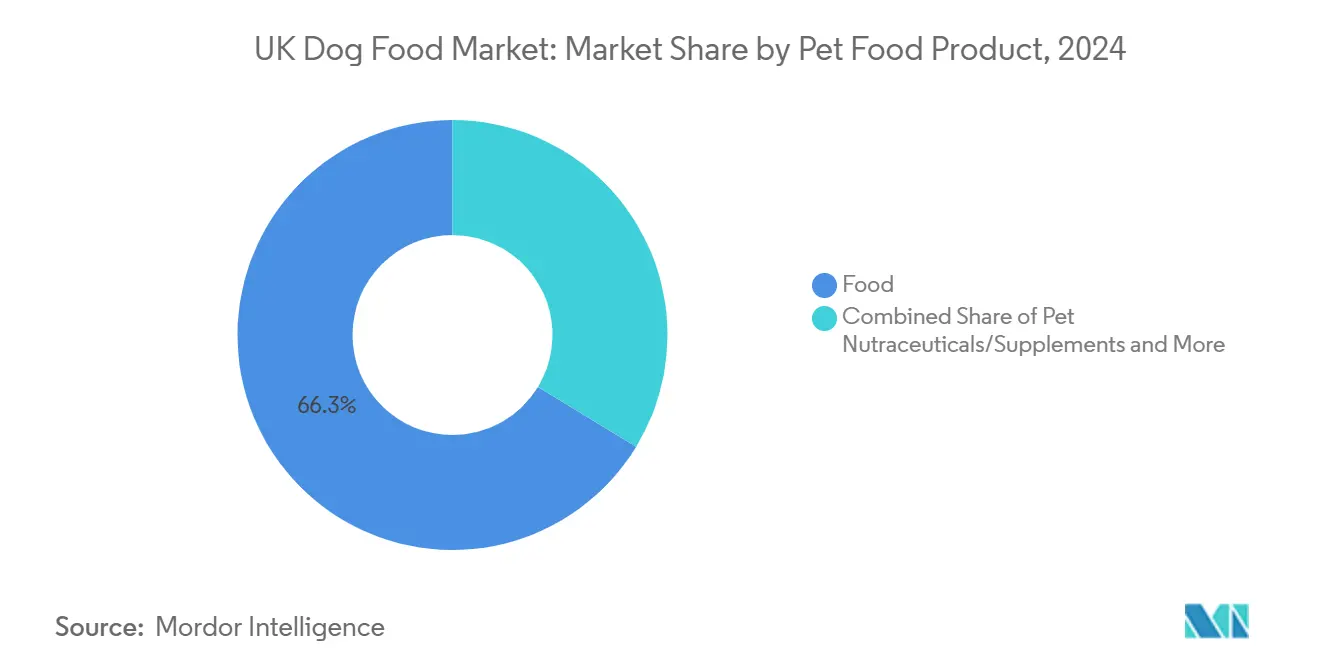

- By pet food product, food captured 66.3% of the UK dog food market share in 2024, while pet nutraceuticals and supplements are poised to post a 9.7% CAGR through 2030.

