United Kingdom Cyber Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 1.75 Million |

| Market Size (2031) | USD 3.08 Million |

| Growth Rate (2026 - 2031) | 12.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Cyber Insurance Market Analysis by Mordor Intelligence

The United Kingdom Cyber Insurance market is expected to grow from USD 1.56 million in 2025 to USD 1.75 million in 2026 and is forecast to reach USD 3.08 million by 2031 at 12.03% CAGR over 2026-2031.

Structural demand arises from mandatory breach-notification rules, the enduring shift to hybrid work, and Lloyd’s globally recognized capacity hub. Heightened ransomware activity, averaging 50% victimization of U.K. firms in 2024, accelerates the adoption of standalone cover. Continuous digitalization among small and micro businesses unlocks a fast-growing segment in the UK cyber insurance market, while premium inflation and tighter sub-limits temper penetration. Reinsurance capacity pressures and systemic-risk uncertainties signal a maturing market moving toward selective underwriting and active-risk management models.

Key Report Takeaways

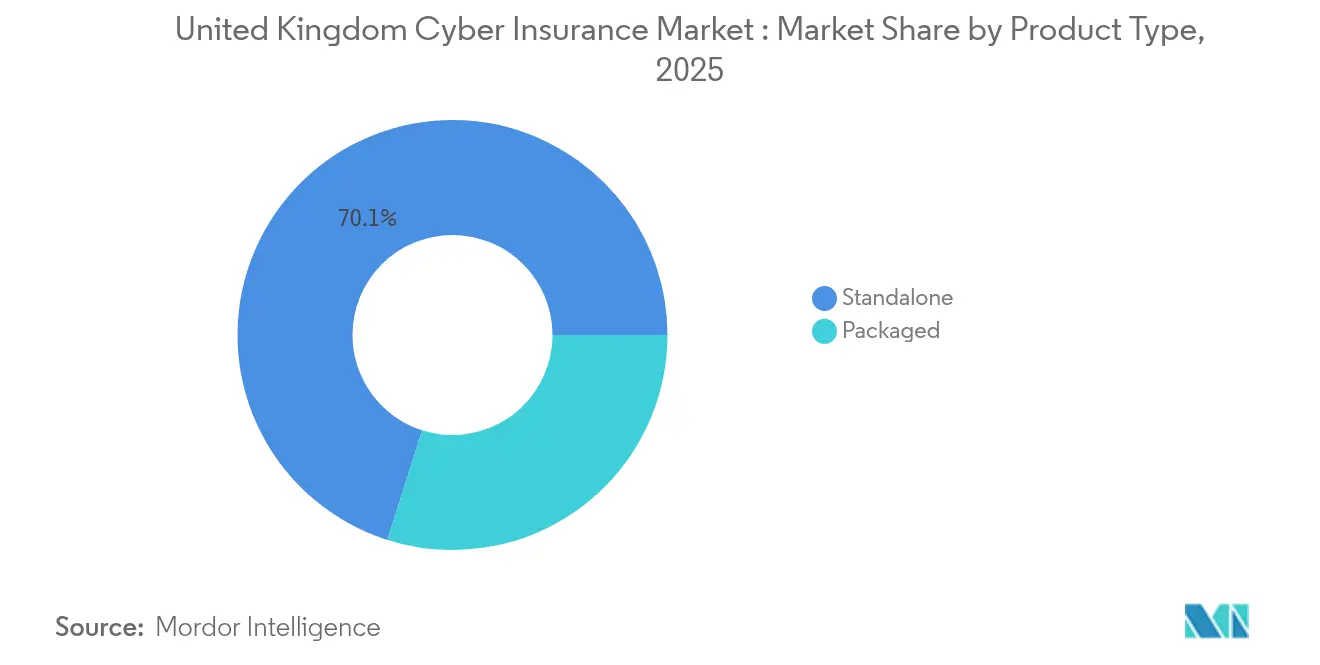

- By product type, standalone policies captured 70.10% of the United Kingdom cyber insurance market share in 2025, whereas packaged extensions trailed significantly.

- By enterprise size, large enterprises controlled 43.00% revenue of 2025 in the UK cyber insurance market; small and micro businesses are forecast to grow at a 13.12% CAGR through 2031.

- By industry vertical, BFSI led with 28.45% share of the United Kingdom cyber insurance market size in 2025; healthcare & life sciences is advancing at a 12.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Cyber Insurance Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating ransomware frequency & severity | +2.8% | United Kingdom-wide | Short term (≤ 2 years) |

| Mandatory GDPR & ICO breach-notification fines | +2.1% | United Kingdom-wide | Medium term (2-4 years) |

| Post-COVID remote-work attack-surface expansion | +1.9% | United Kingdom-wide | Medium term (2-4 years) |

| SME-focused digital broker platforms (embedded) | +1.6% | United Kingdom-wide | Long term (≥ 4 years) |

| United Kingdom government Cyber Essentials scheme uptake | +1.3% | United Kingdom-wide | Medium term (2-4 years) |

| NHS & CNI zero-trust procurement mandates | +1.1% | United Kingdom-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Ransomware Frequency & Severity

Ransomware campaigns have matured into well-financed ecosystems that target both critical infrastructure and mid-market firms. Double- and triple-extortion tactics drive up forensic, legal, and business-interruption costs, pushing average claim values past historical models. Supply-chain attacks, exemplified by MOVEit, expose even security-mature organizations through third-party software dependencies. Insurers now embed continuous-monitoring services and incident-response retainers within policies to shorten dwell time and recover data swiftly. Market capacity favors carriers that can leverage threat-intelligence telemetry to refine pricing in near-real time.

Mandatory GDPR & ICO Breach-Notification Fines

The 72-hour disclosure rule compels firms to formalize incident-response playbooks and purchase higher indemnity limits covering regulatory defense and penalty mitigation. ICO enforcement demonstrates a readiness to impose multi-million-pound fines for insufficient technical controls, especially in healthcare and finance[1]Information Commissioner’s Office, “Guide to the UK GDPR,” ico.org.uk. Insurers differentiate underwriting by mapping policy wording to accountability principles, rewarding certified controls with premium credits. As cross-border data transfers rely on standard contractual clauses, carriers add extensions for legal consultancy and escrow services. Heightened regulatory clarity transforms compliance coverage from a discretionary add-on into a core purchasing driver.

Post-COVID Remote-Work Attack-Surface Expansion

Permanent hybrid-work models fragment security perimeters, replacing intranet-centric defenses with cloud and SaaS reliance. Consumer-grade routers, personal devices, and poorly configured VPNs enlarge entry points for credential stuffing and phishing. Underwriters evaluate endpoint-detection rollouts, MFA adoption rates, and employee training metrics before binding cover. Distributed evidence complicates digital forensics, elongating business-interruption losses that policies must now explicitly cover. Vendors delivering secure-access service edge (SASE) and zero-trust network access integrate with insurers to feed telemetry that supports predictive risk scoring.

SME-Focused Digital Broker Platforms (Embedded Cyber)

Platform ecosystems such as Acturis embed quotation, risk scoring, and policy issuance within accounting or payroll software, lowering purchase friction for resource-constrained SMEs. Real-time APIs collect cyber-hygiene data, patch cadence, port scans, and TLS configurations, which allow dynamic pricing and automatic coverage adjustments. Government research shows only 8% of businesses hold standalone cyber cover, illustrating the latent demand that embedded solutions address. Continuous monitoring services bundled with policies foster a subscription mindset rather than annual renewal, helping reduce churn. Regulatory scrutiny over embedded distribution is prompting clear disclosure and opt-out safeguards to preserve consumer protection.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium inflation & coverage sub-limits | -2.3% | United Kingdom-wide | Short term (≤ 2 years) |

| Limited actuarial loss history for the United Kingdom market | -1.8% | United Kingdom-wide | Medium term (2-4 years) |

| War-exclusion & systemic-risk uncertainty | -1.5% | United Kingdom-wide | Long term (≥ 4 years) |

| Reinsurance capacity tightening (post-MOVEit) | -1.4% | United Kingdom-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Inflation & Coverage Sub-Limits

Annual premium hikes of 15–25% outpace many firms’ risk budgets, compelling buyers to select lower limits or accept higher retentions. Sub-limits on business-interruption, bricking, and reputational harm leave sizable gaps only discovered during claims. SMEs, already confronting tight cash flow, risk-averse selection by exiting the market, and enlarging insurers’ high-risk pools. Rising reinsurance costs flow directly into retail pricing with limited transparency[2]Lloyd’s, “Market Bulletin Y5381,” lloyds.com. This feedback loop threatens sustainable growth unless actuarial certainty improves and alternative risk-transfer instruments emerge.

Limited Actuarial Loss History for the United Kingdom Market

Less than three decades of structured cyber-loss data hampers credible severity curves for AI-driven exploits or nation-state attacks. Disparate reporting standards produce incomplete datasets, underestimating incident frequency and tail-risk exposure. London’s concentration of underwriting talent increases the correlation of modeling assumptions, magnifying systemic error potential. Silent-cyber exposures buried in property or liability forms distort pure-cyber loss ratios. Carriers invest in consortium data lakes and anonymized threat-intel feeds to augment scarcity, but need standardized reporting mandates to accelerate model maturity.

Segment Analysis

By Product Type: Standalone Policies Drive Market Evolution

Standalone offerings accounted for 70.10% of the United Kingdom cyber insurance market share in 2025, underscoring demand for specialized coverage unhindered by generic indemnity caps. The segment is forecast to grow at a 12.78% CAGR, reinforcing its position as the primary engine of the United Kingdom cyber insurance market. Buyers recognize that silent-cyber gaps in commercial-combined packages present unacceptable uncertainty when regulators can impose multimillion-pound fines. Active-insurance models layered atop standalone forms integrate monitoring, threat-intel, and rapid-response retainers, shortening mean-time-to-contain and lowering severity. Packaged add-ons remain relevant for micro-enterprises entering cover for the first time, but their constrained limits and incident-response capabilities curtail adoption as cyber maturity rises.

Standalone carriers leverage proprietary telemetry from policyholder networks to refine pricing and automate endorsements during the policy term. This feedback-rich environment allows mid-term limit increases or ransomware-deductible reductions once risk controls improve. Average premiums span £2,000-£15,000 for SMEs and £50,000-£500,000 for large corporates, reflecting exposure granularity over headline turnover. Technology-vertical endorsements cover source-code escrow, crypto-asset theft, and AI-model poisoning, illustrating the pace of product diversification. The packaged segment may sustain single-digit growth by aligning with embedded-broker platforms targeting long-tail micro-businesses that value simplicity over breadth.

Note: Segment shares of all individual segments available upon report purchase

By Enterprise Size: SME Growth Outpaces Large-Corporate Adoption

Large enterprises held 43.00% of the United Kingdom cyber insurance market size in 2025, owing to regulatory mandates, global footprints, and sophisticated risk-management processes. However, small and micro firms are predicted to post a 13.12% CAGR, adding momentum to overall market expansion. Government surveys show only 43% of businesses carry cyber cover, highlighting substantial headroom for insurers willing to craft affordable, jargon-free propositions. Digital-broker APIs assess patch latency, MFA rollout, and web-app exposure to generate bite-sized premiums that align with constrained budgets. Medium enterprises—often possessing partial in-house security teams—bridge the adoption gap, with 62% holding cover and favoring policies that bundle staff-training vouchers and tabletop-exercise services.

SMEs confront acute human-resource limits that impede incident detection and response, amplifying downtime costs relative to turnover. Embedded cover inserted at point-of-sale within POS, accounting, or cloud-hosting subscriptions mitigates procurement inertia. Large corporate buyers increasingly demand parametric triggers for critical supplier outages and affirmative language for network failure cascades. Underwriters set sub-segment risk budgets, often capping SME aggregate exposure at 25% to contain correlated ransomware shocks. Multi-year policy maturities remain rare, even for blue-chip risks, given the velocity of threat evolution and implications of capital charges.

By Industry Vertical: Healthcare Emerges as Fastest-Growing Sector

BFSI institutions commanded 28.45% of the United Kingdom cyber insurance market share in 2025, reflecting tight Prudential Regulation Authority oversight, PCI-DSS obligations, and extensive digital banking penetration. Healthcare & life-sciences premiums are forecast to expand at a 12.72% CAGR to 2031, driven by electronic patient-record adoption and rising ransomware targeting of hospitals. The United Kingdom cyber insurance market size for healthcare is set to widen as medical device connectivity and telemedicine platforms enlarge attack surfaces. Meanwhile, manufacturing uptake accelerates due to Industrial IoT rollouts that elevate operational-technology risk once shielded from IP-based threats. Public-sector entities show growing interest in cover that aligns with National Cyber Strategy mandates for resilience.

Healthcare buyers demand clauses for patient-safety impacts, regulatory investigation and forensic autopsies across clinical systems. Insurers respond with wording that funds system-validation costs and compensate revenue losses from canceled procedures. BFSI leaders push for an affirmative cloud-outsourcing extension, ensuring claims transparency when third-party service outages interrupt digital banking. Retail & e-commerce firms prioritize payment-card data breaches and distributed-denial-of-service resilience during peak shopping windows. Education institutions seek limits tailored to student-data protection and research IP theft, often layered atop tight public-budget constraints. Insurers’ vertical specialization yields actuarial insights that improve segmentation discipline while curbing accumulation risk.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

London dominates underwriting activity, housing Lloyd’s syndicates that supply both domestic and international capacity, yet regional cities such as Manchester, Birmingham, and Edinburgh exhibit rising penetration catalyzed by fintech and advanced-manufacturing clusters. Scotland’s distinct legal framework and cross-border data flows shape specialized cover wording, while Northern Ireland’s proximity to the Republic introduces dual-jurisdiction compliance. Government levelling-up funds and full-fiber broadband projects shrink the historic North–South digital divide, broadening the United Kingdom cyber insurance market in previously underserved locales.

Critical National Infrastructure sites, from Scottish wind farms to South-East data centers, require coordinated coverage for cascading supply-chain events. Post-Brexit data-adequacy rulings sustain EU–U.K. transfers, enabling standardized policy extensions that remove compliance uncertainty for multi-jurisdictional buyers. Regional broker networks leverage digital quote-bind platforms to reach SMEs in rural England and the Welsh valleys, where traditional face-to-face breaking is scarce. London’s capacity concentration introduces systemic-risk concerns, prompting syndicates to model regional accumulation scenarios for simultaneous ransomware attacks on healthcare trusts.

Edinburgh’s financial services heritage fosters sophisticated captive-insurance structures that purchase cyber reinsurance out of Lloyd’s, while Cardiff technology parks incubate InsurTech MGAs focused on embedded propositions. The Midlands Engine manufacturing corridor elevates operational-technology exposures, incentivizing hybrid covers that blend property-damage and cyber-trigger clauses. Overall, geographic diversification mitigates correlated loss potential, yet the market remains highly interlinked through London’s central capital pool.

Competitive Landscape

UK Cyber Insurance Market concentration is moderate, with the top five players holding major market share in 2024 due to written premiums, leaving ample room for specialist MGAs and InsurTech challengers. Lloyd’s syndicates, Beazley, Hiscox, and Chaucer, benefit from deep historical data, international following lines, and agile wording committees. Traditional multiline insurers such as AIG and Allianz bundle cyber with property or casualty programs for corporate clients seeking single-tower solutions. Coalition, CFC, and Cowbell differentiate through telemetry-driven underwriting, continuous monitoring dashboards, and integrated incident-response retainers[3]CFC, “Cyber Proactive Response Expansion,” cfc.com. Strategic alliances, exemplified by The Hartford’s quota-share with Coalition, combine balance-sheet strength and technology prowess to accelerate growth.

Technology adoption serves as a competitive moat in the UK cyber insurance market: AI-assisted triage slashes claim-handling times, while dark-web reconnaissance informs risk scoring. Capacity partnerships diversify reinsurance sourcing; for instance, Allianz’s multi-year panel supports Coalition’s European expansion, stabilizing loss-ratio volatility. Policy wording innovation addresses emerging exposures such as AI-model poisoning and cloud-vendor outages, enabling carriers to command margin premiums. Rising capital charges for attritional ransomware losses incentivize diversification into parametric and co-insurance structures. M&A activity is poised to intensify as smaller cyber-focused MGAs seek scale or capital partners to navigate reinsurance pressure.

The FCA and PRA embed operational-resilience tests that favor carriers with demonstrable cyber-risk-management frameworks and incident-response ecosystems. Insurers offering proactive vulnerability-scan reports, phishing-simulation tools, and tabletop-exercise facilitation gain stickiness and reduce loss frequency. Broker-driven distribution remains vital at the upper-middle market, though embedded APIs court the micro-enterprise segment. Capacity providers tether renewal appetite to improved MFA rollout and zero-trust adoption, reinforcing virtuous security cycles across insured portfolios. Over the forecast horizon, differentiation will hinge on real-time data feeds, sector-specific endorsement, and multi-layer reinsurance towers that withstand systemic events.

United Kingdom Cyber Insurance Industry Leaders

AIG

Beazley

Hiscox

Allianz

AXA XL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Markel introduced wrap-around cyber coverage for indirect war losses up to USD 5 million per risk, bridging gaps created by mandatory war exclusions in standard wordings.

- May 2025: CFC upgraded its Cyber Proactive Response suite, extending sector-specific wordings for digital health, fintech, and technology firms with AI-incident clauses and revenue-loss cover.

- September 2024: Coalition launched Coalition Re, a data-driven reinsurance intermediary backed by Aspen, offering non-proportional treaties and white-label products for primary insurers.

- August 2024: Coalition entered Germany via Coalition Insurance Solutions GmbH, supported by a multi-year capacity agreement with Allianz Global Corporate & Specialty SE.

United Kingdom Cyber Insurance Market Report Scope

Cyber liability insurance is an insurance policy that provides businesses with a combination of coverage options to help protect the company from data breaches and other cyber security issues. It's not a question of if the organization will suffer a breach but when. Travelers and cyber insurance policyholders can also access tools and resources to manage and mitigate cyber risk. Cyber insurance generally covers your business's liability for a data breach involving sensitive customer information, such as Social Security numbers, credit card numbers, account numbers, driver's license numbers, and health records.

The UK cyber (liability) insurance market is segmented by product type (packages, standalone) and application type (banking & financial services, IT & telecom, healthcare, retail, and other application types).

The report offers market size and forecasts for the UK cyber (liability) insurance market in value (USD) for all the above segments.

| Packaged |

| Standalone |

| Large Enterprises |

| Medium Enterprises |

| Small and Micro Enterprises |

| BFSI |

| IT & Telecom |

| Retail & E-commerce |

| Healthcare & Life Sciences |

| Manufacturing |

| Government & Public Sector |

| Education |

| By Product Type (Value) | Packaged |

| Standalone | |

| By Enterprise Size (Value) | Large Enterprises |

| Medium Enterprises | |

| Small and Micro Enterprises | |

| By Industry Vertical (Value) | BFSI |

| IT & Telecom | |

| Retail & E-commerce | |

| Healthcare & Life Sciences | |

| Manufacturing | |

| Government & Public Sector | |

| Education |

Key Questions Answered in the Report

How large is the United Kingdom cyber insurance market in 2026?

The United Kingdom cyber insurance market size is USD 1.75 million in 2026, with a forecast value of USD 3.08 million by 2031.

What CAGR is expected for the United Kingdom cyber insurance between 2026 and 2031?

The market is projected to expand at a 12.03% CAGR during the forecast period.

Which product type leads the United Kingdom cyber cover uptake?

Standalone policies hold 70.10% share, reflecting buyer preference for comprehensive, dedicated coverage.

Which enterprise segment is growing fastest in the United Kingdom in cyber cover adoption?

Small and micro businesses demonstrate the highest growth at a 13.12% CAGR through 2031.

Which industry vertical is anticipated to be the fastest-growing?

Healthcare & life-sciences premiums are projected to rise at a 12.72% CAGR through 2031.

What is the primary driver behind rising cyber insurance demand?

Escalating ransomware frequency and severity remain the leading catalyst for policy adoption across the United Kingdom.