UK B2B Fixed Connectivity Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

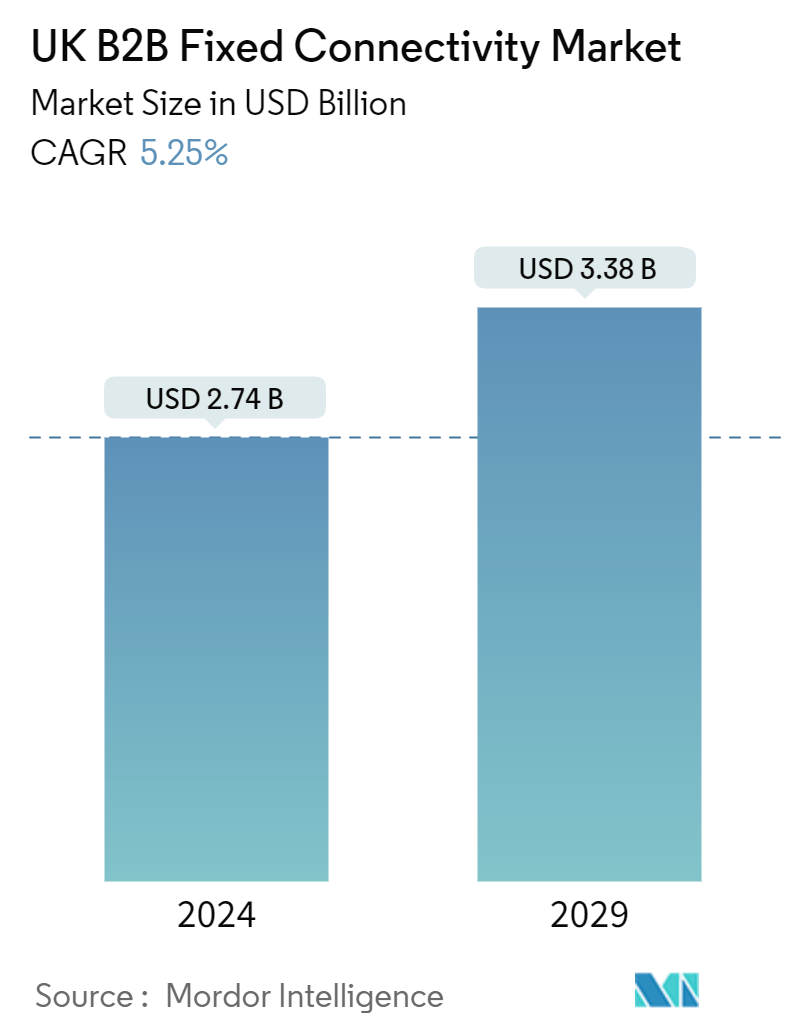

| Market Size (2024) | USD 2.74 Billion |

| Market Size (2029) | USD 3.38 Billion |

| CAGR (2024 - 2029) | 5.25 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

UK B2B Fixed Connectivity Market Analysis

The UK B2B Fixed Connectivity Market size is estimated at USD 2.74 billion in 2024, and is expected to reach USD 3.38 billion by 2029, growing at a CAGR of 5.25% during the forecast period (2024-2029).

A fixed line refers to a cable-based connectivity solution for customers. Fixed line connectivity encompasses all internet connections that rely on a physical line, be it fiber optic or copper. The UK B2B fixed connectivity market is a vital segment of the telecommunications industry, providing essential infrastructure and services that enable businesses to operate efficiently and stay connected in an increasingly digital world.

- Organizations leverage digital transformation to boost customer retention, enhance experiences, and fortify brand reputation via software integration. Such businesses adeptly navigate tech advancements and pivot swiftly in response to industry changes. Notably, the onset of the COVID-19 pandemic catalyzed the digital transformation drive, prompting UK government bodies to hasten their initiatives, with the UK government forming a digital strategy to grow the digital economy - addressing tech sector skills, investment, and infrastructure.

- Fixed line connections are capable of providing high-speed internet. They are scalable and flexible, like ethernet over fiber and ethernet over copper. Therefore, they are suitable for businesses of all sizes and provide cost-effective and high-speed network solutions.

- The work-for-home trend is still strong in the United Kingdom but has now started to fade away slowly. According to the statistics by the Office for National Statistics, as of June 2023, working arrangements among UK workers were: work-from-home all the time at 10%, work-from-home some of the time at 29%, and unable to work-from-home at 39%. With the changes in the work-from-home trend, it is expected that companies in the United Kingdom will have to invest in high-quality fixed connectivity solutions to support increasing on-site workforces.

- The increasing adoption of AI and ML technologies is driving the demand for fixed-line connectivity. The UK government has pinpointed five key technologies for the future: quantum, AI, engineering biology, semiconductors, and future telecoms. Notably, the country is committing GBP 900 million (~USD 1119.40) to develop a state-of-the-art supercomputer, a pivotal move in its broader artificial intelligence strategy, which aims to enable the creation of a homegrown BritGPT. Additionally, the surge in cloud computing, AI/ML, and data center technologies is poised to significantly benefit the market studied.

- High costs and cybersecurity significantly shape the market's growth trajectory. For example, a study by internet service provider Beaming revealed that cybercrime cost the UK economy GBP 30.5 billion (~USD 37.94) last year, impacting 1.5 million businesses. This not only hampers the accessibility and affordability of high-speed connectivity solutions for businesses but also drives up a company's cybersecurity budget, adding pressure to its operational expenses.

- Additionally, downtime and connectivity outages can also have a negative impact on the market. For instance, London-based Vorboss, a provider of direct internet connectivity for businesses, estimates that the UK economy saw a GBP 17.6 billion (~USD 21.89 billion) dip in economic output in the last year due to connectivity disruptions. Following its productivity analysis, Vorboss has urged the UK's communications regulator, Ofcom, to consider implementing an automatic compensation system for businesses facing connectivity downtime. Its study revealed that over half (51%) of businesses with fixed internet contracts encountered service disruptions in the previous year, a number that surged to 60% for businesses in London. Furthermore, nearly one-fifth (19%) of businesses experienced three or more outages, with the number spiking to 28% in London. Although facing potential challenges, the market is poised for improvement in the fixed connectivity industry.

UK B2B Fixed Connectivity Market Trends

Fixed Data is Expected to Grow at a Rapid Pace

- Fixed data includes all dedicated/private line, packet, and circuit-switched access services, which contrasts strongly with the shared nature of standard broadband connections. With fixed data, the user enjoys unimpeded access to the entire bandwidth, eliminating concerns over sluggish speeds or erratic performance. Moreover, dedicated or private lines typically come with a Service Level Agreement (SLA), ensuring a committed quality and performance standard.

- The need for fast and reliable connectivity is rising, with leased line services standing out as a pivotal solution. In 2023, fixed leased line connections dominated the UK business internet market, capturing a share exceeding 39%, a figure that has been consistently climbing, as reported by Connect2, an IT infrastructure firm.

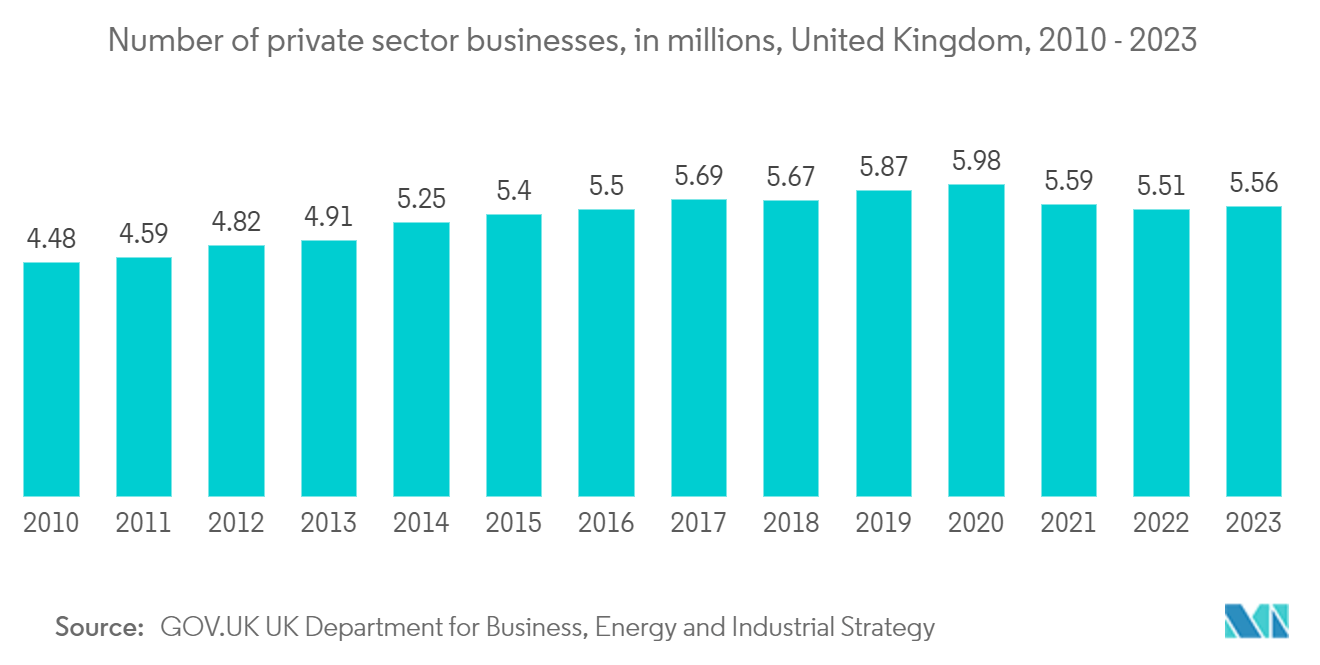

- Companies, corporate offices, and businesses are typical end users of private lines or networks that are part of fixed data services. According to GOV.UK and the UK Department for Business, Energy and Industrial Strategy, in 2023, approximately 5.56 million private businesses were operating in the United Kingdom, a slight increase compared to the previous year. According to the UK Department of Business and Trade, the private sector business population increased by 0.8% (46,000 businesses). The growth in the private business or business sector in the country is expected to drive the demand for fixed data networks.

- Further, the tech industry, including IT, stands as a significant consumer of data, necessitating high-speed internet. As per MOL, a prominent online education and certification platform, the UK tech sector boasts a workforce of more than 1.7 million, contributing a substantial GBP 150 billion(~USD 190 Billion) annually to the nation's economy. With favorable conditions, the UK tech sector has the potential to inject an additional GBP 41.5 billion(~USD 52 Billion) into the economy and generate 678,000 new jobs by 2025. Given these projections, the burgeoning tech and IT sector is poised to be a key driver of the market studied.

- Moreover, a surge in cloud adoption is bolstering the leased line industry in the United Kingdom. Nutanix, a leading name in hybrid multi-cloud computing companies, reports that 84% of UK respondents are embracing a 'cloud smart' approach. This involves deploying applications and workloads across data centers, multiple clouds, and the network edge. In the UK, the adoption of hybrid multi-cloud models is projected to rise from 19% today to 26% in the next three years. Simultaneously, the utilization of multiple public clouds is expected to jump from 11% to 46% within the next one to three years. Businesses in the United Kingdom commonly leverage leased lines for web-based content distribution, cloud applications, voice services, and online backups.

Huge Demand for High-speed Connectivity

- In the United Kingdom, the demand for enhanced connectivity is surging. This surge is primarily fueled by the escalating reliance of both businesses and individuals on the Internet, especially with the proliferation of devices, the advent of the Industrial Internet of Things (IIoT), and ambitious initiatives such as smart cities. As the Internet of Things (IoT) gains prominence, businesses increasingly integrate their devices into the web. This integration spans a variety of systems, from intelligent lighting and security cameras to climate controls, air purifiers, and an array of IoT sensors. Such a network demands high-speed internet, propelling the market under study in the region.

- The UK Department for Science, Innovation, and Technology has allocated GBP 4 million (~USD 4.97 million) to trial smart technology in towns and cities to enhance local connectivity. As part of a larger GBP 1.3 million (~USD 1.61 million) government pilot, various UK towns and cities are set to roll out smart street lamps. These lamps, equipped with next-gen digital technology, will provide EV charging and bolster wireless connectivity. Specifically, six key areas, including Cambridgeshire County Council, Tees Valley Combined Authority, Royal Borough of Kingston upon Thames, Westminster City Council, Oxfordshire County Council, and North Ayrshire Council, are spearheading the testing of these innovative street lamps, which are designed to accommodate EV charging hubs, thereby driving the need for faster internet connections.

- The rising adoption of smart factories, alongside connected systems like SCADA and IIoT, is spurring a heightened demand for high-speed internet connectivity in the region. This, in turn, is propelling the growth of the market under study. A case in point: in February 2024, the UK Research and Innovation's MSI Challenge, in collaboration with Innovate UK, the Engineering and Physical Sciences Research Council, and the Economic and Social Research Council, announced a grant of GBP 3.7 million (~USD 4.6 million) to bolster smart factory projects in the UK. Notably, as per GSMA, systems like automation and robotics mandate speeds exceeding 100 Mbps, with latency under 1 ms. Consequently, these systems necessitate a stable and robust high-speed internet connection, further bolstering the adoption of smart connected systems in manufacturing and, consequently, driving the Fixed Connectivity Market in the region.

- In November 2023, the UK government unveiled a GBP 960 million (USD 1.1 billion) investment aimed at bolstering the nation's data center infrastructure. This initiative is a pivotal part of the government's broader strategy to enhance the country's appeal to scale-up companies. With the UK data center market expanding, there is a parallel surge in the demand for high-speed internet connectivity, further propelling the sector's growth.

- For instance, in January 2024, Google announced a USD 1 billion investment in a new data center in Waltham Cross, Hertfordshire, United Kingdom. This move is set to bolster the country’s computational capabilities, underlining Google's push for AI innovation and improved digital services, not only for its UK users but for a global audience. The expansion of data centers is poised to bolster the fixed connectivity market.

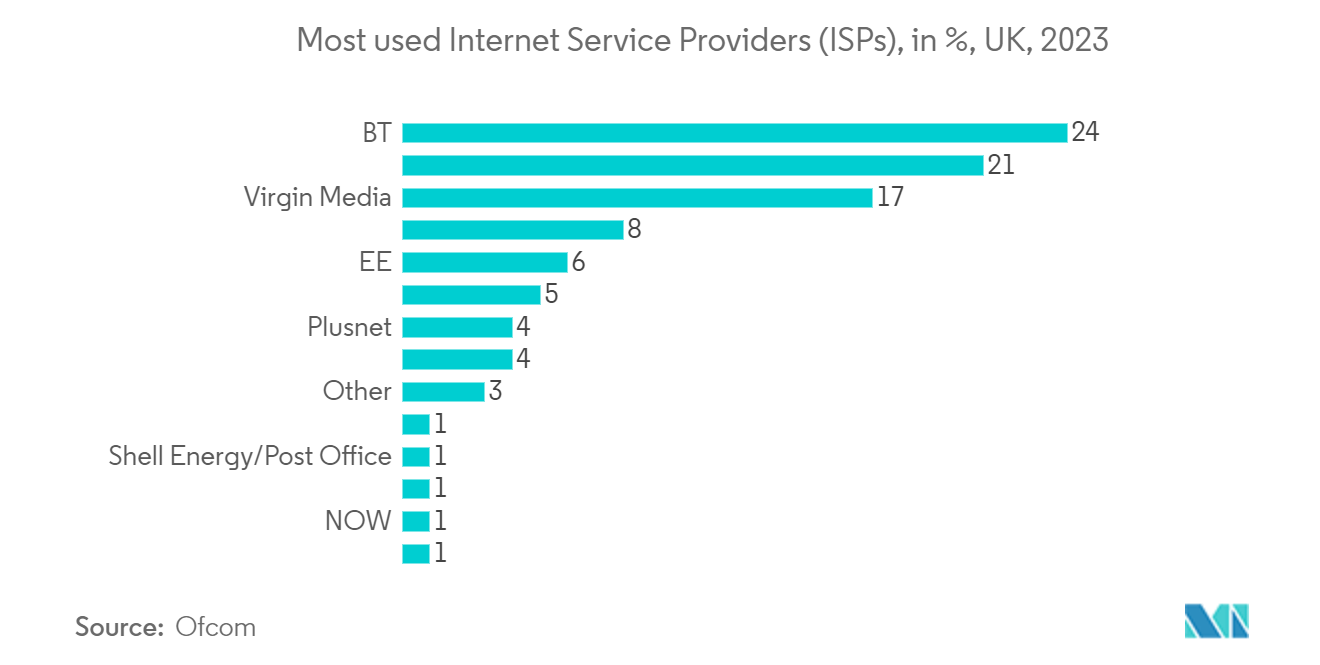

- Further, in 2023, BT held the top spot as the primary internet service provider for approximately 25% of UK households with internet access. Sky followed closely, serving as the main provider for 21% of respondents. Meanwhile, 17% of households favored Virgin Media. These insights were reported by Ofcom, the country’s official regulatory body overseeing broadcasting, telecommunications, and postal services.

UK B2B Fixed Connectivity Industry Overview

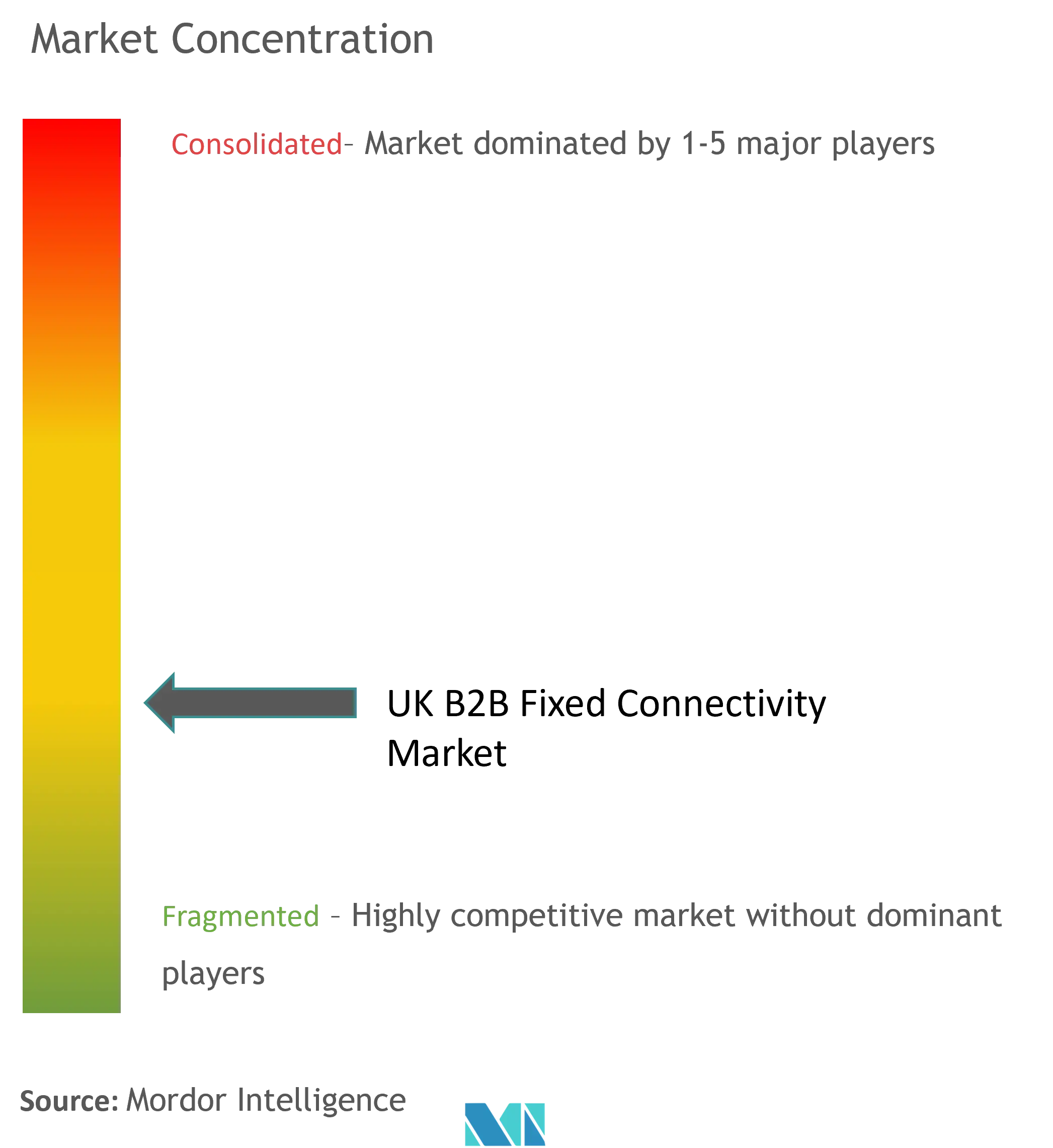

The UK B2B connectivity market is fragmented, with major players like Vodafone Limited, BT Group, Virgin Media Business Ltd, and XLN Telecom Ltd. Players in the market are adopting strategies such as partnerships, agreements, innovations, and acquisitions to enhance their service offerings and gain sustainable competitive advantage.

- February 2024: Virgin Media O2 (VMO2) in the United Kingdom, in collaboration with its major shareholders Liberty Global and Telefonica, unveiled intentions to establish a distinct national fixed network entity, NetCo. This strategic decision is geared toward bolstering the adoption of full-fiber technology, broadening financial avenues, and potentially paving the way for mergers with other network providers. NetCo, a freshly minted entity, will operate as a wholly-owned subsidiary of Virgin Media O2, consolidating the company's cable and fiber infrastructure, which spans around 16.2 million UK premises.

- February 2024: CityFibre, the largest altnet in the United Kingdom, secured five new contracts under the country’s GBP 5 billion (~USD 6.21 billion) broadband subsidy initiative, Project Gigabit. Valued at a cumulative GBP 394 million (~USD 490.04 million), these contracts aim to facilitate full-fiber deployment to 202,000 rural premises. The targeted regions include Buckinghamshire, Hertfordshire, Berkshire, Leicestershire, Warwickshire, Sussex, Kent, Bedfordshire, Northamptonshire, and Milton Keynes. Additionally, with the aid of CityFibre's funding, the company plans to not only expand but also enhance its current infrastructure in these areas, with a goal of reaching an additional 450,000 premises.

UK B2B Fixed Connectivity Market Leaders

-

Vodafone Limited

-

BT Group

-

Virgin Media Business Ltd

-

Sky UK Limited

-

KCOM Group Limited

*Disclaimer: Major Players sorted in no particular order

UK B2B Fixed Connectivity Market News

- May 2024: Openreach, a leading broadband infrastructure provider, announced its ambitious strategy. The plan entails extending full-fiber broadband services to 517 new locations across the United Kingdom, thereby introducing fiber-to-the-premise (FTTP) connections to an additional 2.7 million homes and businesses. Openreach's overarching goal is to ensure that 25 million properties in the country have access to gigabit-capable broadband by the close of 2026. This initiative, which includes reaching 6.2 million homes and businesses in rural and remote areas, comes with a hefty price tag of GBP 15 billion (~USD 18.65 billion).

- April 2024: Nokia and Vodafone joined forces to assess the potential of L4S technology over passive optical networks (PON). This technology has the potential to significantly enhance the online experiences of residential users, particularly in activities such as video conferencing and gaming. The pioneering demonstration occurred at Vodafone's lab in Newbury, United Kingdom, marking the world's first showcase of L4S over PON. The end-to-end network, crucial to this milestone, was exclusively powered by Nokia's cutting-edge technology.

UK B2B Fixed Connectivity Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definitions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Regulatory Landscape in UK for Telecom-related Services

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Huge Demand for High-speed Connectivity

5.1.2 Rising Digital Transformation in the Industries

5.2 Market Restraints

5.2.1 Data Securities and Privacy Concerns

5.2.2 Heavy CAPEX Associated with Advanced Telecom Infrastructure

5.3 Insights on Key Market Indicators Related to Business Fixed Connectivity in UK

5.4 Analysis of Pricing for Fiber and Fixed Broadband for Businesses in UK

5.5 Insights on Adoption of Fixed Leased Lines by Businesses in UK

6. MARKET SEGMENTATION

6.1 By Type

6.1.1 Fixed Data

6.1.2 Fixed Voice

6.2 By Size of Enterprises

6.2.1 Small and Medium-sized Enterprises (SMEs)

6.2.2 Large Enterprises

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 TalkTalk Business Direct Limited

7.1.2 Sky UK

7.1.3 Vodafone Limited

7.1.4 BT Group

7.1.5 Virgin Media Business Ltd

7.1.6 bOnline Limited

7.1.7 KCOM Group Limited

7.1.8 Hyperoptic Ltd

7.1.9 Gigaclear Ltd

7.1.10 XLN Telecom Ltd

7.1.11 Chess Ltd

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

UK B2B Fixed Connectivity Industry Segmentation

In a fixed-line network, two primary components stand out: the core network and the access network. The access network, which boasts nearly ubiquitous coverage, employs copper wires to link individual users to the broader network.

The scope of the report includes segmentation by type (fixed data and fixed voice) and size of enterprises (SMEs, large enterprises) in the United Kingdom. In addition, the report also covers country-specific market dynamics, ecosystem analysis, and evolution.

The report offers market sizes and forecasts in value (USD) for all the above segments.

| By Type | |

| Fixed Data | |

| Fixed Voice |

| By Size of Enterprises | |

| Small and Medium-sized Enterprises (SMEs) | |

| Large Enterprises |

UK B2B Fixed Connectivity Market Research FAQs

How big is the UK B2B Fixed Connectivity Market?

The UK B2B Fixed Connectivity Market size is expected to reach USD 2.74 billion in 2024 and grow at a CAGR of 5.25% to reach USD 3.38 billion by 2029.

What is the current UK B2B Fixed Connectivity Market size?

In 2024, the UK B2B Fixed Connectivity Market size is expected to reach USD 2.74 billion.

Who are the key players in UK B2B Fixed Connectivity Market?

Vodafone Limited, BT Group, Virgin Media Business Ltd, Sky UK Limited and KCOM Group Limited are the major companies operating in the UK B2B Fixed Connectivity Market.

What years does this UK B2B Fixed Connectivity Market cover, and what was the market size in 2023?

In 2023, the UK B2B Fixed Connectivity Market size was estimated at USD 2.60 billion. The report covers the UK B2B Fixed Connectivity Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the UK B2B Fixed Connectivity Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

UK B2B Fixed Connectivity Industry Report

Statistics for the 2024 UK B2B Fixed Connectivity market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. UK B2B Fixed Connectivity analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

UK B2B Fixed Connectivity Market Report Snapshots