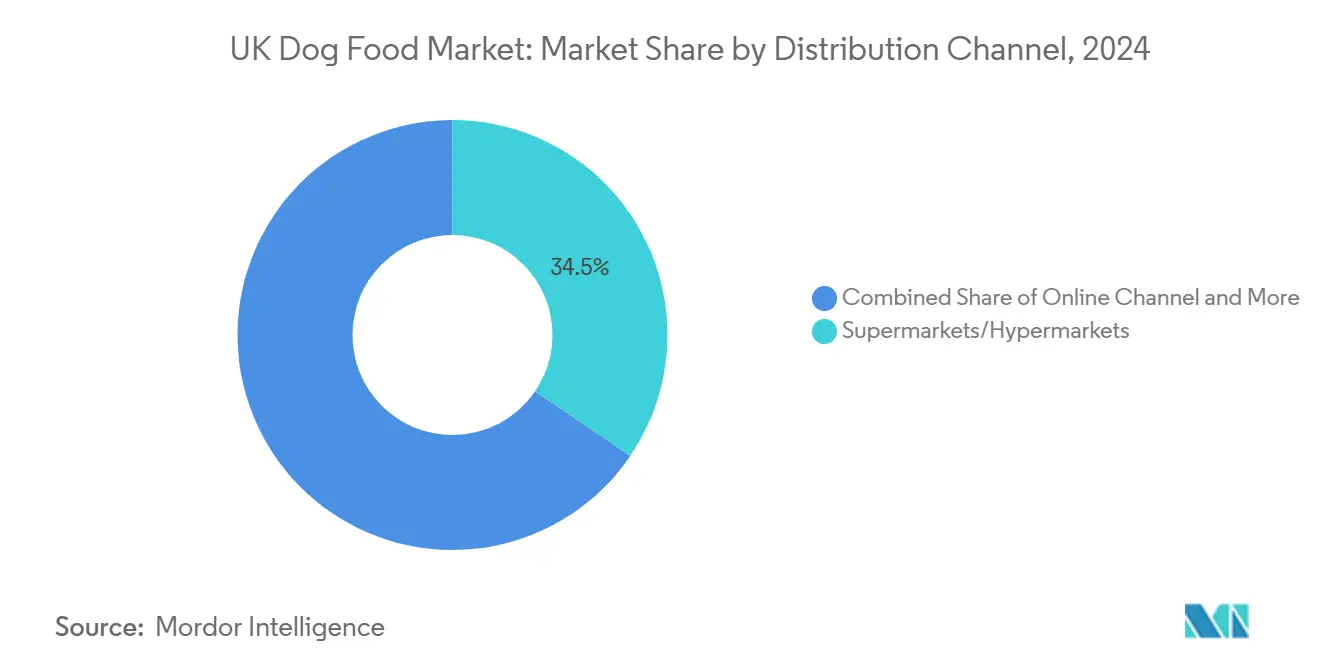

- By distribution channel, supermarkets and hypermarkets commanded 34.5% of sales in 2024, although the online channel is projected to expand at a 7.7% CAGR to 2030.

- The UK dog food market exhibits moderate fragmentation, with the top companies, including Mars, Incorporated, Nestle S.A. (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), Schell & Kampeter, Inc. (Diamond Pet Foods), and Farmina Pet Foods, accounting for 41.7% of market share in 2024.

UK Dog Food Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanization and premiumization | +1.8% | UK-wide, concentrated in affluent urban areas | Medium term (2-4 years) |

| Surge in e-commerce and subscription services | +1.2% | National, with higher penetration in metropolitan regions | Short term (≤ 2 years) |

| Demand for natural and functional ingredients | +0.9% | UK-wide, driven by health-conscious demographics | Medium term (2-4 years) |

| Small-breed boom driving portion-controlled SKUs | +0.6% | Urban centers with space constraints | Long term (≥ 4 years) |

| AI-enabled personalized nutrition platforms | +0.4% | Tech-savvy demographics, early urban adopters | Long term (≥ 4 years) |

| Pet-friendly workplace adoption boosting weekday treat demand | +0.3% | Business districts and progressive employers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pet Humanization and Premiumization

Around 70% of owners now consider their dogs full family members, a mindset that steers purchasing toward grain-free, organic, and breed-specific diets. This behavioral shift drives demand for organic, grain-free, and artisanal formulations, with natural and organic pet food demand increasing 30% according to consumer research[1]Source: Smurfit Kappa, “Pet Care Packaging Market Growth,” smurfitkappa.com. Premium positionings deliver higher margins and encourage experimentation with functional inclusions such as glucosamine for joint support and omega-3 fatty acids for cognitive health. Brands leverage transparent ingredient labels and human-grade sourcing claims to strengthen trust. This sentiment also fuels demand for wet diets that mirror human-ready meal textures and for bespoke meal plans delivered via digital platforms. The shift supports steady above-market growth and underpins the overall UK dog food market.

Surge in E-Commerce and Subscription Services

E-commerce accounted for close to 40% of 2024 UK dog food sales, supported by Amazon UK’s pet category, which generates around GBP 11.5 million (USD 14.4 million) monthly. Subscription specialists such as Butternut Box secured GBP 280 million (USD 350 million) to scale fresh food deliveries, highlighting investor confidence in direct-to-consumer formats. Online channels offer auto-replenishment, micro-targeted promotions, and data-driven product recommendations that increase lifetime customer value. Pandemic-era online shopping habits persist, and rising logistics efficiency enhances service levels even in rural regions.

