UK Aviation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

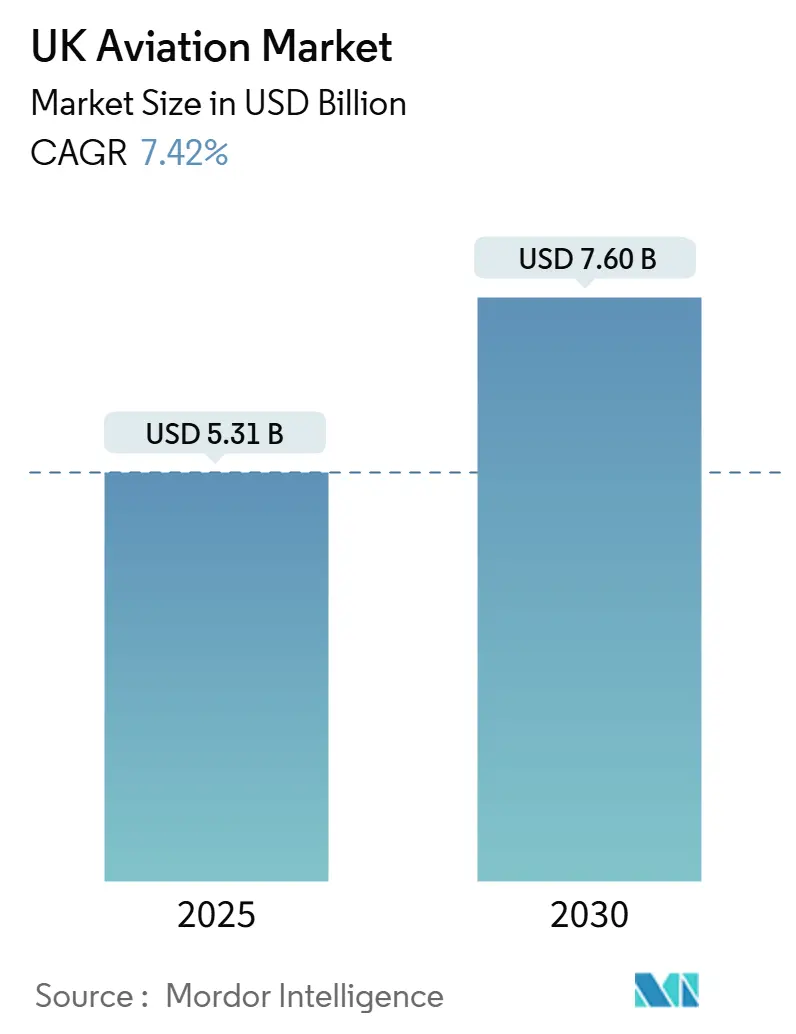

| Market Size (2025) | USD 5.31 Billion |

| Market Size (2030) | USD 7.60 Billion |

| Growth Rate (2025 - 2030) | 7.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Aviation Market Analysis by Mordor Intelligence

The UK aviation market size stands at USD 5.31 billion in 2025 and is forecasted to reach USD 7.60 billion by 2030, registering a 7.42% CAGR. Strong passenger demand recovery, rising defense orders, and a clear decarbonization pathway anchor this expansion. Sustainable aviation fuel (SAF) blending mandates, liberalized bilateral agreements, and renewed regional-airport investment add momentum, while fleet modernization supports lower fuel burn and asset utilization. Defense spending tied to the AUKUS and Tempest programs injects long-cycle revenue streams for domestic manufacturers, and new propulsion concepts attract sizable R&D funding. Capacity constraints at London hubs and persistent labor shortages remain headwinds, yet near-term demand elasticity in visiting-friends-and-relatives travel offsets these pressures.

Key Report Takeaways

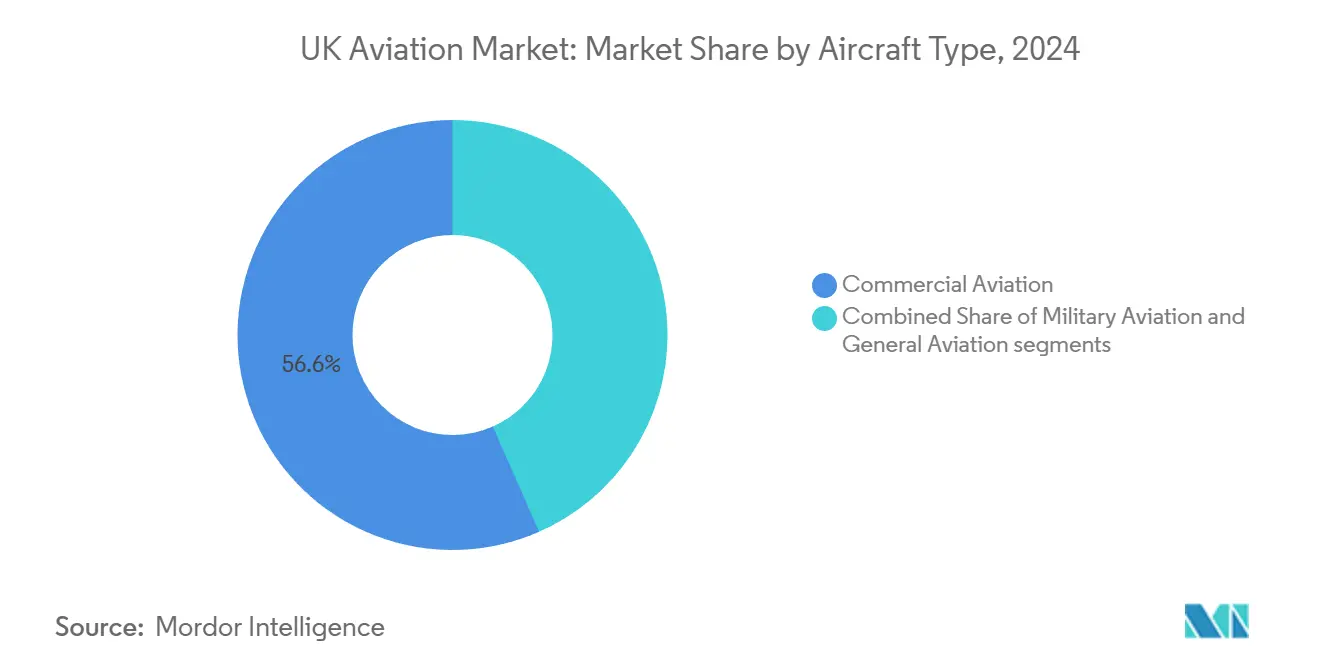

- By aircraft type, commercial aviation led with 56.60% of the UK aviation market share in 2024, whereas military aviation is projected to advance at the fastest 7.87% CAGR through 2030.

- By propulsion technology, turbofan engines accounted for 53.24% of the UK aviation market size in 2024, and turboshaft propulsion is set to expand at an 8.13% CAGR to 2030.

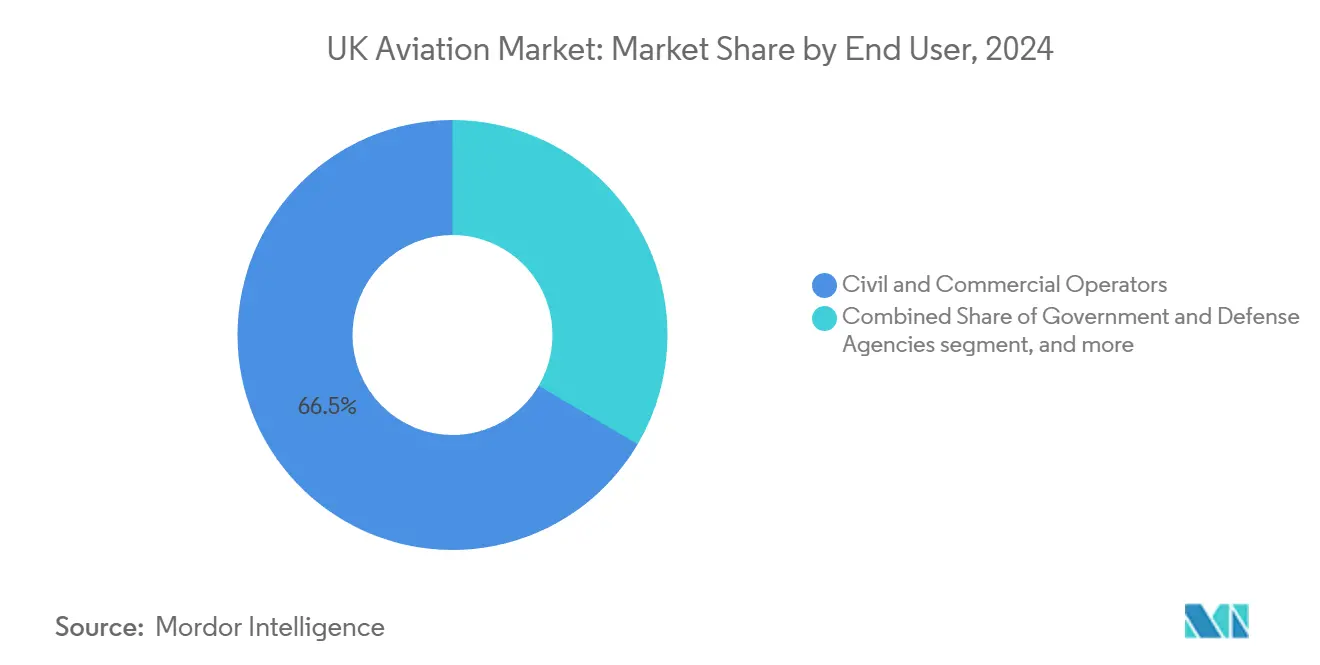

- By end user, civil and commercial operators held 66.52% revenue share in 2024, while government and defense agencies recorded the highest 7.78% CAGR over the forecast horizon.

UK Aviation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-mandated sustainable aviation fuel blending targets | +1.1% | Nationwide; strongest at London hubs and major regional stations | Medium term (2-4 years) |

| Liberalized air services agreements with non-EU countries post-Brexit | +0.9% | Heathrow, Manchester, Edinburgh long-haul corridors | Short term (≤ 2 years) |

| Rapid recovery in visiting friends and relatives (VFR) and discretionary travel demand | +1.3% | Diaspora-linked regional airports | Short term (≤ 2 years) |

| Expansion of regional airport infrastructure under the levelling-up agenda | +0.6% | Northern England, Scotland, Wales, Northern Ireland | Long term (≥ 4 years) |

| Military aviation recapitalization through AUKUS and Tempest programs | +1.0% | Manufacturing clusters in Lancashire, Yorkshire, Scotland | Long term (≥ 4 years) |

| Advancements in electric and hybrid-electric aviation technologies led by UK-based OEMs | +0.4% | R&D hubs in Bristol, Cambridge, Cranfield | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Mandated Sustainable Aviation Fuel Blending Targets

The government’s requirement that 10% of all jet fuel be SAF by 2030 is realigning capital across airlines, refiners, and airports.[1]Department for Transport, “Developing the UK Sustainable Aviation Fuel Mandate,” gov.uk Airlines are accelerating fleet renewal toward SAF-ready engines and lightweight airframes. British Airways is earmarking GBP 400 million (USD 533.73 million) for long-term offtake contracts, shielding its network planning from future carbon surcharges. Domestic refiners are scaling green-fuel capacity to cut import exposure and capture policy incentives. Airports are investing in on-site blending and hydrant upgrades that future-proof their fuel farms. The synchronized replacement cycle for narrowbody aircraft lets carriers align compliance spending with operating cost reduction. Once emissions-based slot pricing is introduced, early adopters gain slot flexibility in slot-constrained hubs.

Liberalized Air-Service Agreements Post-Brexit Unlock Routes

Bilateral open-sky deals with India, the US, and key Asia-Pacific states grant UK carriers extra frequencies and fifth-freedom rights.[2]Foreign, Commonwealth & Development Office, “UK-India Enhanced Trade Partnership,” gov.uk Virgin Atlantic exploited early rights by opening Austin and Tel Aviv services, beating EU rivals on time-to-market. Regional airports secure nonstop connectivity to high-yield markets, easing London hub congestion and diversifying inbound tourism flows. Freight operators gain preferential belly-hold and freighter rights on e-commerce lanes, strengthening UK export competitiveness. Airport operators are co-marketing new routes with local tourism boards, underpinning passenger volumes that de-risk terminal investments.

Military Aviation Recapitalization Through AUKUS and Tempest

AUKUS and Tempest represent a GBP 75 billion (USD 100.07 billion) multi-decade pipeline spanning design, production, and through-life support. BAE Systems leads the airframe and mission-system design, while Rolls-Royce plc supplies adaptive cycle engines built in Derby. The 25% UK content rule secures domestic employment and protects sovereign IP. Joint development with Italy and Japan widens export prospects and underwrites long production runs that lower unit costs. Adjacent investments in composite wings and additive manufacturing benefit civilian programs, tightening cross-sector learning loops. AUKUS submarine-technology offsets stimulate precision-machining supply chains that also serve aero-engine casings.

Rapid VFR Travel Recovery Reshapes Economics

VFR traffic surpassed 115% of the 2019 baseline in 2024 and is fueling robust load factors on Middle East, South Asia, and Eastern Europe routes from Manchester and Birmingham. Low-cost carriers (LCCs) redirect capacity to ethnic-diaspora city pairs where price elasticity is strong and seasonality differs from leisure peaks. Airports optimize immigration and retail layouts to accommodate family groups with longer dwell times. Airlines enjoy countercyclical revenue during downturns, stabilizing cash flow and supporting aircraft utilization rates that justify fleet upsizing.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National-level airport congestion limiting capacity expansion | -0.9% | London system with spillovers to regional feeders | Short term (≤ 2 years) |

| Shortage of skilled workforce across aviation maintenance and air traffic services | -0.7% | National; acute in Scotland, Northern England, Wales | Medium term (2-4 years) |

| Increasing air passenger duty reducing UK's competitiveness as a transit hub | -0.6% | London hubs; long-haul stations | Short term (≤ 2 years) |

| High production and adoption costs of sustainable aviation fuel impacting ticket prices | -0.5% | Nationwide; premium and long-haul cabins | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National-Level Airport Congestion Curbs Growth

Heathrow operates at 98% declared capacity, with peak-hour demand exceeding slot supply by 30%. Weather-induced spacing drops arrival rates to 40 hourly movements, cascading delays across Europe. Gatwick’s single-runway constraint persists as the Northern Runway plan awaits full planning approval. Airlines respond by up-gauging to larger aircraft, which squeezes frequency-based competition and limits new entrant access. The slot premium entrenches incumbent market power and raises barriers for innovative carriers targeting underserved routes.

Skilled-Workforce Shortages Threaten Scalability

The Civil Aviation Authority forecasts a 12,000-engineer shortfall in maintenance licensing by 2030. NATS trimmed peak-summer traffic flow by 15% in 2024 because controller headcount lagged roster requirements, eroding on-time performance. Apprenticeship levy rules have not generated sufficient enrolment; completion rates linger below 60% as graduates chase higher wages in renewables and rail. Regional airports struggle to attract technicians due to location and housing constraints, magnifying downtime risk. Airlines and MROs are adopting augmented-reality (AR) inspection tools and remote-sign-off processes to stretch existing labor, but admit throughput ceilings remain.

Segment Analysis

By Aircraft Type: Commercial Dominance with Accelerating Defense Demand

The commercial segment captured 56.60% of the UK aviation market share in 2024, reflecting its central role in passenger and cargo connectivity.[3]International Air Transport Association, “UK Aviation Economic Benefits Report,” iata.org Transatlantic seat capacity rebounded fastest as US corporate travel resumed and leisure travelers leveraged a strong pound against dollar-denominated ticket prices. Charter and cargo divisions locked in higher yields by balancing pharmaceutical, e-commerce, and perishables flows through Heathrow's dedicated freight lanes. Airlines prioritized cabin densification and Wi-Fi upgrades, monetizing ancillary revenue streams that cushion fuel-price volatility. Meanwhile, business-class refurbishments focused on privacy suites to recapture premium travelers lured by corporate-jet charters during the pandemic.

Military aviation is advancing at a 7.87% CAGR as Tempest prototypes transition from concept to flight test. The Ministry of Defence's (MoD's) pledge to allocate 2.50% of GDP to defense by 2030 guarantees budget headroom for air asset renewal, including tanker and ISR platforms needed for NATO taskings. Fleet commonality strategies favor shared avionics and propulsion across manned and uncrewed systems, extending supplier economies of scale. Export derivatives to Japan and Italy to broaden addressable volume, crowding in private finance for tier-2 suppliers. General aviation remains niche yet resilient, supporting offshore-energy shuttle flights and medical evacuation missions in remote Scottish islands. Regulatory emphasis on safety management systems raises operating costs but rewards operators able to scale audit compliance.

Note: Segment shares of all individual segments available upon report purchase

By Propulsion Technology: Turboshaft Outpaces in Growth

Turbofan engines represented 53.24% of the UK aviation market in 2024, sustained by wide-body and re-engined narrowbody deliveries.[4]Rolls-Royce, “Trent Engine Series Product Portfolio,” rolls-royce.com The Trent XWB and GEnx lead on fuel-burn, noise, and carbon indices, enabling airlines to meet CAA Stage 5 noise caps. Engine OEMs expand subscription-style total-care contracts that guarantee predictable shop-visit costs and harvest in-use data for digital twins. Turboshaft propulsion posts the highest 8.13% CAGR through 2030 as the Army upgrades Apache and Wildcat fleets. Leonardo’s Yeovil facility adds depot-level support capacity, anchoring lifetime value in the domestic aftermarket.

Piston and turboprop engines retain specialist roles in training, island-hopping, and freight feeder services. Their operators benefit from SAF compatibility retrofits that extend asset life without significant airframe changes. Electric-propulsion demonstrators such as Vertical Aerospace’s VX4 showcase zero-emission missions up to 100 miles, but certification frameworks and charging infrastructure need maturation before fleet deployment. Hybrid-electric architectures, blending gas-turbine range extenders with battery boost, are tipped for 19-seat commuter aircraft by the late decade, potentially displacing older turboprops on sub-400-mile routes.

By End User: Civil Stability and Defense Upside

Civil and commercial operators generated 66.52% of 2024 demand, supported by resilient e-commerce airfreight and pent-up leisure travel. Airlines rationalized fleets around the A320neo and B787 families, cutting seat-kilometer cost and aligning with SAF mandates. Cargo integrators expanded leased B777-200LR freighters to meet overnight parcel growth, while ACMI providers capitalized on seasonal imbalances. Digital ticket-distribution partnerships widened small-airport visibility, improving load factors on underserved routes.

Government and defense agencies are the fastest-growing buyers at a 7.78% CAGR, propelled by AUKUS-related maritime-patrol aircraft, Unmanned Aerial Vehicles (UAVs) swarms, and space-domain awareness assets. Accelerated procurement cycles favor spiral upgrades over monolithic programs, keeping budget outlays steady and smoothing supplier cash flows. The business and general aviation cohort responds to executive demand for door-to-door agility; UK-based corporations are reinstating fractional-ownership schemes to curb exposure to scheduled-flight disruptions. Sustainability pressures push owners toward SAF-ready cabins and flight-planning software that minimizes fuel and charges.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

London’s three airport systems—Heathrow, Gatwick, and Stansted—handle the majority of passenger and belly-hold freight, anchoring global network airlines and high-value corporate travel. Each new long-haul route at Heathrow contributes GBP 50 million (USD 66.39 million) in annual gross value added, illustrating the multiplier embedded in flag-carrier operations. Yet dependency on two-runway Heathrow and one-runway Gatwick constrains national capacity during weather or labor disruptions, as seen in summer 2022 when ATC staffing gaps forced 8% flight cancellations.

The Levelling-Up agenda is rebalancing flows. Manchester’s Terminal 2 expansion lifts airport throughput potential to 55 million passengers by 2030, spurring hotel and logistics development around Airport City. Edinburgh’s proposed second runway would enable nonstop West Coast-US links and capture higher-yield traffic from the finance and tech sectors. Cardiff and Belfast International leverage UK Export Finance guarantees to upgrade cargo aprons, positioning themselves as freighter reliever bases when London slots tighten. Regional gains diversify national resilience and attract MRO and training colleges that feed local employment.

Industrial geography mirrors aviation’s historical roots. Rolls-Royce’s Derby campus hosts civil-aerospace R&D, while Bristol anchors defense and space propulsion. Lancashire’s Warton and Samlesbury plants assemble prototype Tempest sections, clustering high-temperature composite suppliers within easy truck radius. Scotland’s Glasgow Prestwick corridor supports avionics and radar fabrication, leveraging university partnerships on artificial-intelligence flight-test instrumentation. These clusters concentrate know-how, cutting logistic lead times and reinforcing the UK aviation market as a cradle for advanced design and manufacturing.

Competitive Landscape

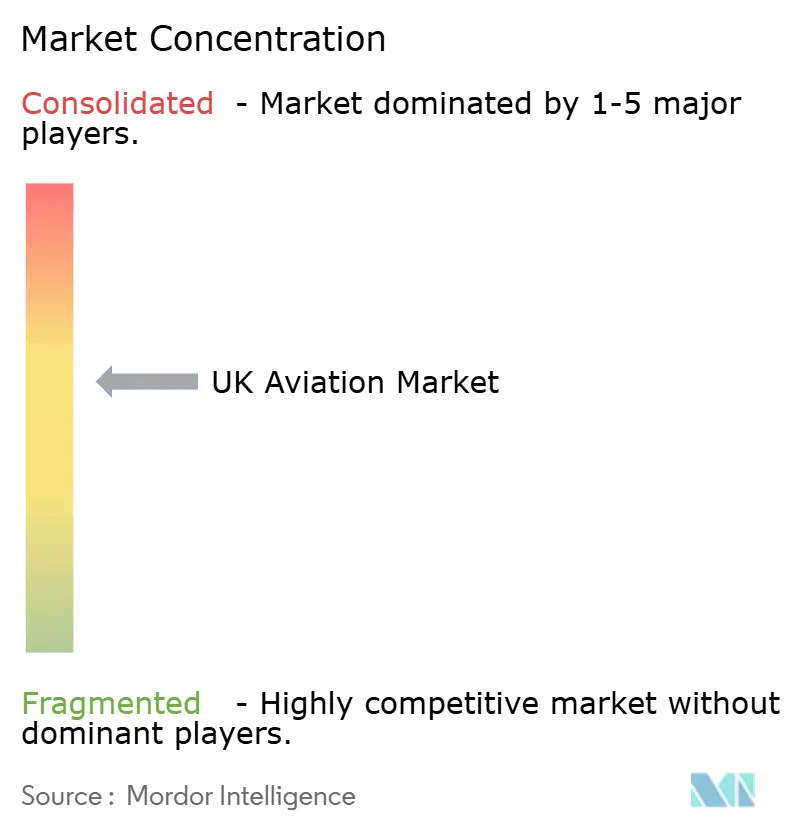

The UK aviation market shows moderate concentration: the combined revenue share of Airbus SE, BAE Systems plc, and Leonardo S.p.A. holds a significant market share, granting bargaining power without blocking newcomer innovation. BAE Systems plc leverages its electronic-warfare expertise to secure the Tempest mission-system prime and a GBP 4.2 billion (USD 5.60 billion) radar contract extension. GKN Aerospace partners with Airbus SE on hydrogen fuel cell wing integration, extending its composite-spar leadership into zero-carbon architectures.

Reaction Engines explores precooler technology for hypersonic and high-altitude platforms, potentially disrupting traditional turbofan performance envelopes. Engine MRO independents like StandardAero invest in big-data prognostics to compete with OEM in-house shops. Regulatory catalysts, like CAA’s carbon-pricing roadmap, reward incumbents that bundle hardware with predictive maintenance and SAF-sourcing guidance, while late adopters risk margin squeeze.

Tier-2 suppliers face consolidation pressure. Precision-machining shops in Midlands aerospace alley weigh robotics investment against uncertain order books; some choose to merge to reach scale thresholds needed to bid on Tempest work packages. Digital supply chain mandates force SMEs to adopt PLM and blockchain traceability, raising capex but unlocking access to higher-margin defense offsets. Players who integrate design, build, and sustainment services maintain a strategic advantage as operators pursue lifecycle-cost certainty.

UK Aviation Industry Leaders

Airbus SE

BAE Systems plc

The Boeing Company

Lockheed Martin Corporation

Leonardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The UK and The Boeing Company formed a partnership to manufacture surveillance aircraft for the United States Air Force, with the contract expected to generate more than GBP 36 million (USD 48.04 million) for the UK economy.

- April 2024: Defence Equipment & Support awarded a GBP 122 million (USD 162.84 million) contract for six Airbus H145 helicopters to provide aviation support for UK military forces.

- December 2022: The US Army announced a contract to supply next-generation helicopters to Textron Inc.'s Bell unit. The Army's "Future Vertical Lift" competition aimed at finding a replacement as the Army looks to retire more than 2,000 medium-class UH-60 Black Hawk utility helicopters.

UK Aviation Market Report Scope

Commercial Aviation, General Aviation, Military Aviation are covered as segments by Aircraft Type.| Commercial Aviation | Passenger Aircraft | Narrowbody Aircraft |

| Widebody Aircraft | ||

| Regional Jets | ||

| General Aviation | Business Jets | Large Jet |

| Mid-Size Jet | ||

| Light Jet | ||

| Piston and Turboprop Aircraft | ||

| Commercial Helicopters | ||

| Military Aviation | Fixed-Wing Aircraft | Combat Aircraft |

| Multi-Role Aircraft | ||

| Transport Aircraft | ||

| Training Aircraft | ||

| Rotorcraft | Multi-Mission Helicopter | |

| Transport Helicopter | ||

| Others | ||

| Turboprop |

| Turbofan |

| Piston Engine |

| Turboshaft |

| Others |

| Civil and Commercial Operators |

| Government and Defense Agencies |

| Business and General Aviation Owners |

| By Aircraft Type | Commercial Aviation | Passenger Aircraft | Narrowbody Aircraft |

| Widebody Aircraft | |||

| Regional Jets | |||

| General Aviation | Business Jets | Large Jet | |

| Mid-Size Jet | |||

| Light Jet | |||

| Piston and Turboprop Aircraft | |||

| Commercial Helicopters | |||

| Military Aviation | Fixed-Wing Aircraft | Combat Aircraft | |

| Multi-Role Aircraft | |||

| Transport Aircraft | |||

| Training Aircraft | |||

| Rotorcraft | Multi-Mission Helicopter | ||

| Transport Helicopter | |||

| Others | |||

| By Propulsion Technology | Turboprop | ||

| Turbofan | |||

| Piston Engine | |||

| Turboshaft | |||

| Others | |||

| By End User | Civil and Commercial Operators | ||

| Government and Defense Agencies | |||

| Business and General Aviation Owners | |||

Market Definition

- Aircraft Type - All the aircraft related to commercial, military and general aviation have been included in this study

- Sub-Aircraft Type - Fixed-Wing passenger aircraft, freighter aircraft, business jets, piston fixed-wing aircraft, military fixed-wing aircraft, and rotorcraft are included under this study.

- Body Type - Body type includes all types of aircraft segmented based on application/size/capacity/role.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms