Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

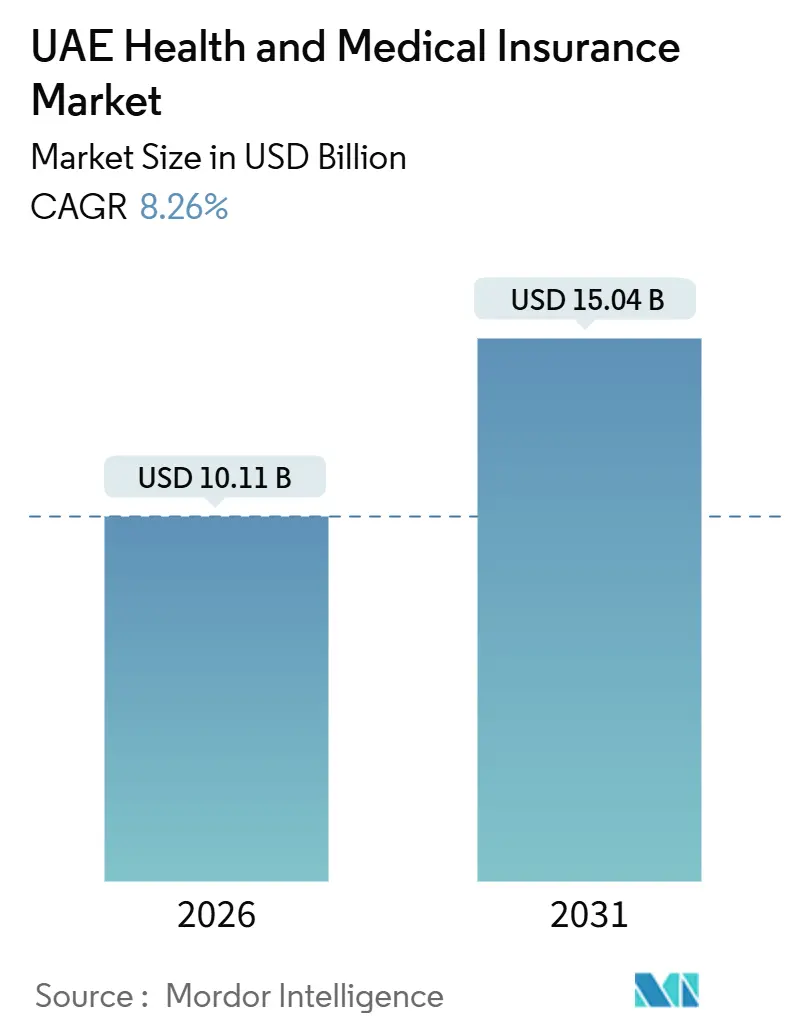

| Market Size (2026) | USD 10.11 Billion |

| Market Size (2031) | USD 15.04 Billion |

| Growth Rate (2026 - 2031) | 8.26% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Health And Medical Insurance Market Analysis by Mordor Intelligence

The UAE health and medical insurance market size is USD 10.11 billion in 2026 and is forecasted to reach USD 15.04 billion by 2031, registering an 8.26% CAGR over the forecast period. Macro forces underpinning growth include the UAE's expatriate-dominated demography - where 10.04 million of the 11.35 million residents (88.5%) are foreign nationals as of mid-2025 - creating persistent demand for employer-funded group schemes[1]GMI Research Team, “UNITED ARAB EMIRATES (UAE) POPULATION STATISTICS 2025,” GMI Research Team, www.globalmediainsight.com. The system links health insurance compliance with residency procedures, which raises coverage adherence for employees and dependents under emirate-specific rules and visa processing requirements. Digital rails are improving data liquidity and care coordination, led by Abu Dhabi’s Malaffi health information exchange that connects all hospitals and a large network of clinics and clinicians, which enables payers to strengthen adjudication and utilization management.

Key Report Takeaways

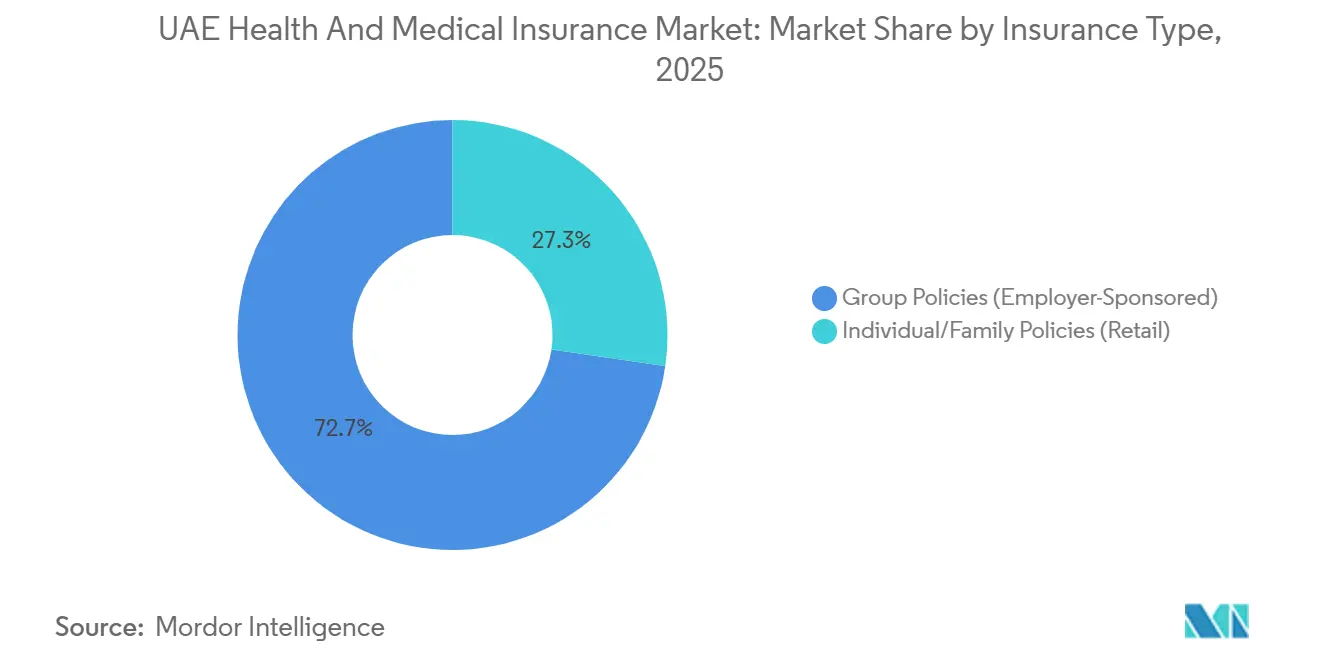

- By insurance type, group policies led the UAE Health and Medical Insurance Market with a 72.69% market share in 2025, while individual and family coverage are projected to expand at a 10.22% CAGR through 2031.

- By service provider, private insurers dominated the UAE Health and Medical Insurance Market with a 92.64% share in 2025, and the segment is forecasted to grow at a 9.45% CAGR through 2031.

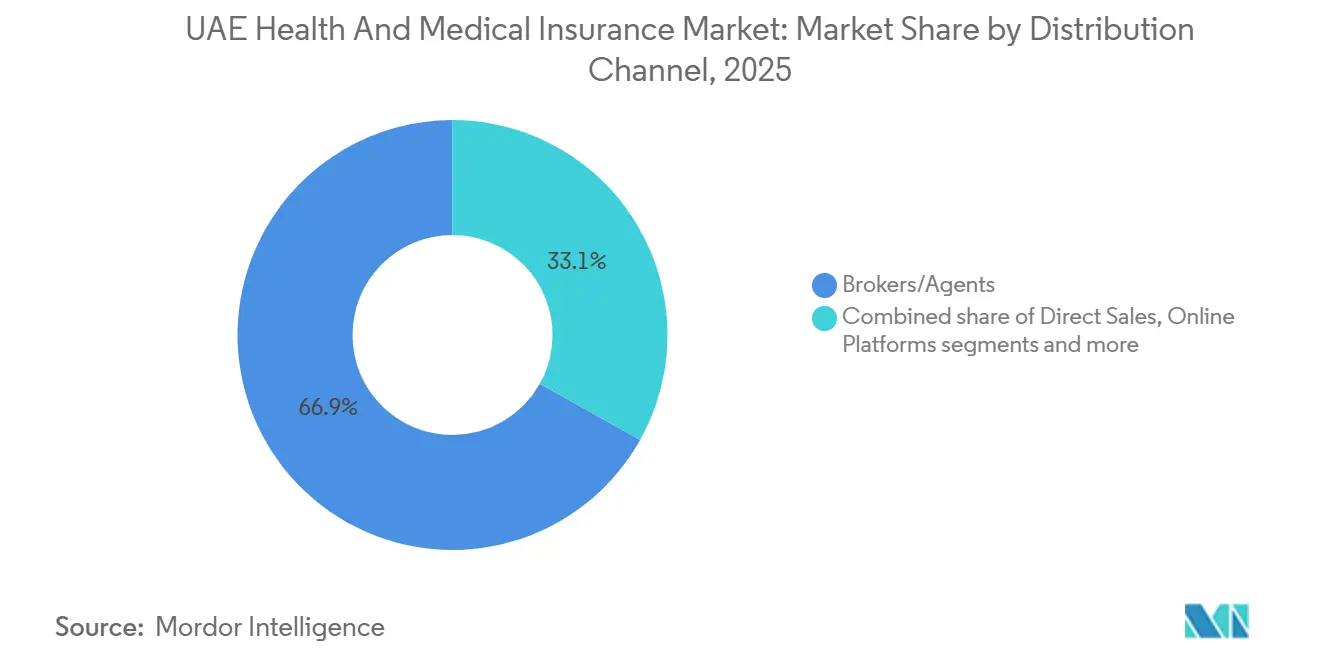

- By distribution channel, brokers and agents held a 66.89% share of the UAE Health and Medical Insurance Market in 2025, while online platforms are expected to record the highest growth at a 13.87% CAGR through 2031.

- By coverage mandate, mandatory policies commanded an 86.22% share of the UAE Health and Medical Insurance Market in 2025, while voluntary plans are projected to post an 11.82% CAGR through 2031.

- By geography, Dubai accounted for a 58.75% share of the UAE Health and Medical Insurance Market in 2025, while the Northern Emirates are projected to expand at a 9.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Health And Medical Insurance Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compulsory Health Coverage Enforcement Across All Emirates | +2.8% | National, with early gains in Sharjah, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain | Short term (≤ 2 years) |

| Growing Expatriate Population and Employer-Sponsored Schemes | +1.9% | National, concentrated in Dubai and Abu Dhabi, spills over to the Northern Emirates. | Medium term (2-4 years) |

| Digital Health Ecosystem Integration Driving Product Innovation | +1.4% | National, led by Abu Dhabi platforms | Medium term (2-4 years) |

| Medical Inflation Outpacing GDP and Lifting Premium Volumes | +2.1% | National, acute in large private provider markets | Long term (≥ 4 years) |

| Post-COVID-19 Rise of Sharia-Compliant Takaful Health Products | +0.8% | National, stronger in Abu Dhabi, Dubai, and Sharjah | Medium term (2-4 years) |

| Shift Toward Preventive-Wellness Riders and Chronic Disease Management | +0.6% | National, led by Dubai and Abu Dhabi, is expanding to the Northern Emirates. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Compulsory Health Coverage Enforcement Across All Emirates

The nationwide mandate, effective January 1, 2025, requires employers to fund health insurance for private sector staff and domestic workers and sets a basic package at AED 320 (USD 87.11) per year with no waiting period for chronic diseases, which removes entry barriers and moves large cohorts into insured status under a single compliance framework[2]Ministry of Human Resources and Emiratisation, “The Basic Health Insurance Scheme,” MOHRE, mohre.gov.ae. Because residency procedures require proof of valid coverage at issuance and renewal, the policy strengthens adherence and elevates the baseline of insured lives across visa-linked workforce segments. The combination of a low-cost basic plan and enforcement via immigration processes has created a predictable on-ramp for employer enrollment that supports premium stability and systematic coverage inclusion across emirates. Payers can now calibrate distribution and network strategy at a national scale, while aligning underwriting models to standardized plan features and co-pays defined by public authorities. As claims utilization increases under broader access, market participants monitor loss experience and leverage official claims data to refine pricing and benefit design over the forecast horizon.

Growing Expatriate Population and Employer-Sponsored Schemes

Employer obligations to provide coverage tie directly to work permits and residency rules in key emirates, which structurally favors group plans and keeps employee coverage at the center of underwriting volumes in the UAE health and medical insurance market. In Abu Dhabi, the official basic plan framework is administered through Daman and aligns with policies that extend to family members under specific eligibility criteria, which raises per‑policy values compared to single‑employee plans. Formal compliance pathways for employee and dependent benefits sustain the commercial pool and support continuity in renewals as insurers build retention programs around employer groups. Healthy macro conditions reinforce labor market resilience and corporate activity, which supports paid memberships and underwriting scale in the current period. As coverage expands in the Northern Emirates under the national mandate, employer‑sponsored schemes are positioned to remain the dominant source of risk pooling and premium flows in the UAE health and medical insurance market.

Digital Health Ecosystem Integration Driving Product Innovation

Abu Dhabi’s Malaffi has achieved full hospital connectivity and links a large roster of clinics and clinicians, enabling payers to access longitudinal medical data that enhances adjudication, target setting, and fraud control in the UAE health and medical insurance market. Abu Dhabi's Malaffi health information exchange, operational since its 2018 launch, connects hospitals and clinics - 1,539 facilities serving 39,600 clinicians - holding records from 98% of patient episodes and facilitating payer access to longitudinal data for risk stratification[3]Fourrage, Ludo, “The Complete Guide to Using AI in the Healthcare Industry in the United Arab Emirates in 2025,” Fourrage, Ludo, www.nucamp.co. The digitization of claims and electronic health information is improving validation cycles and reducing manual rework, which supports faster settlement and better provider contract enforcement at scale. Leading carriers are augmenting these rails by deploying advanced analytics for pricing and anomaly detection, illustrated by GIG Gulf’s Eagle Eye initiatives that embed generative AI into core decision-making. Digital identity and app-based services are becoming standard in product experiences, with insurers in the UAE integrating teleconsultations and streamlined verification to simplify onboarding and improve patient journeys. With continued platform investments and public-private data interoperability, digital-first distribution and claims management are set to capture an increasing share of new issuance and renewals.

Medical Inflation Outpacing GDP and Lifting Premium Volumes

Gross medical cost trends in the UAE are forecasted to escalate 11.3% in 2026, driven by the proliferation of high-cost cancer and cardiovascular treatments, overutilization of diagnostic services, and imported pharmaceutical inflation exacerbated by currency headwinds[4]WTW, “2026 Global Medical Trends Survey,” WTW, www.wtwco.com. Macroeconomic projections for headline inflation remain contained, which amplifies the relative weight of healthcare cost trends in benefit design and underwriting. Regulators have progressively refined minimum plan parameters and claims frameworks, which raises the need for insurers to calibrate benefit structures, provider networks, and authorization rules to stabilize loss ratios. In practice, carrier strategies combine product tiering, digital utilization management, and deeper provider collaboration to keep margins within target ranges during a period of higher claims velocity. As the claims base grows with broader inclusion of insured lives under the national mandate, continuous actuarial review and network optimization remain central to pricing responses.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price‑Regulated Essential Plans Compressing Underwriting Margins | -0.9% | National, pronounced in Dubai and Abu Dhabi, spills‑over to the Northern Emirates. | Medium term (2-4 years) |

| High Fraud & Abuse Incidence Inflating Loss Ratios | -0.7% | National, higher in dense private provider markets | Medium term (2-4 years) |

| Fragmented Provider Billing Systems Hindering Cost Control | -0.5% | National, acute in the Northern Emirates, with lower digital maturity | Medium term (2-4 years) |

| Frequent Regulatory Revisions Raising Compliance Costs | -0.4% | National, centralized at CBUAE, with emirate-specific rules | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Regulated Essential Plans Compressing Underwriting Margins

Essential and basic plan frameworks in the UAE set defined minimum benefits and pricing guardrails that ensure affordability for low‑income employees and dependents, which compresses underwriting spread on mandatory tiers in the UAE health and medical insurance market. In Abu Dhabi, the official basic plan administered by Daman is positioned to maintain access and includes structured co‑pays and limits across inpatient and outpatient services, which requires carriers to balance plan compliance with loss experience. As national coverage extends to all seven emirates, insurers are managing the profit dynamics of essential plans by relying on operational efficiency and claims discipline rather than price expansion on regulated tiers. Pricing and benefit changes trigger mid‑cycle updates to policy administration and provider contracting, which adds administrative cost during transition periods and tightens room for underwriting cushions. The net effect puts a premium on scale, analytics, and network quality to keep combined ratios resilient within the regulated essential plan segment of the UAE health and medical insurance market.

Frequent Regulatory Revisions Raising Compliance Costs

A new federal insurance law introduced in September 2025 consolidated supervision and increased enforcement powers for the Central Bank of the UAE, which elevates compliance expectations and reshapes licensing and control frameworks for insurers and intermediaries. Emirate‑level health authorities continue to refine claims and coding rules to accommodate digital care modalities and new service definitions, which require timely updates to policy wording and claims engines. The cumulative effect of federal and emirate‑specific revisions raises one‑time system upgrade costs and ongoing audit requirements, which are more burdensome for smaller carriers relative to scaled incumbents in the UAE health and medical insurance market. Compliance also intersects with distribution realignment and direct payment traceability, which requires internal policy changes and tighter controls across finance, operations, and broker management. As rule changes stabilize, the market is expected to benefit from improved transparency and stronger policyholder protections supported by uniform oversight.

Segment Analysis

By Insurance Type: Group Policies Anchor Employer Mandates, While Individual Plans Tap Digital Natives

Group policies held a 72.69% market share in 2025, remaining the primary segment under employer-paid coverage rules. Individual and family policies are projected to grow at a 10.22% CAGR through 2031 in the UAE health and medical insurance market. Health insurance compliance tied to visa issuance drives demand for employer-sponsored schemes, ensuring steady group policy renewals. In Abu Dhabi, family coverage requirements under the basic plan increase per-contract values for employer groups insuring employees and dependents within regulatory thresholds, strengthening the group segment. The nationwide health insurance mandate, implemented in 2025, expands access for workers and households in the Northern Emirates, enhancing group risk pooling. Improved data integration from connected health systems and stricter claims regulations boost underwriting confidence for group plans, despite rising claims volumes due to broader coverage.

The retail segment benefits from app-based processes and integrated identity verification, simplifying policy issuance. Teleconsultations and electronic prescriptions enhance perceived value for policyholders. Specialized products, including Sharia-compliant options, support retail demand as consumers seek personalized plans beyond basic compliance coverage. Strengthened online distribution enables retail insurers to optimize pricing, reduce underwriting turnaround times, and improve accessibility across income groups. Regulatory frameworks ensure standardized benefits at the base level and diverse add-on modules at higher tiers, supporting segment expansion within a stable compliance-driven environment.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Service Provider: Private Insurers Command Market as Public Schemes Serve Citizens

Private carriers held 92.64% of premiums in 2025 and are expected to grow at a 9.45% CAGR through 2031, underscoring their central role in plan design, network contracting, and claims execution. Public and social programs, covering citizens and specific employee groups, operate outside the commercial pool, setting complementary guardrails rather than shaping the premium base. Daman, a government-linked insurer in Abu Dhabi, anchors official plan administration and provider integration for state-funded and basic coverage, influencing private market practices in benefit design and claims governance. Scale advantages enable private insurers to invest in analytics, automation, and compliance readiness, which are critical under tighter federal oversight. Digital advancements allow private insurers to differentiate through service quality and preventive care features while meeting mandatory coverage requirements.

Company results highlight the private segment's strength and focus on core capabilities. PureHealth’s expansion of Daman into property and casualty insurance in June 2025 diversifies its portfolio, balancing health line volatility while maintaining strong provider relationships. Carriers are also upgrading fraud prevention, pricing, and network analytics, as seen in GIG Gulf’s technology initiatives for pricing precision and claims oversight. These efforts enhance the competitive positioning of private insurers, which leads the UAE health and medical insurance market in underwriting capacity and digital sophistication.

By Distribution Channel: Brokers Retain Lead as Digital Platforms Disrupt with Speed

Brokers and agents dominated 66.89% of the distribution in 2025, driven by their role in managing employer plans and regulatory compliance across the Emirates. Stricter federal supervision has led insurers to align payment processes and documentation with direct settlement standards, improving transparency. Direct channels and bancassurance remain key for cross-selling to existing customers and corporate clients seeking bundled financial solutions. Online platforms are projected to grow at a 13.87% CAGR through 2031, supported by automated underwriting and telehealth integration. Investments in straight-through processing and identity verification are expanding digital distribution, catering to individual buyers and small businesses seeking transparent pricing and quick policy issuance.

Insurers are enhancing omni-channel capabilities, combining broker expertise for group programs with digital solutions for retail and SME segments. Platforms now streamline policy issuance, claims, and member services, reducing administrative tasks and improving cycle times. Public platforms like Malaffi enhance interoperability and enable automated checks, expediting claims and reducing errors. Digital engagement supports preventive care, offering wellness and chronic condition management as optional riders in online plans. Industry recognition for digital execution validates strategies prioritizing customer experience and innovation. The combination of broker expertise and digital efficiency is expected to shape distribution trends in the UAE health and medical insurance market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Coverage Mandate: Mandatory Policies Dominate as Voluntary Riders Gain Traction

Mandatory coverage constituted 86.22% of the market in 2025, driven by regulations linking insurance to visa issuance and residency. The federal basic scheme, priced at AED 320 (USD 87.11) for eligible workers, established a uniform coverage baseline across the Northern Emirates under centralized administration. In Abu Dhabi, Daman’s platform implemented basic plan parameters, enhancing predictability for co-pays and benefit limits. Insurers are aligning products, claims processes, and provider contracts to maintain margins under essential plan rules while preparing to offer additional riders and enhanced benefits. With enforcement tied to immigration controls and emirate-specific regulations, the mandatory segment remains the primary allocator of insured lives and claims volumes in the UAE health and medical insurance market.

Voluntary policies are expected to grow at an 11.82% CAGR through 2031, as households seek services beyond essential plans, including broader maternity, dental, and international coverage. Insurers differentiate voluntary tiers with wellness benefits, teleconsultations, and worldwide assistance for frequent travelers or expatriates. Sharia-compliant options are expanding within supplemental coverage, supported by improved governance standards and positive performance by specialized providers. Takaful Emarat, for example, achieved revenue growth and profitability restoration in 2025 through a restructured portfolio. Voluntary demand is anticipated to align with rising expectations for preventive care, chronic disease management, and cross-border healthcare access in the UAE health and medical insurance market.

Geography Analysis

Dubai held a 58.75% market share in 2025, reflecting mature mandatory coverage adoption and a robust private provider ecosystem supporting enhanced plan tiers. The emirate’s scale enables carriers to offer products from essential benefits to premium international tiers, with digital claims and provider connectivity improving efficiency. Investments in pricing analytics and fraud detection enhance service quality and resolution speed, key to competitive differentiation. Regulatory continuity and documentation standards ensure sustained coverage adherence, supporting stable renewals. Broader national regulations since 2025 position Dubai as a leader in premium pools and digital utilization management within the UAE health and medical insurance market.

Abu Dhabi accounted for a significant share of insured lives and premiums, supported by integrated governance of plan administration, provider networks, and data exchange through Malaffi. Its basic plan framework ensures consistent benefit delivery and member services, with clear co-pay and limit guidelines, maintaining pricing discipline. Updated claims and adjudication rules accommodate telehealth and evolving modalities, standardizing processes for carriers and providers. Public oversight and connected health data strengthen fraud prevention and care management analytics. Regulatory stability allows carriers to refine plan tiers and provider arrangements, supporting long-term quality and cost outcomes in the UAE health and medical insurance market.

The Northern Emirates are projected to grow at a 9.96% CAGR through 2031, driven by the nationwide mandate and expanded formal coverage, including domestic staff. First-time enrollees entering under a unified compliance framework prompt insurers to develop cost-effective products and regional networks. The addition of essential benefits is expected to increase claims in general practice and outpatient services, requiring strong claims governance and provider management. Digital claims processing and payer-provider data integration can replicate efficiencies seen in Abu Dhabi and Dubai, advancing standardized processes and member experiences. Regulatory clarity and digital maturity position this region to expand its role in the UAE health and medical insurance market.

Competitive Landscape

Leading private players dominate the market, leveraging advantages in underwriting, reinsurance, and digital investments. Daman’s expansion into property and casualty (P&C) lines diversified its revenue streams and demonstrated a broader approach to multi-line risk management under PureHealth’s integrated platform. ADNIC’s strong growth and profitability in H1 2025, supported by regional expansion and a strengthened balance sheet, enabled it to address compliance and pricing challenges. Sukoon’s robust Q3 2025 earnings and solvency highlighted its ability to invest in customer experience and process automation amidst regulatory changes. Competitive dynamics are driven by premium scale, provider contracts, and digital execution, streamlining quoting, onboarding, and claims management.

Technology adoption differentiates market players as insurers integrate AI and analytics into pricing, fraud detection, and care management workflows. GIG Gulf piloted generative AI tools to enhance pricing accuracy and identify anomaly patterns, enabling faster and more precise decision-making. Daman’s partnership with AXA Global Healthcare expanded international private medical insurance options for corporate groups, offering improved portability and global access through a unified customer experience. Public digital infrastructure, such as Malaffi, facilitates data sharing between payers and providers, strengthening alignment on clinical episodes and enabling efficient pre-authorization processes. Awards and recognitions reflect the sector’s shift toward digital innovation and customer-centricity, with leading insurers recognized for product development and service quality. Scale and digital capabilities are critical for achieving sustainable competitive advantages.

Mergers, acquisitions, and portfolio repositioning enhance capital efficiency and expand product offerings. ADNIC’s acquisition of a 51% stake in a Saudi carrier positively impacted its performance. Daman’s entry into P&C lines aims to mitigate health line volatility by diversifying its underwriting portfolio. Sukoon’s acquisition of a UAE life insurance portfolio supported its diversification strategy and created cross-selling opportunities. Takaful Emarat’s turnaround demonstrated the effectiveness of focused operating models aligned with Sharia governance and investments in digital capabilities. Federal oversight and licensing reforms raised compliance and governance standards, favoring well-capitalized incumbents capable of scaling technology investments. These factors sustain competitive intensity while reinforcing the strengths of market leaders combining robust balance sheets with advanced digital capabilities.

UAE Health And Medical Insurance Industry Leaders

Daman

GIG Gulf (formerly AXA Gulf)

Abu Dhabi National Insurance Company (ADNIC)

Sukoon Insurance (formerly Oman Insurance Company)

MetLife

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Takaful Emarat reported a successful business turnaround with insurance revenue up 51% year-on-year to AED 444.4 million (USD 121.0 million) and a return to profitability with AED 22.8 million (USD 6.2 million) income before tax for the nine months ending 30 September 2025.

- June 2025: PureHealth announced that its insurance arm, Daman, has expanded from a health-focused provider into the high-growth Property and Casualty (P&C) insurance segment, adopting the new legal name The National Insurance Company – Daman to reflect its broader insurance scope.

- June 2025: Sukoon’s Accident & Health Insurance product was recognised as “Best New Digital Insurance Product” at the Global Brand Awards 2025, highlighting its advancements in digital insurance solutions and integration with digital platforms.

- April 2025: Abu Dhabi National Insurance Company (ADNIC) completed the acquisition of a 51% stake in Allianz Saudi Fransi Cooperative Insurance Company - now renamed Mutakamela Insurance Company - expanding its regional footprint and strengthening its position in the Saudi insurance market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the UAE health and medical insurance market as all gross written premiums generated by private and public schemes that reimburse inpatient, outpatient, pharmaceutical, and preventive medical expenses for UAE residents and eligible visitors.

Scope exclusion: travel insurance sold solely for outbound trips is left outside this analysis.

Segmentation Overview

- By Insurance Type

- Individual/Family Policies (Retail)

- Group Policies (Employer-Sponsored)

- By Service Provider

- Private Health Insurance Providers

- Public/Social Health Insurance Schemes

- By Distribution Channel

- Direct Sales

- Online Platforms

- Brokers/Agents

- Banks (Bancassurance)

- By Coverage Mandate

- Mandatory Coverage

- Voluntary/Supplemental Coverage

- By Geography

- Dubai

- Abu Dhabi

- Northern Emirates (Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah, Fujairah)

Detailed Research Methodology and Data Validation

Primary Research

We interviewed underwriting heads at national insurers, third-party administrators in Dubai and Abu Dhabi, large employers, and licensed brokers across the Northern Emirates. These conversations tested desk-derived assumptions on average premium per member, utilization ratios, and likely impacts of the new mandatory cover for domestic workers.

Desk Research

Analysts began with Ministry of Health & Prevention yearbooks, Central Bank solvency statistics, and Dubai Health Authority tariff filings, which clarify premium pools and claims costs. We layered in population and expatriate data from the Federal Competitiveness & Statistics Centre, medical inflation indices from the World Bank, and policy counts published by the Insurance Authority. Company filings, insurer annual reports, and reputable media such as Gulf News added color on pricing shifts and product launches. Paid portals, notably D&B Hoovers for carrier financials and Dow Jones Factiva for deal tracking, provided depth. This list is illustrative; many additional public and subscription sources informed the desk phase.

A follow-up scan of academic journals, Emirates Insurance Association white papers, and patent databases (Questel for digital-health platforms) helped verify technology uptake and cost-containment trends.

Market-Sizing & Forecasting

Mordor's model marries a top-down reconstruction of gross written premiums, starting from regulator-reported sector totals and adjusting for self-insurance pools, with bottom-up sense-checks on sampled average premium times covered lives. Key drivers include (i) resident and expatriate headcount, (ii) employer compliance rates, (iii) average premium escalation linked to medical inflation, (iv) claims loss ratios, and (v) uptake of digital distribution. A multivariate regression, using premium growth as the dependent variable and the above indicators plus GDP per capita as predictors, anchors the 2025-2030 forecast. Where carrier data were patchy, sampled broker books and TPA claim files filled the gaps before reconciliation.

Data Validation & Update Cycle

Outputs pass a three-layer review: analyst, senior peer, and domain lead, before sign-off. Models refresh every twelve months, with interim revisions triggered by material regulatory or macro events to ensure clients receive the latest view.

Why Mordor's UAE Health and Medical Insurance Baseline commands reliability

Published market estimates often diverge because firms pick different premium definitions, include distinct customer cohorts, or refresh at uneven intervals.

Key gap drivers here are whether expatriate dependents are counted, whether figures capture earned or written premiums, and how aggressively medical inflation is projected beyond 2027.

Mordor reports gross written premiums for all mandatory and voluntary plans and updates assumptions annually, whereas some publishers rely on older hospital billing surveys or apply fixed escalation factors.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.34 B (2025) | Mordor Intelligence | - |

| USD 8.72 B (2024) | Global Consultancy A | Excludes dependents on employer plans; older base year |

| USD 8.00 B (2024) | Regional Analyst B | Uses earned premiums, not written; limited broker sampling |

| USD 10.03 B (2025) | Trade Journal C | Assumes uniform 10% premium hike; no loss-ratio cross-check |

In sum, by combining regulator data, granular primary inputs, and annual refreshes, Mordor delivers a balanced, transparent baseline that executives can trace back to clearly stated variables and repeatable steps.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the UAE health and medical insurance market?

The UAE health and medical insurance market size is USD 10.11 billion in 2026 and is projected to reach USD 15.04 billion by 2031 at an 8.26% CAGR, supported by nationwide mandatory coverage and rising claims intensity.

How does the nationwide mandate affect coverage and compliance in the UAE?

From January 2025, employers must fund health insurance for eligible private sector workers and domestic staff under a defined basic package priced at AED 320, with coverage linked to visa issuance and renewal to enforce compliance.

Which segment leads distribution in the UAE health and medical insurance market, and what is growing fastest?

Brokers and agents lead with a 66.89% share due to their role in corporate schemes, while online platforms record the fastest growth with a projected 13.87% CAGR through 2031 as digital issuance and telehealth features expand.

How are digital platforms and data exchanges shaping insurer operations?

Abu Dhabi’s Malaffi connects hospitals and clinics to payers, improving adjudication, fraud controls, and claims cycle speed, while carriers invest in AI for pricing and anomaly detection to strengthen performance.

What role do voluntary plans play alongside mandatory coverage?

Voluntary plans are projected to grow at 11.82% CAGR to 2031 as households add riders for maternity, dental, wellness, and international portability that extend benefits beyond essential plan requirements.

Which recent strategic moves by leading insurers are notable in the UAE?

Daman expanded into property and casualty lines to diversify income, ADNIC accelerated growth supported by regional acquisition, and GIG Gulf piloted generative AI tools for pricing and fraud detection.