Demand for Natural and Functional Ingredients

Consumer preferences increasingly favor natural, minimally processed ingredients that deliver specific health benefits beyond basic nutrition. Functional ingredients, including probiotics, omega-3 fatty acids, and specialized proteins, are gaining traction as pet owners seek preventive health solutions addressing common canine conditions. The regulatory landscape supports this trend, with the Food Standards Agency providing clear guidance on four approved insect protein species (yellow mealworm, house cricket, banded cricket, black soldier fly) for sustainable protein alternatives[2]Source: Food Standards Agency, “Imports Intelligence Hub,” food.gov.uk. Brands pair functional claims with veterinary endorsements, linking daily nutrition to preventive health. Clear on-pack communication and clinical-style validation are becoming table stakes as shoppers scrutinize ingredient lists.

Small-Breed Boom Driving Portion-Controlled SKUs

Urban housing constraints propel ownership of compact breeds such as Cockapoos and Cocker Spaniels, the two most viewed breeds on national puppy marketplaces in 2024. These dogs require higher-caloric-density meals in smaller servings. Manufacturers respond with mini-pouch wet diets, small-kibble dry foods, and 100 ml cartons focused on waste reduction. Precise calorie control supports weight management and aligns with veterinarians' preventive care advice.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-led down-trading to own-label | -0.8% | National, particularly affecting price-sensitive segments | Short term (≤ 2 years) |

| Post-Brexit ingredient-sourcing uncertainty | -0.6% | UK-wide, affecting import-dependent manufacturers | Medium term (2-4 years) |

| Veterinary labor shortage limiting prescription diet uptake | -0.4% | National, concentrated in rural and underserved areas | Long term (≥ 4 years) |

| Consumer skepticism over insect-protein claims | -0.2% | UK-wide, varying by demographic segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inflation-Led Down-Trading to Own-Label

Economic pressures compel cost-conscious consumers to migrate from premium branded products to private-label alternatives, constraining revenue growth for established manufacturers. Inflationary impacts on household budgets create price sensitivity that benefits retailers' own-brand offerings, which typically provide cost savings compared to national brands. This trend particularly affects middle-income households, which experience reduced discretionary spending power, forcing difficult choices between high-quality pet nutrition and budget constraints. Supermarket chains leverage this dynamic by expanding their private-label pet food portfolios with improved formulations that narrow the perceived quality gap with branded alternatives while maintaining attractive margins.

Post-Brexit Ingredient-Sourcing Uncertainty

Brexit implementation continues to generate supply chain disruptions and cost increases that challenge UK pet food manufacturers' operational efficiency. Export Health Certificate requirements impose GBP 205 million (USD 256 million) in additional costs since implementation, while Common User Charge fees reach up to GBP 145 (USD 181) per consignment[3]Source: European Parliamentary Research Service, “EU-UK Trade Flows,” europarl.europa.eu. Irregular border inspections and sanitary paperwork lengthen lead times for meat meals and vitamins imported from continental suppliers. Companies diversify toward domestic farms and offshore partners outside the European Union to secure supply.

Segment Analysis

By Pet Food Product: Nutraceuticals Strengthen Premium Evolution

The food segment generated the bulk of revenue, equivalent to 66.3% of the UK dog food market share in 2024. Dry kibble retains volume leadership through affordability and shelf stability, yet wet diets outpace in value due to premium positioning and higher average price per kilogram. The UK dog food market size for pet nutraceuticals and supplements is projected to expand at a 9.7% CAGR, reflecting owner interest in joint, skin, and gut health solutions. Functional powders with glucosamine, fish-oil chews, and probiotic sprinkles illustrate the shift from general wellness to targeted outcomes.

Demand for prescription-grade therapeutic foods remains supply-constrained by veterinary shortages, prompting consumers to shift toward non-prescription SKUs that mimic renal or gastrointestinal profiles. Treats maintain steady growth as owners reward good behavior and reinforce training, with freeze-dried meats and dental chews capturing higher price points. Novel proteins such as insect meal and cultivated chicken position brands at the intersection of sustainability and hypoallergenic benefits within the broader UK dog food market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Acceleration Redefines Reach

Supermarkets and hypermarkets still account for 34.5% of 2024 sales due to nationwide coverage and weekly grocery-trip convenience. Their end-aisle displays and price promotions keep mainstream shoppers engaged. Yet the online channel, projected at 7.7% CAGR, offers frictionless replenishment and access to niche recipes unavailable on physical shelves. The UK dog food market size attributable to digital platforms should surpass by 2030 when including direct-to-consumer subscriptions.

Specialty pet stores carve a premium niche through staff expertise and curated assortments, attracting enthusiasts seeking breed-specific or raw diets. Convenience outlets meet impulse and emergency needs, especially in high-density urban areas where weekday treat demand rises. Omnichannel loyalty programs that blend click-and-collect services with auto-ship discounts emerge as a central strategy for brands chasing share across the evolving UK dog food market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

England houses have a major share of the national dog population, making it the epicenter of consumption and distribution planning. London, Manchester, and Birmingham anchor high-density pockets where premium wet and functional products find early adopters. Scotland, with a high proportion of dogs, tends to favor larger breeds, which in turn increases demand for high-protein and joint-support formulas. Wales' population shows the highest share of brachycephalic breeds, prompting the need for tailored diet opportunities focused on weight control and respiratory support.

Regional logistics concentrate over half of the dogs in South East England, North West England, East England, South West England, and Yorkshire and the Humber. Manufacturers prioritize multi-temperature warehousing near these corridors to maintain freshness for wet and fresh-frozen diets. E-commerce fulfillment centers located along the corridors enable overnight delivery to the majority of households, boosting online repeat purchase rates.

Brexit’s impact varies by region. Scotland and Northern Ireland face regulatory duality when shipping products across the Irish Sea, compelling certain brands to operate mirrored stock-keeping units that satisfy divergent labeling rules. Northern Ireland’s Windsor Framework introduces additional documentary checks, pushing smaller suppliers to partner with third-party logistics providers that specialize in cross-border compliance. Collectively, these factors shape a geography-specific competitive playbook that balances speed, cost, and regulation within the UK dog food market.

Competitive Landscape

The UK dog food market exhibits moderate fragmentation, with the top companies, including Mars, Incorporated, Nestle S.A. (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), Schell & Kampeter, Inc. (Diamond Pet Foods), and Farmina Pet Foods, accounting for 41.7% of market share in 2024. Multinationals Mars Incorporated and Nestlé S.A. (Purina) lead through expansive portfolios and multi-channel distribution; yet, the fragmented ownership of the remaining shares leaves opportunity for agile challengers. Mars Petcare’s USD 1 billion digital investment builds data infrastructure that informs portion algorithms and predictive reorder prompts in 2024. Nestlé S.A. (Purina) upgrades packaging to pyramid-shaped single-serve cups that elevate shelf differentiation and freshness credentials.

Domestic manufacturers GA Pet Food Partners and Inspired Pet Nutrition leverage private-label agreements with major grocers, a strategy that embeds them within the inflation-driven shift toward own-label. In September 2023, Butternut Box’s USD 350 million funding haul signals venture capital's belief in cooked-fresh subscription models that sidestep physical retail. Acquisitions by General Mills and VAFO Group indicate a broader consolidation wave targeting brands with strong natural or functional positioning.

White-space opportunities lie in recyclable mono-material pouches, climate-positive insect proteins, and AI-driven meal customization. Competitive intensity is amplified by the need to display high ingredient transparency and by rising marketing spend on social platforms where pet influencers wield purchasing sway across the UK dog food market.

UK Dog Food Industry Leaders

-

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

-

Mars Incorporated

-

Schell & Kampeter Inc. (Diamond Pet Foods)

-

Farmina Pet Foods

-

Nestle S.A. (Purina)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Mars Petcare is investing USD 1 billion over three years in the development of artificial intelligence and digital platforms, with a focus on personalized nutrition solutions. This strategic initiative positions the company to compete with emerging direct-to-consumer brands leveraging technology for customized dog food formulations.

- April 2024: General Mills completed the acquisition of Edgard and Cooper, a European premium pet food brand, for an undisclosed amount to expand its presence in the natural and sustainable pet food segment, including dog food. The acquisition strengthens General Mills' portfolio with products emphasizing fresh ingredients and environmentally conscious packaging.

- July 2023: Colgate-Palmolive Company (Hill's Pet Nutrition Inc.) introduced its new MSC (Marine Stewardship Council) certified pollock and insect protein products for pets, including dogs with sensitive stomachs and skin lines in United Kingdom. They contain vitamins, omega-3 fatty acids, and antioxidants.

UK Dog Food Market Report Scope

Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets are covered as segments by Pet Food Product. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel.| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft & Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | ||

| Diabetes | ||||

| Digestive Sensitivity | ||||

| Obesity Diets | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary tract disease | ||||

| Other Veterinary Diets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft & Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | |||

| Diabetes | |||||

| Digestive Sensitivity | |||||

| Obesity Diets | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary tract disease | |||||

| Other Veterinary Diets | |||||

| By Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms